Introduction

The unofficial end of summer is upon us. Stocks are up, rates (OK, some rates) may be on their way down, and a growing handful of officials at the Fed and the Bureau of Labor Statistics are on their way out. After spending the past three months writing about stock markets, bond markets, AI, the Fed, the yield curve, and AI, again, we can’t help but think we’ve missed something…

“Well, what else could we be forgetting?”

…

“HOUSING!!”

Yes, housing, the sick man of the U.S. economy for the past few years, is a topic we’ve not addressed directly since about this time last year. With the selling season dying down, we’ll use this edition of the Weekly Edge to supply some Labor Day beach reading on the state of the U.S. housing market, with inspiration from perhaps the most famous movie ever to take place almost entirely in a single house: Chris Columbus’ 1990 classic, Home Alone.

Housing’s Importance to the Economy

“You guys give up, or you thirsty for more?”

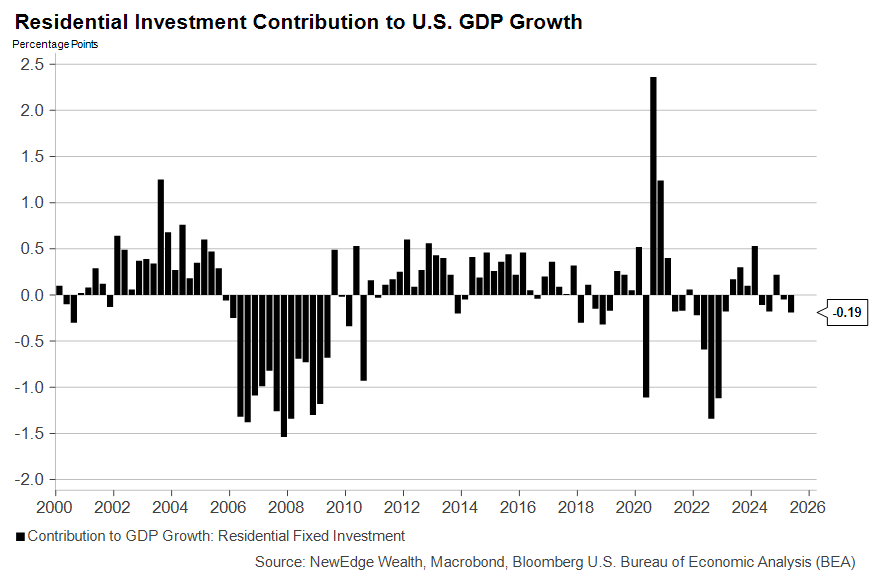

While rarely the largest contributor to U.S. economic growth, U.S. housing (or “residential investment” in GDP parlance) has often been a harbinger for broader economic trends. Construction and remodeling ground to a halt beginning in early 2006, many quarters before the start of the U.S. recession that coincided with the global financial crisis. Homebuilding also boomed in 2020 following the easing of COVID restrictions as cash-flush households demanded more living space, an indicator that growth would remain strong into the mid-2020s.

Most recently, the sector has been a small drag on GDP, with construction growth historically weak:

