The Headlines

- It’s a jungle out there: S&P500 Q3 earnings are expected to decline -0.3% year-over-year (YoY), although this headline number masks wide dispersion between the sectors with the highest EPS growth (Communications at +32% YoY) and the lowest (Energy at -38% YoY)

- The eye of the storm passes: This season may mark the end to the recent earnings recession that began in 4Q22, with margin pressures easing sequentially and earnings growth broadening out across sectors. Expectations for a return to YoY EPS growth in Q4 and 2024 show that analysts expect these trends to continue.

- Magnificent for a reason: The Magnificent Seven stocks (the seven largest companies in the S&P500) are expected to carry the bulk of earnings growth this quarter, with estimates for a whopping **double checks notes** 35% revenue growth and 200% earnings growth YoY.

- Something for everyone: Depending on how you slice it, this earnings season could generate vastly different narratives about the underlying trends in corporate profits. Excluding the energy sector, S&P earnings are expected to rise 4%, but excluding the top 5 companies by market capitalization, S&P earnings are expected to decline -4% YoY.

It’s Been a Long, Cold, Lonely, Winter: Is 3Q23 the End to the Earnings Recession?

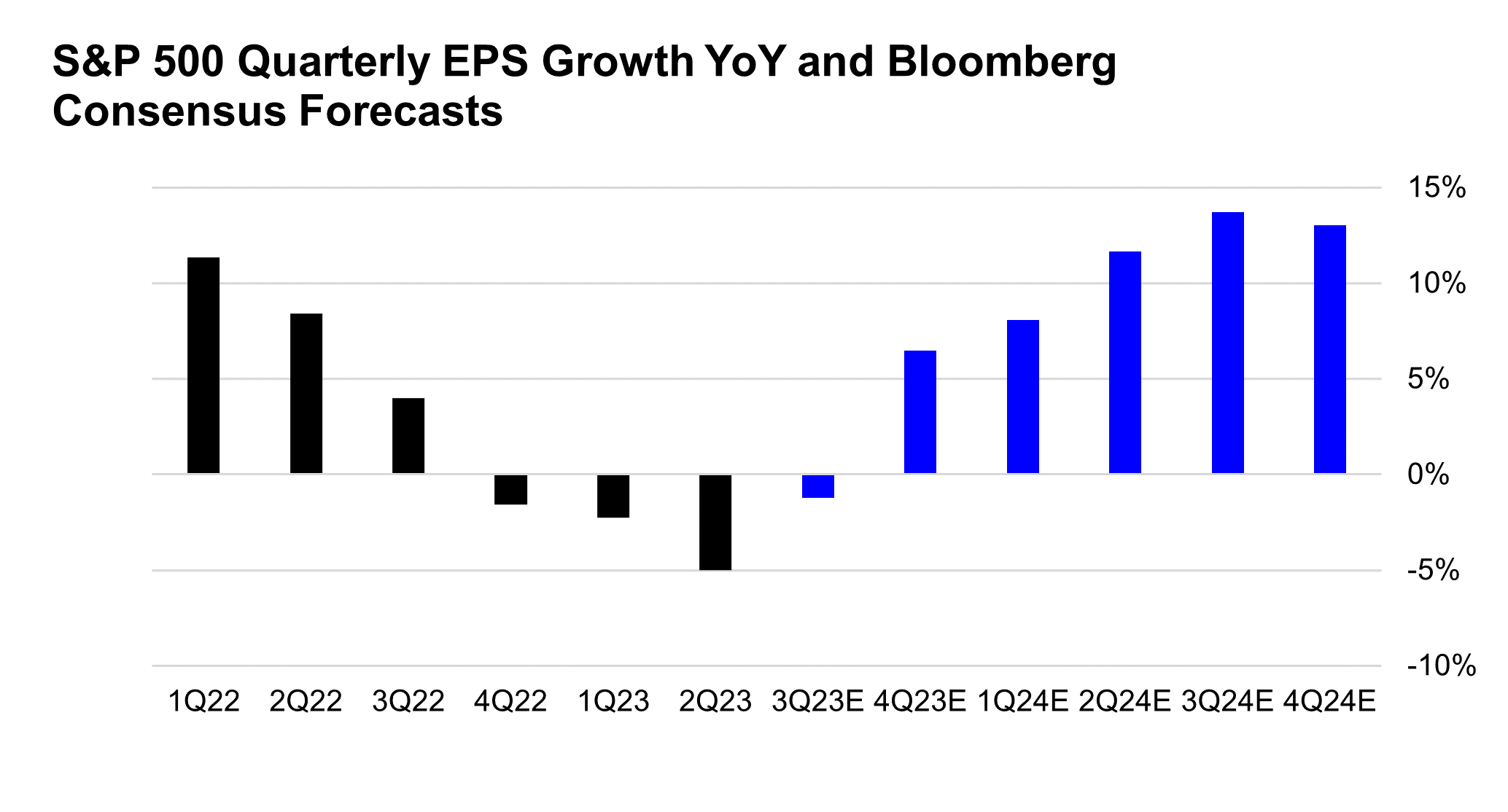

An earnings recession began in S&P 500 EPS in the fall of 2022. Earnings began to decline in 4Q22 and have continued to post YoY drops in each subsequent quarter. Based on consensus forecasts, analysts expect this to be the last quarter of YoY EPS declines, with a return to growth in 4Q23 and into 2024. Importantly, this earnings recession