Once You Go In, You Don’t Come Out…Until Today

“Remember, once you’re inside, you’re on your own”

New York City’s Mayor-elect, Zohran Mamdani, has generated lively debate among investors regarding their municipal bond holdings and the financial future of New York City. His campaign platform featured a range of tax increases and new debt to support programs aimed at improving affordability and income inequality. This has caused some NYC investors to ask whether they should be approaching their municipal bond portfolios in a different way. Will the wealthiest leave? Will the city remain friendly to businesses? Will all of this be just too big a bite for this apple to handle?

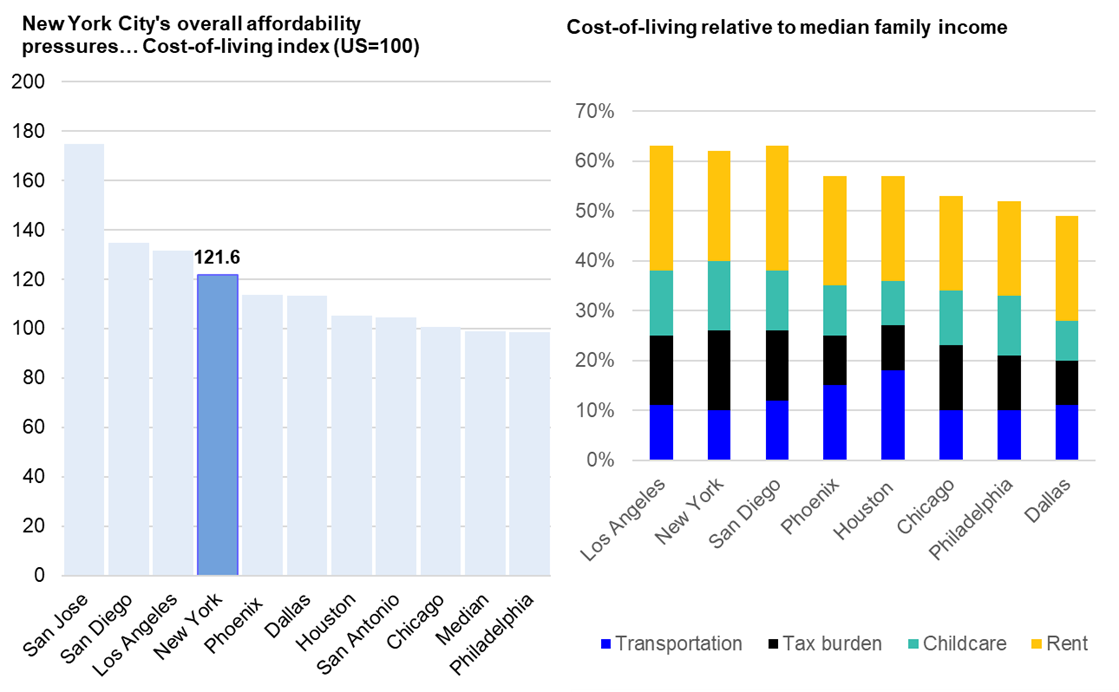

For starters, the mayor-elect has a point with regards to poor affordability. New York’s City’s cost of living is among the highest in the nation. High residential rents and childcare costs weigh heavily on New Yorkers. The city’s median household income is 24% higher than the U.S. median, but this is somewhat negated by a comparatively high tax burden.

Escape from New York is a 1981 cult classic sci-fi action-adventure film starring Kurt Russell as Snake Plissken. It combines serious dystopian themes with a multitude of B-movie campiness. We’ll have some fun using its film noir influenced dialogue and plot to highlight our analysis as we take a deeper dive into the potential impact of the mayor-elect’s progressive agenda on investors’ portfolios.

