The Case of the Dovish Central Bank

It’s a strange case from the start. A case with a hole in the center. A doughnut.

This week, the Federal Reserve’s Open Market Committee (FOMC) held its final monetary policy gathering of the year, and it used the occasion to slash its policy target rate one more time. While the economic data flow remains impaired by the 43-day government shutdown, the committee saw enough weakness in the labor market to feel it needed to ease policy for the third time in as many meetings.

Investors in money market funds know that Fed decisions impact short-term yields immediately, but it’s not yet clear that the cumulative 1.75% reduction in the federal funds rate since September 2024 has had a meaningful positive impact on the economy. We’ll use this penultimate Weekly Edge of 2025 to discuss the reasoning behind the Fed’s decision, the frustration of waiting for policy changes to affect the economy, and the outlook for the Fed next year as it prepares to welcome a new Chair.

As our topic touches on both solving mysteries through the power of deduction and “cutting”, what better film to provide inspiration for this week’s piece than 2019’s Knives Out, the second sequel to which has just been released in theaters and on streaming. As Benoit Blanc (and a certain other famous detective) would say, the game is afoot.

The Fed Provides Important Clues About 2026

The complexity and the gray lie not in the truth but what you do with the truth once you have it.

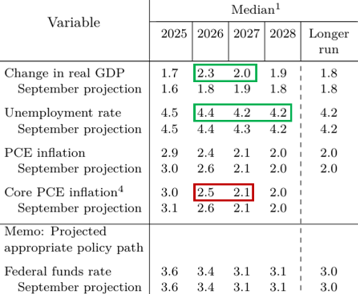

The Fed did not deliver any surprise twists at its December meeting, but it did leave a trail of breadcrumbs for us to follow as we attempt to deduce what might be in store for monetary policy in 2026. Let’s start with the Fed’s Summary of Economic Projections, which are updated four times each year

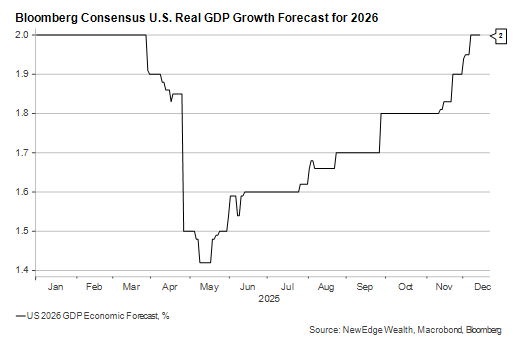

The most notable change is the upgrade to 2026 GDP growth to 2.3% (above current Bloomberg consensus at 2.0%), which suggests that members are becoming more constructive on the growth outlook and may not be inclined to reduce rates further. Supporting that view is the fact that the Fed still sees the labor market stabilizing next year, with unemployment topping out just a tick higher than it is today (4.4%), without any further policy help.

On the other side of the Fed’s dual mandate, they have modestly reduced inflation forecasts for both 2025 and 2026, even if projections out to 2027 remain somewhat above the 2% target. Chair Jerome Powell seemed confident in his press conference that much of this excess inflation will diminish once the goods price increases from this year’s new tariffs roll out of the one-year calculation.

Taken together, these forecasts suggest that the Fed does not see further easing as an urgent priority. That view can clearly be seen in the final set of forecasts showing just one cut in each of the next two years as the Fed glides its policy rate down to neutral.

At the same time, as Powell emphasized in his comments, the Fed remains data dependent. We would note that its current unemployment forecasts – benign as they are – set a rather low bar for further cuts should data disappoint in the coming months. If the November and December jobs reports surprise on the downside, the Fed could keep cutting rates in January and beyond.

Investors do, indeed, seem to suspect that the Fed’s employment outlook is too rosy but not significantly so. Market pricing shows a little more than two cuts for 2026. We would likely only see three cuts or more if the unemployment rate were to rise well above 4.5%.

Lower Long-Term Rates: The Dog That Isn’t Barking

Physical evidence can tell a clear story with a forked tongue.

