This week we are providing our assessment of the third quarter S&P500 earnings season which could be appropriately summarized by AC/DC’s “Back In Black”, as the broad index has returned to profit growth after four straight quarters of declines. Many companies this quarter are “back on the track and beatin’ the flack” as the song lyrics go, highlighted by earnings growth that is coming in ahead of expectations, and earnings beats that are above average for a typical quarter. Tempering the enthusiasm for these results has been both the weak price reaction post earnings and the negative revisions to fourth quarter estimates which we will explore below.

The Headlines

- Better than expected: With 90% of the S&P500 having reported, Q3 2023 earnings results have thus far surpassed consensus expectations. Headline earnings growth of 3.7% YoY is well above the preseason consensus estimate which called for an earnings decline of -1.2% YoY.

- Not out of the woods yet: While Q3 has been a welcome surprise, and the first quarter of positive earnings growth since last year, earnings expectations for Q4 have been revised lower by 4pp over the past several weeks, reflecting slowing economic activity and continued pressures on corporate profitability.

- A preview of 2024?: Could the negative revisions to Q4 growth suggest more difficult times ahead? Expectations are high for 2024 with consensus earnings growth of 10% (up from just 1% growth in 2023). Nominal GDP growth is expected to fall below 5% next year, and to reach 10% calendar year earnings growth we’ll need to see continued margin expansion, which may be difficult to achieve as the tailwinds from price increases fade and input costs remain elevated.

Q3 2023: The End of the Earnings Recession

As we wrote last month in our third quarter earnings preview, it was possible that the third quarter would mark the end of the earnings recession that began in late 2022, and thus far corporate profits have delivered.

With 90% of the S&P500 having reported, it is clear earnings growth is now back in positive territory, on pace to rise 3.7% YoY, and well above the preseason consensus estimates of a decline of -1.2% YoY. Overall, 81% of companies have posted positive earnings surprises, which is above the 10-year average of 74%, and the highest percentage of beats in two years. In addition, companies that post earnings beats are exceeding estimates by an average of 7.1%, which is also above the 10-year average beat of 6.6%.

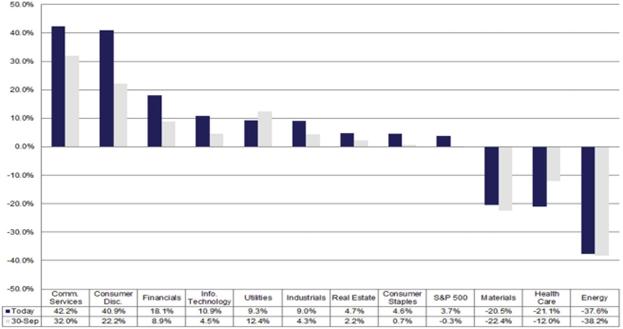

The largest earnings beats this quarter are coming from the Communications sector (EPS growth of 42% YoY vs. 32% expected), the Consumer Discretionary sector (EPS growth of 41% YoY vs 22% expected), the Financials sector (EPS growth of 18% YoY vs. 9% expected), and lastly, the Technology sector (EPS growth of 11% YoY vs 5% expected).

S&P 500 Earnings Growth YoY vs. Preseason Expectations: Q3 2023

Revenue Growth Remains Elusive

In terms of revenue growth, the story is not quite as convincing, and slower revenue growth is one of the main reasons why expectations for Q4 have been revised lower.

Third quarter revenues are on pace to rise just 2.0% YoY, exceeding the preseason estimate of +1.1% YoY, but only up marginally from last quarter. Thus far just 48% of companies have beat revenue expectations, which is below the 10-year average of 64%, and in aggregate companies are reporting revenues that are 0.7% above expectations, also below the average revenue beat of 1.3% over the past 10-years.

Half of S&P500 sectors have reported revenues that slowed sequentially and only 4 of 11 sectors posted YoY revenue growth that exceeded the average rate of inflation over the past year of 5%. Price increases helped drive double digit revenue growth in 2022, but this year consumers are being more selective and price sensitive, and as a result price increases are in many cases being offset by declining volumes.