Speaking of Taxes…

“New York City is now a maximum-security prison”

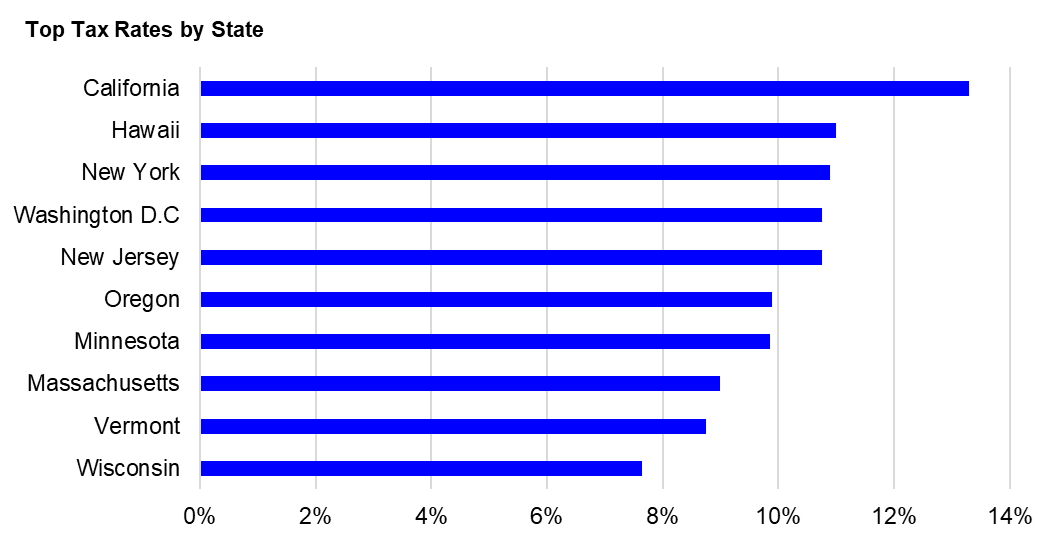

New York is one of a small number of cities to levy a sizable income tax. Its highest-income residents already pay an additional 3.876% city tax on top of one of the highest state income tax rates in the U.S.. A key component to finance the mayor-elect’s agenda centers around an additional 2% tax rate on the wealthiest New Yorkers earning over $1 million per year. This would, of course, require approval from the state legislature and the governor, who had expressed reluctance about raising taxes but is now considering a higher corporate tax rate as part of a broader effort to raise revenue.

Strong Fiscal Governance

“I swear to God Snake, I thought you were dead”

“Yeah. You and everybody else.”

New York City has long demonstrated disciplined budgeting practices and, as a result, has maintained a credit rating of AA for nearly two decades. It operates under multiple levels of state and local oversight and balanced budget requirements, which have constrained radical policy deviations. The ability to realign fiscal priorities within a balanced budget while sustaining economic vitality will be a key to the city’s future credit quality.

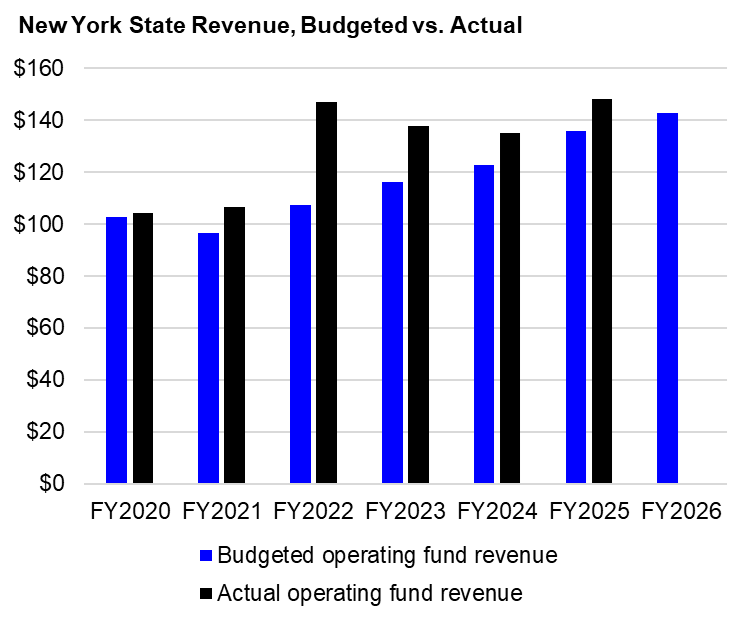

New York State’s credit profile, also AA, benefits from its large and diverse economy, which generates above-average income and wealth, and from strong budget management. The state consistently sees revenue outperformance, which has allowed it to add $25 billion to reserves in the past three fiscal years.

