You may have grown up hearing about “the family trust” or “the family partnership,” or estate plans designed by your parents. Words like legacy and stewardship might already feel familiar. Yet as the next generation in your 20s, 30s, or 40s, you may now be wondering:

What does my financial future look like for me, my children, and the generations to come?

Even with family wealth in the background, many high-earning young professionals are determined to forge their own path- creating security, independence, and opportunities that reflect their values. For those balancing demanding careers, raising children, and taking on new responsibilities, now is the ideal time to establish a clear, intentional wealth strategy.

Defining Your Vision of Success

Success is deeply personal. It may mean achieving financial independence, building wealth separate from the family through your own earnings and investments, funding your children’s education without overreliance on trust structures, traveling without limits and pursuing unique experiences, taking on leadership roles in family enterprises or foundations, or making meaningful charitable gifts and leaving a lasting legacy. Now is the time to begin clarifying your goals, understanding your full financial picture, and designing a plan that adapts as your life and wealth evolve.

Grounding Wealth in Your Values

Wealth strategy isn’t only about numbers—it’s about what those numbers represent. Money is a tool, and when used intentionally, it can help you shape the life you want to live and reflect the values you want to express.

For some, that means embracing the values passed down through the family, such as philanthropy, entrepreneurship, or stewardship of a family business. For others, it may mean carving out new priorities—whether that’s sustainability, social impact investing, or creating experiences that strengthen family bonds.

As you think about your own wealth journey, ask yourself:

- Which family values do I want to carry forward?

- Where do I want to establish my own path?

- How can I align financial decisions with what matters most to me and my children?

By grounding your planning in values, you create a framework for making decisions that not only grow and protect wealth but also give it meaning. Wealth becomes more than a financial resource—it becomes a tool for building a life of purpose and legacy.

The Core Pillars of Planning for Next Gen Wealth

Most young professionals’ priorities fall into three overlapping areas: budgeting to build wealth, positioning assets through strategic investing and retirement planning, and protecting their future with estate and legacy planning. You don’t need to tackle everything at once—start with what matters most today, and over time these pieces will come together into a unified long-term strategy.

1. Cash Flow and Budgeting: A Foundation for Flexibility

Budgeting isn’t about restriction- it’s about aligning your spending and saving with your goals. The goal is to ensure your spending and saving reflect your priorities and values, while also creating flexibility for future opportunities. Building consistent habits now allows you to meet near-term needs, fund long-term goals, and preserve wealth across generations.

The first step is to determine why you want a budget. Clarifying your “why” makes it easier to stay motivated and on track. Do you want to simplify complex income streams, ensure lifestyle spending is sustainable, reduce financial friction with a spouse or family, or continue to build wealth your own way, or build a framework for teaching the next generation? Defining the purpose of a budget keeps you motivated and provides a roadmap for decision-making.

Step One: Know Your Income

For ultra high net worth families, the challenge is often the complexity of income streams. Consider all sources such as salary, bonuses, equity compensation, investment income, or trust distributions.

Tip: If income is irregular, “pay yourself a salary” based on your average or your worst-case month. This reduces overspending risk. Automating transfers into separate accounts—spending, savings, and giving—creates smoother cash flow management.

Step Two: Understand Your Expenses

Gaining visibility into your spending habits is key to building a solid liquidity analysis. Start by tracking your expenses for at least 30 days to see where your money is going. There are several ways to do this:

- Cash Flow Worksheet – Your NewEdge Wealth advisor can provide a template to map out your inflows and outflows.

- Digital Tools – Platforms like eMoney (available through your advisor) or apps such as Mint and PocketGuard can help you automatically categorize and track spending.

- Review Statements – Break your spending into fixed expenses (housing, food, transportation) and discretionary expenses (entertainment, vacations, hobbies).

Finally, don’t forget to account for one-time or irregular expenses, like annual insurance premiums, holiday gifts, or family vacations. These can be easy to overlook but have a big impact on your overall budget.

Step Three: Identify and Prioritize Goals

Clear goals bring structure to the strategy you put in place for your wealth. Start by writing down your goals across different time horizons:

- Short-term (1-3 years) – A vacation, purchasing a car, or home renovation.

- Mid-term (3-7 years) – Paying down debt, building an emergency fund, or saving for a new home.

- Long-term (7+ years) – Including funding your children’s education, preparing for retirement, or legacy creation.

Be as specific as possible and assign target dates to each goal. Putting your goals in writing, with clear timelines, not only helps you measure progress but also increases accountability—making it more likely you’ll follow through.

Step Four: Decide How Much to Save and Choose a Budget Framework

Once you’ve identified your goals, the next step is to decide how much to set aside and choose a structure that works for you. A few practical approaches include:

- Zero-Based Budgeting – Assign every dollar a purpose each month (housing, debt repayment, savings, investments, lifestyle). At the end of the month, your income minus expenses should equal zero. Action item: List your monthly income, then allocate every dollar until nothing is left unassigned.

