AI’s Impact on Markets, Adoption Trends, Hyperscaler Capex, and the Path to Return on Investment

“If you build it, he will come” is a message heard throughout the 1989 baseball classic Field of Dreams. While it has been nearly four decades since its release, the film’s key messages of the power of dreams, confidence, and purpose, offer notable parallels to the current state of the AI ecosystem. In particular, today’s massive capital investment in the infrastructure to support the expected demand for this generational technology.

Artificial Intelligence technology has shown remarkable progress since ChatGPT’s revolutionary large language model burst onto the scene in late 2022, and its evolution has generated impressive returns for many companies viewed as the largest near-term beneficiaries. However, this stellar performance, combined with a slow pace of AI adoption and monetization by end customers, has also raised questions about rich valuations and potential overinvestment. There are also concerns about the long-term impacts of job displacement on the economy. These doubts, like those attached to all secular trends, can lead to occasional bursts of volatility as we saw this week.

Ultimately, like any new technological wave, time will tell if continued confidence and patience in the AI ecosystem is the right strategy. However, understanding the trends beneath the surface may provide some assurance for investors who are wondering if they should, like Ray Kinsella, “go the distance” or shift their focus within equities to more reasonably valued and possibly less crowded areas. In our view, there is merit to being a long-term investor in portions of the AI ecosystem, but we would prioritize companies supported by underlying fundamentals. We also continue to strongly believe that diversification across regions, styles, and market capitalization is warranted from a risk management perspective, especially in the event these “AI dreams” fail to materialize.

Key Takeaways:

- It is hard to overstate the impact AI has had on U.S. equity markets over the past several years, driving multiple expansion, index concentration, and generating the lion’s share of market performance.

- While we believe we are still in the early innings of the evolution of AI, optimism around its long-term impact has led to bubble-like conditions in certain areas, and as a result, would focus on diversification and prioritize names supported by underlying fundamentals.

- Adoption trends and compute demand look promising, however, continued progress will be key to justifying today’s massive capital outlays from the big four hyperscalers and to supporting premium growth rates, valuations, and healthy returns on investment for this group.

- While the economic impacts of AI adoption have been modest thus far (aside from the significant economic boost of AI infrastructure development), continued adoption will likely contribute to productivity growth in the coming years and put upward pressure on the unemployment rate, although this is likely to be frictional vs. structural unemployment.

- Technological innovation has historically resulted in the creation of more jobs than it disrupts, and while it is still early, we believe there is potential for a similar outcome with the evolution of AI. Continued adoption could also drive much-needed operational efficiency at many corporations, which would also help support today’s lofty market valuations.

“People will come Ray” – The AI Ecosystem and Equity Market Impacts

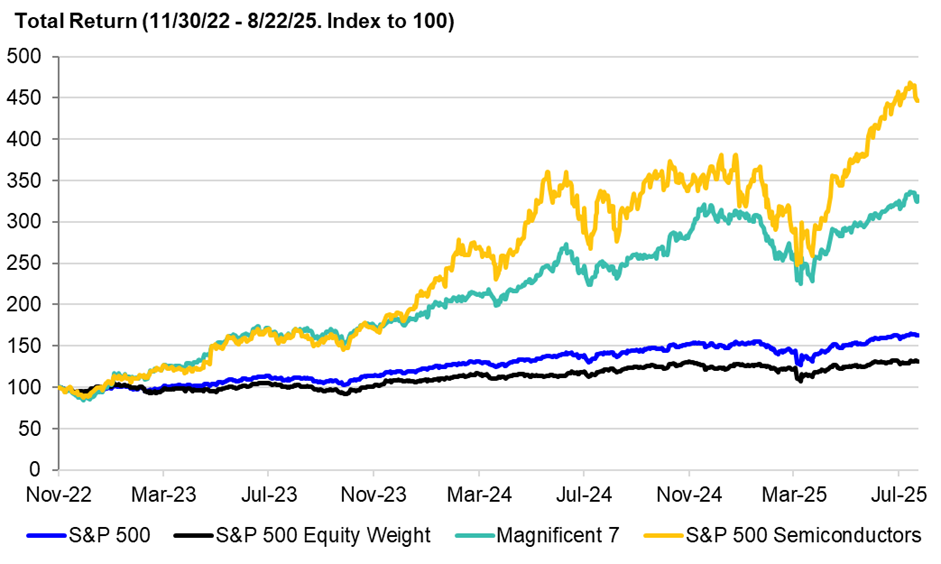

The launch of OpenAI’s Chat-GPT in November 2022 is generally considered the beginning of the current AI technological wave. While many companies had been working on AI innovation at the time, this event sparked an arms race among leading tech companies that has led to massive windfalls for businesses that provide the picks and shovels in this space. Meanwhile, the excitement over future productivity benefits from AI has provided a secular growth narrative for equity markets. Even amid macro turbulence and policy uncertainty, the S&P 500 has sustained a premium valuation relative to history and produced remarkable 20% annualized returns from November 2022 through mid-August 2025.