occurred without an economic recession, but instead was the result of normalizing/falling operating margins after the surge in margins in 2021/2022 driven by strong corporate pricing power. Importantly, if an economic recession were to materialize in 2024 or after, renewed earnings weakness could be expected, challenging the current consensus forecasts of strong growth next year and the year after.

Third Quarter 2023 Preview

For the third quarter, broad S&P 500 Index level corporate earnings growth looks somewhat uneventful, with expectations for -0.3% YoY EPS growth and +1.7% YoY revenue growth. Below the surface however, sector level expectations indicate wide dispersion across industries, highlighting how the current economic environment of slowing consumption and tightening financial conditions is having a divergent impact on a wide range of companies.

While consensus is expecting another quarter of modest declines in corporate earnings, generally companies appear to be turning a corner when it comes to generating profit growth. If results follow expectations, the third quarter would represent the fourth consecutive quarterly decline in profit growth, however it would be the best quarter since the current earnings recession began in the fall of 2022, and a substantial improvement from the -5% YoY earnings decline in the second quarter.

Revenue growth of 1.7% YoY, while less than half the rate of current YoY CPI inflation, would also indicate a potential trough in top line growth. It would match the revenue growth generated in the second quarter and suggest that the slowdown from double digit top-line growth one year ago may be bottoming out.

