Introduction: Know Your Enemy

“Think ya know what it’s all about? Huh! Hey yo, so check this out!”

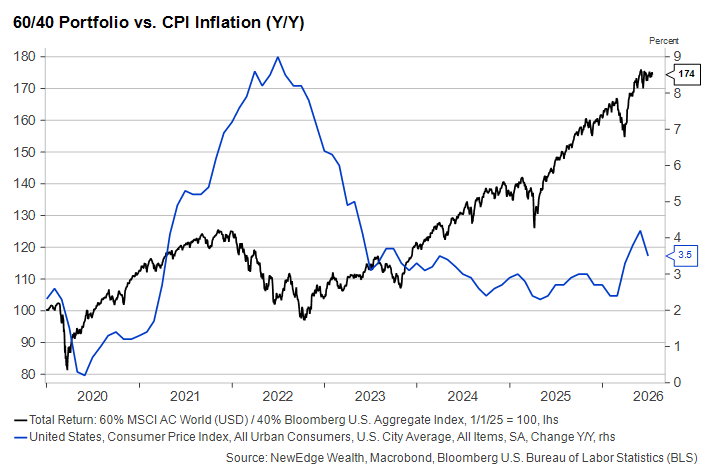

Last week’s whirlwind of Fed commentary and inflation data created a few market gyrations but ultimately left interest rates lower and the need for rate hikes less urgent. Evidence that inflation may finally be back on the decline is welcome news for investors, even as it arrives with a reminder that the newly opaque Federal Reserve may limit the extent to which we can enjoy it.

We think the current economic backdrop continues to support a Fed on “hold”, neither hiking nor cutting rates, which we argue is the best outcome for risk assets in the near term. The Fed will only be compelled to hike rates if inflation becomes a more powerful “enemy” and the economy is running uncomfortably hot. If the Fed is cutting rates anytime soon, it will be because the “enemy” is weak growth and a softening labor market.

It’s important for investors to “know their enemy” when thinking about the forward rate path and find ways to diversify around the various risks it presents. Rage Against the Machine’s 1992 release, “Know Your Enemy”, lyrically and tonally encapsulates how both hot inflation and weaker unemployment could wreak havoc on markets, but in different ways. (And yes, we appreciate the inherent irony of using Rage Against the Machine song to inspire a written commentary for clients of a financial services firm.)

As of 7/17/26

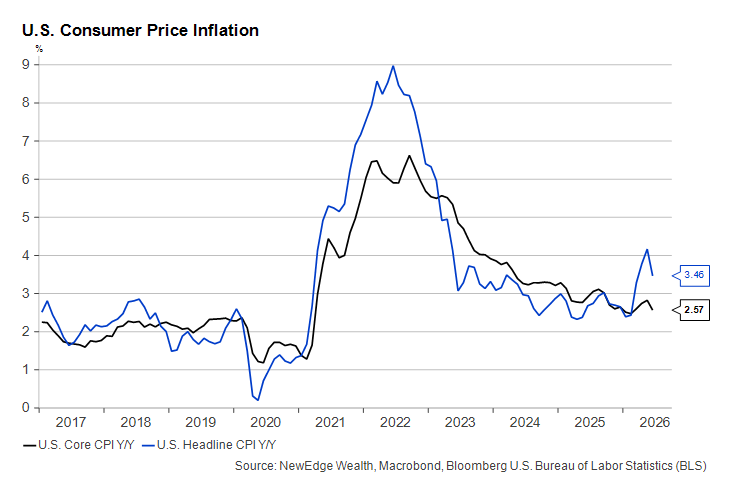

But we learned this week that what inflation takes away from investors it can eventually give back by moderating and allowing rates to fall and equity multiples to expand. Both Consumer and Producer Price Inflation for June came in significantly softer than expected, permitting investors to breathe at least a temporary sigh of relief. If (and this is a big “if” given geopolitical events this week) energy prices remain comfortably below their peaks from earlier in the U.S.-Iran conflict, inflation could continue to moderate in the coming months.

As of 7/17/26

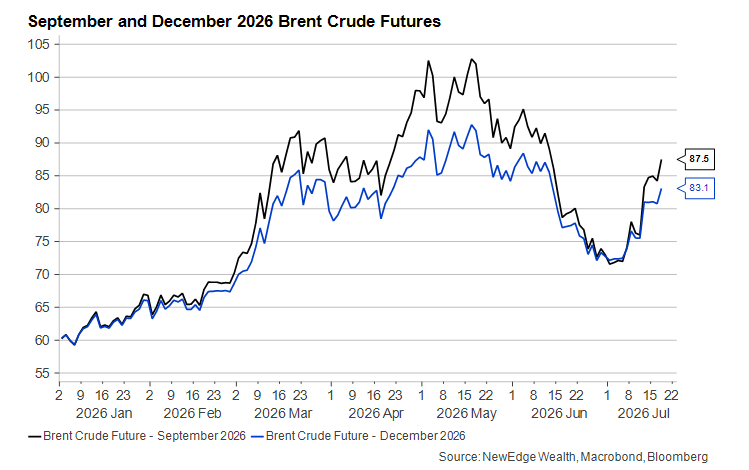

Traditionally, the three major sources of inflation are energy prices, housing and the labor market. Right now, neither housing nor the labor market look like major risks. Energy remains a major wild card. As commodity traders become more sensitive to the risks of a prolonged conflict in the Middle East, futures markets may begin to reflect a higher-for-longer environment for oil prices. Should the conflict deescalate once more, however, energy should continue to exert a downward pull on annual inflation:

As of 7/17/26

Hoping We Have Passed “Peak Fed Hawkishness”

“Something must be done”

Markets, of course, continue to view inflation risks through the prism of interest rates. Upside inflation surprises tend to push rates higher as investors a) demand a higher yield for fixed coupon payments; and b) anticipate tighter policy via higher interest rates from the Federal Reserve.

