“It sure ain’t no surprise.” The U.S. election is upon us.

As investment strategists, we worry primarily about the macroeconomic environment and its influence on the major drivers of asset prices, like interest rates and corporate earnings. Today, however, we will briefly veer into politics as the approaching U.S. election and balance of power in Washington, D.C., dominate the headlines…even on the financial news networks.

In this piece, we’ll assess the state of the race, discuss the U.S. federal debt and deficit in the context of different political power-sharing arrangements, and evaluate the candidates’ economic platforms. The most significant policy development of the next president’s term, whoever it is, will likely be the evolution of the tax code, which will impact earners of all income levels as well as corporations.

“Tell me what you think about your situation.” The election is gonna be close.

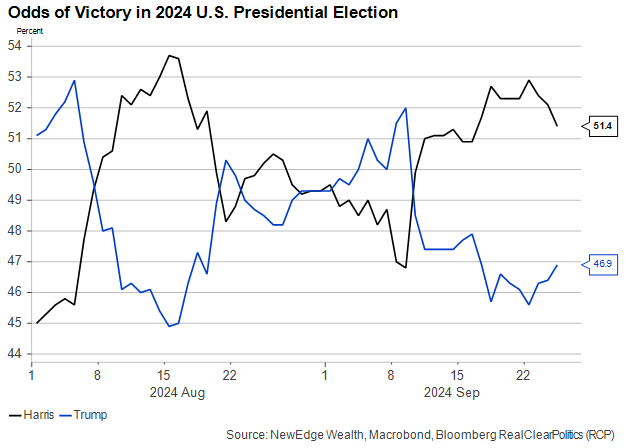

Betting markets, polling averages, and our lived experience over the past several decades all tell us the same thing. The U.S. electorate is evenly divided, and the November elections for the White House and Congress are going to be close. We do not necessarily expect firm results on Election Night or for several days after, with so many states polling within the margin of error.

Betting odds calculated by RealClearPolitics show the presidential race between former President Donald Trump and Vice President Kamala Harris as a toss-up, meaning we should expect some market reaction once the outcome is known and fully priced in.

Of course, the president does not have full control over public policy, which makes the Senate and House of Representatives races important for policy expectations. Currently, the House is controlled by Republicans, while the Senate is held by Democrats. Margins in both chambers are historically narrow.

Senate control is broadly expected to switch to the Republicans, who are seen as likely to flip seats in West Virginia, Montana, and Ohio, all of which voted solidly Republican in 2016 and 2020.

Democrats, on the other hand, must defend incumbents in the swing states of Pennsylvania, Nevada, and Wisconsin, and they have vulnerable open seats in Arizona, Michigan, and Maryland. Their hope of flipping any Republican seats rests on slim hopes of upsets in Texas, Nebraska, or Florida.

A President Harris would likely have to deal with a partially or fully oppositional Congress, while President Trump, should he win, is likely to have Republican majorities in both houses. This makes it highly unlikely that progressive initiatives such as Supreme Court reform or taxation of unrealized capital gains will pass in the next four years, even if Harris should emerge victorious.

With the Senate likely to be close to evenly split, any legislation with a hope of passing will need to be related to taxes or spending, which can be enacted with a 51-vote majority thanks to Budget Reconciliation rules, rather than the usual 60-vote threshold. It just so happens that a major expiring tax provision will force such action in 2025.

“If Chicken Little tells you that the sky is falling.” Tax Hikes in 2026? Or Bigger Deficits?

Taxes will be the major policy focus of the next four years. The individual tax provisions in the 2017 tax bill (the Tax Cuts and Jobs Act, or TCJA) will expire on January 1, 2026. If this bill is allowed to expire, it would represent a significant tax increase on everyone who currently pays income taxes (and even some who do not). This seems like a calamity that even an acrimonious, divided government should be able to avoid.