Wealth Flight Concerns

“Take me with you Snake.”

“Why?”

“I can think of lots of reasons why.”

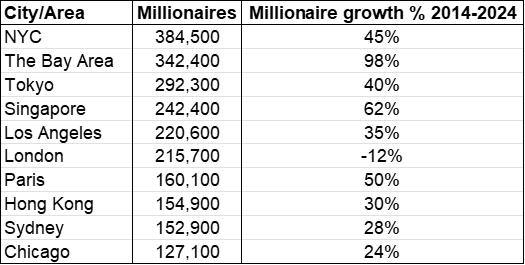

Despite New York’s well-earned reputation for credit discipline, there is significant concern that the new mayor’s agenda will lead to a mass exodus of wealthy New Yorkers, which will deprive the state and city of significant income tax revenue. But so far, the high tax burden has not been a detriment to growth. No other city in the world has more millionaires than The Big Apple, and the number of millionaires has grown at an impressive rate of 45% over the past 10 years, a decade that obviously included the COVID-19 pandemic.

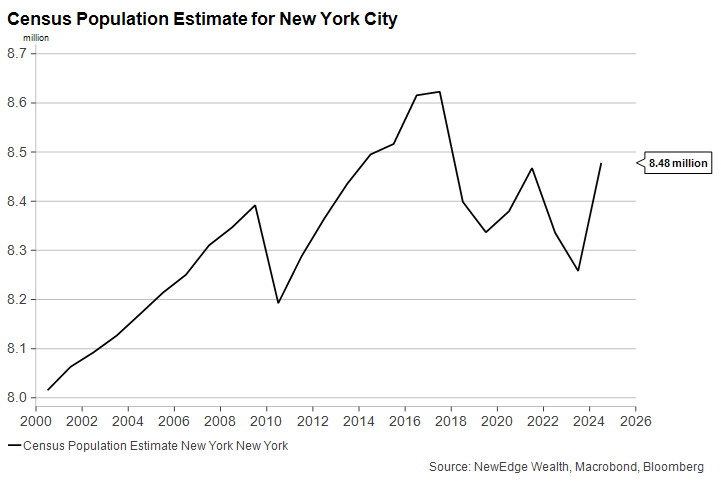

Census estimates show New York City’s population continues to recover from its swoon in the late 2010s and early 2020s.

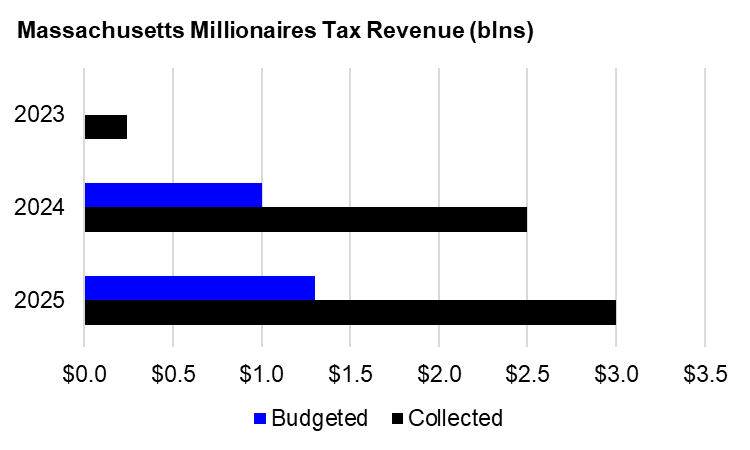

Limited experience with so-called millionaires’ taxes in places like Massachusetts, which charges a 4% surtax on incomes over $1 million, suggests that fears of a mass exodus can be overstated. Since the tax began in 2023, Massachusetts has seen limited wealth flight, overall population growth and higher than expected revenue.

Market Reaction and Headline Risk

“What’s wrong with Broadway?”

