Introduction

“Don’t panic.”

Investors have now lived through several weeks of heightened market volatility, driven primarily by a combination of disappointing economic data and erratic policymaking. As we’ll point out in this piece, the amount of market churn – especially intraday – has been unusually high while the peak-to-trough declines in most major indexes have not…at least, not yet. But those familiar with Douglas Adams’ classic science fiction story A Hitchhiker’s Guide to the Galaxy may be asking themselves, “Would it save you a lot of time if I just gave up and went mad now?”

We think not. In fact, now seems a good time to provide some perspective on what we have seen thus far from the Trump administration on trade policy and government spending. What is the likely impact on the economy and the markets? We believe data will be “lumpier” and markets more volatile, but there are always ways for investors to seek to capitalize when there are opportunities and protect portfolios when it is prudent (often both at once).

Bracing for (Limited) Economic Impact

“For a moment, nothing happened. Then, after a second or so, nothing continued to happen.”

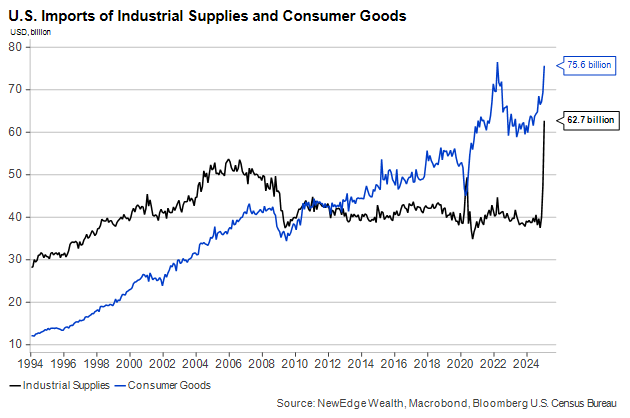

We are only now receiving economic data from January and February, but what we have so far supports the observation we made last year that the threat of tariffs – even if they never go into effect – can warp economic behavior. Imports of consumer goods and industrial supplies surged in anticipation of higher import taxes before President Trump even took office, as can be seen in the chart below.

This pulling forward of demand has already created “lumps” in the data. Spending on durable goods like appliances and cars soared last quarter but seems set to fall in the first half of this year. Most households do not purchase a new washing machine every three months, after all.

Some of the most reliable economic forecasters are onto this trend. The Federal Reserve Bank of Atlanta publishes a running “NowCast” of current quarter GDP. We are still early in the Q1 data cycle, but NowCast’s current estimate of negative 2.4% annualized growth would make the start of 2025 the weakest in years.

There are at least two reasons not to panic about this graph. First, the massive drop at the end of February was due to a very large increase in January’s trade deficit. Because this was driven almost entirely by firms and households avoiding future tariffs, we believe the deficit should narrow in the coming months. Second, for similar reasons, consumption may look weak in the Q1 GDP report because some demand was pulled forward into the prior quarter, when household spending growth annualized at a blistering 4.2%.

Businesses Pulling Back From Hiring and Investment?

“We demand rigidly defined areas of doubt and uncertainty!”

Unfortunately, even after discounting the lumps that GDP is taking from trade, domestic demand is weakening. Personal spending on durable goods fell in January after the December tariff avoidance binge, but outlays for non-durables and services were also soft. Consumers are feeling less certain about their job prospects and have not seen their wages climb as fast as over the past year. Yet we see no signs of imminent collapse in the labor market.

Considering the context in which it arrived, Friday’s February U.S. employment report was downright normal. Job creation remains solid, though government layoffs should begin to show up more clearly in next month’s report. The unemployment rate rose slightly to 4.1%, but it will have to rise considerably higher to tempt the Fed off the sidelines to cut rates again.

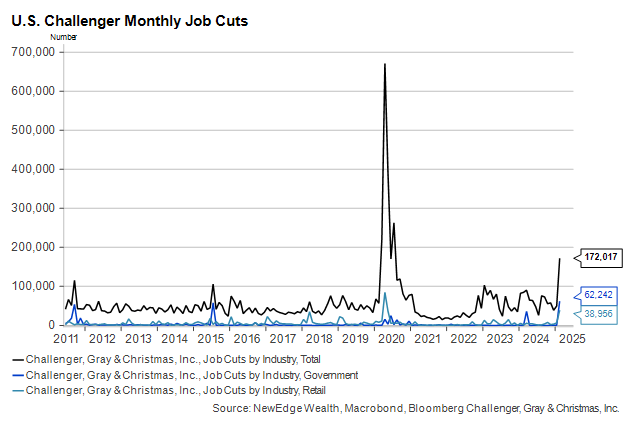

While official data on the jobs market remains good, private indicators like the Challenger Job Cuts survey have begun to flash orange. Layoffs last month were the highest since 2020, and only a portion of them can be blamed on the so-called DOGE cuts of government workers.

