You’ve spent years earning and growing your wealth, but will your wealth strategy stand the test of time? Financial models guide crucial investment decisions—from portfolio allocation to long-term planning—yet they’re only as reliable as the assumptions and expertise behind them. Like any roadmap, a financial model provides direction but mindlessly following it without adaptation can lead you right off a cliff when conditions change.

Market shifts, economic surprises, and personal circumstances constantly challenge even the most meticulously crafted plans. To truly assess the strength of your wealth strategy, it’s essential to understand not just how financial modeling has evolved, but how to interpret and adjust these plans properly with professional guidance.

The Evolution of Financial Modeling: From Simple Maps to GPS

Financial modeling has advanced significantly over the past century, shaped by breakthroughs in mathematics, computing, and financial theory.

Early Foundations (Pre-20th Century)

- 18th and 19th century financiers applied fundamental accounting principles and discounted cash flow (DCF) analysis to evaluate investments

- Modeling relied on manual calculations and simple arithmetic, primarily for business valuations, loan assessments, and government bond pricing.

- These rudimentary models served as basic maps with limited predictive capabilities

20th Century: Building Sophisticated Navigation Tools

1920s–1950s: Statistical and Portfolio Theories

- Economists like John Maynard Keynes emphasized expectations and uncertainty in investment decision-making

- Harry Markowitz’s 1952 Modern Portfolio Theory introduced optimizing risk and return, establishing the foundation for quantitative financial modeling

- These innovations transformed financial planning from simple arithmetic to strategic analysis

1960s–1970s: Birth of Modern Financial Models

- William Sharpe’s 1964 Capital Asset Pricing Model (CAPM) provided a systematic approach to determining expected returns based on risk

- Early computer adoption enabled more complex forecasting and budgeting

- Financial planning began incorporating more variables, though still limited by technological constraints

The Rise of Spreadsheet-Based Modeling (1980s-1990s)

- Personal computers and spreadsheet software (Lotus 1-2-3 in 1983, Microsoft Excel in 1985) democratized financial modeling

- Complex scenario planning became accessible to a broader audience of financial professionals

- The ability to test multiple scenarios revolutionized how advisors could plan for various outcomes

2000s–Present: The Era of Advanced Analytics and Real-Time Adaptation

- Monte Carlo Simulations: Increased computing power enabled sophisticated risk analysis—now standard in most financial plans

- Advanced Tools: Python, R, and AI-powered platforms are reducing reliance on spreadsheets and enabling automation

- Integrated Approach: Modern finance incorporates big data, artificial intelligence, and machine learning to improve forecasting, risk management, and decision-making

- Behavioral Factors: Future models increasingly factor in investor behavior and psychology, along with market irrationalities

While today’s models are more sophisticated than ever, they remain plans rather than certainties. Knowing when to follow the model’s direction and when to take a detour requires expertise. An experienced wealth advisor can be your navigator.

Garbage In, Garbage Out: The Importance of Accurate Inputs

Similar to how a GPS system requires accurate starting coordinates and destination information, a financial model is only as reliable as its inputs. To assess the reliability of your financial plan, it’s essential to evaluate both the predictable and unpredictable variables that drive outcomes.

Known Variables (Predictable Factors)

These are the foundational elements of your financial plan:

- Current resources (your balance sheet)

- Current income and spending needs

- Ages of plan participants

- Defined financial goals (legacy and philanthropic objectives)

Unknown Variables (Uncertain Factors)

These factors introduce uncertainty and require informed estimation:

- Expected investment returns

- Volatility and other investment risks

- Correlations between holdings

- Future purchasing power (inflation)

- Tax rates and portfolio turnover velocity

- Life expectancy of plan participants

Modern Monte Carlo simulation tools integrate these inputs to provide probability-based outcomes, helping inform asset allocation and long-term financial stability. However, even the most advanced model can’t perfectly predict the future.

That’s where professional guidance becomes indispensable—not just to input the right data, but to interpret results, stress-test assumptions, and adapt when reality diverges from the model. Like a skilled navigator who knows when to question the GPS’ recommendation, an advisor understands when market conditions, economic shifts, or personal circumstances warrant recalibration of your financial roadmap.

When the Master Plan Meets Reality: Unexpected Detours

Financial models provide valuable guidance, but history repeatedly demonstrates how unforeseen events can challenge even the most carefully crafted plans. Two significant events in the past 25 years illustrate the danger of blindly following models without professional interpretation:

2008 – The Great Financial Crisis: When All Roads Led Downward

During this crisis, nearly all major risk asset classes experienced severe, simultaneous losses:

- MSCI Global Stock Index: -40.3%

- Corporate Bond Index: -4.9%

- High Yield Bonds: -26.2%

- Public REIT Index: -37.7%

- US Private Equity Index: -30%

The Model Failure: The traditional belief in diversification as a risk management tool collapsed when every risk asset became highly correlated. Many investors who rigidly followed their models found themselves in free fall, with no safe havens in sight. This “Black Swan Event” wasn’t predicted by standard financial models, which hadn’t accounted for such extreme short-term declines or the simultaneous collapse of multiple asset classes.