- 50/30/20 Rule – Allocate 50% of income to necessities (housing, food, transportation), 30% to lifestyle wants (entertainment, travel), and 20% to savings and debt repayment. Action item: Run your monthly numbers through this formula to see if you’re in balance or need adjustments.

- Bucket Planning – Separate personal wealth from family wealth, dividing money into different “buckets” aligned with time horizon:

- Short-term (1–3 years) – Keep readily available resources for emergencies, household needs, or near-term goals.

- Mid-term (3–7 years) – Designate funds for priorities such as a property upgrade, tuition, or other predictable expenses.

- Long-term (7+ years) – Use long-range structures—such as retirement accounts, trusts, or family entities—to support growth, legacy, and wealth transfer.

- Protection Overlay – Safeguard your plan by regularly reviewing insurance coverage, legal structures, and premarital planning to protect both personal and family wealth.

Common Mistakes to Avoid

- Saving aggressively for retirement while neglecting near-term needs, leading to premature withdrawals and penalties.

- Forgetting to plan for irregular but predictable expenses such as property taxes, tuition, insurance premiums, or vacations.

- Overcomplicating the system—a good budget should be easy to track and maintain.

- Failing to revisit your budget annually or when life changes (new job, marriage, children).

2. Strategic Investing and Retirement Planning

A common question is, “Where should I invest first?” While there’s no one-size-fits-all answer, high earners often follow a broad sequence to ensure liquidity, tax efficiency, and multigenerational impact:

- Liquidity – Maintain 6–12 months of core lifestyle expenses in cash equivalents to preserve flexibility in all market environments.

- Debt Management – Pay down high-interest debt, but evaluate family-structured loans.

- Retirement Accounts – Maximize tax-advantaged contributions and employer matches where available, but also consider how these accounts integrate with broader estate planning goals.

- Education Funding – With the continued rise of higher-education costs, many families prioritize education savings early. Establishing 529 Plans can be highly effective, especially when coordinated with grandparents who wish to contribute and simultaneously reduce their taxable estates. More advanced structures, including trusts, can also be used to support educational legacies. For a deeper dive, see our whitepaper, Maximizing College Savings with 529 Plans.

- After-Tax Brokerage Accounts – Surplus cash flow can be directed into taxable investment accounts to pursue mid- and long-term goals. At this stage, ultra high net worth families often implement advanced strategies such as irrevocable trusts, family LLCs, or other wealth transfer strategies to shift appreciation outside the estate and strengthen generational planning.

Most use a combination of these steps simultaneously. For example, you might contribute to a retirement plan to capture your match while building your emergency fund. Once the fund is established, you can increase retirement contributions and fund brokerage or education accounts to support long-term goals.

Why Start Now?

Compounding is powerful. Early investing not only magnifies long-term wealth creation but also provides flexibility, optionality, and the ability to fund philanthropic or family goals on your own terms. Your NewEdge Wealth team can help determine the right asset mix and investment selections for your goals and risk profile.

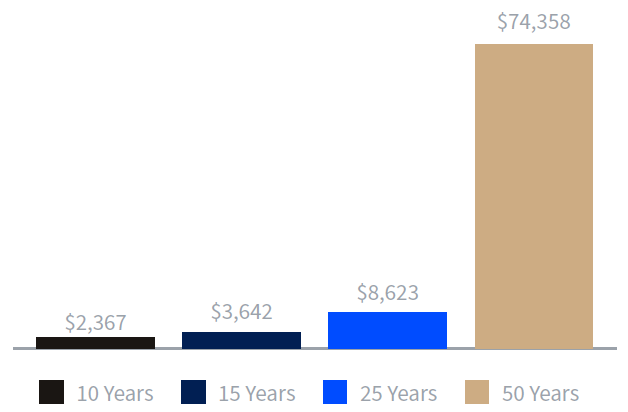

The Power of Investing: Understanding the Compound Effect

What does $1,000 grow to in 50 years, if we invest it at 9% compound interest?…in 10 years, that $1,000 grows to $2,367

…in 15 years, that $1,000 grows to $3,642

…in 25 years, that $1,000 grows to $8,623

…in 50 years, that $1,000 grows to $74,358

For ultra high net worth families, these principles apply at scale: disciplined early planning turns modest annual allocations into multigenerational capital.

Retirement Planning: Why It Matters Now?

It might feel far away, but the earlier you start, the more powerful compounding becomes. Even modest contributions in your early years can snowball into significant savings. High earners often have access to multiple retirement savings opportunities. The right approach depends on your compensation, benefits, and tax situation.

