“Go ahead. Make my millennium.”

The Federal Reserve has trimmed its policy target by 175 basis points (1.75%) since September 2024, but longer-term Treasury yields are actually higher today than they were then. This is running counter to President Trump’s transparent desires to bring interest rates down further to help stimulate recoveries in the housing and manufacturing sectors. While presidents have limited abilities to control rates on their own, they do have the power to nominate Governors to the Federal Reserve Board, which does set short-term interest rates.

In the 1988 classic, Beetlejuice, one can summon the titular character by saying his name three times. In doing so, multiple characters unleash a force they were not quite prepared for. The president has now similarly called for help from a source whose views and methods will be difficult to predict: “Kevin Warsh. Kevin Warsh. Kevin Warsh”. In this piece, inspired by the “ghost with the most” himself, we will dive deeper into Warsh’s views, the likely changes coming to the Fed’s approach, and the impact all of this may have on financial markets.

This week’s movie tie-in also affords us the chance to pay a brief tribute to the late Catherine O’Hara. Before she was Kevin’s mom in Home Alone or the iconic Moira Rose in Schitt’s Creek, she was the eccentric Delia Deetz in Beetlejuice, leading a dinner party in a hilarious haunted calypso. In this and every other role, she made us laugh.

“What do you think? You think I’m qualified?”

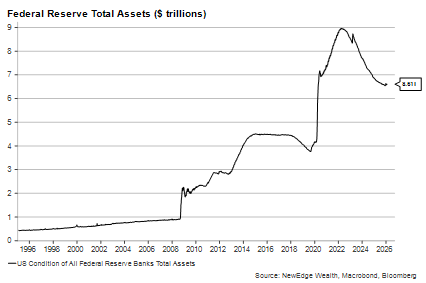

New Fed Chairs don’t come along that often. Jerome Powell has been in his seat since 2018, originally appointed by President Trump and reappointed in 2022 by President Biden. Chair Janet Yellen served for only one term before Powell, but before her, the Fed only had three different chairs since 1979. This makes President Trump’s nomination of Kevin Warsh to lead the central bank notable and almost certainly consequential. Warsh was the youngest Fed Governor ever, appointed by President George W. Bush in 2006 at the age of 35 and serving until 2011, when he resigned largely due to differences with then-Chair Ben Bernanke over the balance sheet expansion that eventually became known as QE2 (which was neither the first nor the last quantitative easing effort, as the chart below shows). As this decision would indicate, Warsh had a reputation for focusing on price stability (i.e., low inflation) over other factors in the pre- and post-GFC (Great Financial Crisis) period (i.e., high unemployment).

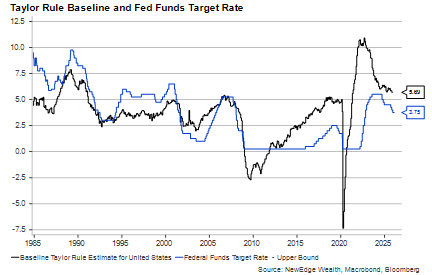

This might make Warsh seem a strange choice for a president who is laser-focused on getting the Fed to cut rates. But Warsh has been striking a more dovish tone since the 2024 election, positing that lower rates might now be appropriate. This view goes against widely used monetary policy guides like the Taylor Rule, which calls for the Fed to raise rates given relatively high inflation and relatively low unemployment:

“I’m just doin’ my job. Besides, I thought we had a deal!”

Warsh will certainly say more at his upcoming Senate confirmation hearing about how he’ll approach the job. Unlike other recent selections for Chair, Warsh has not been at the Fed for many years. While he has better industry connections than perhaps any previous nominee, he has also been pointedly critical of the Fed’s current approach to monetary policy and seems to be promising to bring sweeping changes to it. (“A little gasoline… blowtorch… no problem.”)

Warsh will lead a Federal Open Market Committee (FOMC) with a preexisting bias toward lower interest rates and ample liquidity provision. This could prove awkward for a central banker whose claim to fame has been opposing a large Fed balance sheet and resisting easier monetary policy during times of large federal budget deficits.

The trouble for Warsh – or any new Chair – is that the FOMC operates by consensus as a committee, not as a dictatorship, though the Chair does have disproportionate sway. Warsh’s preferred policy mix will likely be to further shrink the balance sheet – assuming he can do so without setting off a liquidity crisis – to create some room to lower interest rates. Remaking the Fed’s portfolio will likely require Warsh to coordinate closely with the U.S. Treasury, but it will also require buy-in from his colleagues.

