One of the coolest bits of trivia from the intense and infamous recording of Fleetwood Mac’s 1977 album, Rumors, is how the acoustic guitar track on “Never Going Back Again” was recorded.

In order to maintain the bright and crisp sound of Lindsay Buckingham’s picking and pinching, his guitar was restrung every 20 minutes during the recording. Though these resets were tedious for the guitar tech, the result is a spritely sound that a Rolling Stone critic at the time said, “belies the bad-news subject matter” (which of course was Buckingham’s tumultuous, stop-and-go relationship with Stevie Nicks).

This Classic Albums lore of how restrings and resets can help belie bad news reminds us of calls for large rate cuts from the Fed, acting as an attempt to restring or reset the U.S. economic cycle and belie any bad news that comes from potentially growth-dampening policies like tariffs or immigration.

This week’s Edge will look at the calls for big rate cuts given today’s inflation backdrop, whether policy makers are “never going back again” to 2% inflation goals, how the Fed’s dual mandate is currently in a duel that we call “Stagflation Lite”, and how tariffs could impact corporate profitability and thus economic growth.

“Come Down and See Me Again”: Calls for Cuts Despite Inflation

Earlier in the week, Treasury Secretary Bessent argued on Bloomberg’s Surveillance that the Fed Funds rate should be 150-175 bps lower based on “any model”. Bessent is not alone in calls for rates to be cut meaningfully from current levels, with a chorus line of auditionees for the Fed Chair position arguing for swift and meaningful rate cuts to begin as soon as September (you can almost hear them sing “I Hope I Get It”).

Bloomberg’s John Authers called this assertion that “any model” is pointing to such large rate cuts “breathtaking” as he asked, “Where is Bessent pulling these rate models from?” In his article, Authers shows that many models, such as the Taylor Rule, point for rates to actually be higher (to be clear, we are not making that argument!), and notes that if the Fed were to cut by 175 bps, the Fed Funds rate would be the lowest it has ever been in the last 70 years when inflation was this high (with a core reading above 3%).

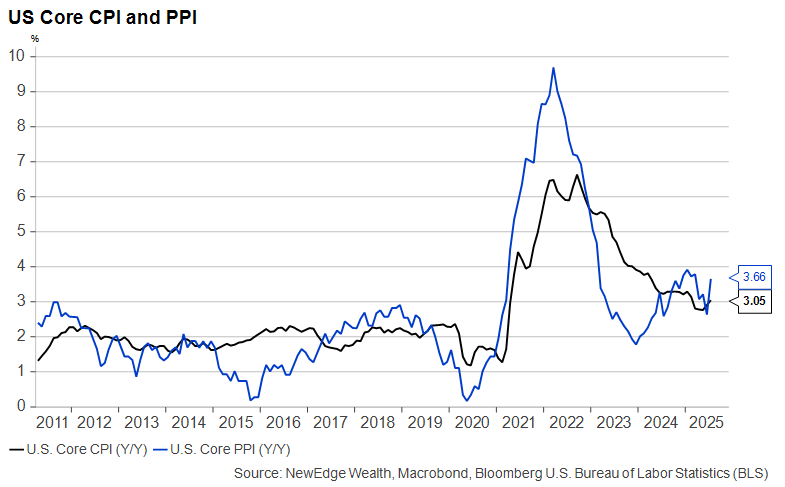

Calls for such large rate cuts while inflation remains sticky and even accelerating above the Fed’s 2% target, as seen in this week’s CPI and PPI data (with the latter showing its largest one-month jump since 2021 as tariff impacts work their way through supply chains), has caused many to posit that policy makers are effectively singing along with Buckingham, saying they’re “never going back again” to that 2% target.

The implications of a quiet or explicit abandonment of the Fed’s 2% target are a topic of healthy debate that is likely to evolve as the Fed begins to cut rates in this sticky inflation backdrop.

