I am not afraid to keep on living

“Famous Last Words”, My Chemical Romance

If there is a GOAT (Greatest of All Time) title for “Famous Last Words” in financial market valuations, it has to go to Irving Fisher, who infamously quipped in 1929 that “stock prices have reached what looks like a permanently high plateau.” Of course, we know what happened after this not-so-reassuring statement: the Dow plunged 89% and took 25 years to make a new high.

A modern honorable mention for this “new paradigm” assertion for market valuations goes to Dr. Robert Shiller, the creator of the Cyclically Adjusted Price to Earnings Ratio (CAPE). In 2021, Dr. Shiller justified high equity valuations vs. long-term history by arguing that stocks were not expensive because real bond yields were so low, meaning investors were still earning an attractive “excess yield” in equities.

More “Famous Last Words”, Shiller’s assertion was challenged throughout 2021 and 2022 as bond yields rose rapidly and stock valuations fell, reminding investors to not use one over valued asset to justify the valuation of another over valued asset (note that stock valuations fell throughout 2021 but stock prices still rose thanks to a huge increase in earnings).

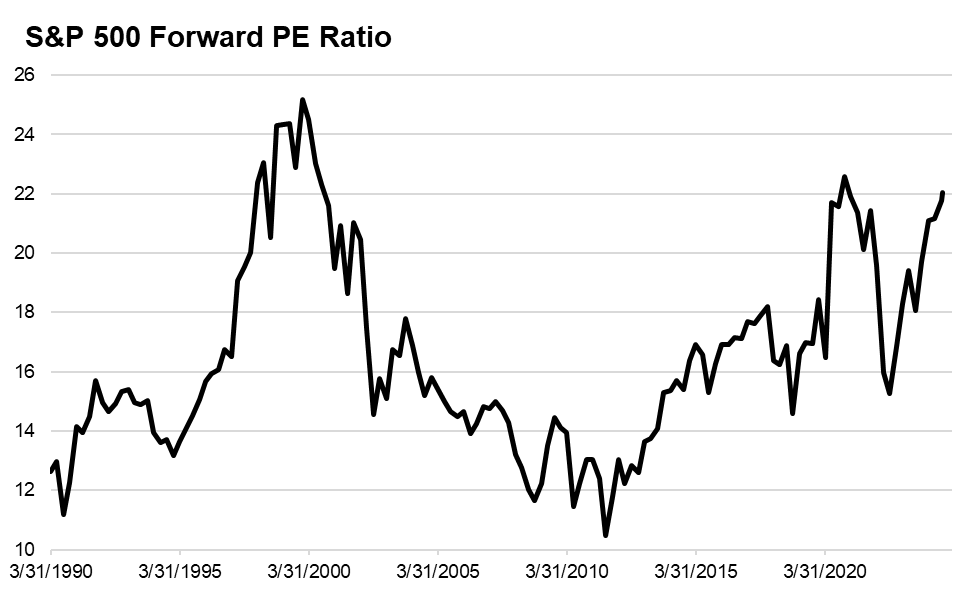

One of the most incredible feats of this equity market over the last two years has been the S&P 500’s ability to experience stunning valuation expansion. In fact, the forward price to earnings (PE) ratio for the S&P 500 is +44% from the October 2022 low, contributing well over 2/3 of the total price return of the index, which is +64% since 10/12/22.

This move higher in valuations has returned the S&P 500 to 22x forward earnings, a level that has only been surpassed two times in modern history: at the height of the late-1990s/2000s tech bubble and at the 2020 COVID peak when markets were being flooded with liquidity and earnings were depressed.

Source: Bloomberg, NewEdge Wealth, as of 10/18/24

So as investors look at today’s fulsome and heady valuations with wide eyes that could rival the iconic glare of Gerard Way from My Chemical Romance, we must face important questions about valuations, mostly as we near 2025.

We do not want to utter our own “Famous Last Words” in trying to justify today’s expensive valuations, but we must acknowledge the reasons why valuations are so high and be realistic that valuations are a poor predictor of short-term returns. In truth, you could have argued at any point over the last year that stocks were expensive, but there needs to be a catalyst to change this march to ever-higher multiples.

In today’s Weekly Edge, we will don our emo marching band apparel and explore the source of today’s full valuations, the drivers of future valuation moves, and how the outlook for valuations could impact stock performance into 2025.

Our conclusion from this analysis is that valuations are exceptionally high for the S&P 500 and are likely to eventually dampen forward returns looking out beyond the next year. This does not mean to be uninvested in equities, but instead to remain valuation disciplined and attuned to future risks to valuations. We do not rule out the upside risk of further valuation expansion in a melt-up scenario, driven by today’s extraordinary backdrop of stimulative fiscal and monetary policy into a relatively strong economy.

Our constant phrase this year of “respect the uptrend but don’t ignore the risks” remains relevant and helpful.