While 20% annualized returns for the S&P 500 over a three-year period are rare (occurring about 7% of the time since 1950), even more astounding has been the concentration of this performance among a handful of leading AI companies. Since November 2022, the Bloomberg Index of Magnificent 7 stocks has generated an annualized return of 55%, dwarfing the still healthy 10% annualized return for the average stock or equal weight S&P 500 Index.

Also, thanks to a combination of earnings growth and multiple expansion, over this period, 58% of the S&P 500’s total return has come from a handful of companies viewed as leaders in the AI infrastructure and platform space (NVDA, META, AAPL, AMZN, GOOGL, MSFT, AVGO). This is a remarkable level of concentration and according to Goldman Sachs, in 2025 alone, more than 70% of the S&P 500s 10% YTD return has come from a basket of AI beneficiaries.

Ultimately, these statistics underscore the importance and contribution of the AI narrative to U.S. equity markets, yet the key questions we have going forward are how much longer can this secular growth story support equity market performance and premium valuations, can all this investment be justified by accelerating AI adoption trends, monetization, and revenue growth in the future, and what will be the eventual impact on the U.S. labor market and broader corporate profitability?

“Is this heaven” – An AI bubble or still in the early innings?

For the last several years, investors have clamored to get exposure to companies, both public and private, that are exposed to the AI ecosystem, including semiconductor designers and manufacturers, hyperscalers, industrial data center suppliers, and power producers. For investors in these segments, the environment over the past few years may seem like heaven, and while some of this value creation has been driven by underlying profit growth, recent uneasiness around valuations and crowded positioning has begun to raise questions.

OpenAI, the creator of ChatGPT, was recently valued at $500B, making it the most valuable private company in history. While the company has seen remarkable user growth over the last three years, it has now reached a valuation that is more than twice the value of bellwether software firm Salesforce, a company that generates nearly four times as much recurring revenue annually and serves over one hundred thousand corporate customers around the world. While some of this can be attributed to an extraordinary growth rate, even OpenAI CEO Sam Altman recently commented that, in his view, investors are “overexcited about AI today”, while noting in the same sentence that AI is likely the “most important thing to happen in a very long time”.

We would agree that there are certainly pockets of excess or bubble-like conditions in parts of the AI ecosystem (Palantir recently trading at 90x next 12-month revenues for example), and that investors may be overly optimistic about the pace of adoption and potential monetization of this technology. However, this is not uncommon in the evolution of any new technology, and ultimately a deflating bubble, while painful for some, can create a more rational environment for capital allocation and reward more disciplined investors with long-term value creation.