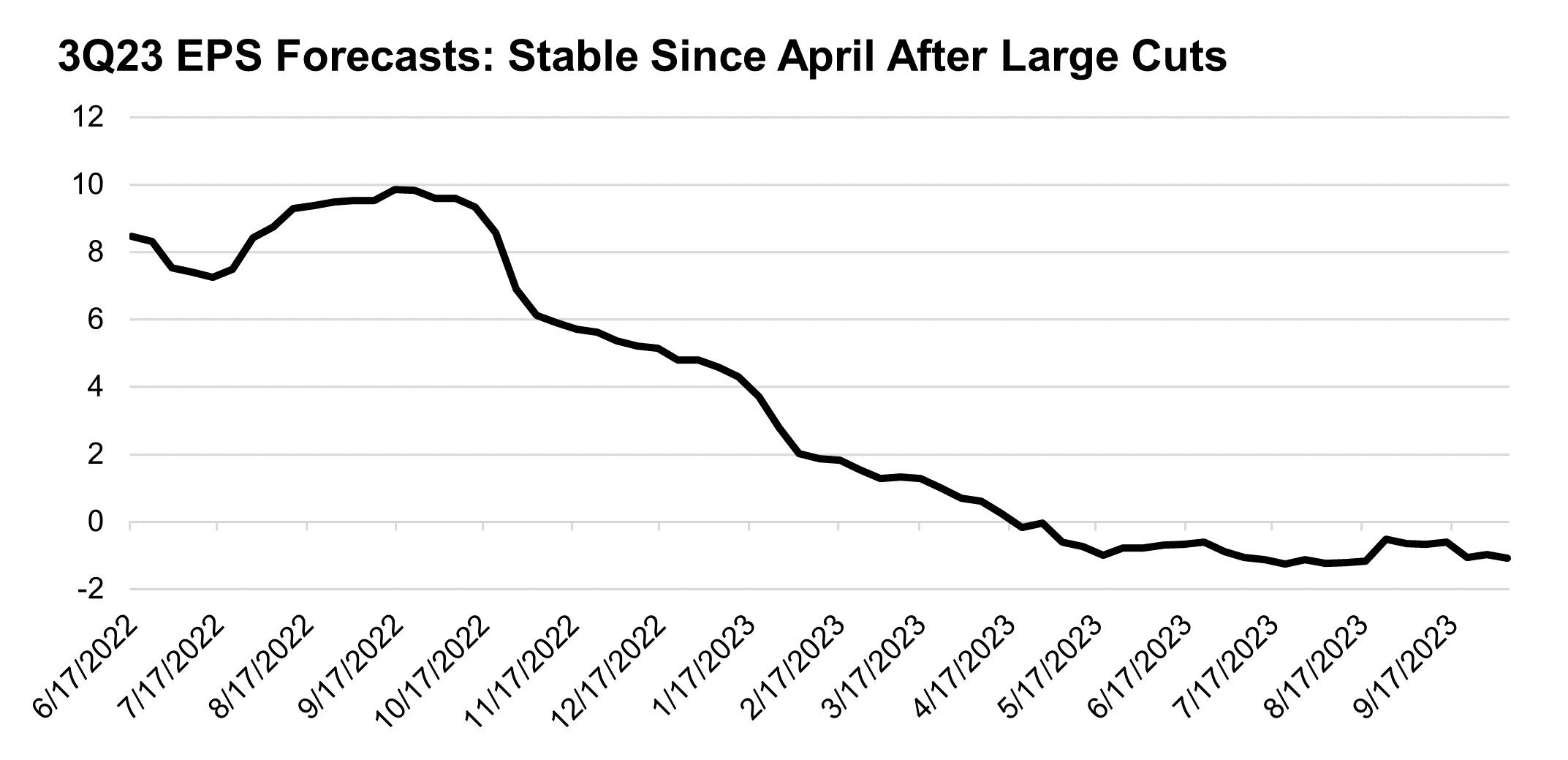

Typically, earnings expectations are revised lower by about 3-4% as we approach a new season, which often lowers the bar for earnings beats. However, this season there has been very little change to the headline third quarter earnings estimate, which sits almost exactly where it did at the end of June. In our view, index level earnings estimates are masking the substantial revisions at the sector level, as the increased expectations of +8% in the Consumer Discretionary sector +5% in the Technology sector are offsetting negative revisions in a number of other sectors.

Not All Sectors Are Created Equal

In aggregate 8 of 11 sectors are expected to post positive YoY earnings growth this quarter, an improvement from the 6 of 11 sectors that reported positive YoY earnings growth in the second quarter. Consensus expects this quarter to be led by earnings growth in the Communications sector at +32% YoY, followed by the Consumer Discretionary sector at +22% YoY. The weakest earnings growth is once again expected to come from the Energy sector at -38% YoY and the materials sector at -22% YoY. Looking for the Brightside in Energy and Materials, these large declines in 2023 set up for easy YoY comparisons in 2024, creating potential for improved growth next year.

The Financials sector is expected to be a surprising bright spot this quarter, posting 9% YoY earnings growth, which would break a stark streak of 6 straight quarterly earnings declines. Within the sector the highest earnings growth is expected in the insurance and financial services industries, while the traditional banking industry is expected to post modest 4% YoY growth. Businesses with heavy investment banking and capital markets franchises are expected to post -7% YoY growth, due to continued sluggish underwriting and advisory revenues for IPOs, debt issuance, and M&A.