“Can You See My Eyes Are Shining Bright?”: The Source of Today’s Full Valuations

We think there are five main reasons that have combined to drive today’s high S&P 500 valuation:

1. Growth and Policy Support: Earnings and GDP growth estimates have been rising, supporting a risk-on tone for markets that is often supportive of expanding valuations. Very simply, when investors are feeling more confident about the future, they tend to be willing to pay more for future returns. This is not always the case (such as 2001-2007, when EPS estimates were rising but stock valuations were still falling post the tech bubble), but generally better growth is a good backdrop for valuation expansion. We have been reminding investors of this extraordinary backdrop for risk assets, driven by supportive fiscal and monetary policy into a relatively strong economy, is a key reason by both stock and credit valuations are so extended.

2. Liquidity: Liquidity has been supportive of risk assets over the last two years (despite the Fed arguing that financial conditions are “tight”), helped by Treasury actions that have helped to offset tightening in liquidity from the Fed, such as from the shrinking of the Fed’s balance sheet. This is based on the great work of Dan Clifton at Strategas, who has argued that Yellen’s “liquidity bazooka” from focusing Treasury issuance on short-dated debt has offset Powell’s liquidity drain. This theory has been further advanced with the Miran and Roubini’s Activist Treasury Issuance thesis. Understanding this supportive liquidity backdrop helps to explain why broad financial conditions have eased so significantly in the past two years, well before the Fed began its interest rate cutting cycle.

3. Scarcity: Stocks are an increasingly “scarce” asset, with buybacks outweighing issuance significantly in recent years. Just in 2024, equity issuance has been a mere $139B, while there has been a record $1.1T of buybacks. When we think of this as simple supply and demand, this shrinking supply of stocks paired with increasing demand for stocks (thanks to the $7T of extra liquidity still in the global economy post the extraordinary COVID measures, according to Guggenheim) results in higher prices.

4. Constitution: As the S&P 500 become increasingly dominated by high quality Tech and Magnificent 7 names (the S&P 500’s weighting to the Tech sector is now over 30%), while old-economy sectors like Energy have shrunk (now just 3% vs. a 16% weight in 2008), the overall index has arguably become more deserving of higher valuations. This notion reflects the work of Mike Mauboussin, who argues that the increasing “intangible” assets of S&P 500 companies makes historical analysis of valuation multiples something investors should do “with great caution.”

5. Hopes and Dreams: Optimism around AI/technology, positioning chases, and the fear of missing out, have all combined to create a sentiment backdrop that has been resiliently optimistic, if not euphoric at times over the past two years. Bloomberg’s Cameron Crise quantifies this sentiment boost to valuations with his Hopes and Dreams Indicator, which is the amount of the market’s valuation that cannot be explained by book value or the next three years of earnings expectations. This week he noted that the Hopes and Dreams Indicator for the S&P 500 hit its highest level since September 2000.

“A Life That’s So Demanding”: The Drivers of Future Valuation Moves

We see two main catalysts that could challenge valuations in the coming quarters: fading EPS growth expectations and/or higher yields.

This catalyst is not to say that valuations cannot go any higher from here (respect the trend), but we encourage investors to not baseline to extraordinary periods like the 2000s tech bubble to reach price targets or argue for further valuation upside. We would also argue that the further valuations expand from today’s levels, the more fragile the market will be to future surprises.

