Introduction

“Who says nothing is impossible? Some people do it every day!”

The war in Iran that began six weeks ago may already be on the verge of wrapping up. But transportation and shipping costs have rocketed higher and are unlikely to fully reverse for several months even with a ceasefire in place and oil once again flowing. U.S. GDP trackers have more than halved their estimate for Q1 growth since the war started. Markets are forward-looking, however. All major U.S. equity indexes made new all-time highs in the past week even before the U.S. and Iran announced that the Strait of Hormuz would reopen to commercial traffic.

Fans of Mad Magazine will recognize the influence of the publication’s infamous mascot, Alfred E. Neumann, on this week’s edition. Borrowing his look from the Little Rascals and his quotability from Yogi Berra (albeit with considerably more biting cynicism), Alfred will chime in throughout this piece to put everyone (including us) in their rightful place as the topics move from geopolitics to markets to risks. What, if anything, has the chaos of the past six weeks taught us as investors? And what are the risks as we move forward?

We’re (Still) Monitoring the Situation

“It takes one to know one — and vice versa!”

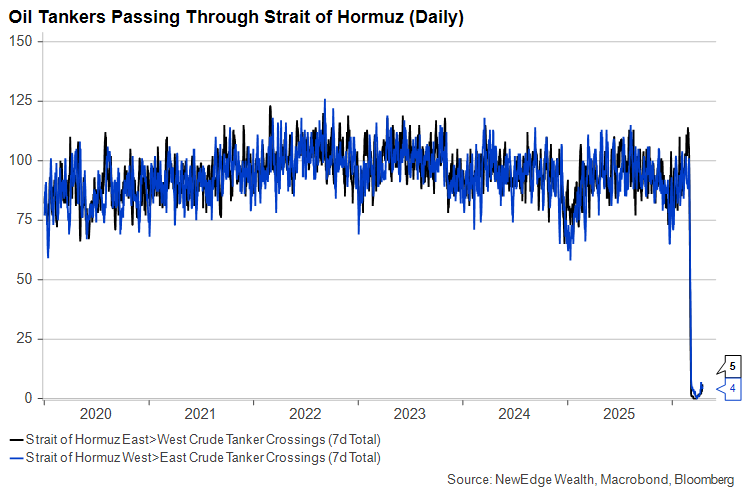

It’s been several weeks since the start of the Iran War and the de facto closure of the Strait of Hormuz, the narrow channel through which close to 20% of the world’s oil supply (not to mention liquified natural gas and fertilizer precursors) flows. Iran effectively closed the Strait in March but as of this writing had agreed to allow commercial ships to pass through once again while the ceasefire is in place. If this holds, the past six weeks have created a massive air pocket in global energy shipments that will persist even if daily shipments return to normal:

Prior to this week, the dual blockade (U.S. blocking Iranian oil and Iran blocking everything else) meant that oil importers in Asia, Europe, and elsewhere would face acute shortages. These are likely to materialize in some form even if the strait reopens immediately. Many oil-producing Gulf states have shut their production down or seen infrastructure damaged by bombing. It may take some time for supply to fully return to February levels.

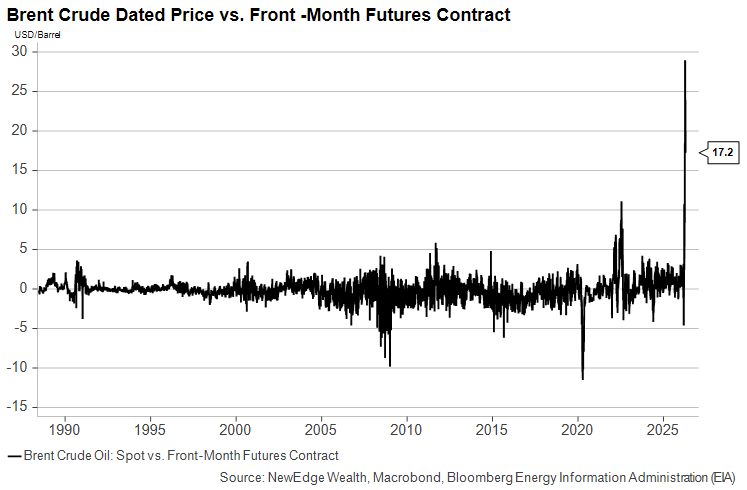

The war’s effects have already shown up in the historically wide gap between the paper futures contract price for June and the physical delivery price. It’s currently much more expensive to buy a barrel of oil immediately than to secure one for purchase in one or two months’ time:

The effects of physical shortages on spot prices are inescapable. Futures prices are lower because investors, hedgers, and end-users of oil assume with good reason that supply will improve shortly. Financial markets anticipated a quick resolution, as well, which takes us into our next section.