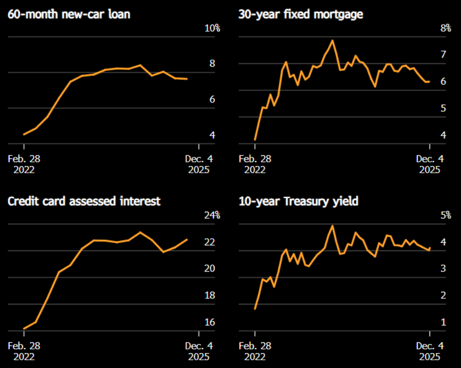

Investors and politicians have bemoaned the Fed’s lack of speed in getting interest rates down. Nearly 200 basis points of cuts in just over a year isn’t nothing, but consumers are not seeing sharply lower borrowing costs. This helpful set of charts from Bloomberg tells the story well. While the rates that consumers are most exposed to are down from their peaks, they remain well above the levels households became accustomed to in the 2010s and, more recently, in the immediate aftermath of the COVID-19 pandemic:

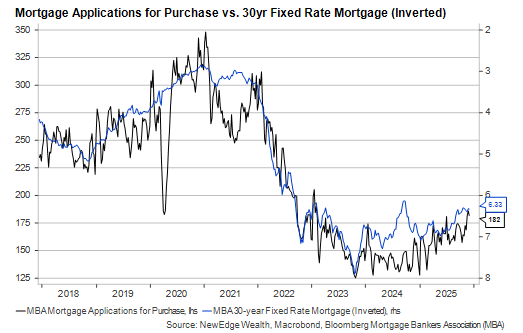

The 10-year U.S. Treasury rate is down a little in 2025, and 30-year fixed-rate mortgage rates are slightly lower than they were just before the Fed started cutting last year. But when rates are only down “slightly” or “a little”, the economic effects tend to be muted, as we’ve seen with the failure of mortgage applications to approach their 2018 average, let alone the peaks during the housing boom of late 2020 and early 2021.

Are higher long-term rates a red herring?

Funny, Ransom, you skipped the funeral, but you’re early for the will reading.

In both 2024 and 2025, long-term interest rates fell on initial hopes for Fed easing, only to move back up once the rate cuts were underway. This year’s low for the 10-year U.S. Treasury yield came nearly two months ago. While it isn’t unprecedented for long rates to begin moving up during an easing cycle, this usually happens in the context of a clear sign that the economy is bottoming.

The simplest explanation for rates’ refusal to fall further is that the outlook for the global economy in 2026 remains solid and may, in fact, be getting better. Outside the U.S., central banks in Europe and Japan are likelier to be hiking than cutting rates next year. And as U.S. economists refine their forecasts for 2026, we are seeing more upward than downward revisions, as the Bloomberg consensus average shows:

As Cameron wrote in last week’s piece, investors appear to be encouraged by the sunnier outlook, which has the potential to strengthen and broaden company earnings next year. This week’s rotation into economically sensitive U.S. small-cap stocks and cyclical sectors of the S&P 500 also reflect this optimism. The question is: will the rotation last and is this optimism justified?

The new Fed Chair’s influence may be suspect

I am here at the behest of a client.

The mysterious hole at the center of our policy uncertainty doughnut will be filled once we get news of 2026’s single biggest policy change: the new Chair of the Federal Reserve.

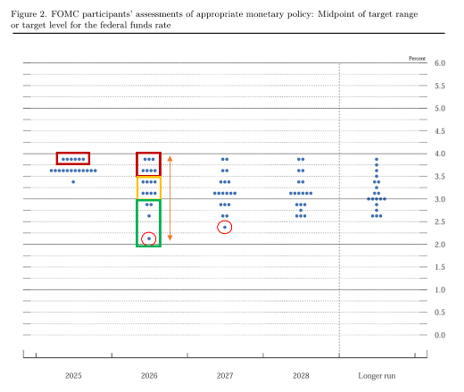

For most of 2025, the knives have been out for the Powell-led Fed, with a torrent of criticism from key members of the Trump administration, including now-Fed Governor Stephen Miran and likely Powell successor Kevin Hassett. Assuming Hassett gets the post (Polymarket has his chances at an imposing 74%), he will take the reins of the most divided FOMC in memory. The gap between the highest and lowest policy rate forecasts for 2026 in this past week’s new “dot plot” is just shy of 2%, and there is no central tendency among committee members.