Third quarter earnings season began Friday morning with reports from some of the nation’s largest banks including J.P. Morgan, Wells Fargo, and Citigroup. The results were broadly better than expected, and generally illustrate resilient profitability in the face of economic uncertainty, however concerns remain about slowing loan growth, weakening consumer balance sheets, and challenges on the banks’ own balance sheets due to the recent jump in rates.

Margins Front and Center

This year we have written extensively about profit margins and how rising input costs, wage pressures, and slowing top line growth have squeezed corporate profitability in virtually every industry. Expectations of 1.7% revenue growth and -0.3% earnings growth indicate the squeeze is ongoing, but expectations suggest these pressures may be easing.

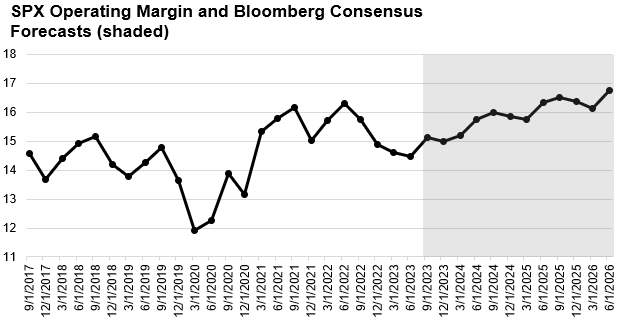

Expectations for Q3 call for index level operating margins of 15.1%, and while this is lower than the 15.8% operating margins we saw a year ago, it does represent a sequential improvement from the second quarter’s operating margin of 14.5%. This increase is expected to come mainly from margin expansion in the healthcare and industrials sectors, although the biggest sector in the index, technology, is also expected to report margin expansion, boosting index leading operating margins from 29% last quarter to 31% this quarter.

While this is an encouraging sign, sustained margin improvement will likely be difficult in this environment and likely act as an anchor on earnings growth in the coming quarters, driven by the combined forces of resilient wage growth, a “higher for longer” interest rate regime, fading pricing power, and accelerating capex needs. We note that current forecasts for 2024 earnings incorporate a return to near-record margins for the S&P 500, which could be a challenge next year given this backdrop.

Magnificent Growth from the Magnificent Seven

Lastly, turning to the Magnificent Seven Stocks, the seven largest companies in the S&P500 which account for 28% of the index market capitalization are expected to post…well magnificent results. These companies (Apple, Microsoft, Alphabet, Nvidia, Amazon, Meta, Tesla) are expected to post average revenue growth of 35% and average earnings growth of 200% YoY. These averages are heavily skewed by Nvidia which is expected to post over 1,000% EPS growth for the quarter, but even excluding Nvidia, the remaining companies are expected to post average EPS growth of 60% YoY.

The equal weighted basket of these Magnificent Seven companies is up over 95% in 2023, accounting for the majority of the S&P500s year-to-date returns. This strong performance has been driven by the combined forces of cost cutting, core business reacceleration, and investor enthusiasm about AI. While this has led to multiple expansion in each of these companies, this expansion only accounts for about half of the YTD return, illustrating the robust earnings momentum that is occurring under the surface within these companies. This earnings momentum is leading to continued positive revisions for the group as well, as over the last two months forward EPS estimates have been revised higher by more than 10%. While the group trades at a premium valuation of 34x the next twelve months earnings estimates and 7x sales, their dominant position in the index and healthy growth outlook is one reason why the health in this handful of names has been able to carry the market cap weighted S&P 500.

Conclusion

Overall, we see potential for earnings to come in better-than-expected for 3Q23, as they do most quarters (over the past 10 years companies have exceeded earnings expectations 73% of the time by an average of 6.4% according to FactSet), but more importantly, we will be following companies’ commentary about their expectations for growth and profitability as we near 2024. Will they strike a cautious note about the uncertain economic and market environment, or will they sing The Beatles and look for the sun to come out for growth into next year? We’ll listen closely and report back to you on the other side of earnings season.