Contribution Levels

- Always take advantage of employer matches if available—it’s essentially “free money.”

- Incremental increases of 1–2% annually can have a significant long-term impact.

Account Types

- 401(k) Plans – 2025 contribution limit of $23,500 ($31,000 if age 50+).

- Self-employed Options – SEP and SIMPLE IRAs offer higher contribution limits for entrepreneurs.

- Traditional and Roth IRAs – $7,000 annual limit ($8,000 if 50+). Roth IRAs grow tax-free, and Traditional IRAs allow tax-deferred growth. If neither you nor your spouse participates in an employer-sponsored retirement plan, your Traditional IRA contributions are fully deductible regardless of income. Otherwise, deductibility may be subject to income limits.

- Backdoor Roth IRAs – A strategy for high earners who exceed income thresholds.

- Defined Benefit or Cash Balance Plans – Allow for larger, tax-deferred contributions, often ideal for business owners or highly compensated professionals.

- Mega Backdoor Roth contributions – Available through certain employer plans, significantly expanding Roth savings potential.

Additional Considerations

- Healthcare Planning – Use Health Savings Accounts (HSAs) and Flexible Spending Accounts (FSAs) to manage medical expenses tax-efficiently.

- Equity Compensation – RSUs, stock options, and carried interest can be powerful wealth builders but require strategic planning to minimize tax exposure.

3. Protecting Your Legacy: Estate, Premarital, and Insurance Planning

Estate planning is not only for later in life—it’s about making intentional decisions now to protect yourself, your family, and your legacy. The process begins with a net worth statement, which helps you understand your assets, liabilities, and overall financial picture. For guidance on the essential documents everyone should have once they turn 18, see our whitepaper Estate Planning Your Child Needs Once They Turn 18.

A comprehensive estate plan should:

- Address complex assets and structures, including family enterprises, closely held businesses, concentrated stock positions, and trusts with powers of appointment or unique provisions.

- Keep beneficiary designations aligned across accounts and entities to avoid conflicts or unintended outcomes.

- Integrate life insurance strategically to provide liquidity for estate taxes, equalize inheritances, and safeguard legacy assets from forced sales.

- Plan for digital and intellectual property alongside traditional assets.

- Coordinate multigenerational plans to ensure consistency with parents, siblings, or children who may already have established trusts or structures.

- Thoughtfully select fiduciaries (trustees, executors, guardians) with the skills and temperament to manage both assets and family relationships.

- Incorporate premarital planning as a form of financial protection. By proactively addressing inherited and gifted wealth, families can align marital agreements with broader legacy objectives while preserving harmony between spouses and across generations.

Insurance

Insurance is a critical part of wealth preservation and estate planning. Properly structured policies can provide tax-efficient liquidity as a form of income replacement, protect illiquid assets (such as real estate, art, or business interests), help mitigate estate taxes, and reinforce family security. Key considerations include:

- Life Insurance – Provides income replacement, funds estate tax obligations, and facilitates wealth transfer.

- Disability Insurance – Protects your earning power in case of illness or injury.

- Property & Casualty Insurance – Essential for safeguarding residences, yachts, aircraft, collections, and other lifestyle assets.

Insurance is important for both income earners and non-income earners, ensuring your family is protected no matter your circumstances.

Your NewEdge team will work alongside your estate planning attorney to design a plan tailored to

your needs. If you don’t already have counsel in place, we can recommend experienced attorneys to partner with.

Pulling It All Together

Building and preserving wealth for your family is not about following a rigid formula. It’s about defining what success looks like for you, making intentional choices, and putting strategies in place that evolve as life unfolds.

For ultra high net worth families, the challenge can be balancing individual independence with the broader family structures in place. Each pillar of planning—cash flow, investing, estate & legacy—interlocks like a puzzle. By starting early, you gain optionality, control, and confidence, whether wealth comes from your own career, your family, or both.

Your NewEdge team will guide you, connect the right professionals, and ensure your plan reflects your values while fitting seamlessly into the broader family framework. To explore how to identify and prioritize your values in planning, see our whitepaper Valuing Your Values.

The earlier you begin, the more options and flexibility you have. Your NewEdge team is here to guide you, connect the right professionals, and help you shape a financial future that truly reflects your vision and build your own intentional legacy.

Frequently Asked Questions

How do I balance career income with trust distributions?

Create a system where trust distributions supplement—not define—your lifestyle. Your advisor can help you “separate streams” so earned income supports independence while inherited wealth is positioned for long-term growth.

Do I need an estate plan if I’m already a beneficiary of one?

Yes. You need your own will, power of attorney, healthcare directive, and possibly a revocable trust to ensure independence and clarity for your family.

Should I set up a revocable trust now?