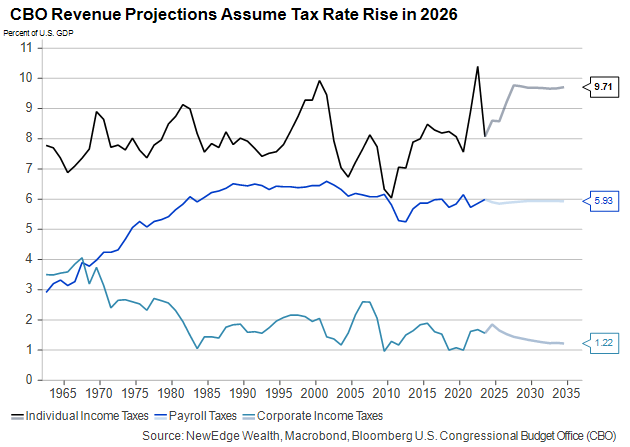

As startling as the prospect of a jump higher in taxes is for individuals and businesses, these tax dynamics also have major implications for the federal budget. The Congressional Budget Office’s long-term budget projections assume the sunsetting TCJA provisions will expire without renewal, which explains why they show a jump in income tax revenues beginning in 2026. Because at least some of these provisions are likely to be extended, the CBO’s deficit projections look too optimistic.

Importantly, the TJCA’s corporate tax cut provisions do not sunset in 2026, and the revenue that corporate taxes generate is set to continue falling relative to the size of the economy. Meanwhile, demographics’ downward pull on the size of the labor force, as the American population ages, is capping the growth in payroll tax revenue.

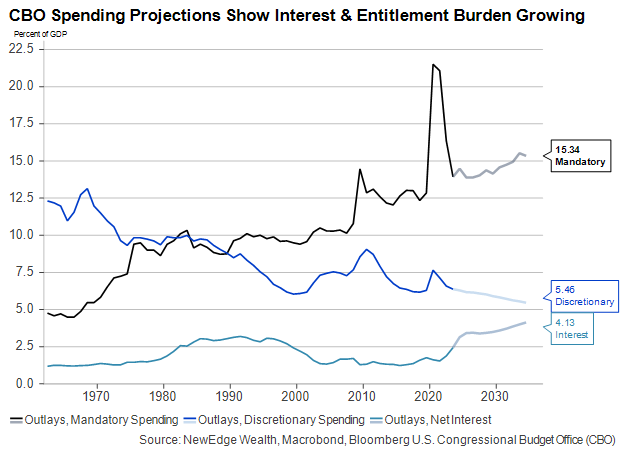

Demographics are also responsible for most of the expected growth in federal spending in the next decade. Social Security, Medicare, and other off-budget programs will be responsible for the lion’s share of new spending in the next decade. Discretionary spending, which includes military spending, is a smaller percentage of GDP than it’s been in decades and is set to shrink further.

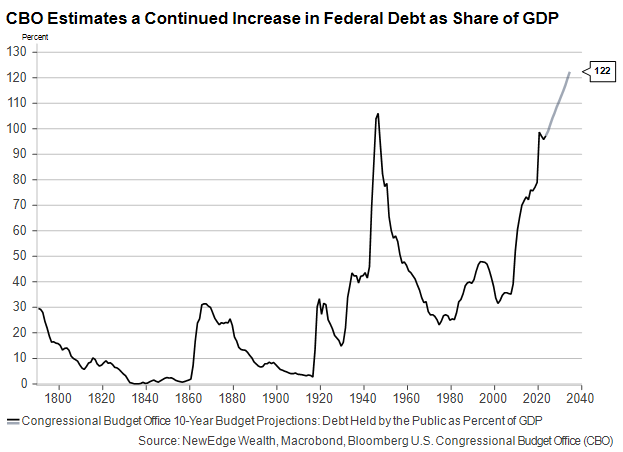

The combination of uncontrolled spending growth and lower tax revenues unavoidably creates larger budget deficits, even if U.S. growth remains resilient. The CBO expects the U.S. debt to grow to its largest share ever of the overall economy by the end of this decade.

This is the dilemma politicians face as they promise new tax cuts and more spending without touching entitlement programs. That construct does not permit a serious attempt at deficit reduction regardless of the election’s outcome.

High debt levels and unsustainable deficit growth could eventually lead holdings of U.S. Treasuries to demand higher interest rates. For now, though, the bond market remains focused on Fed policy and the slowing economic environment rather than long-term fiscal challenges. Investors have been willing to finance the new Treasury supply at lower interest rates. Even so, average rates on the U.S. debt are unlikely to return to their lows from 2020 or 2021.

“Complication, aggravation is getting to you.” Divided government and deficits.