A central bank’s reaction function matters a great deal for how markets respond to inflation news. History is rife with examples of central banks (primarily but not exclusively in emerging markets) that either ignore or miscalculate the risks of higher inflation and see their currencies and sovereign bonds sell off sharply. Stocks’ reaction has been more case-dependent. On the one hand, higher inflation can help profit margins. On the other hand, too much inflation can lead to financial instability and economic collapse, neither of which is good for business.

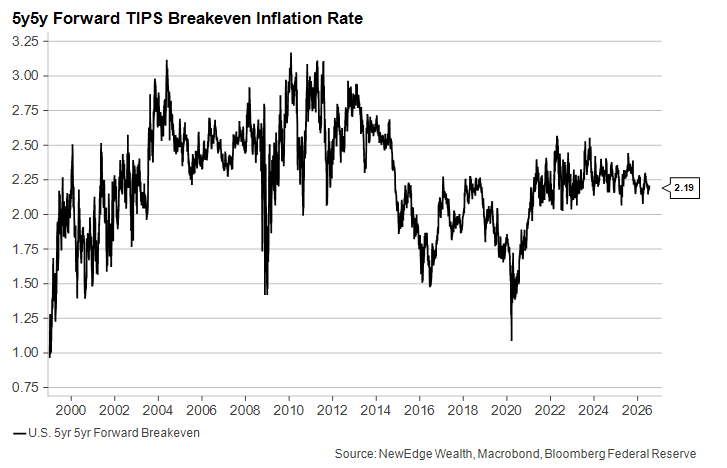

More credible central banks, which have nearly always included the Federal Reserve, tend to get the benefit of the doubt from investors on handling inflation risks. Communicating and executing policy calmly and competently can help keep investors’ inflation expectations low, and those low expectations can helpfully become their own self-fulfilling prophecy. One look at the 5-year 5-year forward breakeven rate of inflation – essentially the inflation risk premium priced into the Treasury market – tells you that at no time in the past five years have expectations become “unanchored” from the Fed’s two percent target despite the fact that target has never been reached:

As of 7/17/2026

Enter Kevin Warsh, the new Fed Chair who has vowed to bring inflation back down to target to help preserve his institution’s credibility. Warsh testified before Congress last week for the first time and chose to “drop the style clearly”, to borrow a RATM lyric. His comments revealed little about his plans for monetary policy or even his framework for making decisions. Chair Warsh’s colleague on the Fed’s Board of Governors, Chris Waller, has been on the opposite side of the transparency spectrum lately. Waller gave a speech last Monday in which he strongly hinted at a willingness to vote for a rate hike at the July 29th meeting if inflation data, specifically core inflation, worsened. His comments sent the odds of a July hike to as high as 45% intraday on Monday before this week’s inflation data came in cool and caused the July hike expectations to fall to less than 15% by the end of the week.

As of 7/17/2026

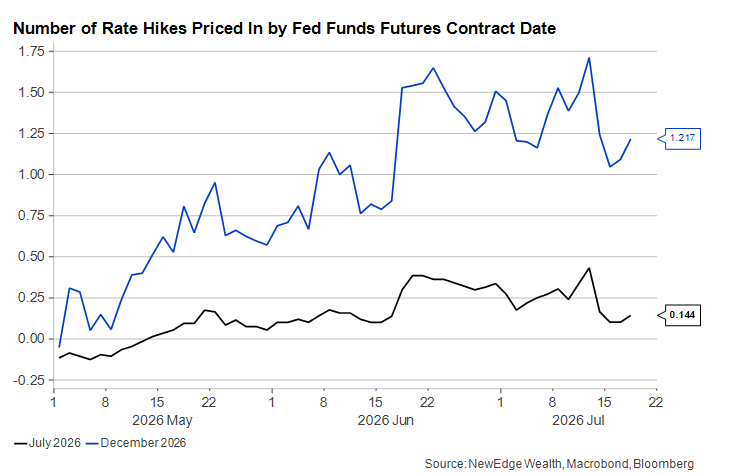

Barring a prolonged return to oil prices above $100/bbl (and gasoline prices above $4/gallon), inflation may remain quiet enough for the Fed to keep policy on hold for the remainder of the year. If “action must be taken” in either direction – both hikes and cuts were floated as possibilities in the June meeting minutes – it’s unlikely to be good news for equity markets. Hikes would mean high inflation and volatile bond markets, while cuts would only come amid a serious macroeconomic deterioration. The pricing out of hikes, which would show up as a drop in the blue line above, would be positive for just about every asset class.