If you have children, want to avoid probate, or ensure your wealth transfers smoothly to chosen individuals or charities, a revocable trust may be worth considering. It offers control and flexibility—enabling you to manage your assets during your lifetime, designate someone to step in if you become incapacitated, and clearly outline how your assets are distributed after your death. Different types of irrevocable trusts can also be useful for tax planning if your wealth is expected to grow significantly.

What about premarital planning?

For ultra high net worth families, premarital planning is a crucial safeguard. Think of it as a form of insurance: in the event of death or divorce, if a prenuptial agreement isn’t in place, the state law will determine how your assets are divided. A prenup allows you and your spouse to make those decisions yourselves and be intentional about specific assets. These agreements are highly customizable—they don’t have to be “all or nothing.” Well-crafted prenuptial agreements and trust structures protect both spouses while ensuring that family wealth isn’t unintentionally converted into marital property.

When should I start thinking about philanthropy or giving back?

You don’t need to wait until later in life—philanthropy can begin at any stage. From small annual gifts to Donor-Advised-Funds (DAFs) or family foundations, giving back can be built into your plan today.

Work with your NewEdge advisor to ensure you are gifting the most optimally positioned asset from a tax perspective.

Should I give independently or as part of family philanthropy?

It’s a balance of both. Creating your own DAF or foundation gives you independence to express your values directly. On the other hand, participating in family philanthropy may allow you to help direct larger grants to organizations and can be a meaningful way to collaborate, strengthen relationships, and align shared values across generations.

How do I ensure giving fits into my bigger plan?

No matter the path you choose, it’s important to consider how philanthropy interacts with your broader goals—whether that’s simply giving back, reducing income taxes, mitigating estate taxes, or a combination of all three.

What’s the right amount to save towards retirement in my 20s, 30s, or 40s?

There isn’t one number, but saving at least 15–20% of income is a strong target. The earlier you start, the more flexibility you’ll have later as you build your personal wealth.

Should I open a 529 Plan for my kids or wait until grandparents decide what they’ll fund?

It’s often smart to open a plan early to maximize tax-free growth and take advantage of any available state income tax deductions. Even modest contributions can compound meaningfully over time. If grandparents plan to contribute significantly, your advisor can help coordinate whether you should direct savings toward other goals using trusts. For more guidance, see our whitepaper, Maximizing College Savings with 529 Plans.

I’m receiving equity compensation at work—how do I avoid a tax surprise?

Stock options and RSUs can create both opportunity and risk. Timing exercises and sales around tax rules is key. Your advisor can coordinate with your CPA to create a tax-smart strategy and diversify concentrated stock positions.

What if I want to buy a home in the next 3–5 years?

That’s a mid-term goal. It usually belongs in a conservative investment account or a high-yield savings account. Your advisor can help you set up a dedicated “home purchase fund” so you don’t jeopardize other long-term goals. It’s important to understand what you can afford up front, the different lending options available, including intra-family loan structures and how much you can afford as an ongoing monthly expense. For more guidance, see our whitepaper, The Keys to the Castle – Buying a Home.

How do I balance planning for my own future with honoring family expectations?

This is one of the most common challenges for next-generation clients. The answer lies in creating clarity: what wealth do you want to build on your own terms, and what do you want to steward from family structures? Your advisor can help navigate these conversations while protecting your independence

and vision.

IMPORTANT DISCLOSURES

The views and opinions included in these materials belong to their author and do not necessarily reflect the views and opinions of NewEdge Capital Group, LLC.

This information is general in nature and has been prepared solely for informational and educational purposes and does not constitute an offer or a recommendation to buy or sell any particular security or to adopt any specific investment strategy.

NewEdge and its affiliates do not render advice on legal, tax and/or tax accounting matters. You should consult your personal tax and/or legal advisor to learn about any potential tax or other implications that may result from acting on a particular recommendation.

The trademarks and service marks contained herein are the property of their respective owners. Unless otherwise specifically indicated, all information with respect to any third party not affiliated with NewEdge has been provided by, and is the sole responsibility of, such third party and has not been independently verified by NewEdge, its affiliates or any other independent third party. No representation is given with respect to its accuracy or completeness, and such information and opinions may change without notice.

Investing involves risk, including possible loss of principal. Past performance is no guarantee of future results.

Any forward-looking statements or forecasts are based on assumptions and actual results are expected to vary from any such statements or forecasts. No assurance can be given that investment objectives or target returns will be achieved. Future returns may be higher or lower than the estimates presented herein.

An investment cannot be made directly in an index. Indices are unmanaged and have no fees or expenses. You can obtain information about many indices online at a variety of sources including: https://www.sec.gov/answers/indices.htm.

All data is subject to change without notice.

© 2026 NewEdge Capital Group, LLC