Consumers in “The Space Between”

The latest twists in 2025’s economic policy soap opera came from a federal court this week striking down the bulk of U.S. tariffs…only for a higher court to put that ruling on hold less than 24 hours later. While we wait for the appeals process to play out and anticipate alternative tariff measures from the Trump administration, we will focus this week on the U.S.’s enduring source of economic strength, its consumers.

U.S. consumers are correctly thought of as the most important economic actors in the world, constituting the lion’s share of output from the world’s largest economy. For years, economists have doubted households’ collective will and ability to grow spending and keep the global economy afloat, and for years those doubts have been proven needless.

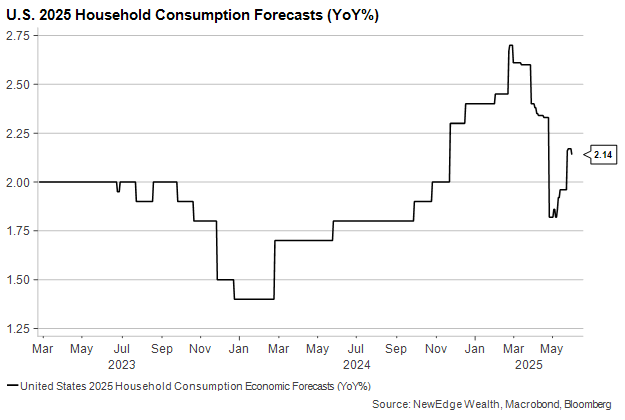

Coming into 2025, economists were optimistic about the consumer outlook, forecasting 2.4% growth on average. At the time, we were more cautious in our outlook given the slower hiring rate, diminished savings, and falling real income growth. Forecasts rose higher in Q1 but fell by close to 1% with the onset of the tariffs. They’ve rebounded a bit as those tariffs have been walked back, but with the Q1 personal consumption growth rate just revised down to 1.2% and real spending for April growing at just 0.1%, we see further downside risk to the full-year consensus:

In the world’s iconic on-screen introduction to Superman (1978), Christopher Reeve’s man of steel assures Margot Kidder’s incredulous Lois Lane, “Easy, miss! I’ve got you!” as he flies up to catch her in mid-fall from the roof of a skyscraper. Her characteristically snappy-under-duress reply is, “You’ve got me? Who’s got you?” We’re wondering the same thing about consumers, who have been coming to the economy’s rescue for five years and counting. The forces allowing them to do so are still around today but in weaker form. And new risks are on the horizon…especially if tariffs escape from their banishment to the Phantom Zone.

“They Can Be a Great People” – What Kept Consumers Going After the Pandemic?

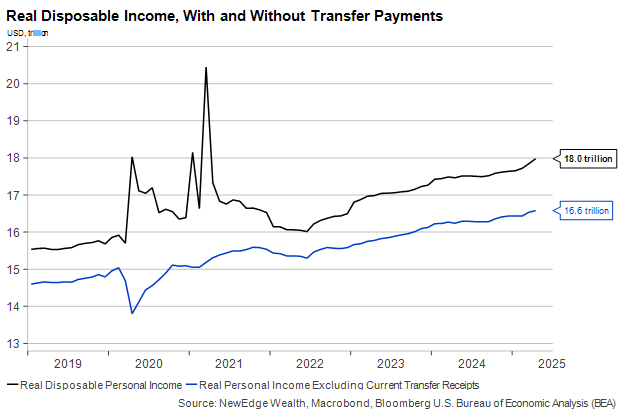

Consumption growth is inextricably linked with income growth. and consumers have enjoyed a lengthy period of warm-to-hot labor market conditions. While price increases have sometimes outpaced wage growth, household incomes are a good deal higher in 2025 than they were in 2019. Further real growth from here will be, in part, due to confidence that the labor market will remain solid.

In 2022, inflation took real income growth into negative territory, but real spending held up well. The unprecedented amount of excess savings at the time, a result of government stimulus payments and the constraints of the pandemic, backstopped the consumer during the inflation spike.

