This week, we are revisiting the small and mid-cap U.S. equity segment, dissecting recent performance trends and analyzing what are, once again, lofty expectations for profit growth in the coming calendar year. This cohort, which is generally comprised of the 2,500 U.S. companies with market capitalizations from $100M – $20B, is in our view one of the more complex market segments today, and, in some ways, is “livin’ on a prayer” as Bon Jovi would say, given those lofty expectations and recent performance trends that have favored more speculative areas. However, there remains an opportunity where the right combination of economic growth, policy support, underlying margin expansion, and renewed investor appetite helps make these prayers a reality.

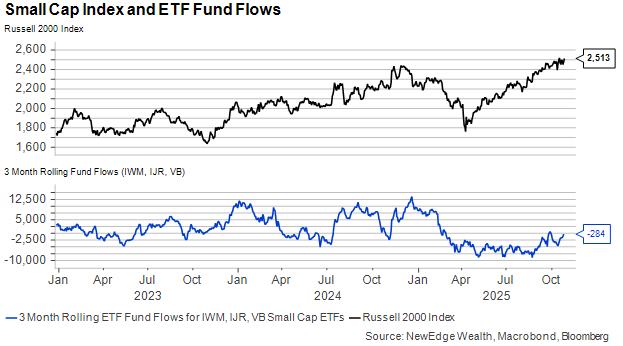

The environment for small and mid-cap equities is certainly complex today, mainly due to the wide range of cross currents that continue to impact this segment, ranging from evolving monetary and fiscal policy, to muddy but possibly improving economic data (evidenced by Friday’s CPI report). The group’s lofty earnings expectations continue to see negative earnings revisions, making the recent rally driven primarily by valuation expansion. Notably, despite recent outsized performance from more speculative areas of the group, like non-profitable tech, smaller cap size ETFs continue to experience persistent outflows and light positioning, conditions that have lead to powerful short-term reversions in these indices in the past. While we don’t know when this complexity will ease, in our view it does create an environment that provides ripe opportunities for stock selection and should ultimately reward more disciplined and fundamental investors.

Key Takeaways

• For several years now market participants have been suggesting that the coming year will be the time small caps finally outperform their large cap peers (an outcome last seen in 2020). We see this in the lofty earnings expectations, calls for a mean reversion in earnings growth, valuations, and performance, and perennial optimism that future policy and economic activity will be more supportive for these smaller companies.

• In our view, for small caps to generate more sustained outperformance they will need to deliver on earnings expectations, something we have not seen for several years. Instead, earnings estimates have been continually cut for smaller companies, which is partly why larger companies have continued to outperform as larger companies tend to benefit from greater economies of scale, more diversified revenue streams, and wider moats.

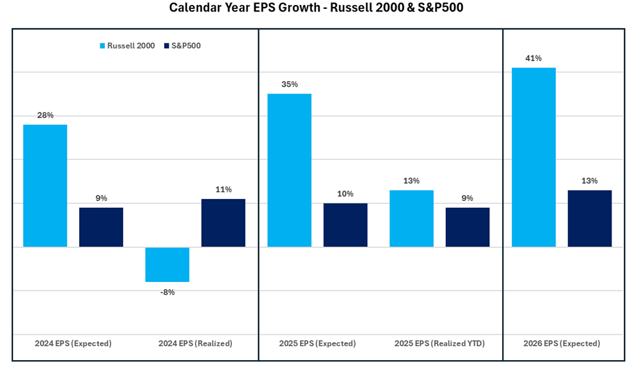

• Smaller cap earnings expectations for 2026 are once again remarkably high, with base case expectations of 41% YoY EPS growth in the Russell 2000 Index (a rate of growth only seen once in the last 15 years). These expectations are fueled primarily by margin expansion as opposed to revenue growth, making operational efficiency for these companies (through lower input costs, pricing power, and lower interest costs) critical in the coming year.

• Ultimately, we think these expectations will be difficult to achieve given the current economic environment, but instead of suggesting investors steer clear of the small and mid-cap segment, we believe there remains a compelling opportunity for fundamental active managers in this space to identify underappreciated companies that can deliver on these lofty expectations. We would argue that the opportunity set for finding attractively priced stocks within the smaller cap universe is likely greater than in large cap names.

In the near term, we could see a continued “positioning chase” within smaller caps, as investor outflows from the group, as measured by ETF flows, still are negative despite the large rally since the April lows. This suggests that the “pain trade” (a movement in an index or stock that is counter to what is expected) is likely still higher for the smaller cap index, even with its weaker fundamentals.