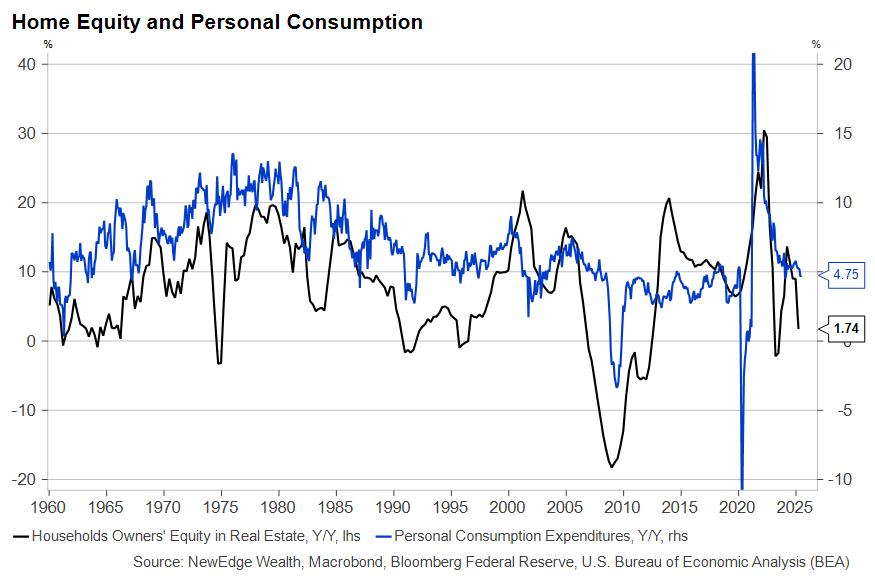

The housing market affects the economy in ways beyond the physical building or remodeling of homes. Rising home prices – or, more precisely, rising home equity – have a strong relationship with personal consumption growth. The recent softening in consumption growth from very high rates in the early 2020s has coincided with a flattening of home equity balances:

In addition to being sensitive to changes in home prices, consumer spending also lies downstream from home sales and construction. New homeowners tend to spend more than those who remain in place do. As more homes are built and sold, consumer spending tends to strengthen.

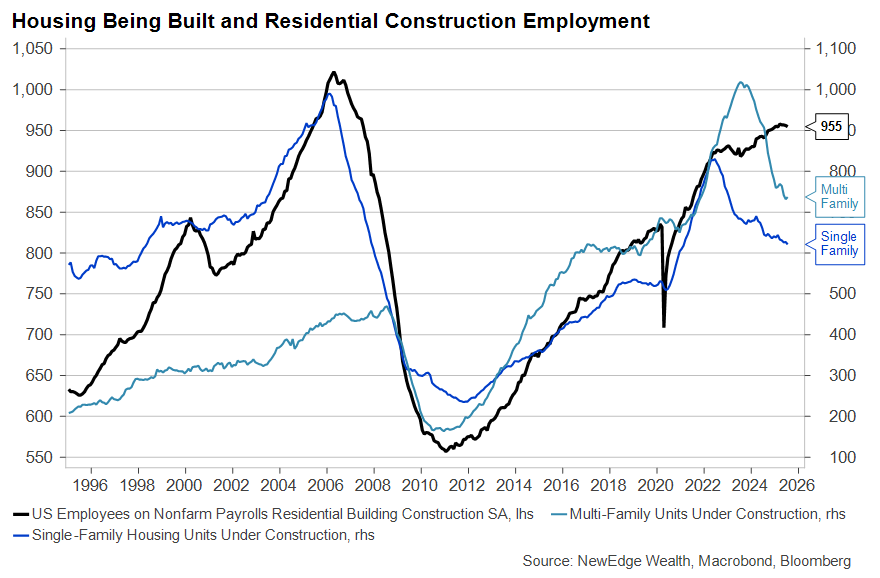

Residential construction is also a significant source of employment, with close to a million jobs tied directly to homebuilding and many more related to the broader housing industry. We have been struck by the sector’s resilience given the sharp declines in projects under construction. Builders may be more sensitive than other business owners to potential worker shortages, given a) their experience during and just after the pandemic; and b) the large percentage of construction workers potentially affected by the more restrictive immigration regime.

Housing (Still) in Recession

“Think positive, Frank!”

“You be positive. I’ll be realistic.”