A Stunning 360-Degree Turn for Markets

“Fools rush in…and get the best seats”

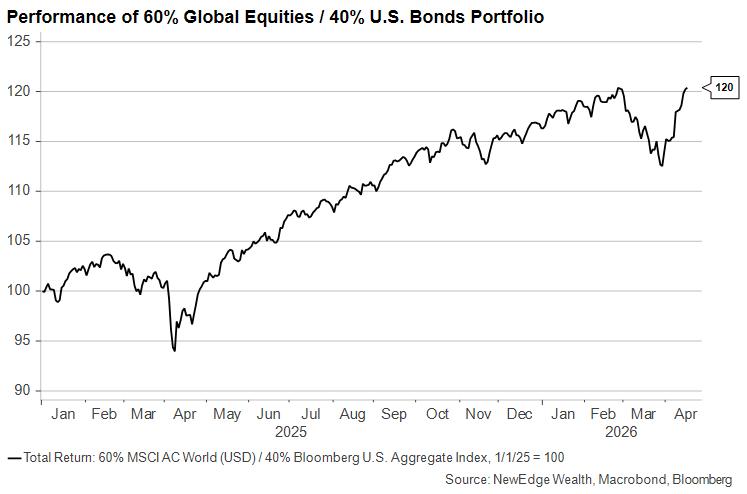

The first half of April has seen one of the strongest market comebacks in decades. Since the point of maximum geopolitical worry on March 30th, interest rates have fallen, equity markets have rallied, and credit spreads have narrowed. We often speak of V-shaped recoveries as the ideal scenario following a 5% or 10% correction. In this case, the recovery was about twice as fast as the initial drawdown:

In our March 13th piece, we speculated that the reason equity markets had not reacted more negatively to the onset of the war was the Trump Administration’s reputation for reversing policies when they begin to harm financial markets. Both the rhetoric and the actions coming from the White House have rewarded that faith. Friday’s morning’s apparent constructive developments toward a deal to end the war boosted market sentiment further.

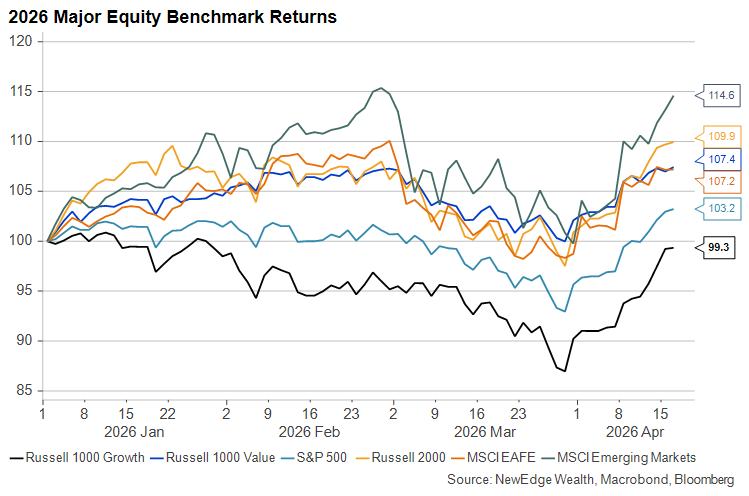

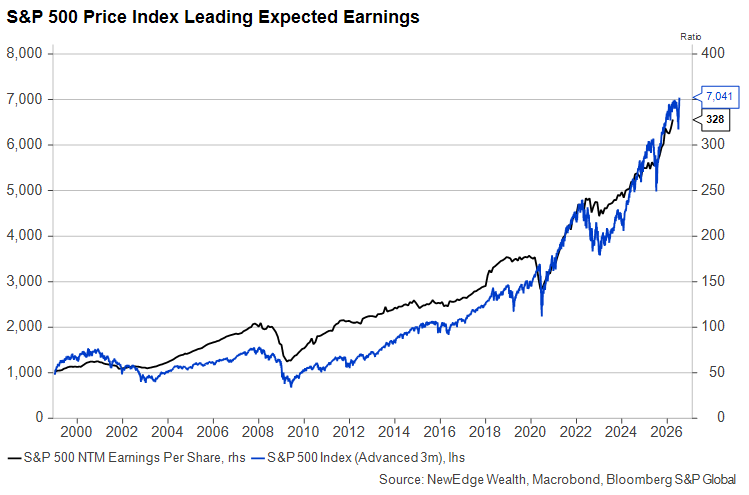

In addition to general optimism about the war ending, stocks have been powered ahead by further upward earnings revisions (particularly to a small number of high-growth U.S. companies) and renewed broad risk appetite for emerging markets, as this chart of year-to-date market returns shows.