For the past 18 months, real wage growth has softened even with inflation on the decline, but consumers have continued to growth their real spending by more than 3%. We doubt this trend is sustainable. Either income growth will rise from here or spending will need to slow. We are already seeing signs of the latter in the rising savings rate.

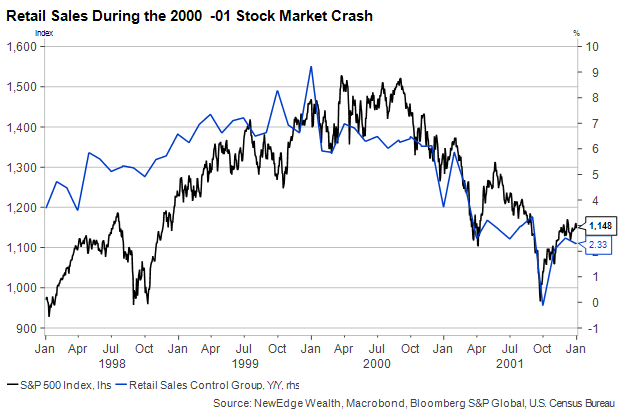

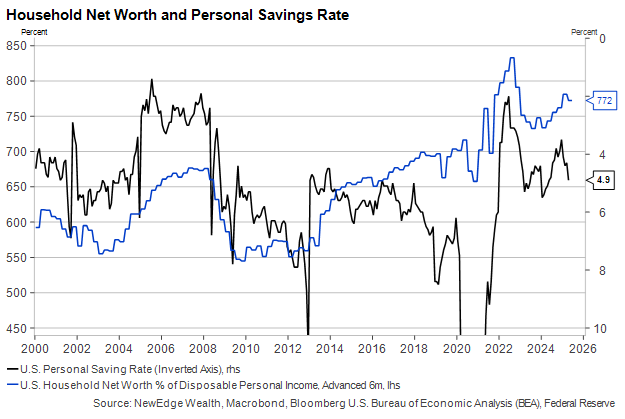

Surging stocks create confident consumers. The Tech Bubble and subsequent Tech Wreck showed that households respond to the wealth effect. During times of rising asset prices, savings rates drop as consumers feel confident spending more of what they earn. When asset prices fall, the opposite happens.

The wealth effect does not only show up during crises. When household net worth is rising as a percentage of income (the blue line on the chart below), personal savings rates (the black line, inverted) have fallen. The past six months of flattish portfolio returns coupled with a slowing in home price appreciation (more on that below) have likely contributed to the rise in the savings rate, punctuated by the incredible volatility during the month of April.

“You will bow down before me! I swear it! No matter if it takes an eternity” – Higher rates are taking a long time to affect consumers