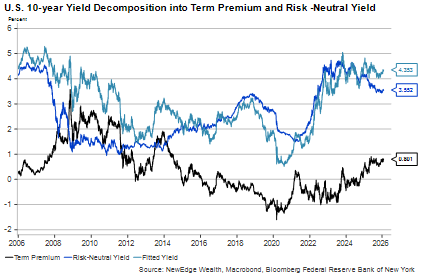

Warsh clearly has a mandate from the White House to lower interest rates, and most members of the FOMC will likely acquiesce to one or two cuts in the second half of the year unless the economy is roaring. But it will be difficult to lower short-term rates in such a way that does not set off inflation concerns and send long-term rates higher. Interestingly, when we decompose the 10-year U.S. Treasury yield into (a) expectations for short-term rates, and (b) the term premium, we find that things look quite a bit like 2006, the first time Warsh came to the Fed. The level of interest rates (the green line) is in the mid-4% range, and the term premium (the black line) is comparable:

To thread this needle, other Trump-adjacent policymakers – including soon-to-be former Governor Steven Miran (and now former Chair of the Council of Economic Advisors) – have mused that easier regulatory policy and A.I.-driven productivity gains could translate into precisely the kind of disinflationary growth that could recommend lower rates without setting off inflation. It is not clear how much purchase an argument that emphasizes the overall policy environment over the value of incoming data will have on the FOMC. Most members who favor rate cuts do so because they fear the labor market is weakening.

The FOMC Chair has never dissented from the majority opinion, but that could change in just a few months. If June is the first Warsh-led meeting and we still have stable unemployment and above-target inflation, it will be difficult for the newly-installed chair to sway the voting members to support his plea for rate cuts.

“It’s Showtime!”

Before the promise of a Warsh Fed becomes a reality, there are a few formalities to go through. First, a handful of Senate Republicans may stall the nomination process unless and until the Department of Justice drops the investigation into current Chair Jerome Powell. While this investigation officially centers on an ongoing Fed construction project with cost overruns, some Senators appear to believe that the true motivation is retribution over Powell’s failure to slash interest rates as aggressively as the administration would prefer. This is the Fed’s own interpretation of this legal action as well, as Powell made clear in this video.

Second, while Governor Miran will stay on the FOMC until Warsh is confirmed, Powell himself may also choose to step down when his chairmanship lapses, as most modern Chairs have. This would give President Trump a chance to nominate another Board Member to further reshape the committee. Powell is free to remain a governor until 2028, however.

Third, the Supreme Court is set to rule in the coming months on the president’s ability to fire Governor Lisa Cook for cause. Should the court rule in Trump’s favor, it could trigger a series of firings that could remake the Board virtually overnight and unlock even deeper rate cuts in 2026.

The big caveat to all of this is the economy itself. A recent string of good data, punctuated by uncomfortably warm producer price inflation and an unexpected spike in manufacturing sentiment, has complicated the case for aggressive rate cuts. Even a new Chair flanked by loyal deputies will be hard-pressed to get interest rates down if the data and the market are pushing in the other direction.

Investors are counting on stronger economic and earnings growth in 2026. If they’re correct, long-term interest rates are likely to remain elevated even if a doggedly dovish Fed is cutting overnight rates. If they’re wrong and the economy weakens, the Fed should have no problem getting rates to go lower. Neither scenario paints a promising picture for cyclical recoveries in construction or manufacturing, both of which could use lower interest rates, but not at the expense of a stagnant economy.

Without knowing precisely how things will play out, the Fed’s mantra starting in June may be, “Let’s turn the juice on and see what shakes loose.”

IMPORTANT DISCLOSURES

The views and opinions included in these materials belong to their author and do not necessarily reflect the views and opinions of NewEdge Capital Group, LLC.

This information is general in nature and has been prepared solely for informational and educational purposes and does not constitute an offer or a recommendation to buy or sell any particular security or to adopt any specific investment strategy.

NewEdge and its affiliates do not render advice on legal, tax and/or tax accounting matters. You should consult your personal tax and/or legal advisor to learn about any potential tax or other implications that may result from acting on a particular recommendation.

The trademarks and service marks contained herein are the property of their respective owners. Unless otherwise specifically indicated, all information with respect to any third party not affiliated with NewEdge has been provided by, and is the sole responsibility of, such third party and has not been independently verified by NewEdge, its affiliates or any other independent third party. No representation is given with respect to its accuracy or completeness, and such information and opinions may change without notice.

Investing involves risk, including possible loss of principal. Past performance is no guarantee of future results.

Any forward-looking statements or forecasts are based on assumptions and actual results are expected to vary from any such statements or forecasts. No assurance can be given that investment objectives or target returns will be achieved. Future returns may be higher or lower than the estimates presented herein.

An investment cannot be made directly in an index. Indices are unmanaged and have no fees or expenses. You can obtain information about many indices online at a variety of sources including: https://www.sec.gov/answers/indices.htm.

All data is subject to change without notice.

© 2026 NewEdge Capital Group, LLC