As we’ve often pointed out, earnings estimates tend to respond with a short lag to changes in stock prices. But for the third year out of the last four, stocks have corrected and re-corrected quickly enough that analysts have not had time (or need) to trim profits expectations. Of course, we are still early in 2026, and stocks have plenty of opportunities to stage another swoon, particularly if hostilities in the Middle East resume.

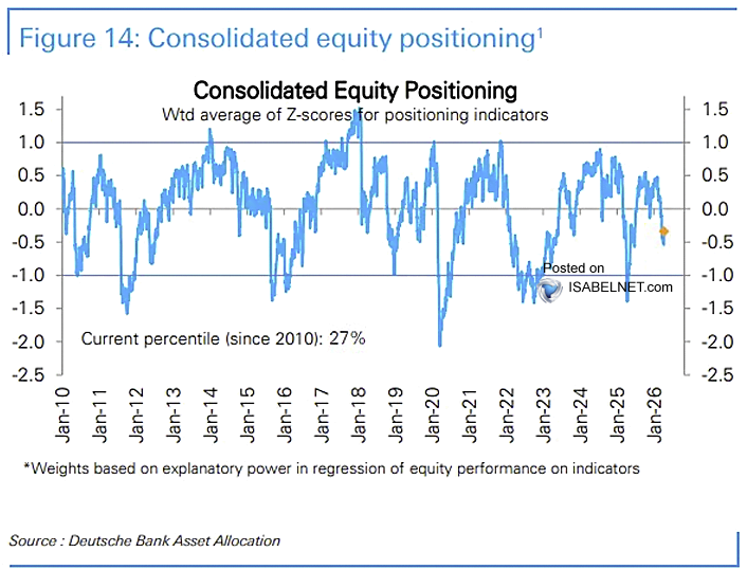

For the time being, the rally may continue to have legs as earnings reports start to flow in and investors chase the gains. According to positioning data from Deutsche Bank shown on the chart below, many investors became underweight stocks during the March sell-off and are now faced with the choice of increasing their positions or watching from the sidelines:

Impressive, Yes. But Sustainable?

“You can be on the right track and still get hit by a train!”

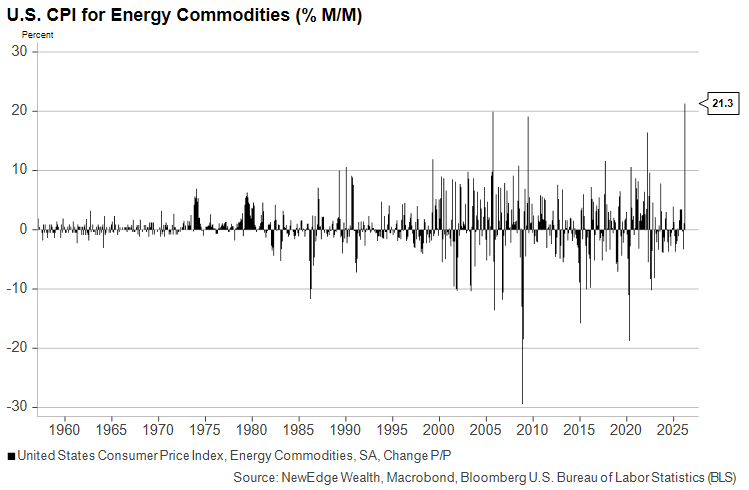

Market behavior over the past six weeks has reflected the onset of an initial supply shock followed quickly by expectations of that shock quickly fading. Financial markets are discounting virtually no lasting economic damage from the war. Interest rates have risen since February, the opposite of what we would see if recession fears had increased. Fed rate cut expectations have been pushed out to the end of the year as March inflation readings showed the single largest one-month energy price increase in history:

It’s true that household sentiment has touched a new all-time low, but it’s hard for us to take that reading seriously in isolation. Consumer confidence has been in the doldrums for years, but people have continued to save less and spend more quarter after quarter.

