Introduction: Why Bonds?

“My answer is I don’t have the first d*** clue.”

Just when investors thought it was safe to go back into the bond market, the Iran War and resulting inflationary concerns reversed the January-February decline in rates (rally in bond prices) and then some.

Expectations for Fed cuts have quickly turned into fears of Fed hikes given the inflationary backdrop, while the correlation between bonds and stocks, which had been reverting to negative territory over the past two years, has snapped back to being unhelpfully positive. Said another way, stocks and bonds have been moving together in the last two months, and investors have noticed. Still, bond selloffs allow investors to “lock in” higher yields on the other side. Further, diversified investors need to ask whether stocks can continue to provide an outsized share of portfolio returns in the coming years.

For inspiration this week, we turn to Jack Nicholson’s iconic turn as Colonel Nathan Jessup in Rob Reiner’s 1992 courtroom drama, A Few Good Men. Featuring one of the most gripping showdowns between an attorney and a hostile witness in cinema history, the film ultimately asks us to deliver a verdict on whether we can (or should) rely on deeply flawed characters to perform essential, occasionally dangerous functions. In the year 2026, it seems a growing number of investors view bonds through a similar lens. But we caution against ordering a “Code Red” and banishing them from a portfolio at this time.

Why Do We Own Bonds?

“I would rather you just said ‘thank you’ and went on your way.”

We understand from client conversations that investors are hesitant to add exposure to fixed income, even with interest rates close to multi-decade highs. Let’s start with the reasons it has historically made sense for investors to own bonds as part of a diversified asset allocation. As we go through the list, the reasons for bonds’ waning popularity in recent years will become clear.

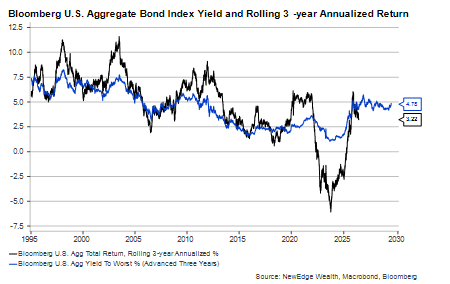

1. High yields – Bonds are first and foremost a source of income. The amount of income a bond pays is a function of both its market risk (i.e., sensitivity to changes in the interest rate and credit environments) and its default risk. While bonds rarely beat equities over periods longer than a year, major benchmarks like the Bloomberg U.S. Aggregate Bond Index have historically provided mid-single digit percentage yields and comparable subsequent total returns, with the 2021-2023 period a very notable and very recent exception:

As of 5/21/26

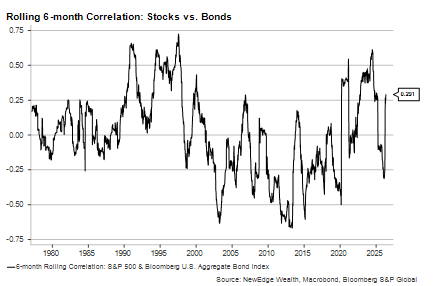

2. Low correlation to stocks and other risk assets – Throughout the 2000s and 2010s, the prices of stocks and bonds tended to move in different directions. Returns on both asset classes were generally positive, but the offsetting timing of those returns paved a smooth road for diversified portfolios. But stock-bond correlations have turned positive in the 2020s as high inflation has replaced slow growth as the primary market concern. Inflation risks hurt the prices of both stocks and bonds, leading to painful correlation spikes in both 2022 and 2026:

As of 5/21/26

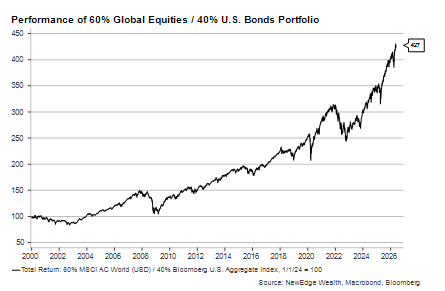

3. Rebalancing Ability – The main drawback of holding a 100% equity portfolio is that when stocks decline, there is no money available to buy more of them at discounted prices. Bonds have historically been an excellent port in a storm during growth scares and recessions like 2001 and 2008. Having the courage to rebalance out of appreciated bonds into plummeting stocks in March 2020 meant that diversified portfolios were able to recover their COVID losses in a matter of weeks. In the past few years, however, equity corrections have been so brief that rebalancing was neither necessary nor feasible. And the last time stocks did enter a bear market, in 2022, bonds were down even more on a risk-adjusted basis:

As of 5/21/26

How Have Bonds Performed Recently?