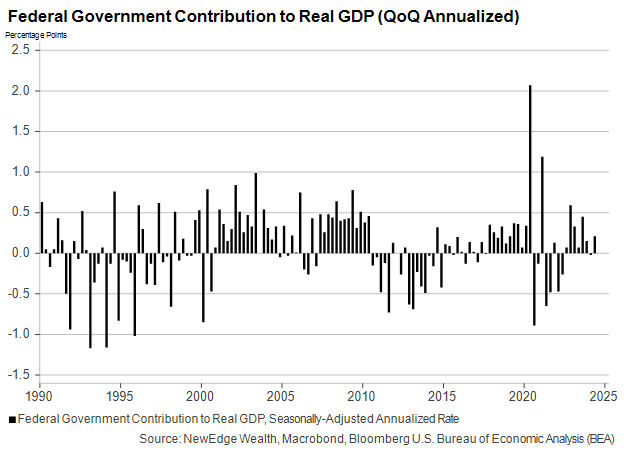

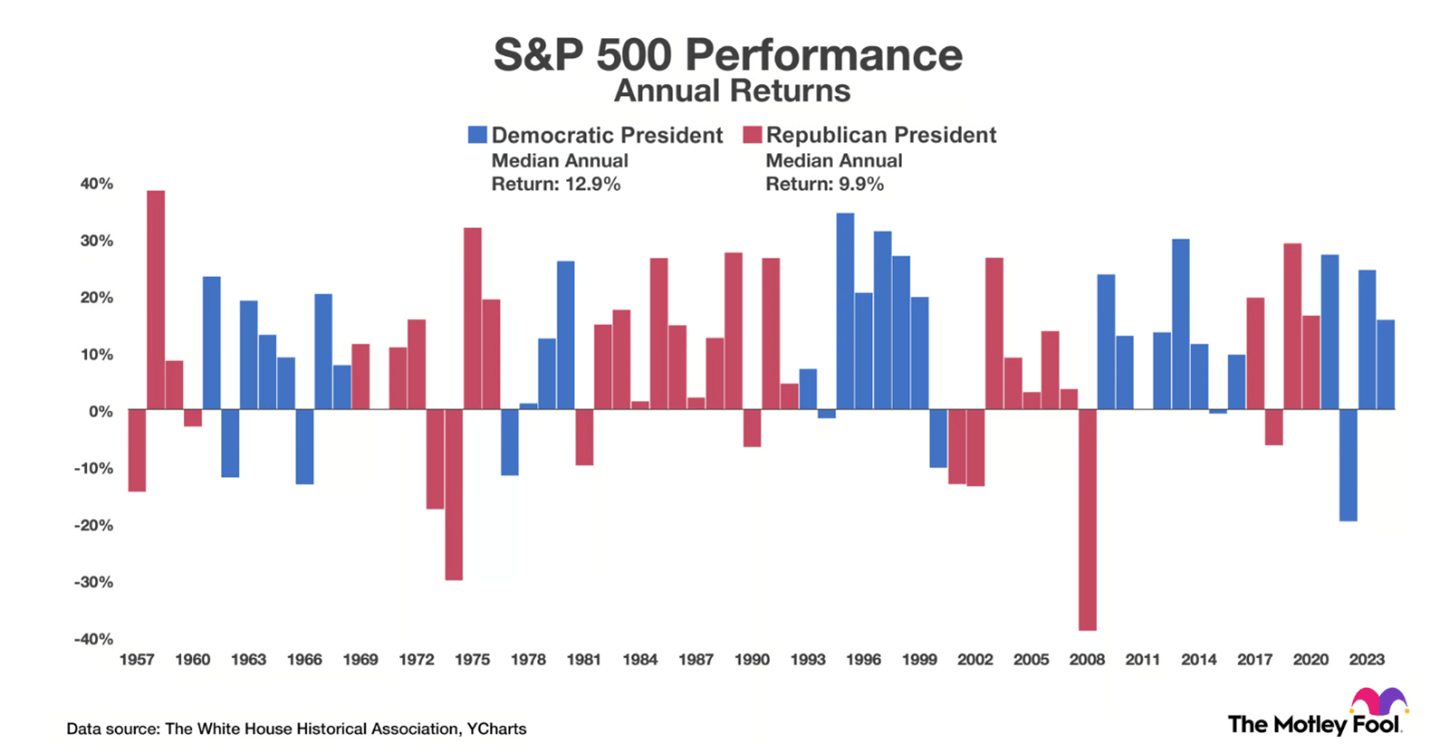

The past several decades have featured increased partisan rancor and gridlock, producing few market-moving public policies outside of changes to the tax code. Historically, divided governments have produced smaller deficits under Democratic presidents and larger deficits under Republican ones. When there is unified control, deficits usually grow regardless of which party is in charge.