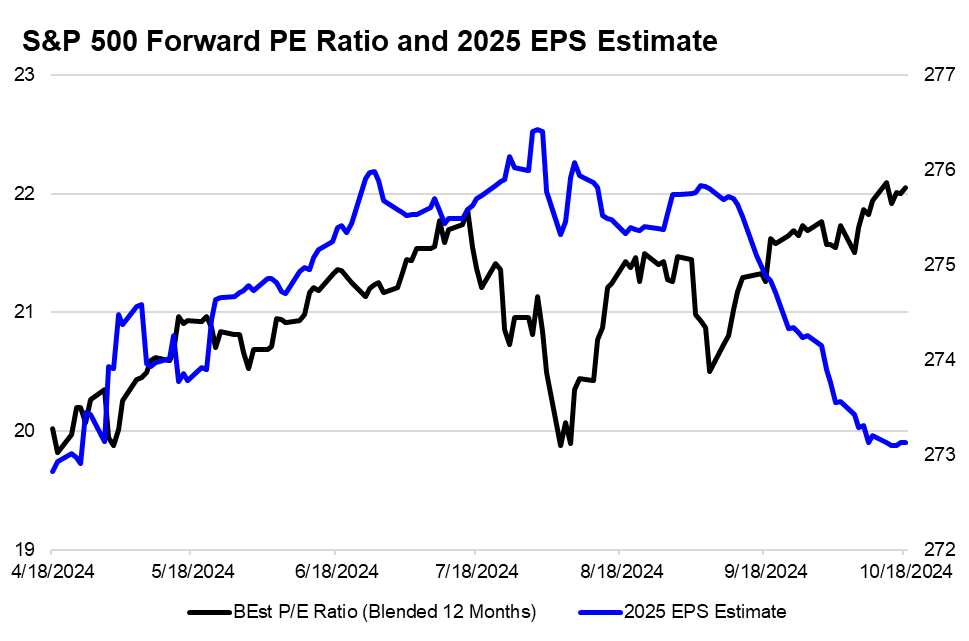

For the first catalyst of earnings estimate cuts, we must note that these cuts have already been happening without any impact to stock valuations or prices. Analysts have been slightly trimming their 2025 EPS forecasts since early August (-1% or ~$3/share) and yet valuations have pressed back to their July highs. This is a divergence between fundamentals and price action that certainly bears watching.

Source: Bloomberg, NewEdge Wealth, as of 10/18/24

On the yield front, we think that a surprise jump higher in yields and/or a resumption of an uptrend in yields could challenge today’s high valuations. This would be similar to 2H23, when the S&P 500’s PE multiple fell 13% as the 10 Year Treasury yield jumped 150 bps to 5%. However, similar to the caveat on EPS estimates that have already been cut at no expense to valuations, we have seen a nearly 50 bps jump in the 10 Year since September, all the while PE multiples have continued their expansion.

If yields keep rising and EPS forecasts keep getting trimmed, with think eventually this would halt the expansion of and challenge currently high valuations.

“Now I Know That I Can’t Make You Stay”: How the Outlook for Valuations Could Impact 2025 Stock Returns

As we look to 2025, we do not expect valuation expansion to be the key driver of S&P 500 returns, which is another way of saying that we see valuations having greater downside risk than upside potential and that we see earnings growth being a bigger portion of price returns.

Again, valuations are a poor timing tool and given the rare backdrop of stimulative monetary and fiscal policy into a strong growth environment, we cannot rule out the upside risk of a melt-up or bubble.

If we do see significant further upside to valuations from today’s levels, we would see it as a risk to longer-term equity returns, given melt-downs typically follow melt-ups and the aftermath of bubbles can take years and even decades to heal. We do not think we are in a bubble today, speculative fervor is the one missing piece, but we are on watch as we start to see speculative excitement starting to pick up in recent weeks.

If earnings are to be the bigger driver of returns next year, it does imply a more muted S&P 500 price return for 2025 (given current consensus is for 13% EPS growth YoY). But it also raises the question if valuations can even be a neutral factor next year or if they will become a headwind if they begin to contract (to learn from Irving Fisher’s “permanently high plateau” folly).

We are reminded again of the 2021 scenario, where the starting 22.5x forward PE was not sustainable and compressed throughout the course of the year as yields rose. The benefit for 2021 was 42% EPS growth that year that provided plenty of cushion for this PE multiple compression.

Given the starting point of such high valuations, we think it prudent of investors to begin by expecting more muted returns in 2025.

“I Am Not Afraid to Walk This World Alone”: Conclusion

Overall, we see the S&P 500 valuation as expensive and a potential dampener for equity market returns in 2025. We acknowledge reasons why S&P 500 valuations should be higher versus history (liquidity, scarcity, composition), but do not go so far to utter “Famous Last Words” that today’s valuations are abundantly attractive or imminently sustainable.

Note, this entire piece focused on the S&P 500 in aggregate, which masks how other indices and individual components do still have attractive, or at least less stretched, valuations. The relative cheapness of unloved parts of the market is a discussion for another day!

IMPORTANT DISCLOSURES

The views and opinions included in these materials belong to their author and do not necessarily reflect the views and opinions of NewEdge Capital Group, LLC.

This information is general in nature and has been prepared solely for informational and educational purposes and does not constitute an offer or a recommendation to buy or sell any particular security or to adopt any specific investment strategy.

NewEdge and its affiliates do not render advice on legal, tax and/or tax accounting matters. You should consult your personal tax and/or legal advisor to learn about any potential tax or other implications that may result from acting on a particular recommendation.

The trademarks and service marks contained herein are the property of their respective owners. Unless otherwise specifically indicated, all information with respect to any third party not affiliated with NewEdge has been provided by, and is the sole responsibility of, such third party and has not been independently verified by NewEdge, its affiliates or any other independent third party. No representation is given with respect to its accuracy or completeness, and such information and opinions may change without notice.

Investing involves risk, including possible loss of principal. Past performance is no guarantee of future results.

Any forward-looking statements or forecasts are based on assumptions and actual results are expected to vary from any such statements or forecasts. No assurance can be given that investment objectives or target returns will be achieved. Future returns may be higher or lower than the estimates presented herein.

An investment cannot be made directly in an index. Indices are unmanaged and have no fees or expenses. You can obtain information about many indices online at a variety of sources including: https://www.sec.gov/answers/indices.htm.

All data is subject to change without notice.

© 2026 NewEdge Capital Group, LLC