Margins are Improving but Not for Everyone

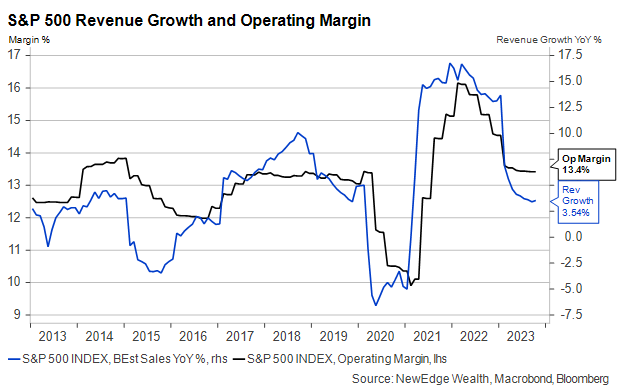

Turning to operating margins, S&P500 companies are expected to post sequential margin improvement for the first time in over a year. Average operating margins of 15.0% are up 0.5pp sequentially, however they are still down from 15.8% a year ago. The margin improvement this quarter has been primarily driven by expansion in the largest companies in the Technology and Communications sectors, which remain the two most profitable sectors in the index.

The biggest detractors from index level operating margins this quarter were the Healthcare and Industrials sectors. Both sectors were expected to be among the largest contributors to margin expansion in Q3, and their wide misses on profitability suggest these areas continue to be among the most pressured by rising input and energy costs.

Price Reactions Are Skewed to the Downside

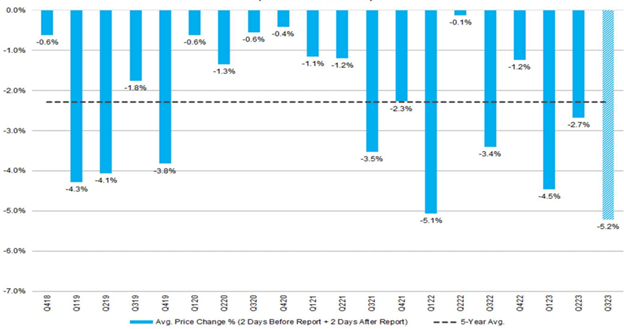

The average one-day price reaction to earnings reports this quarter has been mixed. Despite healthy earnings results, companies that post an earnings beat are enjoying a modest 0.8% gain, which is on par with 5-year average gains, while companies that post an earnings miss are being swiftly sent to the penalty box.

The average one-day price reaction for companies that miss earnings is -5.2%, more than double the 10-year average decline of -2.2%, and on pace for the worst quarterly earnings miss reaction in over a decade.

We attribute the weak price performance to a few factors: the unusually strong index performance and the lack of downside earnings revisions entering earnings season, and generally weaker guidance for the coming quarters. As a result, analysts have thus far cut their earnings growth expectations for Q4 to half of where they stood coming into the quarter, and consensus now expects earnings growth of 3.9% and revenue growth of 3.5% next quarter.

S&P 500 Negative EPS Surprises: Average Price Change %

Previewing 2024: Can the S&P500 Achieve Expectations of Double-Digit Earnings Growth?