The chart below shows the Federal government’s quarterly contribution to U.S. GDP growth, a good proxy for whether deficits are growing or shrinking. The most notable periods of deficit reduction outside of post-recession periods were the second Clinton term (1997-2001) and the second Obama term (2013-2017), during which Republicans controlled at least one house of Congress.

Deficits grew in George W. Bush’s second term (2005-2009) and Donald Trump’s administration (2017-2021). Both periods were punctuated by debt-busting economic emergencies, but deficits were already rising prior to those crises thanks to spending increases and tax cuts.

We’ll now examine the two major presidential candidates’ policy proposals in more detail and discuss their potential impact.

“Would you still come crawling back again?” Inflationary Policies in a Second Trump Term.

President Trump’s economic platform is comprised of tax cuts, tariffs, and immigration restrictions. If enacted in tandem, these have the potential to produce higher inflation, especially if accompanied by greater executive influence on monetary policy decisions. Let’s consider the provisions one at a time.

President Trump’s main policy accomplishment was the Tax Cuts and Jobs Act passed in 2017. Job one for a second Trump term, flanked by allies in Congress, will be to renew the expiring income tax provisions and, potentially, cut the corporate tax rate further.

Building on these tax efforts, Trump has proposed additional tax carveouts on the campaign trail. These include tax exemptions for tips, overtime work, social security payments, and state and local income taxes. All in, these would drive U.S. budget deficits to their largest in history, excluding World War II and COVID.

Budget deficits alone cannot create higher inflation. The economy ran only modestly hotter in 2018 and 2019 following the passage of the TCJA, and that was partially a result of reduced immigration flows and low interest rates. Trump’s 2024 platform includes more immigration restriction as well as higher and broader tariffs, so both policies are worth examining in more detail.

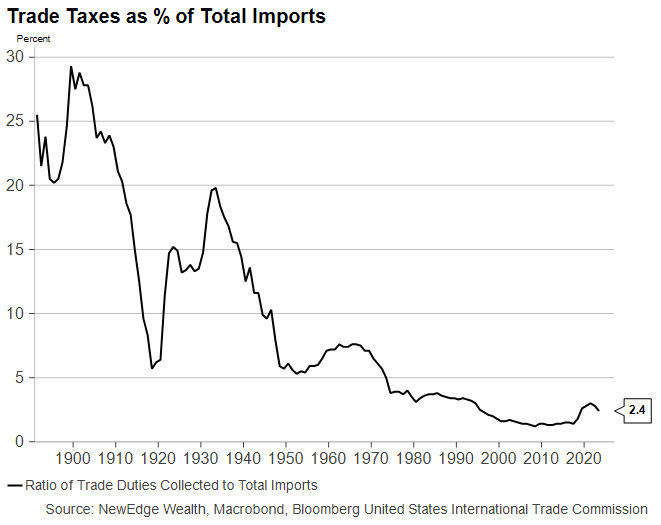

First, on trade, President Trump reversed a decades-long trend of freer trade and lower taxes on imports. But his trade taxes, or tariffs, were modest compared to the first half of the 20th century:

Trump is now pledging to raise tariffs far higher on a much broader array of goods. That he would not need Congressional signoff to do so makes his trade policy promises highly credible.

A 10% tariff on all imported goods and a 60% levy on imports from China would significantly raise the cost of living for most Americans. While this type of “inflation” might not be met with higher interest rates from the Fed, it would have a negative impact on consumer purchasing power. In fact, the potential for tariffs to harm demand was a key rationale that the Fed used for its interest rate cuts in 2019.

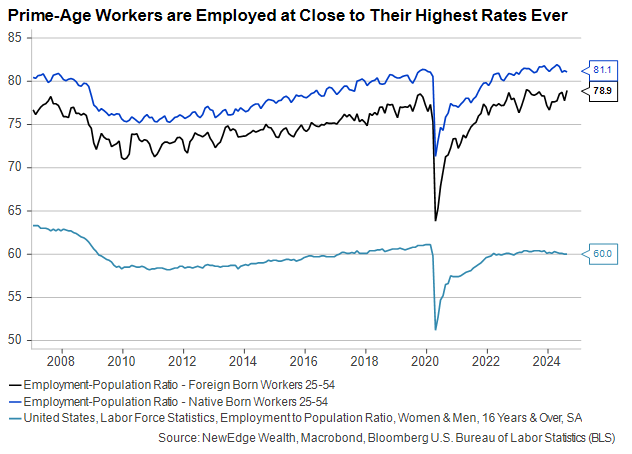

Speaking of inflation, one of the major contributors to the rapid disinflation of 2023-24 has been the increased labor supply, which has relieved some upward pressure on wages as workers became less scarce. With the native-born U.S. labor force shrinking thanks to increased retirements, a surge of immigrant workers and a further rise in employment among prime-age native-born workers have picked up the slack.