Top Points of the Week

By Austin Capasso and Ben Lope

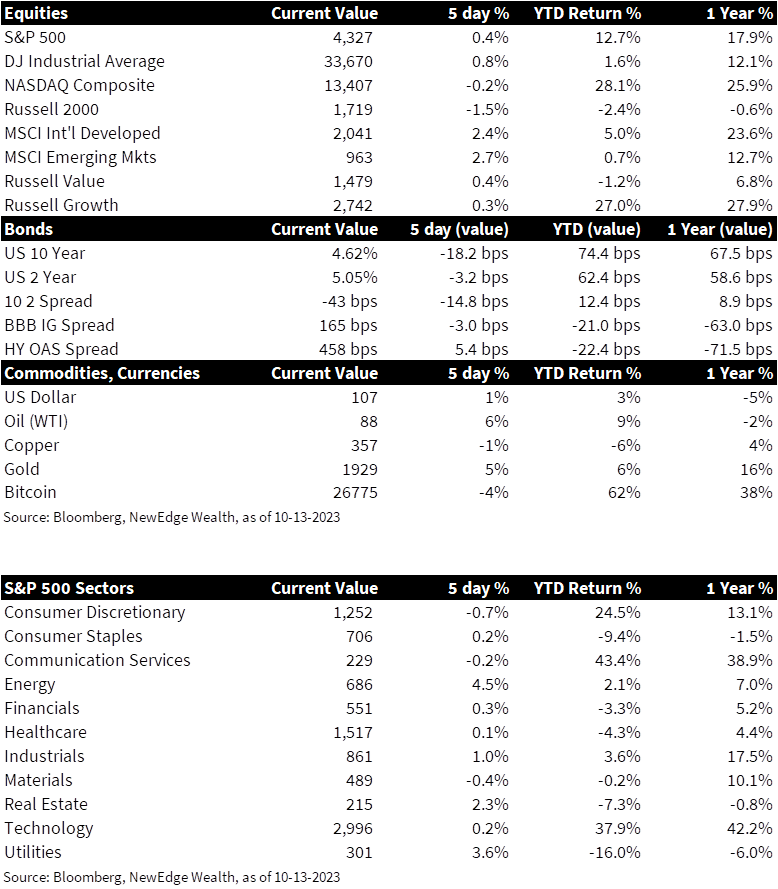

1. Global Equities – US equities posted mixed results this week, as the Dow Jones Industrial Average and S&P 500 indices notched nominal gains, while the NASDAQ Composite ended the week down slightly and the Russell 2000 lost a percent and a half. There was no clear favorite between growth and value stocks. International stocks fared significantly better, with the MSCI Developed Markets and MSCI Emerging Markets Indices each up over 2%.

2. Treasury Market – Yields on 2-year Treasury bills ended the weekly slightly below the levels at which they began the week; however, yields on 10-year Treasury bills recorded a nearly 17bps decrease over the same period. These movement resulted in the 2-10 year yield curve reversing it’s recent trend of becoming less inverted to instead invert by an additional 15bps. Elsewhere in the Treasury market, the 30-year auction saw thew weakest foreign investor demand in over a year, forcing primary dealers to purchase more bonds than in previous auctions.

3. Oil prices see a spike – Oil prices have been on a steady rise for the past few months. Prices are heavily influenced by the Israel-Hamas war, which could possibly involve other countries rich in oil supply, such as Iran. The involvement of Iran is speculative at this point, but if Iran becomes involved in the conflict, up to 20 million barrels of oil per day could be affected by either direct disruption or through obscured logistics (ANZ Oilfield Services). Brent is up 1.7% and WTI is up 1.9% on the week. We will continue to monitor the conflict and price reactions closely.