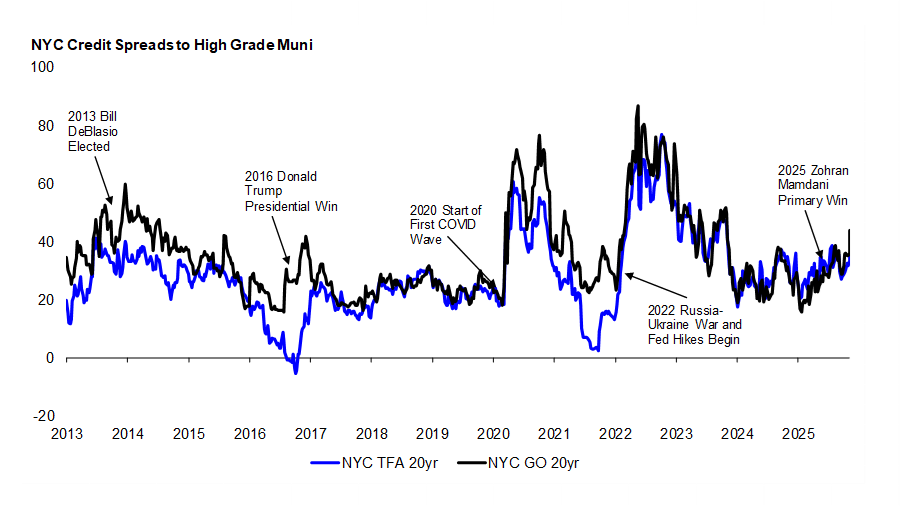

Spreads on the two largest 20-year NYC-related credits (the NYC General Obligation and Transitional Finance Authority bonds) widened after the election of Mayor Bill DeBlasio but rallied into very strong summer technicals the following year. This year, spreads have widened gradually since February, but the NYC GO bond has widened about 8bps further since the end of October, presumably, in part, due to the election outcome. But this is fairly modest compared to the 2013 election as a reference, after which spreads widened by about 20bps. Both credits are currently trading wider than their 12-year average spreads of 29 bps (NYC TFA) and 35bps (NYC GO).

New Yorkers who are uncomfortable with the headline risk and the future of the city’s finances, could consider diversifying their NY municipal bonds away from NYC-related issuers. Bonds that are tied more directly to the state, local municipalities or essential services within NY State still enjoy the full tax benefits and can potentially avoid some of the headline risk associated more directly with NYC.