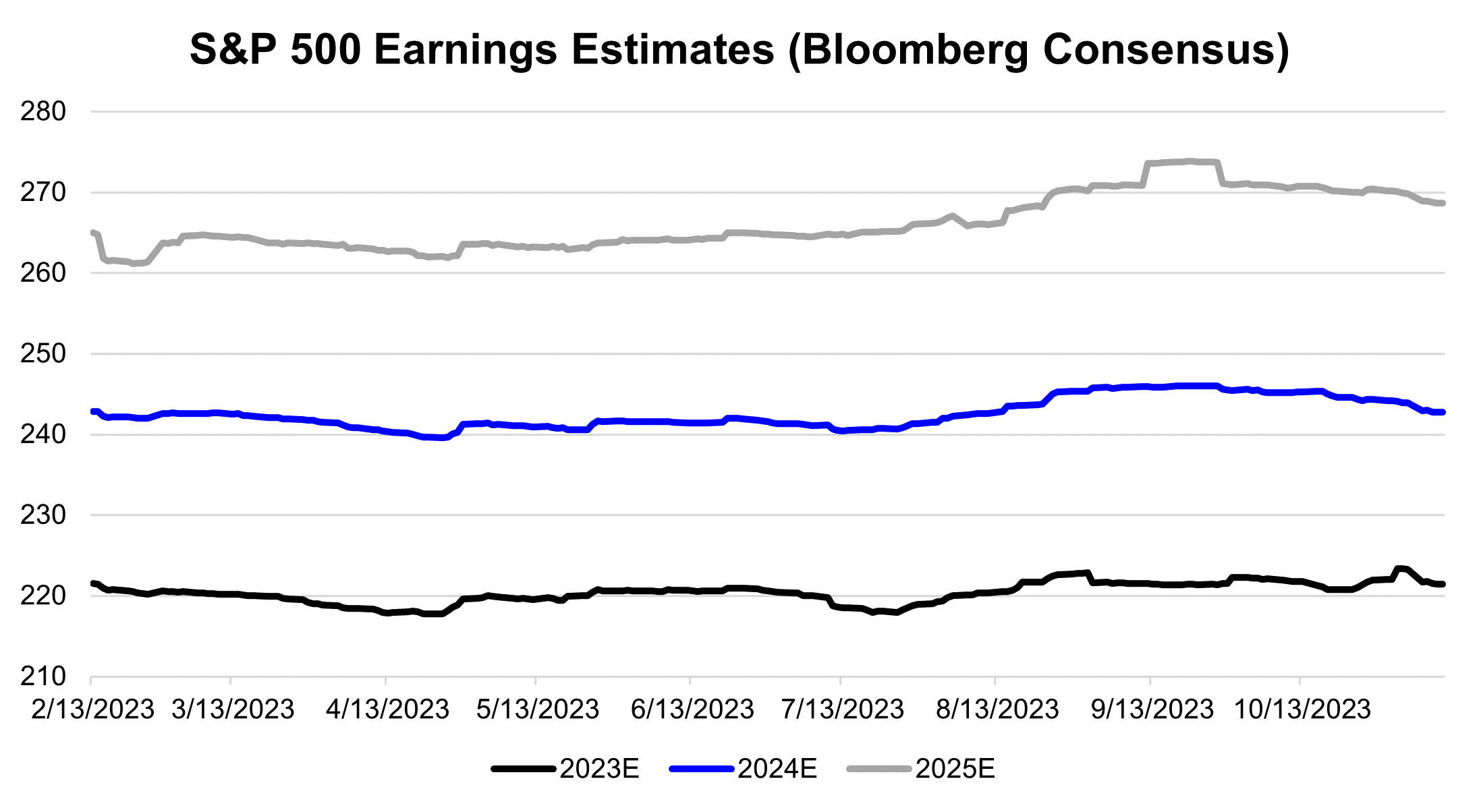

Consensus expectations for 2024 call for 10% earnings growth, and 5% revenue growth, boosted by healthy margin expansion to levels that the index only briefly touched in 2021 and 2022. This was an environment where corporate profitability benefitted from robust consumption, strong pricing power, and ample liquidity. While we don’t doubt companies can continue to find operational efficiency, there is a question if most of the “low hanging fruit” has been picked. As we edge closer to the new year, expectations have already started to decline, and consensus now expects earnings of $243 per share.