4. Hamas terror attacks spark war with Israel – More than 1,300 Israelis were killed and up to 150 taken hostage by Hamas, the Islamist political and military group that governs the Gaza Strip, after the group invaded Israel on Saturday, October 7, in a surprise terror attack that threatens to tip more of the region into conflict. Israel’s military eliminated all Hamas fighters within their borders and have since begun a “complete siege” of Gaza, killing 1,500 Palestinians as the IDF targets Hamas personnel and military assets. The US has vocalized unwavering support for Israel as the nation prepares for a ground assault within Gaza to root out the terror group. In advance of this assault, Israeli officials have instructed approximately 1.1 million Palestinians to vacate northern Gaza.

5. Republican House Speaker position still up for grabs – The Republican Congressional majority will hold a new closed-door vote on their preferred nominee for House Speaker, after their previous nominee, Steve Scalise, failed to gain enough votes to assume the role. The primary contenders for this nominee position are Jim Jordan of Ohio and Austin Scott of Georgia. Party leadership has instructed Republican House members to remain in Washington on Friday so that the closed-door vote can be completed.

6. US September CPI report comes in hotter than expected – The consumer price index (CPI) increased 0.4% on the month and 3.7% from a year ago on a headline basis, above respective forecasts for 0.3% and 3.6%. Core CPI, which strips out volatile parts of food and energy, increased 0.3% on the month and 4.1% on a 12-month basis, both exactly in line with expectations. Energy drove most of the story, with prices rising 1.5%, including a 2.1% spike in gasoline prices and 8.5% increase in fuel oil. The market reacted with a 4-5bps spike in yields of longer maturity bonds.

7. Fed speak this week reiterates their policy mantra: “higher for longer” – Nearly 16 Fed members spoke this week who all gave similar rhetoric on the current stance of Fed policy. The main takeaway, which was reiterated in the Fed Minutes, was that the Fed will remain in a “higher for longer” stance. The Fed believe they have reached sufficient rates to where they can skip a rate hike in the next FOMC meeting in November. However, the Fed still has one more rate hike priced into the Dot Plot before year end, so a rate hike for December’s meeting, which currently has a 25-30% probability of happening, is not out of the question.

8. US PPI report comes in higher than expected – The headline producer price index (PPI) increased 0.5% for September on a month over month basis, against the Dow Jones estimate for a 0.3% rise. The headline reading on a year over year basis increased 2.2%, which is the largest move since April. Core PPI, which excludes food and energy, was up 0.3%, versus the forecast for 0.2%. The hotter than expected reading stemmed from energy prices after gasoline prices rose 5.4%. Investors reacted with a flight to safety into longer maturity bonds given the uncertainties in markets.

9. Financials kick off 3Q 2023 earnings season – Three of the largest banks, JP Morgan (JPM), Citigroup (C), and Wells Fargo (WFC), started Q3 earnings off with encouraging results. Despite a narrative of lingering concerns regarding slower growth and a tougher economic environment, all three companies showed healthy profitability with beats on both top and bottom lines. Financials are projected to post 9% EPS growth off of easier year over year comparisons and are expected to be bright spot this earnings season.

10. Next week’s key economic data – The marquee data points next week include an abundance of Fed speakers on current policy, Fed Beige Book, US retail sales, Philadelphia Fed manufacturing survey, and a look into US leading economic indicators. This will give investors a glimpse into the dynamic of the consumer, health of factories and production, and a chance to hear different perspectives from various Fed members, including Raphael Bostic, who has been the medium between the Fed and markets. Next week’s earnings headline more companies within the Financials sector that should give a good idea of the economy’s health.