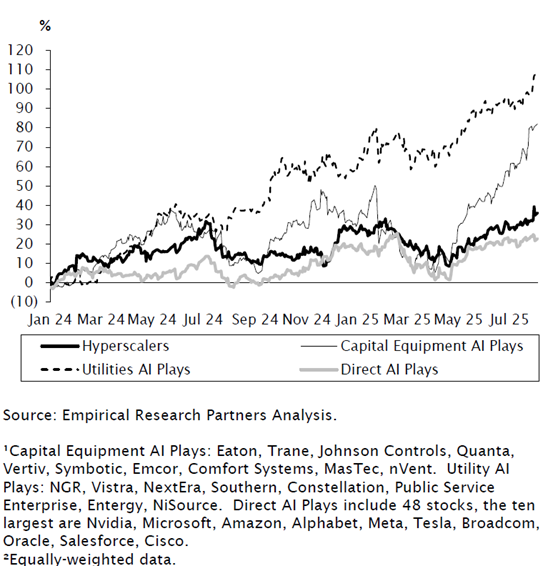

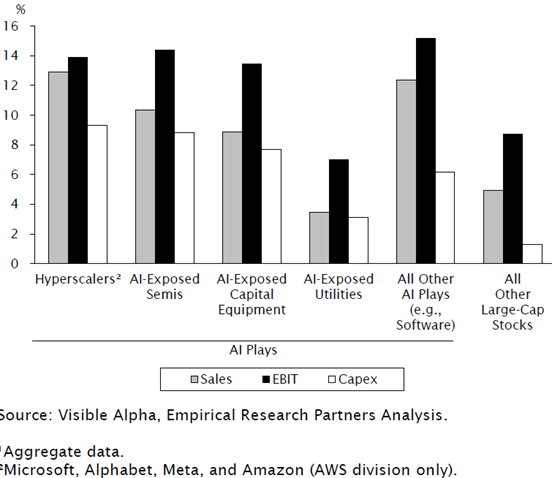

Select AI Plays YTD Performance

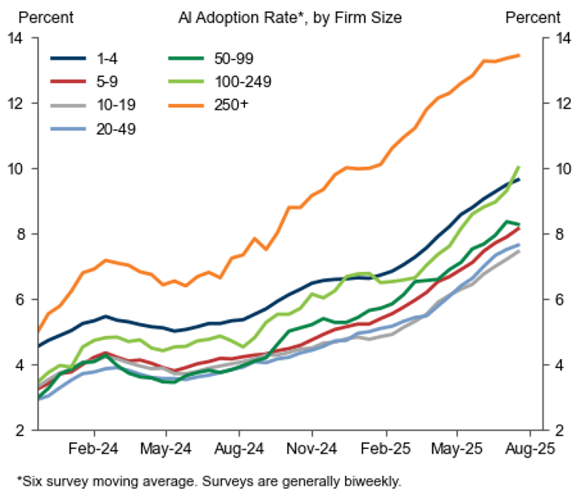

To analyze what inning we are in in the evolution of AI, we can look at current adoption trends. According to a Census Bureau survey of over one million businesses, as of July 2025, only about 9% of companies reported using AI in production on a weekly basis, and 13% said they plan on using AI in the next six months. While this seems low for a technology entering its fourth year of existence, the adoption rate has nearly doubled over the past year, and historically, most new technology takes several years to take hold. In addition, this may be understated given that adoption rates have been higher for large companies (around 14% for companies with more than 250 employees), and so far, adoption has been highest in technology forward industries and those that are more exposed to automation, like software development and credit analysis.

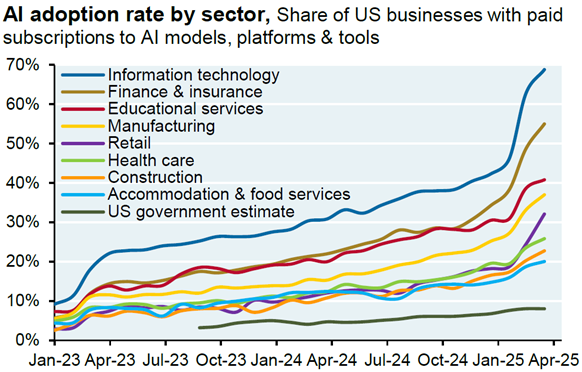

In our view, these trends could be a sign that adoption rates will pick up as AI technology makes its way into a broader subset of industries as well as smaller companies. And while the majority of companies are not using AI in production yet, an increasingly large percentage of companies have paid subscriptions to AI models, platforms and tools, suggesting many companies may be exploring ways to use this technology in production in the future. Ultimately, continued acceleration in these key metrics will be critical to justify lofty valuations and support the elevated capital intensity for many of the largest companies in the market.

“If you build it, he will come” – Context and Thoughts around Hyperscaler Capex

Some of the most eye-popping statistics in the AI ecosystem today continue to be around the capital expenditures from the largest technology companies and hyperscalers (the Big Four being Microsoft, Amazon, Alphabet, and Meta). As a group, the Big Four are expected to spend over $350B on capital expenditures in 2025, the majority of which is directed at building compute capacity. This capex is significantly higher than was originally projected, is up 40% from last year, and is likely to surpass $400B in 2026. This projected spending is a level that is estimated to exceed the collective annual defense spending of the European Union and is approaching half of what the United States spends on defense each year.

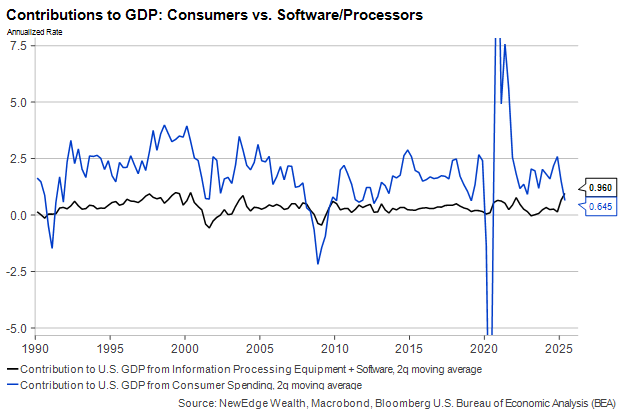

This capex (when measured by investment in computer hardware and software) even contributed more to GDP growth in 2Q25 than the entirety of the U.S. Consumer (which makes up 70% of GDP). Consumption always represents the lion’s share of output, but its growth has slowed this year as AI-adjacent investment has sped ahead.

