Topic Focus: Mega IRAs, Roth Conversions, and Backdoor Roth IRAs

On November 2nd, 2021, Congress released the most recent tax provisions for the Build Back Better Act, including several proposed changes to retirement plans. Amongst the changes are those that directly target contributions to retirement accounts with large balances, limit future Roth Conversions and potentially eliminate the Backdoor Roth IRA strategy. With two months remaining in the calendar year, NewEdge Wealth would like to highlight these potential adjustments so those that can, consider their ability to convert Traditional IRA balances to their Roth counterparts. Specific to these strategies, the changes include:

Roth Conversion: The recent House and Ways Committee announcement could eliminate “Roth conversions for both IRAs and employer-sponsored plans for single taxpayers (or taxpayers married filing separately) with taxable income over $400,000, married taxpayers filing jointly with taxable income over $450,000, and heads of households with taxable income over $425,000 (all indexed for inflation). This provision applies to distributions, transfers, and contributions made in taxable years beginning after December 31, 2031.”[1]

Backdoor Roth IRA Contribution: “Furthermore, this section prohibits all employee after-tax contributions in qualified plans and prohibits after-tax IRA contributions from being converted to Roth regardless of income level, effective for distributions, transfers, and contributions made after December 31, 2021.”[2]

For educational purposes, our team has organized a “need to know” summary and how to guide on executing these strategies in a timely manner. While useful, our team recommends all clients coordinate this strategy with their CPA, attorney, and the NewEdge Wealth team. Executing a Backdoor Roth IRA or Roth Conversion requires proper timing and coordination.

1) What is a Roth IRA?

A Roth IRA is a self-directed retirement account that acts as a tax advantaged vehicle for retirement savings. While a traditional IRA offers tax deferred growth until distributions are made, a Roth IRA offers tax-free growth, is not subject to Required Minimum Distributions (RMDs) during your lifetime and allows for tax-free withdrawals for qualified distributions (money withdrawn after age 59 ½). In addition, while those who inherit your Roth IRA may be subject to RMDs, they won’t have to pay any federal income tax on their withdrawals if the account has been established for at least five years.

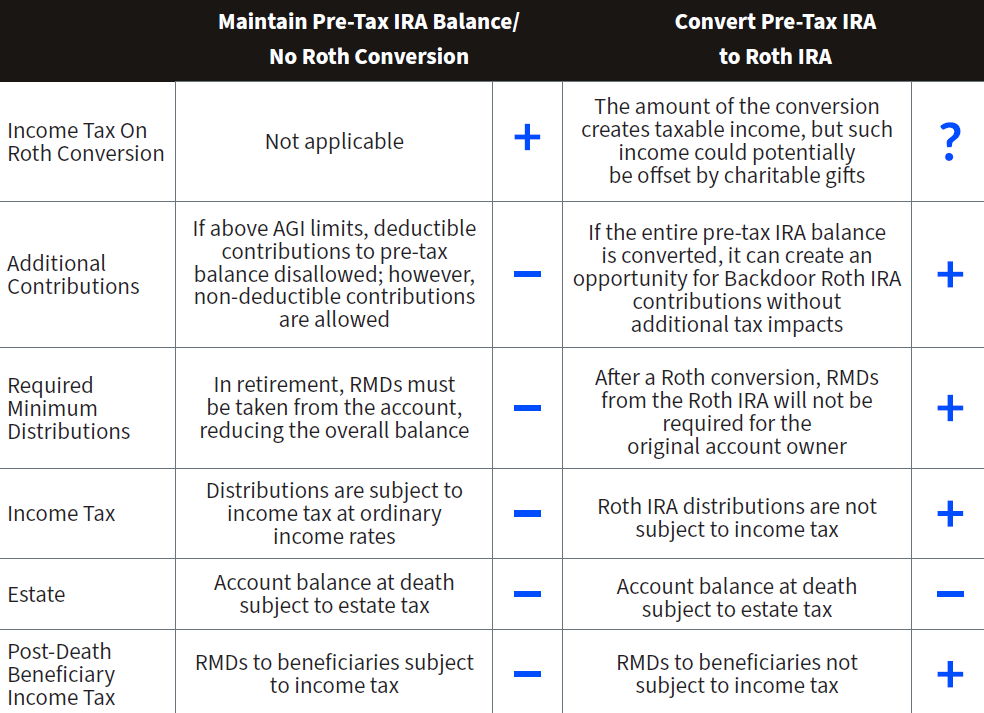

2) What are the differences between a Traditional and Roth IRA?

Source: Dimeo Schneider, 2021 Financial Planning Guide

3) Who can contribute to a Roth IRA?

For 2021, individuals may contribute up to $6,000, $7,000 if age 50 or older, per year directly to a Roth IRA. However, keep in mind your eligibility to contribute to a Roth IRA is based on your Modified Adjusted Gross Income (MAGI).[3] Taxpayers filing as single, head of household, or married filing separately may contribute the full amount if MAGI is less than $125,000. This contribution amount reduces as MAGI increases, and fully phases out at $140,000. [4] There is a phase out period where contributions decrease for a MAGI between $125,000-$140,000 and a MAGI over $140,000 completely restricts one from contributing. Married filing jointly taxpayers may contribute the full $6,000 if MAGI is less than $198,000. This contribution amount reduces as MAGI increases, and fully phases out at $208,000.[5]

4) What is a Roth Conversion?