“You can’t handle the truth!”

As the prior section made clear, bonds have not “acquitted themselves with distinction” over the past five years. This was, perhaps, inevitable given that 2021 appears to have marked the end of the 40-year bull market in bonds. The transition from “ZIRP” (zero interest rate policy) into a more normal interest rate environment was going to be painful whether it happened quickly or slowly.

That pain has continued for most parts of the bond market in 2026 despite a very promising start to the year. Yields on Treasuries for every maturity beyond a few months are significantly higher today than they were on January 1st:

As of 5/22/26

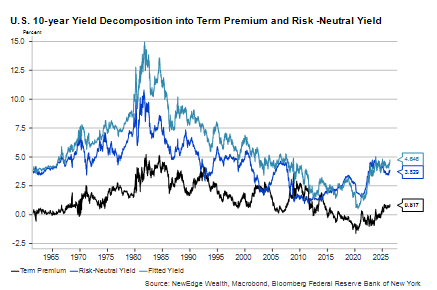

When we dig into why yields have risen, we get multiple answers. Let’s decompose the move in the 10-year U.S. Treasury Note as an example. Its yield appears on the graph below as the green line, made up of the blue line (average short-term rates) and the black line (the term premium).

First, as the blue line on the graph below shows, short-term interest rates are no longer expected to be lower for longer. The Fed has cut interest rates to just over 3.5%, a level it still considers to be restrictive, yet unemployment remains low and stable and core inflation still runs well above its target. This implies that Fed policy is closer to neutral and may, in fact, be accommodative. In other words, average short-term rates may need to be higher, on average, to keep the economy in balance.

Second, turning to the black line, the term premium has inched back up as global sovereign yields (even in places like Japan and Europe) have risen and concerns about the sustainability of the U.S. debt and deficit have reemerged. While the U.S. government is paying its creditors as high a markup to borrow for longer maturities as it has since the early 2010s, the term premium remains lower today than it has been for most of the past fifty years:

As of 5/21/26

On its face, the rise in interest rates, with its multiple drivers, makes fixed income more attractive for investors looking for higher yields and the potential for positive market returns. But much depends on whether rates stay where they are, fall, or move even higher.

What is Our Outlook?

“You want me on that wall. You need me on that wall.”

The path of interest rates from here depends on how long inflation risks continue to dominate growth risks as the primary market drivers. A resolution in the Iran War, assuming it comes with a return to normal transit of ships through the Strait of Hormuz, could eventually help oil prices normalize and remove much of the global inflationary threat. This might not be enough to deliver immediately lower gas prices and inflation readings, but it could remove the threat of Fed rate hikes and a further pass-through to prices in other areas of the economy.

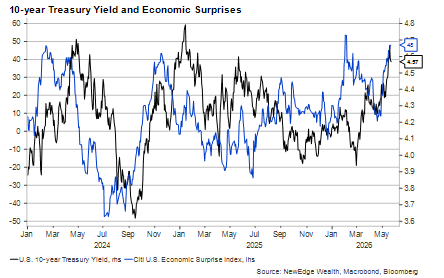

Another way rates could fall this year would be through a growth scare, or, worse, a recession. The risks of economic collapse do not currently appear high. In fact, economic surprises have been positive since the start of the war. But a prolonged period of high gas prices or a sharp further increase in food and energy prices will likely mean negative real income growth translates into negative personal spending growth. Rates could fall in this scenario for “bad” reasons as investors flock to “safe” assets with lower volatility and the Fed is forced to easy policy.