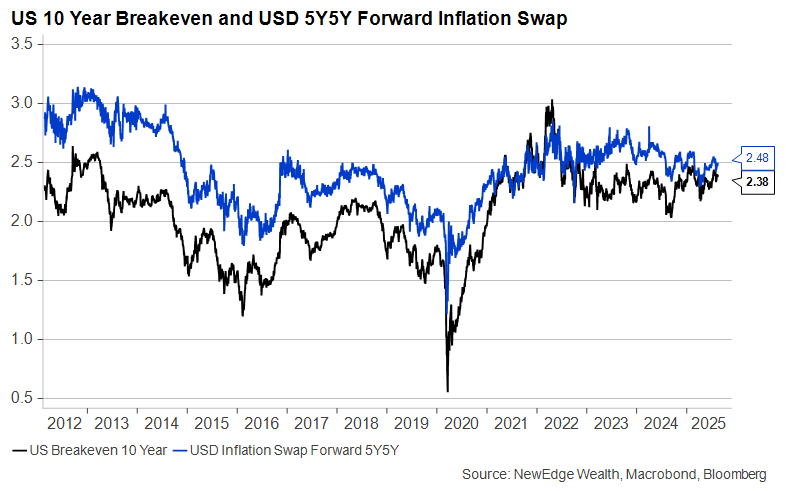

One important impact would likely be on long-term yields, as higher long-run inflation expectations would put upward pressure on these yields. However, at this time, bond markets do not seem all too concerned about a potential target abandonment, as seen in the chart below that shows longer-term inflation breakevens and swaps remaining anchored and within recent ranges.

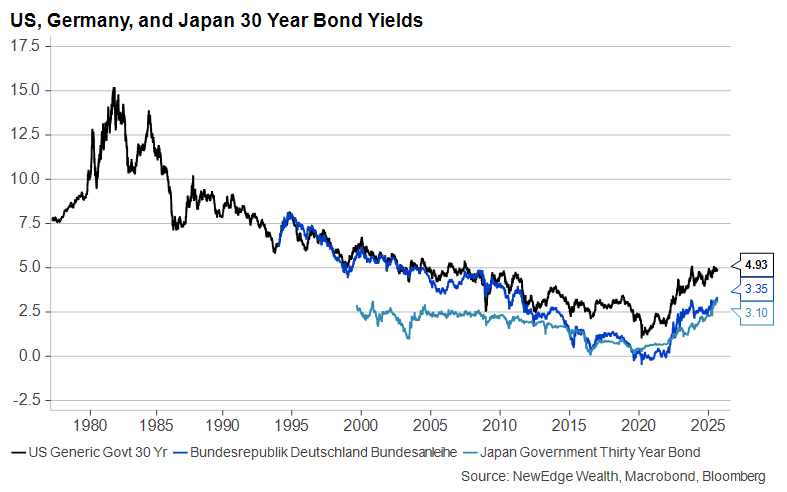

Where we are seeing more “spicy” price action is in 30-year yields around the globe, which are likely reflecting these concerns about stickier long-run inflation in addition to global debt and deficit concerns (which we frame in this recent piece about bond market supply and demand).

It is hard to make the argument that today’s inflation levels or the near-term trajectory of inflation are supportive of the 150-175 bps of rate cuts that some are urging, but, of course, the Fed does not just consider inflation in its policy decision making, it also must balance the outlook for employment, which brings us to the duel.

“Made Me See Where I’ve Been”: Dueling Dual Mandate, Stagflation Lite

The Fed has a dual mandate: price stability and full employment. Based on recent data, the components of this dual mandate appear to be locked in somewhat a duel, where inflation is remaining sticky but growth is slowing.

Real GDP growth in 2025 is forecasted to run at half the pace of 2023 and 2024, while the pace of job additions has slowed materially, all the while, as we profiled above, the progress on disinflation has stalled and there are signs of a reacceleration in inflation.

Said another way, inflation isn’t cool enough that the Fed can solely focus on employment, while employment is not weak enough that the Fed can ignore stickier inflation.

The Fed has said that it intends to view tariff-related inflation as (gasp!) transitory, which means, at the margin, they are likely to prioritize employment in their policy decisions. The challenge in this is that it is hard to argue that Fed rate levels are the cause of recent employment weakness. After all, the real fed funds rate is 100 bps lower than it was last year, and broad financial conditions remain in easy/stimulative territory.

Instead, the source of weaker growth appears to be related to policy uncertainty and policy impacts from pursuits like tariffs and immigration. As Peter Boockvar outlined this week, “The Fed can’t fix tariffs!”.

We have been calling this period “Stagflation Lite: Doesn’t Taste Great, Less Filling”, as the combination of sticky inflation and slower growth has hints of stagflation flavor (like your favorite watery lite beer) but is not quite the “Stagflation Heavy” scenario experienced in the 1970s of soaring inflation and rapidly rising unemployment.

The question is how the current and future Fed will navigate this “Staglation Lite” backdrop and which one of the dual mandates will win the duel. Will the Fed be forced to be patient because of much higher inflation (even if they view it as transitory), or will they need to step in and stabilize growth because of a further deterioration in employment?

This question brings us to our last topic: margins.

“You Don’t Know What it Means to Win”: Tariff Impacts on Corporate Margins

Much like beauty, the question about who is paying these tariff taxes has been in the eye of the beholder (those in support of tariffs argue that the cost will be born by exporters and will have less impact on US businesses and consumers).