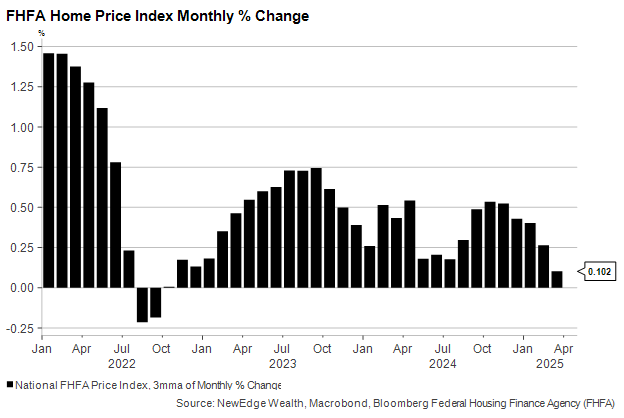

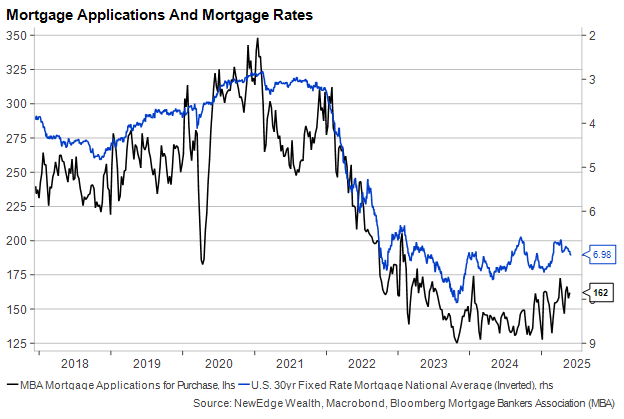

It may seem strange for us to refer to the high level of interest rates as a headwind for consumers when the first Fed rate hikes of the cycle came over three years ago. But, as the saying goes, interest rates have long and variable lagged effects on the economy. Home prices feel those effects and have largely stopped rising in recent months with mortgage rates once again on the rise.

U.S. 10-Year Treasury Yield with RSI

Last week, we showed that the sustained increase in interest rates has been pushing up single-family home inventories to more normal levels. Part of that is because of the effect high mortgage rates (the 30-year fixed rate is back up to 7%) have on demand:

Home sales are a leading economic indicator for many types of consumer behavior, particularly purchases of durable goods like furniture and home decorations, which usually follow a new home purchase.

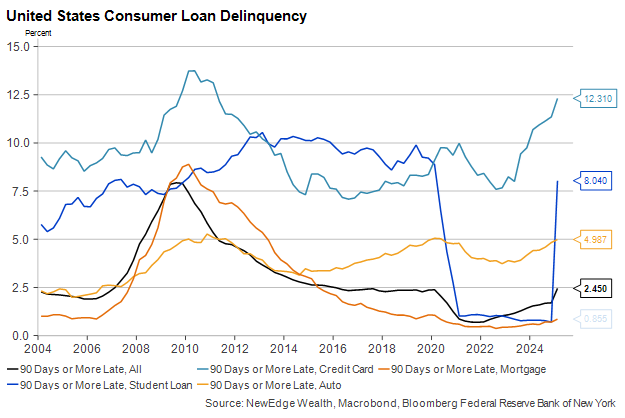

“You Just Described the Exact Contents of My Purse.” – Consumer Credit on Watch

Some households are feeling the bite of high rates and slowing growth through consumer credit channels, though unlike the 2008 crisis, mortgages are not the main source of concern:

Credit card delinquencies are close to their peak levels during the financial crisis, while student loan defaults – which have only recently been turned back on – seem likely to rise from here. The overall level consumer delinquency remains contained thanks to ultra-low-rate mortgages making up the bulk of outstanding credit.

This has also created sharp divides by both age and wealth level between households that are feeling pinched and those that are not. If you own a home, your debt-related expenses are probably quite low. If you’ve been a renter for the past five years, you may be among those who owe considerable balances on credit cards, autos, and student loans.

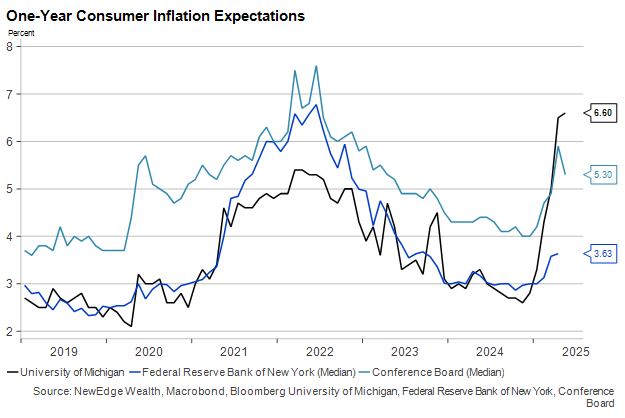

“Do you realize what people are shelling out up there, for a few miserable rooms off a common elevator?” – Inflation expectations are back on the rise

The inflation of 2022 made consumers feel miserable but did not at all dissuade them from growing their spending faster than prices were increasing. A white-hot labor market and significant savings helped them do so without inviting a financial calamity. Now, inflation expectations are back on the rise thanks to a combination of tariff and debt concerns, though the magnitude varies greatly depending on which survey we look at:

Inflation expectations have an ambiguous effect on the consumer outlook. One the one hand, consumers may flock to pluck things off shelves if they believe prices are going to rise. On the other hand, households may not be feeling as financially prepared to weather another round of rising prices and may forgo some discretionary purchases as a result.