IMPORTANT DISCLOSURES

Abbreviations/Definitions: Beige Book: Summary of Commentary on Current Economic Conditions by Federal Reserve District is a report is published eight times per year, where each Federal Reserve Bank summarizes anecdotal information on current economic conditions in its District; Bostic: Raphael Bostic, President of the Federal Reserve Bank of Atlanta; Core CPI: measures the changes in the price of goods and services, excluding food and energy;

Core PPI: measures the change in the selling price of goods and services sold by producers, excluding food and energy. Dot Plot: The Fed dot plot is published quarterly as a chart showing where each of the 12 members of the FOMC expect the federal funds rate to be for each of the next three years and the long term; EPS: earnings per share; Fed speak: refers to speeches about monetary policy given by members of the U.S. Federal Reserve Bord of Governors; FOMC: Federal Open Market Committee; Headline CPI: the raw inflation figure reported through CPI that calculates the cost to purchase a fixed basket of goods to determine how much inflation is occurring in the broad economy; Leading Economic Index (LEI): provides an early indication of significant turning points in the business cycle and where the economy is heading in the near term; Philadelphia Fed Manufacturing Index: measures changes in business growth covering the Pennsylvania, New Jersey, and Delaware region; PPI: Producer Price Index; Retail Sales: represents a key macroeconomic metric that tracks consumer demand for finished goods and acts as a key economic barometer and whether inflationary pressures exist. Retail sales are measured by durable and non-durable goods purchased over a defined period of time.

Index Information: All returns represent total return for stated period. S&P 500 is a total return index that reflects both changes in the prices of stocks in the S&P 500 Index as well as the reinvestment of the dividend income from its underlying stocks. Dow Jones Industrial Average (DJ Industrial Average) is a price-weighted average of 30 actively traded blue-chip stocks trading New York Stock Exchange and Nasdaq. The NASDAQ Composite Index measures all NASDAQ domestic and international based common type stocks listed on the Nasdaq Stock Market. Russell 2000 is an index that measures the performance of the small-cap segment of the U.S. equity universe. MSCI International Developed measures equity market performance of large, developed markets not including the U.S. MSCI Emerging Markets (MSCI Emerging Mkts) measures equity market performance of emerging markets. Russell 1000 Growth Index measures the performance of the large- cap growth segment of the US equity universe. It includes those Russell 1000 companies with relatively higher price-to-book ratios, higher I/B/E/S forecast medium term (2 year) growth and higher sales per share historical growth (5 years). The Russell 1000 Value Index measures the performance of the large cap value segment of the US equity universe. It includes those Russell 1000 companies with relatively lower price-to-book ratios, lower I/B/E/S forecast medium term (2 year) growth and lower sales per share historical growth (5 years). The BBB IG Spread is the Bloomberg Baa Corporate Index that measures the spread of BBB/Baa U.S. corporate bond yields over Treasuries. The HY OAS is the High Yield Option Adjusted Spread index measuring the spread of high yield bonds over Treasuries.

Sector Returns: Sectors are based on the GICS methodology. Returns are cumulative total return for stated period, including reinvestment of dividends.

The views and opinions included in these materials belong to their author and do not necessarily reflect the views and opinions of NewEdge Capital Group, LLC.

This information is general in nature and has been prepared solely for informational and educational purposes and does not constitute an offer or a recommendation to buy or sell any particular security or to adopt any specific investment strategy.

NewEdge and its affiliates do not render advice on legal, tax and/or tax accounting matters. You should consult your personal tax and/or legal advisor to learn about any potential tax or other implications that may result from acting on a particular recommendation.

The trademarks and service marks contained herein are the property of their respective owners. Unless otherwise specifically indicated, all information with respect to any third party not affiliated with NewEdge has been provided by, and is the sole responsibility of, such third party and has not been independently verified by NewEdge, its affiliates or any other independent third party. No representation is given with respect to its accuracy or completeness, and such information and opinions may change without notice.

Investing involves risk, including possible loss of principal. Past performance is no guarantee of future results.

Any forward-looking statements or forecasts are based on assumptions and actual results are expected to vary from any such statements or forecasts. No assurance can be given that investment objectives or target returns will be achieved. Future returns may be higher or lower than the estimates presented herein.

An investment cannot be made directly in an index. Indices are unmanaged and have no fees or expenses. You can obtain information about many indices online at a variety of sources including: https://www.sec.gov/answers/indices.htm.

All data is subject to change without notice.

© 2026 NewEdge Capital Group, LLC