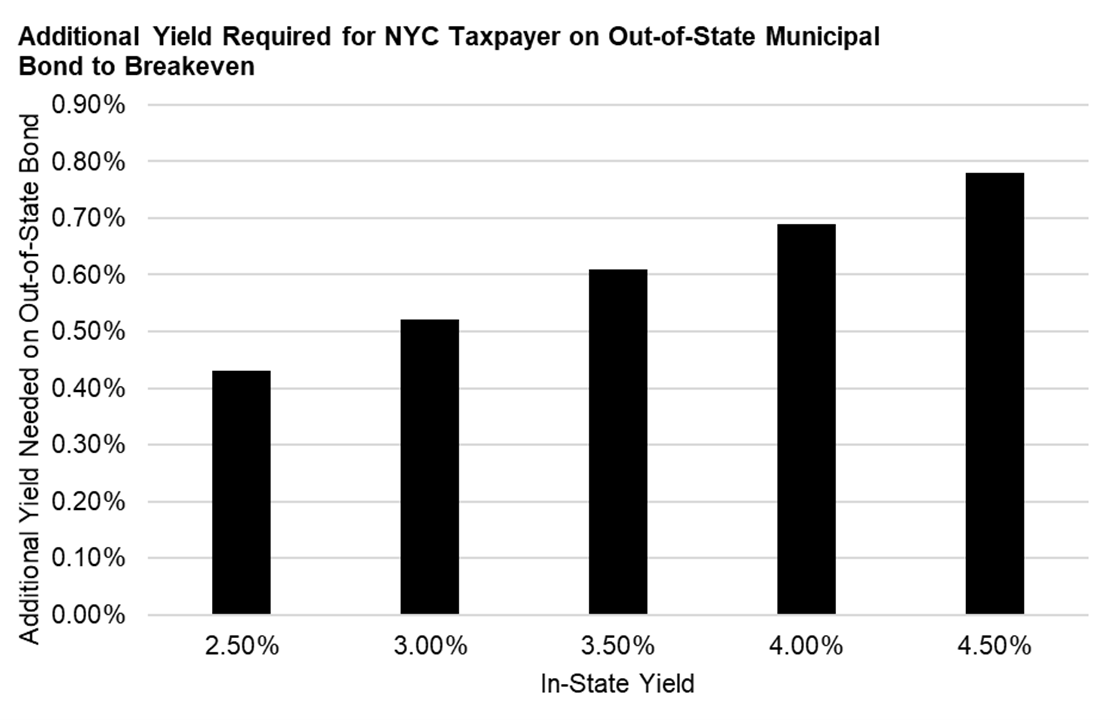

Those NYC residents looking to diversify out of the state entirely, may find that doing so requires accepting lower taxable equivalent yields. Swapping New York bonds for out-of-state issues is difficult to do in a tax efficient manner. Doing so may also require a downgrade in credit quality, which may undermine the goal of owning a municipal portfolio in the first place.

The Case for Munis

“I’m not a fool, Plissken.”

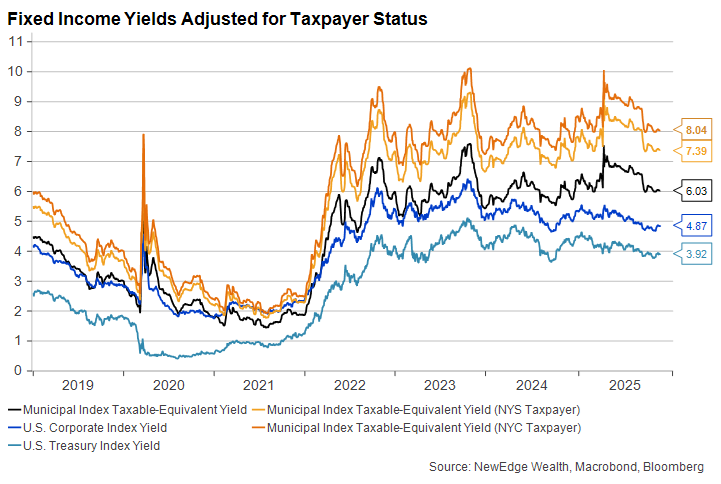

We believe municipal bond yields remain attractive, especially on a taxable equivalent basis, when compared to other fixed income securities. A pre-tax yield of just under 5% on corporate bonds pales in comparison to the 7% or 8% that New York municipals offer to NY State and City residents on an apples-to-apples basis.

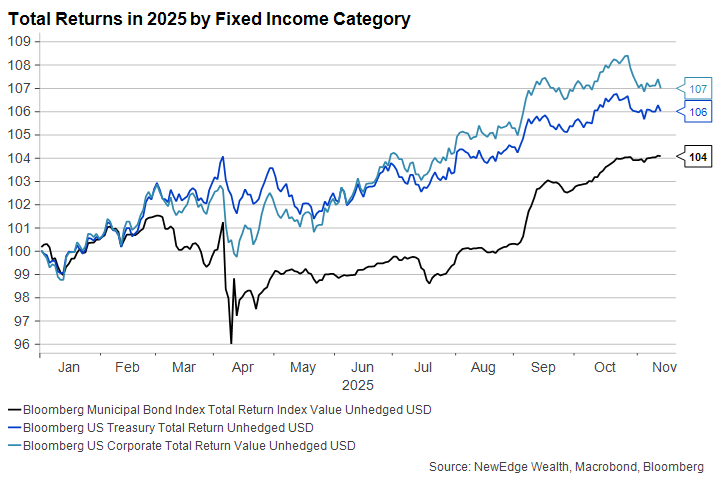

We would be remiss if we ended this piece without commenting on the performance of the broader municipal market in 2025. A difficult first half resulted in cheaper valuations heading into the summer months. This along with positive market technicals and surging investor demand have helped munis outperform in both Q3 and, so far, in Q4. Longer duration bonds performed the best, but we continue to see compelling opportunities in these longer-maturity issues.