As a percentage of total U.S. equity market capex, the hyperscaler spending is at a level only seen in two other industrial waves, notably the energy sector shale oil boom last decade, and the 1960s automotive industry boom, suggesting these hyperscalers view the opportunity in AI to be of similar scale.

In contrast to the “old economy” automotive and oil industries, however, the big four hyperscalers today are all self-funding and despite this elevated capex, these companies still generate healthy free cash flow, with trailing 12-month free cash flow margins averaging high teens today. While these margins have declined substantially over the past few years, they remain at a level that is on par with the broader U.S. equity market. To maintain profitability, the hyperscalers will need to continue to produce healthy top line growth, remain disciplined around operational expenses, and eventually demonstrate effective monetization from AI compute and products. The last of these will likely be a result of increased AI adoption rates and further illustrates the importance of these measures.

Elevated spending and comparisons to past industrial booms can also be viewed as a cautionary tale for the AI ecosystem however, as excessive expenditures have historically led to excess capacity, lower returns on investment, and in some cases an eventual bust. This appreciation for past cycles, and the lack of certainty of return for all this investment, are reasons we think investors need to remain prudent around exposure to many AI businesses, focusing on more efficient capital allocators with clearer paths to monetization that can help support elevated valuations.

Turning back to the Big Four hyperscalers, something that has reassured investors this year, has been the continued commentary from each company that the biggest headwind to faster monetization is constrained compute capacity. This suggests there is still outsized demand for AI fueled compute despite the already extensive investments and current modest AI adoption rates. This supply-demand imbalance and the potential for it to meaningfully increase going forward, are reasons why data center infrastructure continues to be one of the more prevalent investment themes across asset classes and is why there is currently over 100GW of data center capacity under construction in the U.S., representing a 4x increase from the current 25GW of data center capacity.

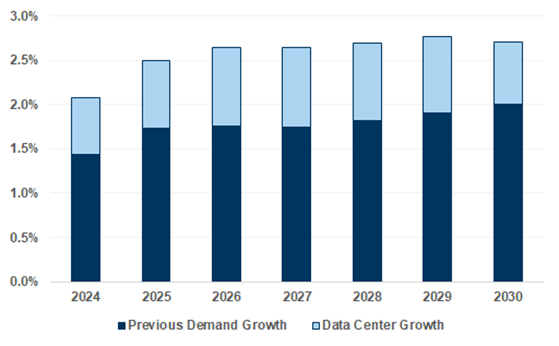

The electricity needs of facilities running large language models, which are known to consume significantly more energy than traditional web searches, are already contributing to energy bottlenecks and putting upward pressure on electricity prices. Meanwhile expectations are that data center power consumption will increase by 160% over the next four years, and lead to 2.5% annual increases in U.S. Power Demand through 2030. This is one reason why U.S. power generators or “AI Utilities” have been strong performers lately, and why many have been partnering directly with hyperscalers to secure long-term power selling agreements.

The Impact of Data Centers on Annual U.S. Power Demand Growth

While today’s investors in the Big Four hyperscalers and adjacent tech giants continue to give these companies the benefit of the doubt on elevated capex and investment, in our view qualifying this investment and maintaining investor enthusiasm will have to come from continued momentum and delivering on expectations of premium revenue and earnings growth relative to the rest of the market. If this growth returns to market wide levels or begins to disappoint relative to expectations, we could see the tide and investor confidence in this capex quickly turn.

Annualized Expected Growth Rates of AI Segments 2026-2030

“Ease His Pain” – The Impact of AI on the U.S. Economy and Labor Market

As we noted, AI capex is having a positive impact on U.S. economic growth today, helping to offset slowing in other sectors like housing and consumption, occurring, in part, due to high interest rates.

However, the true benefits of AI will likely be seen over the longer term in better worker productivity. Strong productivity growth can help ensure healthier long-term economic growth and corporate profitability and provide support for equity market valuations. As AI adoption grows, we may see productivity per worker increase and headcounts at many corporations decline or at grow at rates far slower than revenues, a trend that some CEOs have already highlighted. In the last few months, Salesforce CEO Mark Benioff has said AI is already completing 30-50% of the work done at the company. Microsoft CEO Satya Nadella has said 25% of the code in the company’s software is being written by AI, and J.P. Morgan’s Head of Consumer Banking suggests AI technology could allow the company to reduce their headcount by 10% over the next 5 years. While the commoditization of AI has the potential to create deflationary pressures for certain industries like software, ultimately its broadening adoption is likely to support incremental operational efficiency for many companies.