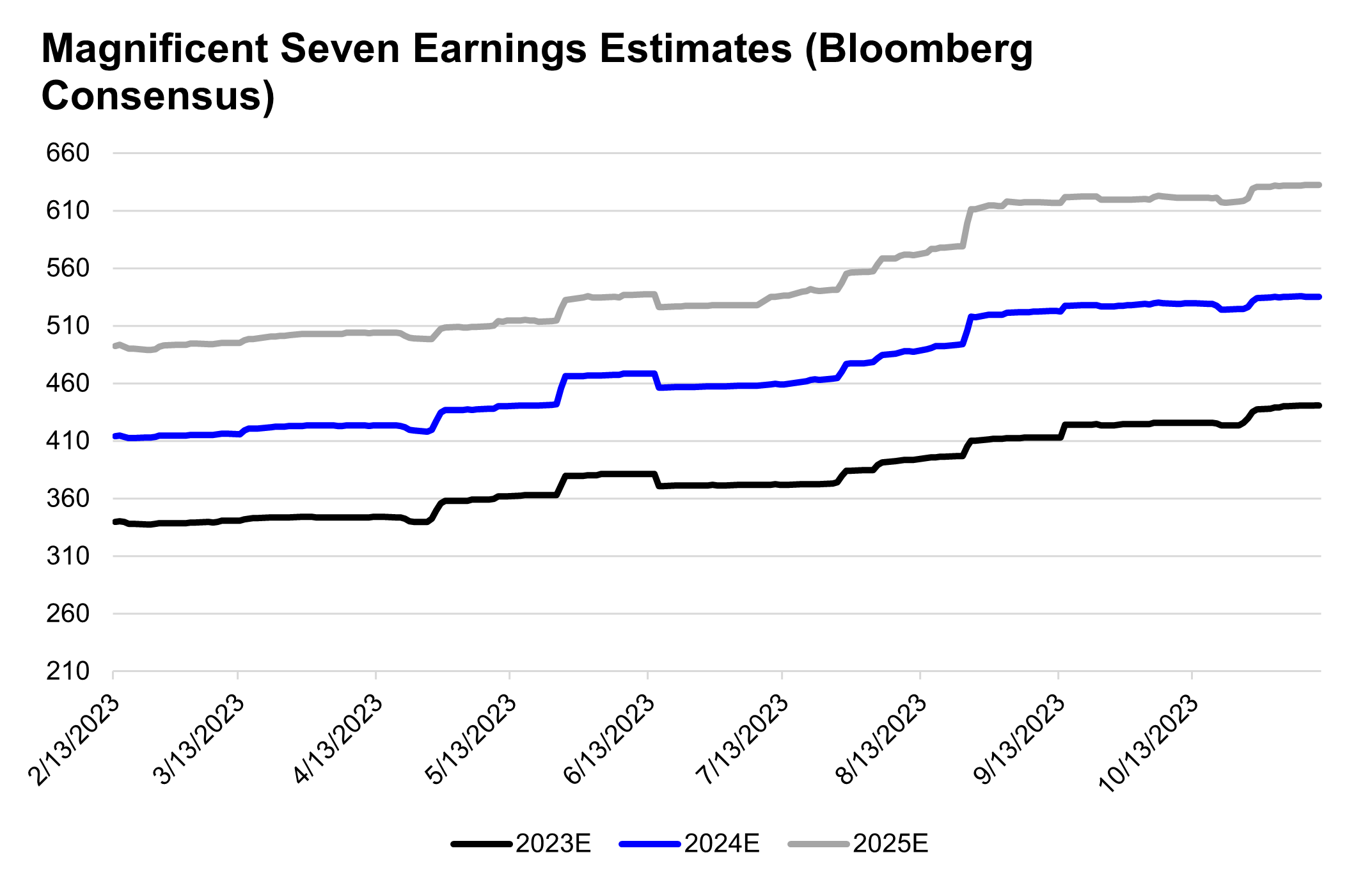

Conclusion & A Look at the Magnificent Seven

As we mentioned earlier, there is one part of the market that continues to show leadership in terms of profitability and performance, and it is the largest seven companies in the index. The Magnificent Seven stocks (Apple, Microsoft, Alphabet, Amazon, Nvidia, Meta, and Tesla), which comprise 28% of the index, continue to exhibit remarkable strength from both a performance and earnings revision standpoint. As of this week, the group is up 5% this quarter, and up over 90% this year, vastly outperforming the S&P 500.

This group is expected to post 33% earnings growth in 2023 and 21% earnings growth in 2024, and these expectations have increased by more than 10% in just the last three months and by 30% over the course of 2023. It is helpful to remember that over the course of 2022, Magnificent Seven EPS estimates were revised lower by ~20%, which created a lower bar to jump over this year.

Certainly, expectations are now high and while many of these companies have wide business moats and management teams adept at driving operational efficiency, we believe investors should remain selective in these names given their premium valuations and “higher bar” for earnings now that forecasts have been raised materially. Ultimately, the Magnificent Seven’s ability to remain market leaders may come down to their ability to exceed these lofty expectations.