Livin’ on a Prayer: Recent Performance Trends

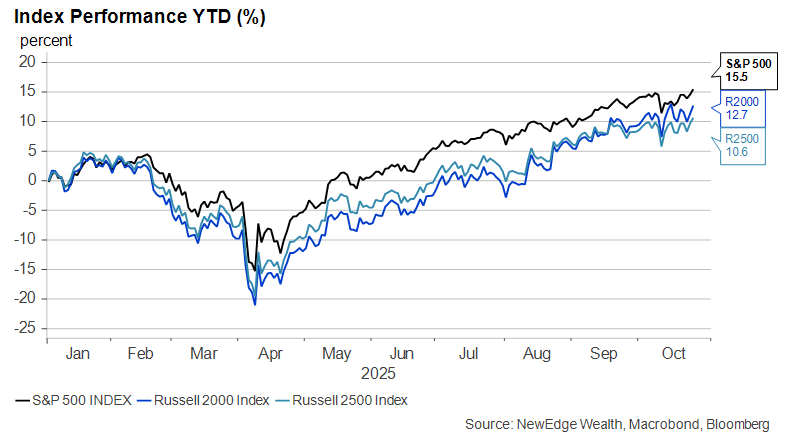

The most recent quarter saw the small and mid-cap segment post surprisingly strong results, with the Russell 2500 Index returning 9% and outperforming the large cap S&P500 for the first time since Q3 of last year. Small caps in particular delivered healthy 12% total returns, with the Russell 2000 Index notching its best quarter since 2023.

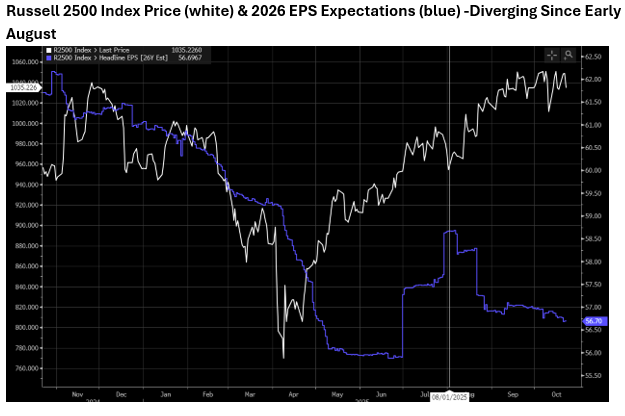

While this turn in sentiment and performance is encouraging, it was primarily driven by multiple expansion, as earnings expectations for 2026 actually declined by mid-single digits during the quarter. Under the surface we also saw more speculative areas within the small and mid-cap universe outperform, with interest rate sensitive and less profitable industry groups like biotechnology, homebuilders, and aerospace & defense, all return more than 20%.

It isn’t surprising to see prices deviate from fundamentals in the near-term, especially in a segment of the market with lower analyst coverage, and given the move towards more accommodative policy outlined by the Fed in September. However, for more sustainable outperformance, we believe the small and mid-cap segment will have to see those positive analyst revisions and rising future EPS expectations that have been such a key driver for the large cap segment.

Shot Through the Heart: The (once again) Lofty Earnings Expectations

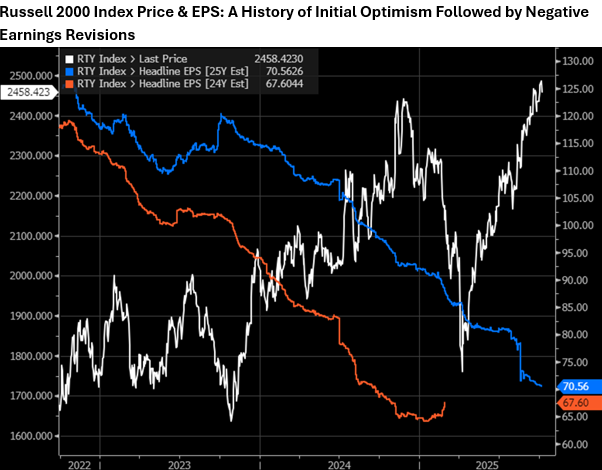

One reason why many have been calling for small caps to finally outperform large caps in the coming year is the expected earnings growth for this segment. The Russell 2000, for example, is expected to post 41% YoY EPS growth in 2026, 3x the 13% EPS growth expected for the S&P500. While the S&P500 has consistently exceeded EPS growth expectations, the small cap segment has a recent history of failing to deliver. Not only is about 40% of this universe consistently not profitable, but as we have seen for the past two years, expectations tend to be overly optimistic for this group.