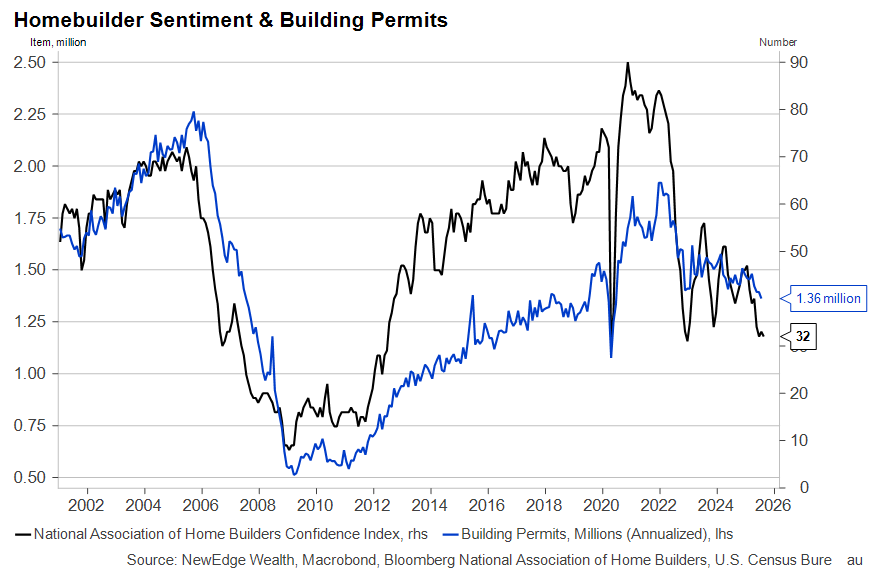

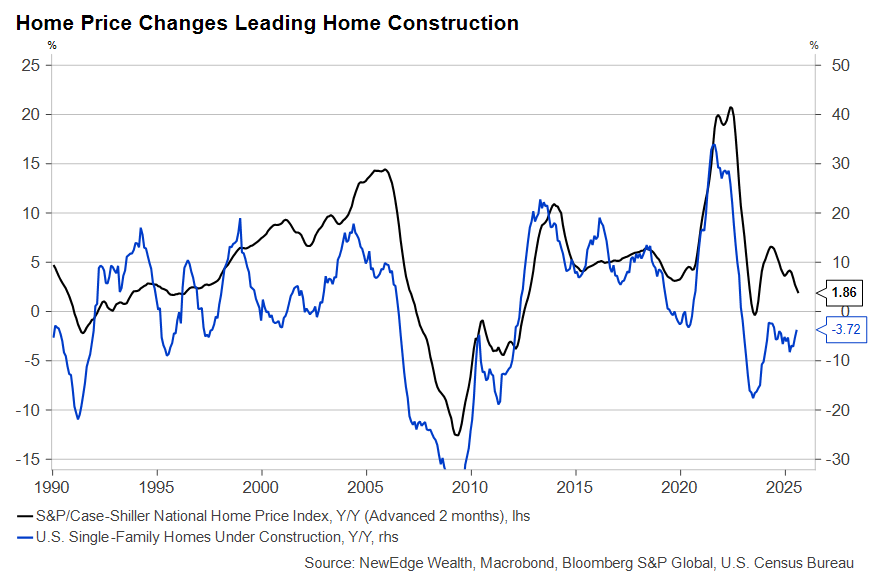

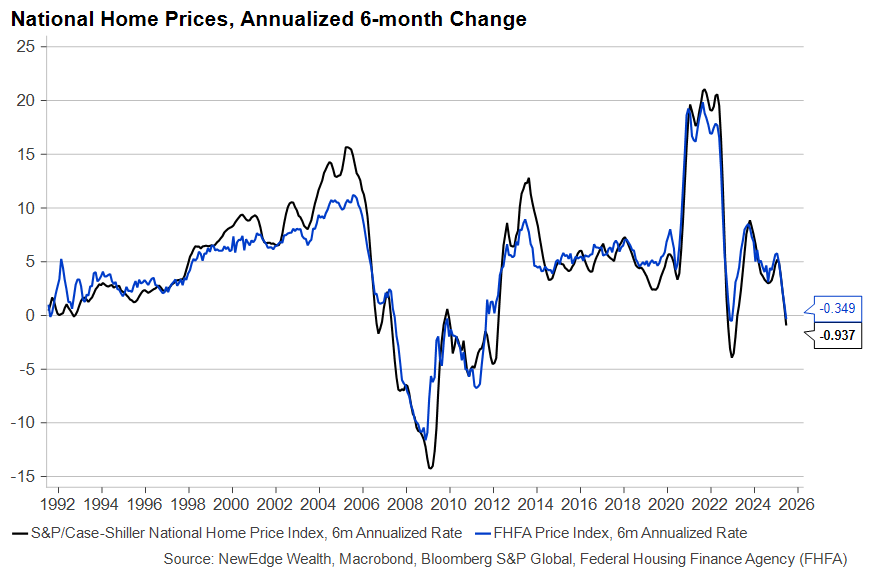

If none of the graphs in the previous section looked encouraging, it’s because the U.S. housing market has been in recession for over two years. Right now, it’s hard to find any aspect of the market – sales, construction, prices, hiring – that doesn’t look impaired. Homebuilder sentiment closely tracks permits for new construction, and both have taken further nosedives this summer:

What makes this cycle different from others, including the one leading up to the 2008 crisis, is that home construction growth (the blue line on the graph below) has been negative since 2022 despite national home prices (the black line) rising steadily:

This anomaly may be disappearing, but not in the way we would have hoped. June national home price data released this week showed a fourth straight month of declines despite 1) depressed inventories in many parts of the country; 2) mortgage rates close to two years removed from their highs; and 3) low unemployment.

Policy Connection

“Look what you did, you little jerk!”

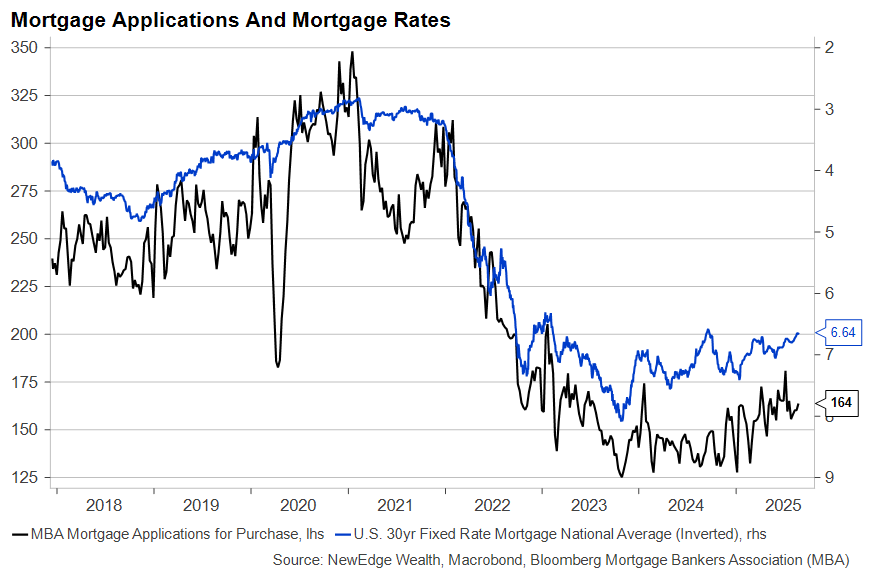

In our previous housing-themed Weekly Edge, we pointed out that years of zero-interest-rate policy had locked a large majority of homeowners in place. Rational fears of trading in a 3% mortgage for 7% one have prevented many people from moving homes (and jobs). We referred to this phenomenon as a frozen housing market. Things have thawed a bit since then, with mortgage rates down slightly and new mortgage applications for purchase off their lows.