Top Points of the Week

By Austin Capasso and Ben Lope

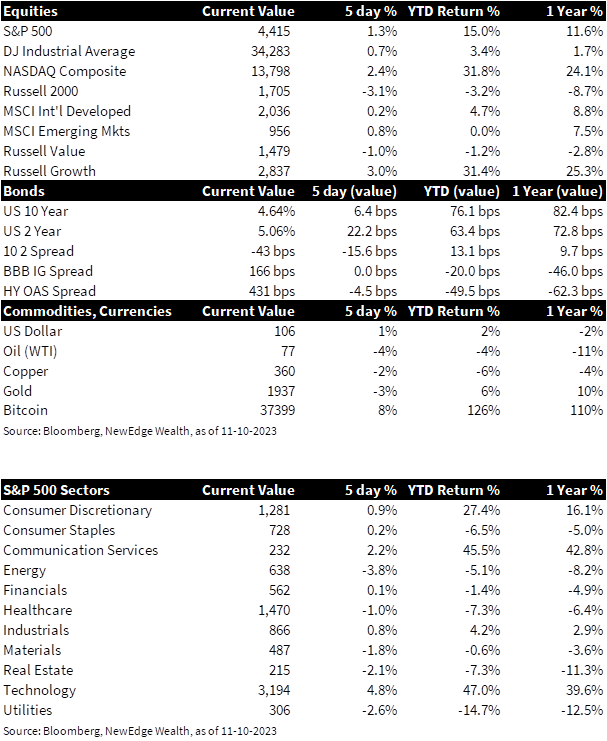

1. Equities – Global equities were mixed on the week. Within the US, the S&P 500 and Dow Jones Industrial Average ended about flat, while the tech-heavy Russell 1000 Growth and NASDAQ Composite indices were up by 1-1.5% Value and small cap stocks lagged on the week, with the Russell 1000 Value index down by just over 2% and the Russell 2000 index down over 4%. International stocks showed muted gains, with the MSCI EAFE and MSCI EM indices each up under 1%.

2. Treasury Curve Inverts Further – Yields on 2-year Treasury bonds increases nearly 20bps on the week, while yields on 10 year bonds stayed mostly flat, leading the 2-10 year Treasury yield curve to reach its most inverted level in a month. Despite the move, the yield curve’s level of inversion is still less than half of what was observed in periods of March and July, where curve was inverted by over 100bps.

3. Oil Continues to Move Lower – The price per barrel of Brent crude oil briefly dipped below $80 this week before a 2% rally on Friday had them close slightly above this level. Oil prices still declined on the week by nearly 5%, continuing a three-week slide. Analysts point the price movement as evidence that investors are currently more concerned about easing global demand than the potential for supply disruptions caused by the turmoil in the Middle East.

4. 30-year Treasury Auction was a Disaster – Yesterday’s 30-year Treasury auction was very poorly bid on by investors and served to be a big macro event for markets. It seems yields were not high enough for investors to be enticed into purchasing bonds that far down the yield curve. Nearly 25% of the 30-year debt was purchased by primary dealers, which is nearly double the average in the past year. The auction gave a clear indication of weak demand for long term government paper and acted as the catalyst for a move higher in rates.

5. Summary of Fed Speak This Week – This has been a very active week of Fed speak after hearing speeches from Powell, Kashkari, Waller, Goolsbee, Logan, and others. Messaging from each member has been very similar. Seems the Fed is planning to push back on the idea of implementing future rate cuts, mentioning it is too early to declare victory on inflation. The Fed will continue its “higher for longer” rate regime and the idea of a possible rate hike into year-end and 2024 with hopes of reaching its 2% inflation target. This is placing pressure on the yield curve and points to better opportunities on the short end as opposed to the long end.

6. US Jobless Claims Continue to Remain Low – The US employment market has continued to remain resilient. The latest jobless claims data dipped to 217,000, which is still a very low level and one that is typical to see in a strong jobs market. That reading is a decline of just 3,000 from last week’s revised 220,000. Although the jobs market remains stable, it has cooled off a bit as a result of the United Auto Workers strike.

7. UK Avoids Recession, But There Still Remain Concerns for Europe – The trend throughout European economies seems to call for stagflation. The latest Q3 GDP reading in the UK showed +0.2%, which indicates no growth for the quarter. This mirrors the +0.1% increase in the latest GDP reading of the Eurozone. Last quarter, England’s services sector showed contraction, their manufacturing sector slumped, and their housing activity dragged after interest rates were raised to the highest level since 2008. Growth in Europe remains a large concern to investors as they face fears of stagflation.

8. CPI and PPI in China Show Deflation – China’s for Consumer Price Index (CPI) and Producer Price Index (PPI) both showed price swings for the month of October. Chinese CPI shrank 0.2% year-over-year in October, more than the expected 0.1% decline. China’s PPI declined 2.6% last month, falling for the 13th month in a row. Seems that China’s real estate concerns, which make up 30% of their economy, are hurting consumer demand and overall domestic growth.

9. Q3 Earnings Update – Over 90% of S&P 500 companies have reported Q3 earnings, and thus far 81% of these companies are beating earnings estimates and 59% are beating revenue estimates. Notable names reporting next week include Home Depot (HD), Cisco Systems (CSCO), and Walmart (WMT).