Entering 2025, the Russell 2000 Index was expected to post roughly 35% EPS growth, yet over the course of this year those expectations have consistently been revised lower and as of mid-October we are on pace for just 13% EPS growth (using expected EPS for Q3 and Q4 which may also be optimistic assumptions). Ultimately the small cap segment has not earned the benefit of the doubt the way the large cap segment has recently, which is why we continue to take these forward estimates with a grain of salt.

This year the Russell 2000 is expected to post 1% YoY revenue growth, surprisingly modest when compared to the mid-single digit nominal GDP growth in the U.S. economy, although this is probably a fair reflection of the state of U.S. economic activity when you exclude things like AI Capex. In 2026 this revenue growth is expected to increase to 5% YoY, an encouraging acceleration, but this also suggests that substantial margin expansion and a return to profitability will be critical for many small cap companies in the coming year to achieve the lofty EPS growth expectations.

Profitability is often elusive in the small cap segment, given these companies lack the economies of scale of their larger cap peers, they tend to have less revenue diversification, have higher labor costs as a percentage of revenue, and they also are typically more capital intensive, with high fixed costs and debt service costs that can weigh on profitability in a higher rate and slower growth environment.

This year the small cap segment has shown some incremental profitability with average operating margins in Russell 2000 increasing by 60bps, rising from 4.7% to an expected 5.3% by year end.

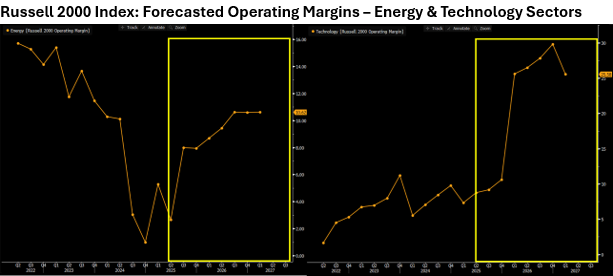

Next year, however, consensus expectations are for these operating margins to nearly double, rising by 350bps and averaging 8.8%. This would be a remarkable level of profitability for the small cap segment: it’s a level only seen briefly over the past few decades, and it has typically coincided with periods of ample liquidity and robust economic growth, a combination that feels somewhat out of reach given current economic trends. The biggest contributors to this operating margin expansion are the energy and technology sectors, traditionally more economically sensitive groups that benefit from inherent operating leverage when growth is accelerating, prices are rising, and debt service costs are falling. As we illustrate in the charts below, these segments are forecasted to post a remarkable recovery in profitability, underscoring the importance of a healthy combination of GDP growth and accommodative policy if these estimates are to be realized.

Never Say Goodbye: Our Overall View on Small & Mid Cap Equities

While we are skeptical that small and mid-cap equities can deliver on the lofty earnings expectations for 2026, given the economic conditions and headwinds to margin expansion we have outlined, surprisingly, we are not suggesting investors avoid this segment of the market. On the contrary, we believe this segment today deserves a closer look from investors, with the caveat that we would prioritize active management and focus on the highest quality cohort of companies that are generally more capital efficient, have unique competitive advantages, and ultimately offer more resilient profitability. In addition, this is a segment that has seen a remarkable level of outflows over the past several years and continues to face persistently weak sentiment. With that set up in mind, it might not take much in the way of earnings surprises to draw some renewed attention to the space and ultimately reward those long-term investors focusing on the fundamentally driven companies in this segment.

IMPORTANT DISCLOSURES

The views and opinions included in these materials belong to their author and do not necessarily reflect the views and opinions of NewEdge Capital Group, LLC.

This information is general in nature and has been prepared solely for informational and educational purposes and does not constitute an offer or a recommendation to buy or sell any particular security or to adopt any specific investment strategy.

NewEdge and its affiliates do not render advice on legal, tax and/or tax accounting matters. You should consult your personal tax and/or legal advisor to learn about any potential tax or other implications that may result from acting on a particular recommendation.

The trademarks and service marks contained herein are the property of their respective owners. Unless otherwise specifically indicated, all information with respect to any third party not affiliated with NewEdge has been provided by, and is the sole responsibility of, such third party and has not been independently verified by NewEdge, its affiliates or any other independent third party. No representation is given with respect to its accuracy or completeness, and such information and opinions may change without notice.

Investing involves risk, including possible loss of principal. Past performance is no guarantee of future results.

Any forward-looking statements or forecasts are based on assumptions and actual results are expected to vary from any such statements or forecasts. No assurance can be given that investment objectives or target returns will be achieved. Future returns may be higher or lower than the estimates presented herein.

An investment cannot be made directly in an index. Indices are unmanaged and have no fees or expenses. You can obtain information about many indices online at a variety of sources including: https://www.sec.gov/answers/indices.htm.

All data is subject to change without notice.

© 2026 NewEdge Capital Group, LLC