It’s Silly Stock Season

At NewEdge Wealth, our investing philosophy values productive and profitable assets purchased at reasonable prices. As we’ll show in this piece, sticking to investments with these “high quality” attributes has historically been associated with higher returns over time. Over the shorter term, however, we know that just about anything can drive markets.

Enter “silly stocks”. The past several weeks have featured meteoric rises in the stock prices of many companies with little to no hope of developing a sustained business model but are, for whatever reason, attractive to investors looking for a laugh or a thrill. To take one example, OpenDoor, a non-profitable online home purchase company, saw its stock increase by as much as 500% before it began to lose some air. More broadly, Goldman Sachs Research has identified a noticeable uptick in speculative investor behavior, eclipsed only by the bubbles that formed in the late 1990s and briefly in 2021.

The randomness and absurdity of aspects of this market environment at times calls to mind one of the classic Monty Python sketches: the Ministry of Silly Walks. In it, John Cleese (in a performance that belongs on the Mount Rushmore of physical comedy with Charlie Chaplin and Buster Keaton) plays a British minister charged with assigning grants and patents to people with…well…silly walks.

The “Silly Walks” sketch only works because of how seriously all the actors are committed to the bit. We are less sure that many investors truly want to hold stocks like Krispy Kreme, Beyond Meat, and GoPro for the long run. However, we are interested in what’s causing the Silly Stock phenomenon and how to navigate through it as we try to help investors seek to achieve optimal risk-adjusted outcomes.

What’s been driving equity markets to all-time highs?

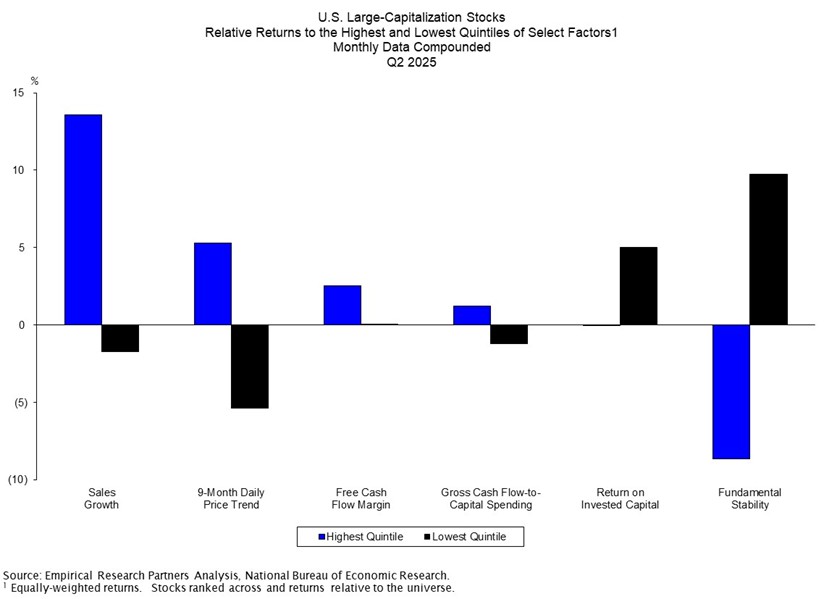

If they haven’t already, investors are about to begin examining their second quarter financial statements, and they may see a familiar pattern in their U.S. equity portfolios. Indexes heavy in large high-growth companies, especially in Tech, performed exceedingly well. Everything else lagged from April’s bottom. More precisely, Q2’s outperformers tended to have high sales growth and strong momentum. Those with stable earnings and high returns on invested capital (ROIC) were less likely to be rewarded.

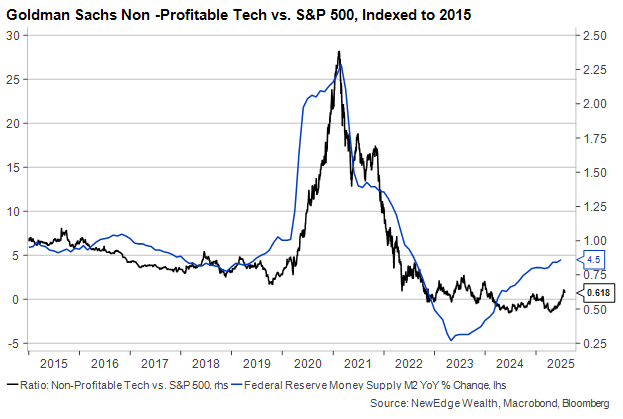

In other words, low-quality companies – those with high leverage, poor profitability, or otherwise nondurable business models – outperformed higher quality companies in the second quarter and have led major indexes back to all-time highs in July. Goldman Sachs’ Non-Profitable Tech Index is a good proxy for this phenomenon. This graph shows its wild trip in 2025 compared to the S&P 500 Index:

Of course, not all unprofitable companies are “silly” in the way that most in the meme stock category undoubtedly are. Many of these newer technology firms have the potential to become profitable, even industry-changing, in the future. But today, they are behaving like silly stocks. Their lack of positive free cash flow makes them difficult to value, and their fad-like attraction causes them to routinely rise and fall by 20% or more in a single, otherwise uneventful, trading session.

Why have “Silly Stocks” been doing so well?

We define “silly stocks” as those with high valuations built on dubious growth potential, making them highly dependent on capital markets financing while returning little capital to shareholders. They tend to thrive in low volatility environments characterized by ample – and sometimes surplus – financial market liquidity.

On the low volatility front, the S&P 500 Volatility Index (VIX) has been below 25 for three months after peaking at more than double that in early April. The S&P 500 has not risen or fallen by more than 1% in a single day in over a month. Compared to economists’ and investors’ worst fears, the macro picture has remained relatively solid – if a bit weaker – since the initial onrush of U.S. import taxes. Note the tight relationship between the betting odds on a 2025 recession and the S&P 500. The mere reduction in recession risk has been good enough for stocks to move higher.

A ripple-free market can often hide violent and broad rotations under the surface, but it can also be a breeding ground for investor fads, as it was in late 2020 and early 2021. Strategas Research estimates that positioning in high beta stocks (those with higher volatility than the market) is as crowded as it’s ever been, while Renaissance Macro notes that the relative performance of high beta stocks is now in the 99th percentile (meaning there are very few times in history where beta has performed better than it has recently). Overall market positioning was extremely light at the April bottom, and we have seen it normalize back towards neutral (the Deutsche Bank Consolidated Equity Positioning Index is now in the 44th percentile) as investors have rushed back into stocks – especially risky stocks – for fear of watching this leg of the bull market pass them by.

“I think that with Government backing I could make it very silly” – More Liquidity on the Way?

While impressive, the current Silly Stock rally pales in comparison to the one at the end of the pandemic. That environment’s defining financial characteristic was the unprecedented surge in liquidity. We saw this in many places in the data, most obviously the bulging budget deficits in 2020 and 2021 as Congress used direct fiscal stimulus to support the partly shuttered economy.

Monetary policy was decisive in the quick stock market recovery in 2020, and the size and persistence of Fed liquidity injections had the unintended effect of supporting less profitable companies as well as cryptocurrencies, which are correlated with changes in financial market conditions:

We’re obviously not currently in anything like the liquidity environment of 2020 and 2021. Monetary policy is not as restrictive as it was two years ago, at least judging from the recovery in money supply (M2) growth. But nominal GDP growth has slowed from more than a 10% pace throughout most of 2021 to a barely 4% pace today, and home prices are in decline across the country, rather than rising at a 20%+ clip like they were in 2021.

Still, liquidity should remain “ample” for now given the Fed’s winddown of Quantitative Tightening and the potential for policy rate cuts soon. Fiscal policy is also set to loosen in 2026 as import tax increases are offset by stimulus from the One Big Beautiful Bill Act (OBBBA). The wall that Silly Stocks slammed into at the end of 2021 is not in sight at the moment.

“You’re really interested in silly walks, aren’t you?” – Why we aren’t buying Silly Stocks