Even so, the cracks forming in the labor market remain thin for now. The number of workers filing for unemployment assistance each week is not rising appreciably, and the magnitude of announced federal job cuts so far is unlikely to change that. But should DOGE cuts and trade uncertainty ripple into the private sector as government contracts are cancelled and planned projects are mothballed, that could change.

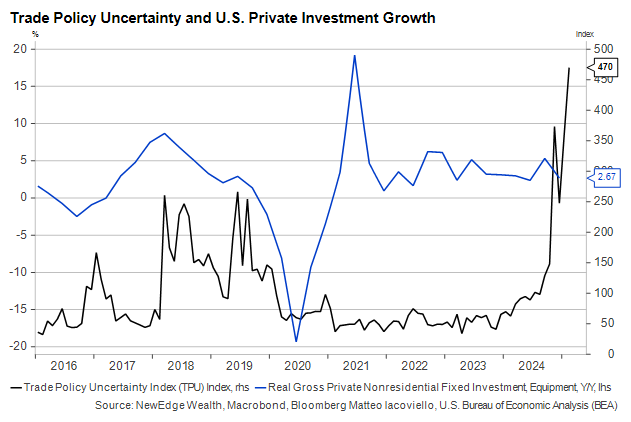

Private investment growth has been strong since the pandemic, and we continue to see announcements of large, high-profile projects related to energy and AI development. But trade policy uncertainty has a history of denting this growth, and there is more uncertainty around trade today than ever before.

A slew of disappointing national and regional manufacturing surveys are signs that history may be repeating itself. The ISM Manufacturing Index’s New Orders component fell from “strong expansion” to “moderate contraction” territory last month. The published comments from respondents to this survey and others like it continue to call out tariffs as contributing to uncertainty and paralysis.

Markets Are Right to Be Nervous About Tariffs

“Anyone who is capable of getting themselves made President should on no account be allowed to do the job.”

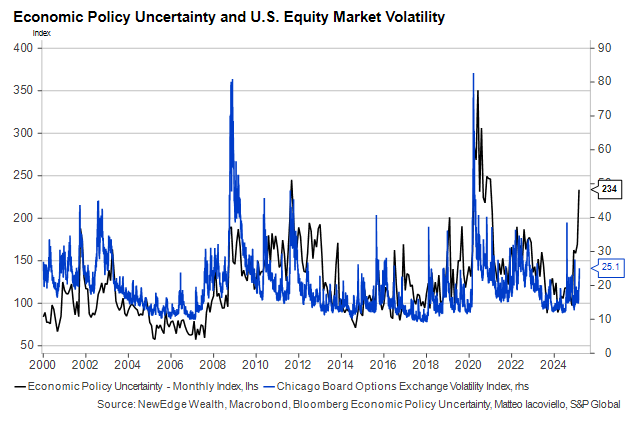

It’s not politically controversial to say that much of the daily (indeed, hourly) equity market volatility of the past few weeks has been driven by the on-again, off-again announcements around tariffs. However, volatility has not yet reached the heights it regularly hit during the last trade war in 2018-2019, let alone during more fraught moments like the near-U.S. Treasury default in 2011 or Covid’s onset in 2020.

Today’s uncertainty stems from a lack of clarity about the tariffs’ purpose, whether many will ever go into effect, and how long they’ll stay in place. This week’s flip-flops on the Mexico and Canada tariffs (the ones on imports from China were, at least, applied clearly and consistently) were more than markets could bear. U.S. stocks tumbled despite positive news from Europe and China, which lifted global interest rates and international stock prices.

Tariffs will become a larger problem for markets if they hurt earnings through either diminished investment (business-to-business sales) or slower consumption growth and a weaker labor market (business-to-consumer sales). By raising highly visible prices such as those on food and energy, tariffs simultaneously lower households’ means and desire to spend, which ends up hitting the discretionary items that make up the vast majority of U.S. consumer purchases.

Conclusion – Investing in a Time of Uncertainty

“I’d far rather be happy than right any day.”