The Navigator’s Value: Advisors who recognized the limitations of traditional models and took proactive measures—increasing cash reserves, implementing tactical hedges, or simply providing the steady guidance needed to prevent panic selling—helped clients navigate this treacherous period with minimal long-term damage.

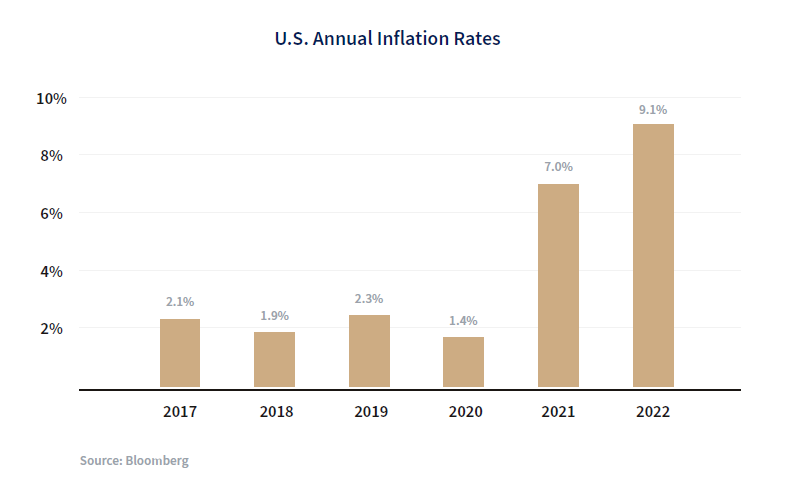

2021–2023 – The COVID-19 Fallout: Inflation’s Unexpected Surge

This period saw inflation skyrocket by 19.5% over three years—far beyond what most models had projected.

The Model Failure: Standard spending projections became obsolete as the purchasing power of portfolios eroded more rapidly than anticipated. Individuals who adhered to outdated spending parameters risked depleting their resources faster than planned.

The Navigator’s Value: Proactive advisors adjusted spending recommendations, restructured portfolios to include inflation hedges, and provided contextualized guidance to help clients maintain their financial security despite the shifting economic landscape.

Beyond Models: The Human Element in Financial Planning

Financial models are essential tools, but cannot replace the judgment, experience, and adaptability professional advisors bring to wealth management. Think of your financial model as a sophisticated plan that requires ongoing interpretation and adjustments:

- Models Don’t Adapt on Their Own: While a GPS can reroute based on traffic, financial models need human intervention to incorporate changing market conditions, policy shifts, or personal circumstances

- Experience Matters: Seasoned advisors have navigated multiple market cycles and can recognize patterns that models might miss

- Behavioral Coaching: Perhaps the most valuable aspect of professional guidance is helping clients avoid emotional decisions during market volatility—preventing the classic “buy high, sell low” mistake that no model can protect against

- Customized Interpretation: Your unique circumstances require personalized interpretation of model outputs—what works for one investor may be entirely inappropriate for another with different goals, time horizons, or risk tolerance

Conclusion: The Dynamic Partnership of Models and Expertise

From basic ledger calculations to AI-driven analytics, financial modeling continues to evolve. Future models will likely bring greater automation, deeper integration of alternative data, and more sophisticated decision-making tools. Yet the fundamental truth remains: a financial model is a plan, not a guarantee.

The only certainty in financial planning is that real life will never perfectly match projections. Models provide the roadmap, but navigating the journey requires ongoing vigilance and expertise. With the right inputs, professional guidance, and an adaptive approach, your financial strategy can remain resilient through changing conditions.

By combining advanced modeling with real-world expertise, your advisor serves as both navigator and guide—helping you stay on course toward your financial goals while steering clear of unexpected cliffs. Together, you can ensure that your wealth strategy remains strong, adaptable, and truly built to last.

Important Disclosures

The views and opinions included in these materials belong to their author and do not necessarily reflect the views and opinions of NewEdge Capital Group, LLC.

This information is general in nature and has been prepared solely for informational and educational purposes and does not constitute an offer or a recommendation to buy or sell any particular security or to adopt any specific investment strategy.

NewEdge and its affiliates do not render advice on legal, tax and/or tax accounting matters. You should consult your personal tax and/ or legal advisor to learn about any potential tax or other implications that may result from acting on a particular recommendation.

The trademarks and service marks contained herein are the property of their respective owners. Unless otherwise specifically indicated, all information with respect to any third party not affiliated with NewEdge has been provided by, and is the sole responsibility of, such third party and has not been independently verified by NewEdge, its affiliates or any other independent third party. No representation is given with respect to its accuracy or completeness, and such information and opinions may change without notice.

Investing involves risk, including possible loss of principal. Past performance is no guarantee of future results.

Any forward-looking statements or forecasts are based on assumptions and actual results are expected to vary from any such statements or forecasts. No assurance can be given that investment objectives or target returns will be achieved. Future returns may be higher or lower than the estimates presented herein.

An investment cannot be made directly in an index. Indices are unmanaged and have no fees or expenses. You can obtain information about many indices online at a variety of sources including: https://www.sec.gov/answers/indices.htm.

All data is subject to change without notice.

© 2025 NewEdge Capital Group, LLC