At least seven members, not all of whom will be voters in 2026, currently do not see the need for additional rate cuts next year. Only four members favor more than two cuts. Even if the new Chair’s “dot” looks like Governor Stephen Miran’s (the red circles on the chart below), it will be hard for him to persuade his colleagues, whom he has spent the past year implying are motivated by political partisanship, to go along (absent a sharp rise in unemployment).

One approach the White House may take is to generate more FOMC turnover to install preferred governors and presidents. Every Fed Governor, three of whom were appointed by President Biden, has voted for all three rate cuts in 2025. But President Trump has already moved to fire Governor Lisa Cook, whose case will be heard at the Supreme Court early next year. The President also implied this week that President Biden’s Fed appointments may have been invalid.

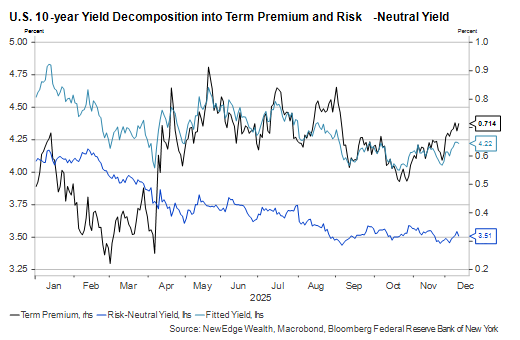

We return to the earlier discussion of stubbornly high long-term rates to posit another theory. With so much uncertainty at the Fed and the potential for more politicization, investors may be reluctant to buy longer maturity securities. As this chart shows, the entire rise in the 10-year U.S. Treasury yield since its mid-October low has come from a higher term premium, not an increase in the average expected short-term rate over the next decade. The term rises at times when investors are becoming less willing to lend money to the government for long periods of time.

Conclusion

I observe the facts without biases of the head or heart. I determine the arc’s path, stroll leisurely to its terminus and the truth falls at my feet.

The Fed has given markets as clear a signal as it can about monetary policy in 2026. Rates are not likely to fall much further absent a material labor market degradation. It should be easy for investors to interpret the next few months of data (starting with next week’s combined October-November payrolls report) through that reaction function. In short, it will take more bad news to get the Fed to cut in January…but not much more.

At the same time, we question how helpful the rate cuts have been or will be, given the failure of easier monetary policy to translate into more manageable household borrowing costs. Indeed, the cuts’ most significant effect thus far has been to reassure equity and credit markets that all is well and will remain so. By historical standards, that’s a relatively narrow channel through which monetary policy has to work. But it may suffice for the time being.

IMPORTANT DISCLOSURES

The views and opinions included in these materials belong to their author and do not necessarily reflect the views and opinions of NewEdge Capital Group, LLC.

This information is general in nature and has been prepared solely for informational and educational purposes and does not constitute an offer or a recommendation to buy or sell any particular security or to adopt any specific investment strategy.

NewEdge and its affiliates do not render advice on legal, tax and/or tax accounting matters. You should consult your personal tax and/or legal advisor to learn about any potential tax or other implications that may result from acting on a particular recommendation.

The trademarks and service marks contained herein are the property of their respective owners. Unless otherwise specifically indicated, all information with respect to any third party not affiliated with NewEdge has been provided by, and is the sole responsibility of, such third party and has not been independently verified by NewEdge, its affiliates or any other independent third party. No representation is given with respect to its accuracy or completeness, and such information and opinions may change without notice.

Investing involves risk, including possible loss of principal. Past performance is no guarantee of future results.

Any forward-looking statements or forecasts are based on assumptions and actual results are expected to vary from any such statements or forecasts. No assurance can be given that investment objectives or target returns will be achieved. Future returns may be higher or lower than the estimates presented herein.

An investment cannot be made directly in an index. Indices are unmanaged and have no fees or expenses. You can obtain information about many indices online at a variety of sources including: https://www.sec.gov/answers/indices.htm.

All data is subject to change without notice.

© 2025 NewEdge Capital Group, LLC