“Fantasy? No, no. It’s history. It’s happening!” – Consumers are not being clear about their feelings on the economy

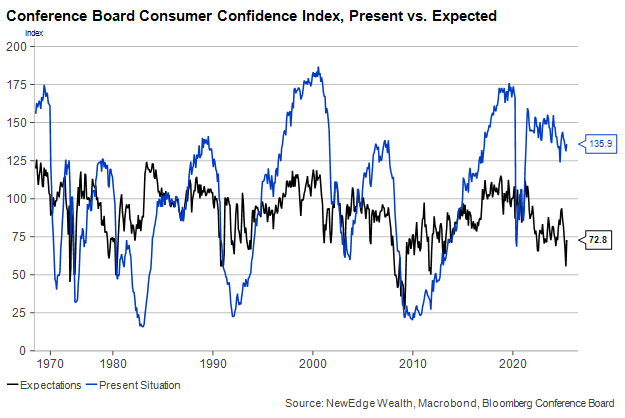

The challenge in forecasting consumer behavior is that what people say and what they do have started to have less and less in common. If we believed consumer confidence surveys, we would have forecasted a recession in 2023 (indeed, most economists did).

Despite a bounce in this month’s Conference Board survey, consumer expectations remain in recession territory. Assessments of the current situation, however, have worsened at a much gentler rate, exhibiting a pattern that, as the graph below shows, is without precedent. Consumer attitudes about the economy tend to be cyclical with sharp peaks and valleys, but the malaise that began in 2021 is something altogether different.

“Alright Luthor, where is it? Where’s that detonator?” – Conclusion

There’s a reason we keep calling the U.S. consumer “resilient”. High interest rates, sudden bouts of inflation, acute policy uncertainty, and a hiring slowdown have collectively generated only a minor slowing in household spending. But credit conditions are fraying around the edges, and the historically long and severe period of poor housing affordability is creating starker populations of “haves” and “have nots”. We see these factors along with the risk of a further drop in real incomes in the second half of the year as pulling consumption growth below 2% in 2025 for the first time since 2020 and, before that, 2013.

On the bright side, tariffs look much less like kryptonite today than they did on April 3rd, and the prospect of declining interest rates providing a (yellow) sunny outlook over the next year means we do not see a ticking time bomb in the U.S. consumer story. But should the courts allow import taxes to return and reintroduce a stag-flationary impulse, “the American way” (borrowing money to buy things we don’t necessarily need) may face its greatest test yet.

IMPORTANT DISCLOSURES

The views and opinions included in these materials belong to their author and do not necessarily reflect the views and opinions of NewEdge Capital Group, LLC.

This information is general in nature and has been prepared solely for informational and educational purposes and does not constitute an offer or a recommendation to buy or sell any particular security or to adopt any specific investment strategy.

NewEdge and its affiliates do not render advice on legal, tax and/or tax accounting matters. You should consult your personal tax and/or legal advisor to learn about any potential tax or other implications that may result from acting on a particular recommendation.

The trademarks and service marks contained herein are the property of their respective owners. Unless otherwise specifically indicated, all information with respect to any third party not affiliated with NewEdge has been provided by, and is the sole responsibility of, such third party and has not been independently verified by NewEdge, its affiliates or any other independent third party. No representation is given with respect to its accuracy or completeness, and such information and opinions may change without notice.

Investing involves risk, including possible loss of principal. Past performance is no guarantee of future results.

Any forward-looking statements or forecasts are based on assumptions and actual results are expected to vary from any such statements or forecasts. No assurance can be given that investment objectives or target returns will be achieved. Future returns may be higher or lower than the estimates presented herein.

An investment cannot be made directly in an index. Indices are unmanaged and have no fees or expenses. You can obtain information about many indices online at a variety of sources including: https://www.sec.gov/answers/indices.htm.

All data is subject to change without notice.

© 2026 NewEdge Capital Group, LLC