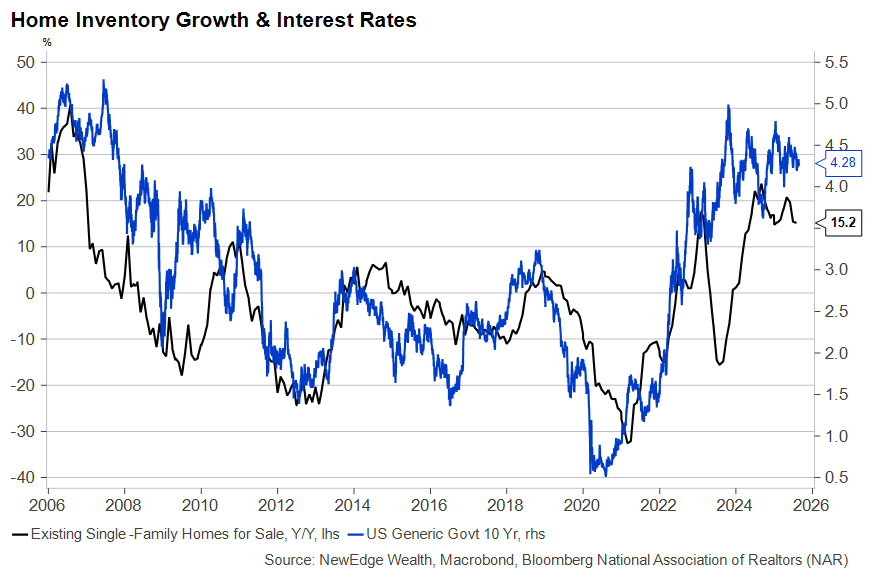

But the centripetal force of locked-in fixed-rate mortgages is certainly still affecting home sales. More sellers are coming to market than was the case a year ago, and inventories have grown at an impressive clip (the black line on the graph below) thanks to high rates, but sales of existing homes remain 20-30% below their pre-pandemic normal.

Given the weaker price trend we cited in the prior section and the hope that lower interest rates are just around the corner, more sellers are pulling their listed homes off the market in anticipation of an improving market ahead. That gamble may ultimately pay off, but if longer-term interest rates stay high, inventories could continue to build, and downward price pressures might only get worse.

In short, while the direction of monetary policy from here may be looser, years of ultra-loose policy in the 2010s, followed by far higher rates since 2022, continue to wreak havoc on both housing supply and demand. A break below 6% on 30-year fixed-rate mortgages may be hard for the Fed to achieve on its own, given the wide fiscal deficit and ongoing inflation concerns. But it’s hard to imagine sales and construction breaking out of their respective ruts anytime soon without lower borrowing costs.

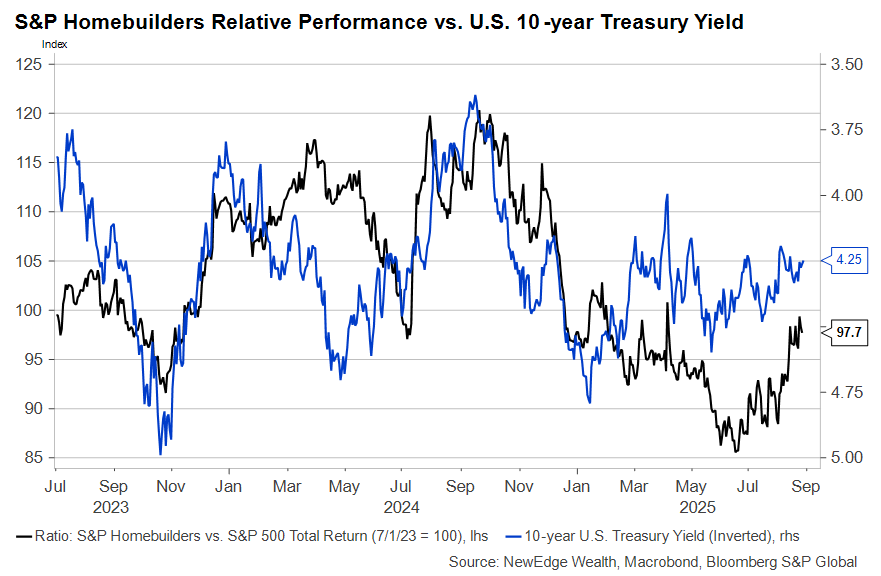

Housing Stocks

“Do you hear me? I’m not afraid anymore!”

As the likelihood of further Fed rate cuts has risen this summer, stocks of companies leveraged to a stronger housing market have seized the reins of leadership. Homebuilder stocks have risen relative to the S&P 500 (the black line on the graph below), as the 10-year U.S. Treasury yield has fallen from its May highs (the blue line against the inverted right axis). Markets are pricing in the potential for higher revenues – and earnings – that would follow from stronger construction growth.

Not all areas of the stock market leveraged to the housing market are exhibiting as much optimism. Many observers expected Home Depot to cite tariffs in its Q2 earnings call as a reason for diminished revenues or squeezed profit margins. Instead, the focus was on the lack of demand for building materials and other items related to home projects, resulting from the prolonged period of rising interest rates.