But as tariff revenue is now running at a rate of well over $300B a year, we are starting to get clearer signs of who is bearing the brunt of the costs thus far.

As seen in July’s import price data, we are not seeing broad evidence that exporters are carrying the weight of tariffs (you would expect to see import prices fall if exporters were cutting their prices in order to offset tariffs). July’s CPI data also showed limited signs that tariff taxes were being passed through to consumers through higher prices. This means that, at least for now, the majority of the cost of tariffs is likely being born by US corporates and could eventually be a headwind to margins.

It was fascinating that in the Bloomberg Bessent interview, the Treasury Secretary expressed hope that exporters would bear some of the cost (again, the data is not supporting this notion yet) but acceptance that U.S. corporates could bear the costs and see their margins “return to normal” after getting “very fat during COVID.”

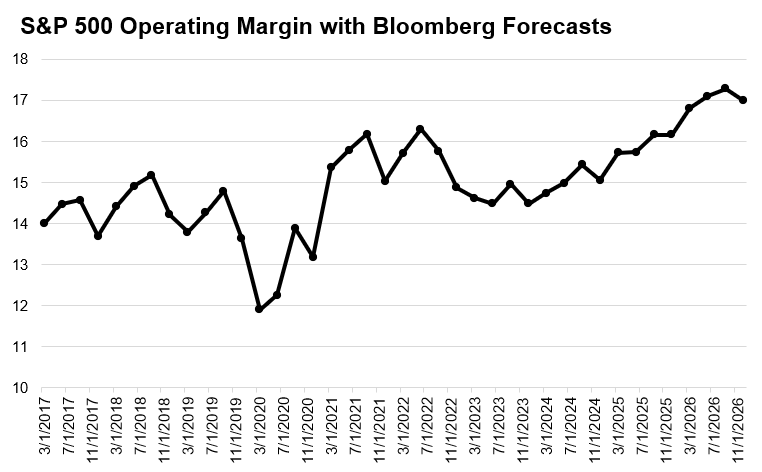

This all stands in contrast to the lofty expectations for corporate margin expansion that are currently being baked into S&P 500 earnings estimates. The chart below shows that the current consensus has margins returning to their 2022 peak in 2025 and pressing to new highs in 2026.

In a world where input costs are going higher thanks to tariffs but pricing power remains soft thanks to a stretched consumer, the achievement of these margin goals will be highly dependent on productivity-enhancing decisions, which can include the application of technologies like AI, but could also include headcount reductions and capital spending austerity.

The biggest question facing economy and market watchers in the coming quarters is whether or not companies will look to defend margins by reducing headcount or pulling back on capital spending. Both of these decisions, if pursued broadly, could weigh on the US economic growth outlook and result in renewed volatility for financial markets.

Conclusion

It is unclear if a restring and resetting of the interest rate policy will be effective at helping the U.S. economy “belie the bad news” of slower growth that has been in motion for 2025. The impact of tariffs on inflation, corporate margins, and corporate cost-saving decisions will be important watch items for U.S. equity markets, which have shown their own incredible ability to “belie bad news” and remain in strong uptrends.

IMPORTANT DISCLOSURES

The views and opinions included in these materials belong to their author and do not necessarily reflect the views and opinions of NewEdge Capital Group, LLC.

This information is general in nature and has been prepared solely for informational and educational purposes and does not constitute an offer or a recommendation to buy or sell any particular security or to adopt any specific investment strategy.

NewEdge and its affiliates do not render advice on legal, tax and/or tax accounting matters. You should consult your personal tax and/or legal advisor to learn about any potential tax or other implications that may result from acting on a particular recommendation.

The trademarks and service marks contained herein are the property of their respective owners. Unless otherwise specifically indicated, all information with respect to any third party not affiliated with NewEdge has been provided by, and is the sole responsibility of, such third party and has not been independently verified by NewEdge, its affiliates or any other independent third party. No representation is given with respect to its accuracy or completeness, and such information and opinions may change without notice.

Investing involves risk, including possible loss of principal. Past performance is no guarantee of future results.

Any forward-looking statements or forecasts are based on assumptions and actual results are expected to vary from any such statements or forecasts. No assurance can be given that investment objectives or target returns will be achieved. Future returns may be higher or lower than the estimates presented herein.

An investment cannot be made directly in an index. Indices are unmanaged and have no fees or expenses. You can obtain information about many indices online at a variety of sources including: https://www.sec.gov/answers/indices.htm.

All data is subject to change without notice.

© 2026 NewEdge Capital Group, LLC