10. The Week Ahead – Next week poses a huge week of data for the US. We will get insight into inflation through US CPI and PPI, a look into the consumer in US retail sales data, as well as a gage on the Federal budget, consumer sentiment, US trade, and the health of manufacturing and services sectors. We will be monitoring this data very closely and any implications it may have for markets.

IMPORTANT DISCLOSURES

Abbreviations/Definitions: Brent blend: a blend of crude oil extracted from oilfields in the North Sea between the United Kingdom and Norway. It is an industry standard because it is “light,” meaning not overly dense, and “sweet,” meaning it’s low in sulfur content; CPI: Consumer Price Index; EPS: earnings per share; Goolsbee: Austan Goolsbee, President of the Federal Reserve Bank of Chicago; Kashkari: Neel Kashkari, President of the Federal Reserve Bank of Minneapolis; Logan: Lorie Logan, President of the Federal Reserve Bank of Dallas; Powell: Jerome Powell, Chair of the Board of Governors of the Federal Reserve System; PPI: Producer Price Index; Waller: Christopher Waller, member of the Federal Reserve Board of Governors.

Index Information: All returns represent total return for stated period. S&P 500 is a total return index that reflects both changes in the prices of stocks in the S&P 500 Index as well as the reinvestment of the dividend income from its underlying stocks. Dow Jones Industrial Average (DJ Industrial Average) is a price-weighted average of 30 actively traded blue-chip stocks trading New York Stock Exchange and Nasdaq. The NASDAQ Composite Index measures all NASDAQ domestic and international based common type stocks listed on the Nasdaq Stock Market. Russell 2000 is an index that measures the performance of the small-cap segment of the U.S. equity universe. MSCI International Developed measures equity market performance of large, developed markets not including the U.S. MSCI Emerging Markets (MSCI Emerging Mkts) measures equity market performance of emerging markets. Russell 1000 Growth Index measures the performance of the large-cap growth segment of the US equity universe. It includes those Russell 1000 companies with relatively higher price-to-book ratios, higher I/B/E/S forecast medium term (2 year) growth and higher sales per share historical growth (5 years). The Russell 1000 Value Index measures the performance of the large cap value segment of the US equity universe. It includes those Russell 1000 companies with relatively lower price-to-book ratios, lower I/B/E/S forecast medium term (2 year) growth and lower sales per share historical growth (5 years). The BBB IG Spread is the Bloomberg Baa Corporate Index that measures the spread of BBB/Baa U.S. corporate bond yields over Treasuries. The HY OAS is the High Yield Option Adjusted Spread index measuring the spread of high yield bonds over Treasuries. The MSCI EAFE Index is designed to represent the performance of large and mid-cap securities across 21 developed markets, including countries in Europe, Australasia and the Far East, excluding the U.S. and Canada. The Index is available for a number of regions, market segments/sizes and covers approximately 85% of the free float-adjusted market capitalization in each of the 21 countries.

Sector Returns: Sectors are based on the GICS methodology. Returns are cumulative total return for stated period, including reinvestment of dividends.

The views and opinions included in these materials belong to their author and do not necessarily reflect the views and opinions of NewEdge Capital Group, LLC.

This information is general in nature and has been prepared solely for informational and educational purposes and does not constitute an offer or a recommendation to buy or sell any particular security or to adopt any specific investment strategy.

NewEdge and its affiliates do not render advice on legal, tax and/or tax accounting matters. You should consult your personal tax and/or legal advisor to learn about any potential tax or other implications that may result from acting on a particular recommendation.

The trademarks and service marks contained herein are the property of their respective owners. Unless otherwise specifically indicated, all information with respect to any third party not affiliated with NewEdge has been provided by, and is the sole responsibility of, such third party and has not been independently verified by NewEdge, its affiliates or any other independent third party. No representation is given with respect to its accuracy or completeness, and such information and opinions may change without notice.

Investing involves risk, including possible loss of principal. Past performance is no guarantee of future results.

Any forward-looking statements or forecasts are based on assumptions and actual results are expected to vary from any such statements or forecasts. No assurance can be given that investment objectives or target returns will be achieved. Future returns may be higher or lower than the estimates presented herein.

An investment cannot be made directly in an index. Indices are unmanaged and have no fees or expenses. You can obtain information about many indices online at a variety of sources including: https://www.sec.gov/answers/indices.htm.

All data is subject to change without notice.

© 2026 NewEdge Capital Group, LLC