Gold’s Strange Relationship With Inflation

“I was born to rage against ‘em”

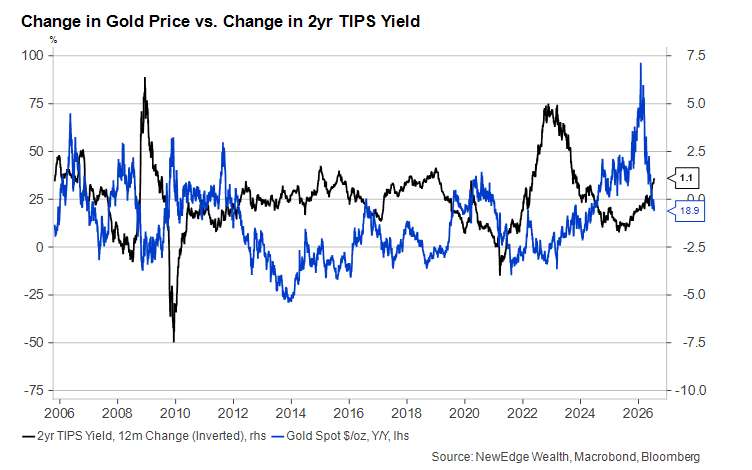

Before we wrap up, it’s worth spending a moment on gold. The yellow rock seemed tailor-made for a year like 2026 in which geopolitical uncertainty and inflation have both spiked unexpectedly. Yet gold has been the worst performing asset in most investors’ portfolios. Gold has seen a particularly sharp correction as real interest rates (yields on TIPS, or interest rates excluding inflation) have drifted higher:

As of 7/17/26

As the graph above shows, gold investors can take solace in the fact that their position is still up almost 19% over the last year. But gold’s price has fallen below $4000/oz after briefly spiking above $5400/oz in January.

You could argue that gold is suffering from a surplus of Fed credibility. Despite elevated inflation, the Fed has been able to keep inflation expectations low, as we showed above, while real interest rates have risen. There is simply less of a need to hedge against inflation risks using gold than there might have been with a wobblier, less credible central bank. The Fed’s greatest asset – its credibility – is gold’s worst enemy.

“Still in a Room Without a View” Until the Fed Raises the Curtain

No one likes a week of soft inflation data better than us, but if we are permitted one nitpick, it’s that markets are still wary of a surprise hike from the Fed this summer. The July FOMC meeting is less than two weeks away. There isn’t any more inflation data coming before then. And yet there is still a nontrivial chance of a quarter-point hike priced into futures markets. We think the remaining odds of a hike derive from markets simply not knowing what the Chair is thinking or what he’ll do.

This lack of transparency has contributed to markets’ diminished understanding of the Fed’s reaction function to incoming data. Indeed, this may be a feature, not a bug, of the Warsh administration. But it will take some time for investors (not to mention investment strategists!) to adjust to this new reality.

Inflation surprises still represent a serious risk to asset prices, but this week provided a view into disinflation’s ability to lift both the floor and the ceiling for portfolio values over the remainder of the year. That outcome is still possible if geopolitical risks stay at a simmer and the Fed charts a steady course.

Lastly, we would be remiss if we did not note the lack of rally in equity markets this week despite cooler inflation and falling expectations for rate hikes. Equity market weakness has, instead, come from a sharp unwind in the dominant (and large-weighted) AI infrastructure trade. Stocks of AI infrastructure producers have been negatively correlated to inflation risks this year, performing best in April and May as prices and rates weighed on the rest of the market, yet struggling in June and July as inflation risks have abated somewhat.

IMPORTANT DISCLOSURES

The views and opinions included in these materials belong to their author and do not necessarily reflect the views and opinions of NewEdge Capital Group, LLC.

This information is general in nature and has been prepared solely for informational and educational purposes and does not constitute an offer or a recommendation to buy or sell any particular security or to adopt any specific investment strategy.

NewEdge and its affiliates do not render advice on legal, tax and/or tax accounting matters. You should consult your personal tax and/or legal advisor to learn about any potential tax or other implications that may result from acting on a particular recommendation.

The trademarks and service marks contained herein are the property of their respective owners. Unless otherwise specifically indicated, all information with respect to any third party not affiliated with NewEdge has been provided by, and is the sole responsibility of, such third party and has not been independently verified by NewEdge, its affiliates or any other independent third party. No representation is given with respect to its accuracy or completeness, and such information and opinions may change without notice.

Investing involves risk, including possible loss of principal. Past performance is no guarantee of future results.

Any forward-looking statements or forecasts are based on assumptions and actual results are expected to vary from any such statements or forecasts. No assurance can be given that investment objectives or target returns will be achieved. Future returns may be higher or lower than the estimates presented herein.

An investment cannot be made directly in an index. Indices are unmanaged and have no fees or expenses. You can obtain information about many indices online at a variety of sources including: https://www.sec.gov/answers/indices.htm.

All data is subject to change without notice.

© 2026 NewEdge Capital Group, LLC