As of 5/22/26

Of course, a continuation of the status quo in the Iran War will likely mean a further grind higher in inflation and, eventually, in interest rates. While they present acute challenges for many U.S. businesses and households, oil at $100/bbl and gasoline at $4.50/gallon is “annoying” but not “crippling” for the overall economy. This could allow the U.S. 10-year Treasury yield to retest its post-COVID high of 4.99% from October 2023.

Conclusion: Is It a Good Time to Add Bonds?

“I’ll answer the question.”

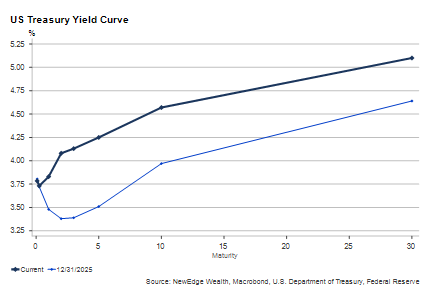

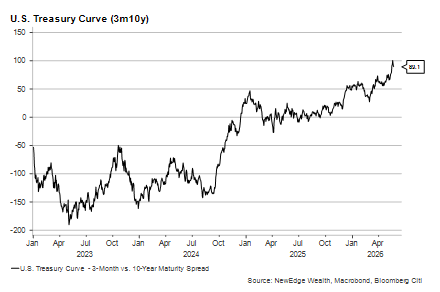

It’s hard for us to paint all investors with the same broad brush. But regardless of age, wealth level, or tax status, most investors have income needs of some kind. Bonds remain an important component of that income “bucket” in diversified portfolios, and they are providing more income today than at just about any point in the last twenty years. Moreover, the steepening in the U.S. Treasury yield curve likely argues for a move out of cash and into longer-duration securities to pick up more yield:

As of 5/22/26

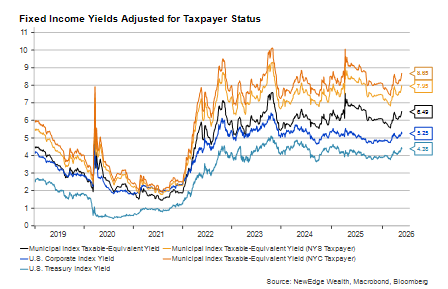

Taxable investors in high-tax states and cities don’t have to settle for the after-tax returns on Treasuries or even corporate bonds. Taxable-equivalent yields on municipal bonds are significantly higher, especially for longer maturities, compared to taxable categories:

As of 5/21/26

Compare a 7-8% taxable-equivalent return on municipals to what we might expect to receive on an S&P 500 index fund moving forward after a three-year period in which returns have averaged more than 20%. For investors who can “handle the truth”, a return to balance – and to bonds – may be a move worth making in these uncertain times.

IMPORTANT DISCLOSURES

The views and opinions included in these materials belong to their author and do not necessarily reflect the views and opinions of NewEdge Capital Group, LLC.

This information is general in nature and has been prepared solely for informational and educational purposes and does not constitute an offer or a recommendation to buy or sell any particular security or to adopt any specific investment strategy.

NewEdge and its affiliates do not render advice on legal, tax and/or tax accounting matters. You should consult your personal tax and/or legal advisor to learn about any potential tax or other implications that may result from acting on a particular recommendation.

The trademarks and service marks contained herein are the property of their respective owners. Unless otherwise specifically indicated, all information with respect to any third party not affiliated with NewEdge has been provided by, and is the sole responsibility of, such third party and has not been independently verified by NewEdge, its affiliates or any other independent third party. No representation is given with respect to its accuracy or completeness, and such information and opinions may change without notice.

Investing involves risk, including possible loss of principal. Past performance is no guarantee of future results.

Any forward-looking statements or forecasts are based on assumptions and actual results are expected to vary from any such statements or forecasts. No assurance can be given that investment objectives or target returns will be achieved. Future returns may be higher or lower than the estimates presented herein.

An investment cannot be made directly in an index. Indices are unmanaged and have no fees or expenses. You can obtain information about many indices online at a variety of sources including: https://www.sec.gov/answers/indices.htm.

All data is subject to change without notice.

© 2026 NewEdge Capital Group, LLC