In terms of the long-term implications of AI, Goldman Sachs expects AI to drive a 15% increase in worker productivity and displace around 6-7% of the U.S. workforce in the next 10-15 years. This displacement is likely to be seen in more entry level positions and in areas that rely heavily on repetitive tasks, ultimately leading to an uptick in temporary as opposed to long-term unemployment as these workers transition to new roles. This would be consistent with past technological innovations, and while these modest numbers assume steadily increasing AI adoption, they would only amount to a small uptick in the average annual displacement rate of 1.5%. Overall trends that suggest concerns about substantial AI labor market disruption are overblown.

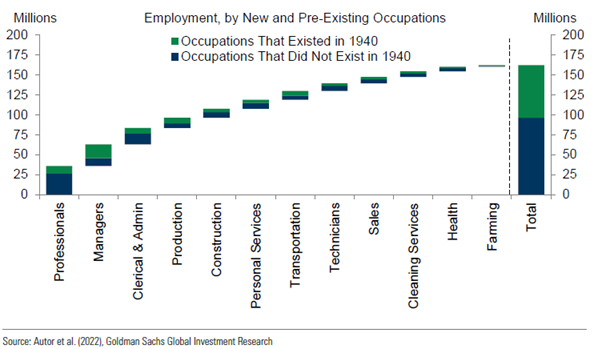

Historically, most technological innovation has been met with similar fears of vast labor market displacement, from automobiles replacing the horse drawn carriage industry to the internet replacing a wide range of services and retail professions. Ultimately, while these innovations did lead to job displacement, job losses were far exceeded by the jobs created from the new industries that emerged from technological advancement. Since 1940, over 85% of employment growth has been a result of technological innovation, and while it is still early in the adoption cycle, we expect the longer-term benefits of AI to outweigh the temporary labor market disruption.

Closing Thoughts

Given the still early phase of adoption and evolution of AI technology, it’s difficult to say how accurate these longer-term assumptions are and what their ultimate impact on markets will be. However, we see some positive signs under the surface that provide confidence in maintaining exposure to many names in the AI ecosystem, especially in investments that are well supported by underlying fundamentals with reasonable valuations.

While broad corporate level AI adoption trends remain modest, they are accelerating for larger companies and for more tech forward industries, suggesting this trend has room to continue. That increased adoption will likely continue to fuel robust compute demand and power consumption from the largest hyperscalers, also suggesting return on today’s outsized infrastructure investments will begin to flow through into monetization. While valuations for this group are no longer cheap, the fact that they are self-funding and still hold average free cash flow margins should provide some insulation from the eventual maturation of this cycle and deceleration in overall growth rates. Lastly, while the economic impact has been modest thus far, there is potential for increased productivity, and lower headcount helping support broad corporate profit margins in the coming quarters, which would be a key contributor to supporting today’s elevated market valuations.

IMPORTANT DISCLOSURES

The views and opinions included in these materials belong to their author and do not necessarily reflect the views and opinions of NewEdge Capital Group, LLC.

This information is general in nature and has been prepared solely for informational and educational purposes and does not constitute an offer or a recommendation to buy or sell any particular security or to adopt any specific investment strategy.

NewEdge and its affiliates do not render advice on legal, tax and/or tax accounting matters. You should consult your personal tax and/or legal advisor to learn about any potential tax or other implications that may result from acting on a particular recommendation.

The trademarks and service marks contained herein are the property of their respective owners. Unless otherwise specifically indicated, all information with respect to any third party not affiliated with NewEdge has been provided by, and is the sole responsibility of, such third party and has not been independently verified by NewEdge, its affiliates or any other independent third party. No representation is given with respect to its accuracy or completeness, and such information and opinions may change without notice.

Investing involves risk, including possible loss of principal. Past performance is no guarantee of future results.

Any forward-looking statements or forecasts are based on assumptions and actual results are expected to vary from any such statements or forecasts. No assurance can be given that investment objectives or target returns will be achieved. Future returns may be higher or lower than the estimates presented herein.

An investment cannot be made directly in an index. Indices are unmanaged and have no fees or expenses. You can obtain information about many indices online at a variety of sources including: https://www.sec.gov/answers/indices.htm.

All data is subject to change without notice.

© 2026 NewEdge Capital Group, LLC