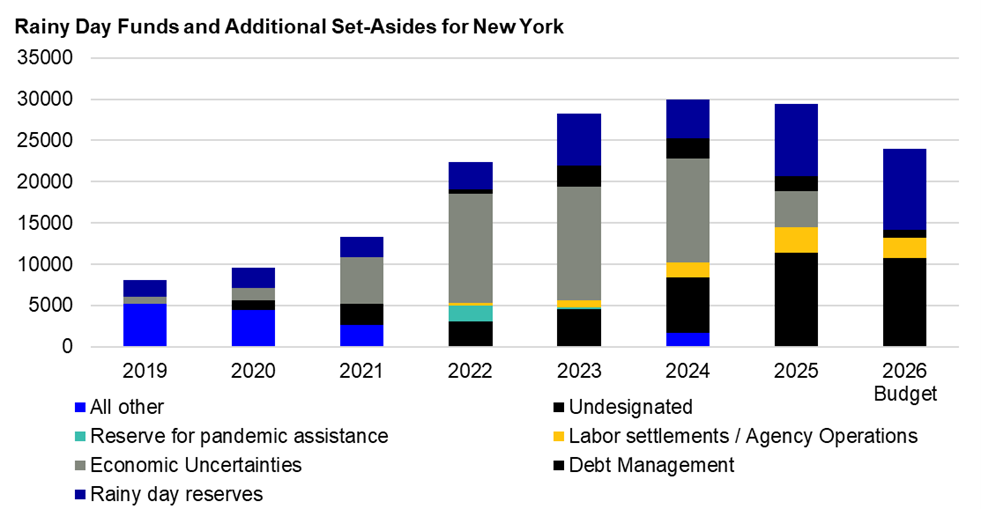

To sum up, our assessment of New York City remains positive, and we continue to see value in the New York municipal market for city and state residents, and in some cases for national buyers. New York’s economy remains broad and diverse, and its budgeting process features strong oversight and accumulated rainy day funds to help it weather a fiscal storm.

We do not have a view on whether or how much of the incoming mayor’s agenda will get through, but do not see it having a negative impact on New York City’s credit rating or a meaningful drag on the performance of its bonds, for now. The tax benefits to New Yorker’s outweigh the credit risks, in our view, which is quite often the case for municipals more broadly. That said, we recognize we are in uncertain times. As such, we will be monitoring future developments and evaluating their potential impact on the city’s finances and credit profile when and if they arise.

IMPORTANT DISCLOSURES

The views and opinions included in these materials belong to their author and do not necessarily reflect the views and opinions of NewEdge Capital Group, LLC.

This information is general in nature and has been prepared solely for informational and educational purposes and does not constitute an offer or a recommendation to buy or sell any particular security or to adopt any specific investment strategy.

NewEdge and its affiliates do not render advice on legal, tax and/or tax accounting matters. You should consult your personal tax and/or legal advisor to learn about any potential tax or other implications that may result from acting on a particular recommendation.

The trademarks and service marks contained herein are the property of their respective owners. Unless otherwise specifically indicated, all information with respect to any third party not affiliated with NewEdge has been provided by, and is the sole responsibility of, such third party and has not been independently verified by NewEdge, its affiliates or any other independent third party. No representation is given with respect to its accuracy or completeness, and such information and opinions may change without notice.

Investing involves risk, including possible loss of principal. Past performance is no guarantee of future results.

Any forward-looking statements or forecasts are based on assumptions and actual results are expected to vary from any such statements or forecasts. No assurance can be given that investment objectives or target returns will be achieved. Future returns may be higher or lower than the estimates presented herein.

An investment cannot be made directly in an index. Indices are unmanaged and have no fees or expenses. You can obtain information about many indices online at a variety of sources including: https://www.sec.gov/answers/indices.htm.

All data is subject to change without notice.

© 2026 NewEdge Capital Group, LLC