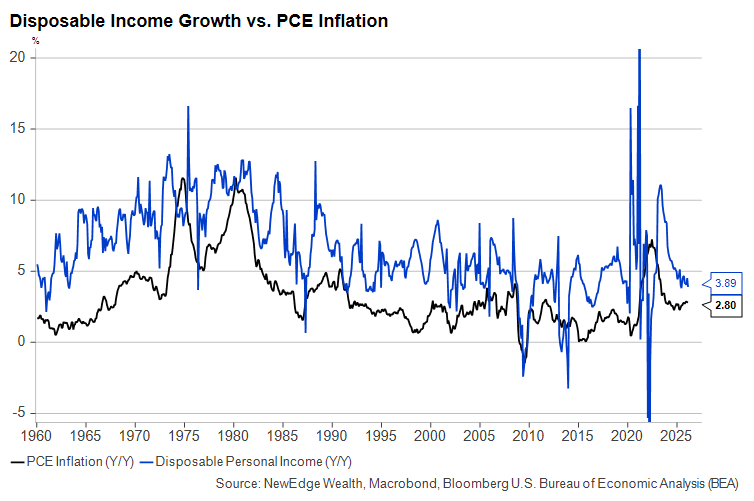

Why might this time be different? We are concerned about a consumer squeeze this summer from unexpectedly high gasoline prices and slowing wage growth. The history of the U.S. economy at times when the blue line on the graph below (disposable income growth) is lower than the black one (headline inflation) is not pretty. Let’s hope they don’t cross again.

Positioning Portfolios for More Choppiness Ahead

“Too often, people who want to offer sound advice give more sound than advice!”

Even the most optimistic among us may be stunned by the speed and strength of the market rally this month. Investors are putting their faith in the political and military leadership of both the U.S. and Iran to reach a peaceful resolution the eases the energy supply shock and reduces economic uncertainty.

Some investors who held back deploying cash in March may be feeling pangs of regret that they did not do so. Timing markets is notoriously difficult, but sticking to a capital deployment plan even when things look dangerous (especially when things look dangerous!) can help eliminate much of that timing risk.

We know from very recent experience what a sudden reescalation of the conflict would likely do to financial markets. There are few hedges against a slower-growth, higher-inflation economic environment. Adding real assets to a portfolio – not just gold but diversified commodities, core real estate, and infrastructure – can be a useful hedge in such periods. Meanwhile, with bonds offering substantially higher yields than they did in late February, many diversified portfolios could benefit from the additional income and low correlation to stocks (in growth scares and recessions, at least) that they provide.

In equity markets, we continue to marvel at the performance of Large Cap U.S. Growth stocks, where earnings look strongest and direct connection to the negative effects of the war on consumers are arguably weakest. Despite a nearly 10% rally this quarter, the Russell 1000 Growth Index looks cheaper than it did to start the year thanks primarily to rising earnings estimates for semiconductor producers.

There are no easy answers to how investors should be positioned or how they should avoid downside risk in the current environment. When asked how he might invest amid the clouds of geopolitical and economic uncertainty, we have a feeling Mr. Alfred E. Neumann would dust off this old chestnut: “It’s what you learn after you know it all that really counts!”

IMPORTANT DISCLOSURES

The views and opinions included in these materials belong to their author and do not necessarily reflect the views and opinions of NewEdge Capital Group, LLC.

This information is general in nature and has been prepared solely for informational and educational purposes and does not constitute an offer or a recommendation to buy or sell any particular security or to adopt any specific investment strategy.

NewEdge and its affiliates do not render advice on legal, tax and/or tax accounting matters. You should consult your personal tax and/or legal advisor to learn about any potential tax or other implications that may result from acting on a particular recommendation.

The trademarks and service marks contained herein are the property of their respective owners. Unless otherwise specifically indicated, all information with respect to any third party not affiliated with NewEdge has been provided by, and is the sole responsibility of, such third party and has not been independently verified by NewEdge, its affiliates or any other independent third party. No representation is given with respect to its accuracy or completeness, and such information and opinions may change without notice.

Investing involves risk, including possible loss of principal. Past performance is no guarantee of future results.

Any forward-looking statements or forecasts are based on assumptions and actual results are expected to vary from any such statements or forecasts. No assurance can be given that investment objectives or target returns will be achieved. Future returns may be higher or lower than the estimates presented herein.

An investment cannot be made directly in an index. Indices are unmanaged and have no fees or expenses. You can obtain information about many indices online at a variety of sources including: https://www.sec.gov/answers/indices.htm.

All data is subject to change without notice.

© 2026 NewEdge Capital Group, LLC