A Roth Conversion is a strategy that allows high-income earners who can’t contribute directly to a Roth IRA to contribute indirectly. To execute, the strategy simply requires an administrative step where one transfers a Traditional IRA balance to a Roth IRA account. When done correctly, the conversion will allow one to benefit from the enhanced tax advantages that a Roth IRA offers. A popular strategy known as a Backdoor Roth IRA Contribution involves one additional step, where an individual makes a non-deductible (after-tax) contribution to a Traditional IRA and then converts the contribution to a Roth IRA.

5) Can I convert a traditional IRA to a Roth IRA?

Anyone, regardless of income, can convert a Traditional IRA to a Roth IRA. Deciding whether to convert to a Roth IRA also depends on several variables, including your current tax rate now versus later, the potential tax bill you may have to pay to convert, and the future plans for your estate. Also, a conversion is permanent—you can’t revert the money back to a traditional IRA if no longer wish to pay a tax bill. Other areas of consideration include:

A) The Traditional to Roth conversion may be treated as ordinary income for the amount converted.

B) Pro Rate Rule and IRA Aggregation can dilute the value of backdoor conversion. This point can come into play if you have other retirement accounts, IRAs, and deductible contributions are being converted.

C) Potential Step Transaction Exposure

D) Tax and Legislative Reform

6) Can I do a partial conversion to a Roth?

Yes. However, if you have multiple non-Roth IRAs, any conversion will be considered to have been made from all the IRAs on a proportionate basis. Also, if you have both deductible and non-deductible contributions held in your non-Roth IRAs, any conversion will be deemed to be taken pro-rata from each contribution type. This is also an important consideration if you are considering a Backdoor Roth IRA contribution, as the pro-rata rule would apply as well.

7) Are there better times to do a Roth Conversion?

In the event taxable income will be recognized during the conversion, individuals should look to deploy this strategy during lower-than-normal income years (i.e. retirement years, before receiving social security income and RMDs take effect). In addition, the coupling of conversions with charitable donations can offset the potential tax liability and lower the overall tax impact to one’s income or asset base.

Source: Dimeo Schneider, 2021 Planning Guide

Monitoring Capitol Hill – Additional Tax Provisions to Consider

Negotiations on Capitol Hill remain fluid, so it is wise for clients to appreciate how certain items may re-emerge or be omitted before the final legislation is passed. Additional provisions related to retirement accounts that remained in the October proposal include:

- New Contribution Limits for Retirement Accounts: The legislation would prohibit additional contributions to Individual Retirement Accounts and Defined Contribution Plans that account values exceed $10M as of the end of the prior taxable year. This limit would apply to single taxpayers (or taxpayers married filing separately) with taxable income over $400,000, married taxpayers filing jointly with taxable income over $450,000, and heads of households with taxable income over $425,000 (all indexed for inflation). This provision would become effective for tax years beginning after December 31st, 2028.

- Accelerated and Increased Required Minimum Distributions (RMDs): Combined retirement account balances that have an excess of $10M at the end of a taxable year would now be subject to required minimum distributions, regardless of Roth characterizations. This provision would apply to tax filers whose income exceeds the thresholds outlined above and would require a 50% distribution value for any excess balance over $10M. In addition, combined retirement account balances over $20M would be subject to a 100% distribution requirement for any amount that exceeds $20M. The 50% distribution rule would still apply to these scenarios after the 100% distribution requirement is met. This provision would become effective for tax years beginning after December 31st, 2028.

As for the omitted items, the latest proposal excluded:

- IRA Investment Conditions: The bill would prohibit an IRA from holding any security if the issuer of the security requires certain asset or education limits (e.g., accredited investors, qualified purchaser, security representative licenses, etc.). In result, alternative investments such as hedge funds, private equity funds, or direct investments would be disallowed as investment options. IRAs holding such investment would lose their IRA status. This provision would become effective for tax years beginning after December 31st, 2021, but there is a 2-year transition period IRAs already holding these investment types.

- Entity Owned IRA Assets: Today, IRA owners cannot invest IRA assets in a corporation, partnership, trust, or estate, which he or she has a 50% or greater interest. The bill would decrease this threshold to 10%. This section generally takes effect for tax years beginning after December 31, 2021, but there is a 2-year transition period for IRAs already holding these investments.

Sources

IMPORTANT DISCLOSURES

The views and opinions included in these materials belong to their author and do not necessarily reflect the views and opinions of NewEdge Capital Group, LLC.

This information is general in nature and has been prepared solely for informational and educational purposes and does not constitute an offer or a recommendation to buy or sell any particular security or to adopt any specific investment strategy.

NewEdge and its affiliates do not render advice on legal, tax and/or tax accounting matters. You should consult your personal tax and/or legal advisor to learn about any potential tax or other implications that may result from acting on a particular recommendation.

The trademarks and service marks contained herein are the property of their respective owners. Unless otherwise specifically indicated, all information with respect to any third party not affiliated with NewEdge has been provided by, and is the sole responsibility of, such third party and has not been independently verified by NewEdge, its affiliates or any other independent third party. No representation is given with respect to its accuracy or completeness, and such information and opinions may change without notice.

Investing involves risk, including possible loss of principal. Past performance is no guarantee of future results.

Any forward-looking statements or forecasts are based on assumptions and actual results are expected to vary from any such statements or forecasts. No assurance can be given that investment objectives or target returns will be achieved. Future returns may be higher or lower than the estimates presented herein.

An investment cannot be made directly in an index. Indices are unmanaged and have no fees or expenses. You can obtain information about many indices online at a variety of sources including: https://www.sec.gov/answers/indices.htm.

All data is subject to change without notice.

© 2026 NewEdge Capital Group, LLC