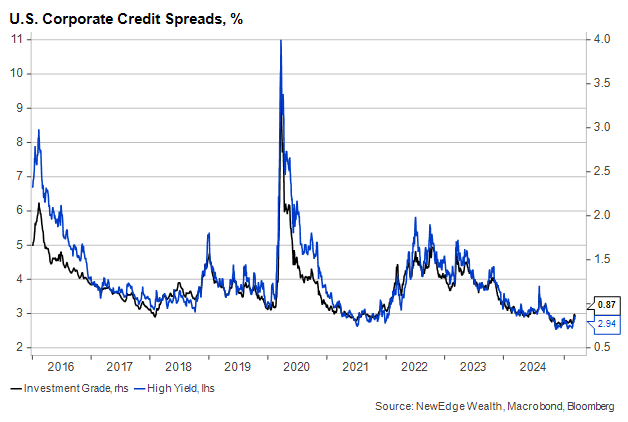

We said earlier not to panic, and we meant it. There is still not much evidence that the economy is on the brink of recession or close to it. Credit spreads, the canary in the economic coal mine, have barely budged from their historic lows.

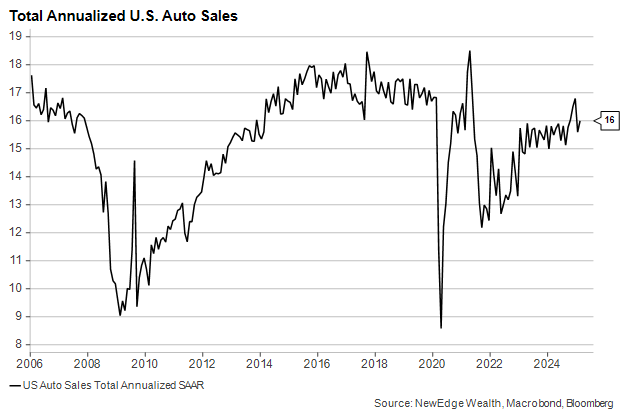

And car purchases rose in February after swooning in worrying fashion a month earlier.

We continue to view this as a normal market correction, not the start of a recession or protracted bear market. Five- to ten percent pullbacks happen regularly, even during sustained economic expansions, and they are often followed by sustained periods of above-average performance.

We do expect this higher volatility environment to continue in the near term. We see lower potential that markets deliver a swift “V-shaped” recovery from recent weakness like we saw multiple times in 2023 and 2024. But even as volatility persists, we do see this volatility presenting investment opportunities.

Investing in a volatile environment does not require perfect market timing. We continue to add Quality names to our equity portfolios while avoiding purely defensive plays that are only likely to outperform in a recession.

Those investors who feel a little more daring can use the recent pullback in interest rates to add exposure to cyclicals. The rate-sensitive parts of the economy had been beaten down by the relentless upward march of Treasury yields, but lower rates without a recession may be just what sectors like homebuilders needed…assuming lumber tariffs don’t bite too hard.

Of course, holding a diversified portfolio also entails being prepared for the worst. Markets are pricing a greater chance the Fed will cut interest rates this spring, but this would not be a welcome development, in our view. Further monetary easing with inflation still well above target would only come amid a material degradation of the labor market.

Be careful what you wish for. Rooting for lower short-term rates is effectively rooting for disappointing data at this point. That is not our expectation, but high-quality bonds, which have rediscovered their diversification properties this year, are part of our strategic and tactical asset allocations just the same.

In short, we are not ready to throw in the towel (a towel being “the most massively useful thing an interstellar hitchhiker can have,” by the way) on this long-term bull market. But we are approaching the coming months with “just perfectly normal paranoia,” as we expect volatility to continue and 2025 to remain in our expected wide, choppy range. Daily market movements should not feel as harrowing as faster-than-light travel, but when they do, it’s important to have a plan.

IMPORTANT DISCLOSURES

The views and opinions included in these materials belong to their author and do not necessarily reflect the views and opinions of NewEdge Capital Group, LLC.

This information is general in nature and has been prepared solely for informational and educational purposes and does not constitute an offer or a recommendation to buy or sell any particular security or to adopt any specific investment strategy.

NewEdge and its affiliates do not render advice on legal, tax and/or tax accounting matters. You should consult your personal tax and/or legal advisor to learn about any potential tax or other implications that may result from acting on a particular recommendation.

The trademarks and service marks contained herein are the property of their respective owners. Unless otherwise specifically indicated, all information with respect to any third party not affiliated with NewEdge has been provided by, and is the sole responsibility of, such third party and has not been independently verified by NewEdge, its affiliates or any other independent third party. No representation is given with respect to its accuracy or completeness, and such information and opinions may change without notice.

Investing involves risk, including possible loss of principal. Past performance is no guarantee of future results.

Any forward-looking statements or forecasts are based on assumptions and actual results are expected to vary from any such statements or forecasts. No assurance can be given that investment objectives or target returns will be achieved. Future returns may be higher or lower than the estimates presented herein.

An investment cannot be made directly in an index. Indices are unmanaged and have no fees or expenses. You can obtain information about many indices online at a variety of sources including: https://www.sec.gov/answers/indices.htm.

All data is subject to change without notice.

© 2026 NewEdge Capital Group, LLC