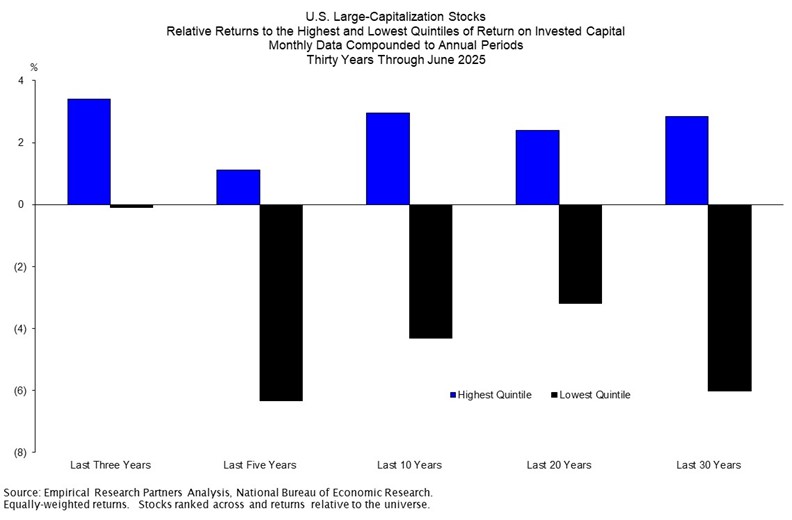

It may be tempting for investors, particularly those who are still not fully allocated to equities, to jump into Silly Stocks and “catch up” to the market. As we said above, while the conditions are not in place for anything like a full resumption of the 2021 rally, non-fundamental market trends can last far longer than fundamental analysts expect. Even so, we are sticking to our core philosophy on long-term investing. Factors that signal higher quality companies (e.g., ROIC) have a demonstrated track record of producing outperformance in equity strategies over all time horizons. And the chart below suggests that it is at least as important to limit Low Quality firms as it is to include High Quality firms in a portfolio:

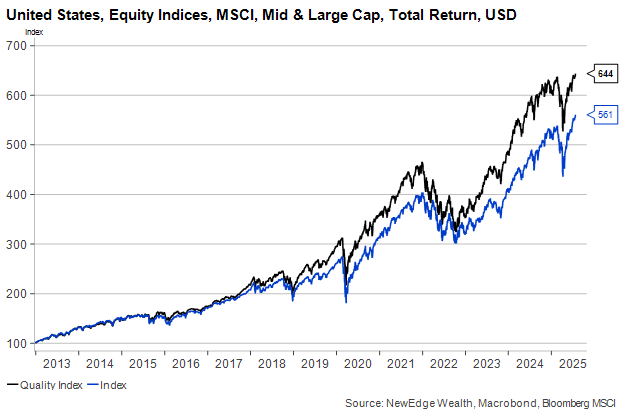

Low quality stocks may outperform over short periods of time but have a history of “giving up” that outperformance over the long-term. Low-quality stocks generally add to portfolio volatility while detracting from overall returns, a rather unappealing combination for any long-term investor. MSCI’s Quality Factor portfolio uses a different methodology than the Empirical chart above, but it produces a similar long-term picture. Profitable companies with low volatility and low leverage have historically shown a steady and enduring run of outperformance, one that we believe is likely to continue:

We still have concerns about the weaker macro environment as growth seems set to remain lackluster in the coming quarters. Valuations are not a good predictor of near-term market performance, but the similarities between the current market and 2021 also remind us of how quickly that bull market came to an end.

The second quarter saw good returns across global equity markets but underperformance among many active managers who tilt their portfolios toward tried-and-true investment styles like low valuation and high quality. We see today as a good moment for investors to consider rebalancing their portfolios back toward these styles as market leadership can – and has – change rapidly in a highly uncertain macro environment.

IMPORTANT DISCLOSURES

The views and opinions included in these materials belong to their author and do not necessarily reflect the views and opinions of NewEdge Capital Group, LLC.

This information is general in nature and has been prepared solely for informational and educational purposes and does not constitute an offer or a recommendation to buy or sell any particular security or to adopt any specific investment strategy.

NewEdge and its affiliates do not render advice on legal, tax and/or tax accounting matters. You should consult your personal tax and/or legal advisor to learn about any potential tax or other implications that may result from acting on a particular recommendation.

The trademarks and service marks contained herein are the property of their respective owners. Unless otherwise specifically indicated, all information with respect to any third party not affiliated with NewEdge has been provided by, and is the sole responsibility of, such third party and has not been independently verified by NewEdge, its affiliates or any other independent third party. No representation is given with respect to its accuracy or completeness, and such information and opinions may change without notice.

Investing involves risk, including possible loss of principal. Past performance is no guarantee of future results.

Any forward-looking statements or forecasts are based on assumptions and actual results are expected to vary from any such statements or forecasts. No assurance can be given that investment objectives or target returns will be achieved. Future returns may be higher or lower than the estimates presented herein.

An investment cannot be made directly in an index. Indices are unmanaged and have no fees or expenses. You can obtain information about many indices online at a variety of sources including: https://www.sec.gov/answers/indices.htm.

All data is subject to change without notice.

© 2026 NewEdge Capital Group, LLC