Small-cap companies, in general, tend to benefit from a drop in interest rates, particularly those that are sensitive to changes in borrowing costs. These stocks are up considerably so far in the third quarter. Non-profitable firms, which make up a large share of the Russell 2000 Small Cap Index, often employ leverage and are among the hardest hit during periods of rising rates. We are not chasing highly leveraged firms here, as many periods of outperformance ignited by interest rate optimism have proven fleeting.

Conclusion

“Keep the change, ya filthy animal!”

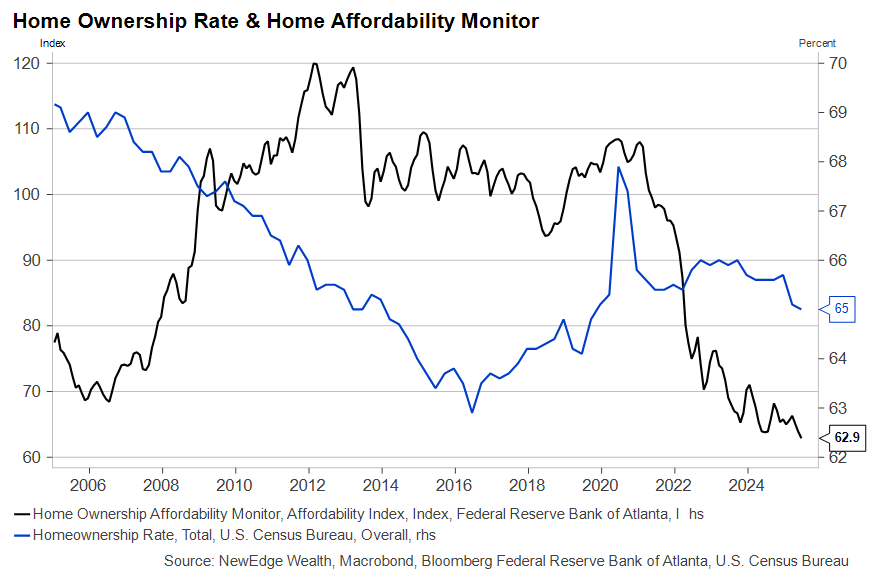

Our core concern about the U.S. housing market is the lack of affordability. Home purchases are an important source of downstream economic activity, and the construction that tends to follow strong sales and rising prices adds to overall prosperity. The latest trends in home ownership and affordability are not encouraging:

The best thing that can be said about the housing market in 2025 is that it does not appear to be as systemically ingrained in the financial system as it was in 2007, the last time affordability took a nosedive and ownership rates began to decline.

The U.S. economy can continue to grow – and many sectors like A.I. and broader technology can continue to flourish – in the absence of a normally functioning housing market. But consumer spending likely cannot return to its post-pandemic roar without a further pickup in home sales. And construction may remain in the doldrums until that happens, and the booms of the 2000s or early 2020s will have to remain “somewhere in our memory”.

IMPORTANT DISCLOSURES

The views and opinions included in these materials belong to their author and do not necessarily reflect the views and opinions of NewEdge Capital Group, LLC.

This information is general in nature and has been prepared solely for informational and educational purposes and does not constitute an offer or a recommendation to buy or sell any particular security or to adopt any specific investment strategy.

NewEdge and its affiliates do not render advice on legal, tax and/or tax accounting matters. You should consult your personal tax and/or legal advisor to learn about any potential tax or other implications that may result from acting on a particular recommendation.

The trademarks and service marks contained herein are the property of their respective owners. Unless otherwise specifically indicated, all information with respect to any third party not affiliated with NewEdge has been provided by, and is the sole responsibility of, such third party and has not been independently verified by NewEdge, its affiliates or any other independent third party. No representation is given with respect to its accuracy or completeness, and such information and opinions may change without notice.

Investing involves risk, including possible loss of principal. Past performance is no guarantee of future results.

Any forward-looking statements or forecasts are based on assumptions and actual results are expected to vary from any such statements or forecasts. No assurance can be given that investment objectives or target returns will be achieved. Future returns may be higher or lower than the estimates presented herein.

An investment cannot be made directly in an index. Indices are unmanaged and have no fees or expenses. You can obtain information about many indices online at a variety of sources including: https://www.sec.gov/answers/indices.htm.

All data is subject to change without notice.

© 2026 NewEdge Capital Group, LLC