It’s unlikely we’ll see a meaningful further increase in employment rates among prime-age workers. In the near term, this means any further labor force expansion must to come from immigration. Policies that restrict immigration won’t have a large negative impact if the jobs market slows, but with unemployment at just 4.2%, “slack” remains largely absent from the economic conversation.

Inflation will be mainly driven by monetary policy, as it always is. But larger fiscal deficits provide economic stimulus, which the Fed would have to factor into any decisions about how quickly and to what level to adjust interest rates.

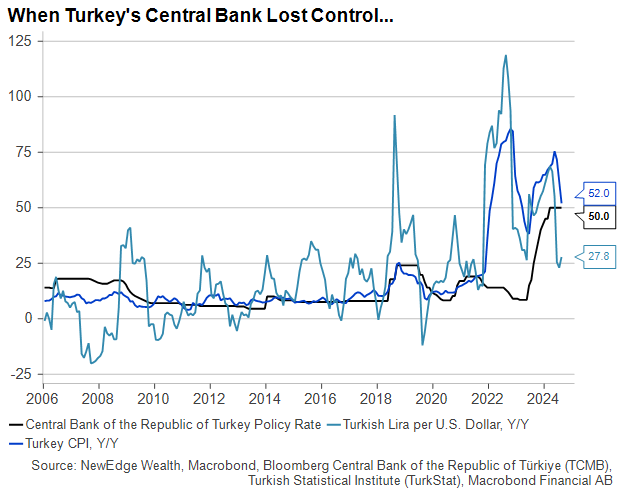

On that topic, Trump has expressed interest on the campaign trail in having more of a say in monetary policy decisions, ostensibly to influence the Fed to keep rates low when they might normally want to hike. This affords us an opportunity to examine a recent real-world case study in which the political capture of the Central Bank of Turkey has resulted in the collapse of its currency and an enduring inflationary spike. Inflation and short-term interest rates in Turkey are both still around 50%.

History is replete with these sorts of lessons. While Congress is unlikely to pass sweeping changes to the Fed’s independent mandate and structure, presidents have the power to name governors to the Federal Reserve Board. The next president will likely be naming current Chair Jerome Powell’s successor by the end of 2025, a hugely consequential appointment.

“We can tell ’em no, or we could let it go.” Harris victory and policies.

Vice President Harris’ campaign has been notoriously light on concrete policy details, but the proposals that have been spelled out include making the tax code more progressive and strengthening targeted tax incentives that help those with children and those who want to start small businesses or buy a home.

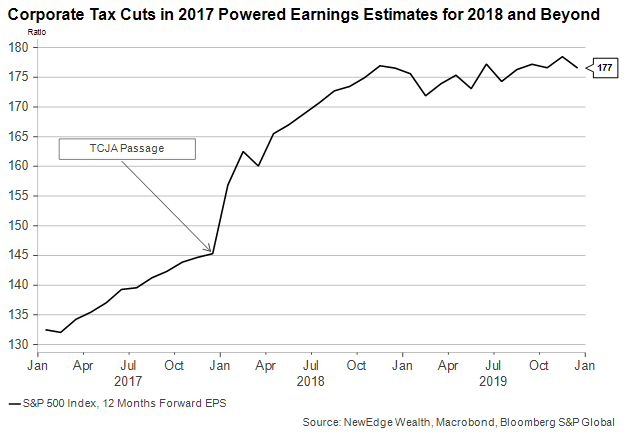

These provisions could make it into law even through a Republican-led Congress as part of a deal that also includes a broad extension of individual income tax rates and no change to corporate tax rates. Harris has proposed increasing taxes on higher earners and corporations as a way to help pay for tax breaks for lower earners, but it’s not clear that a Republican Congress would approve any new tax revenue. This graph of S&P 500 earnings estimates in 2017 and 2018 shows just how impactful the TCJA was on profit expectations:

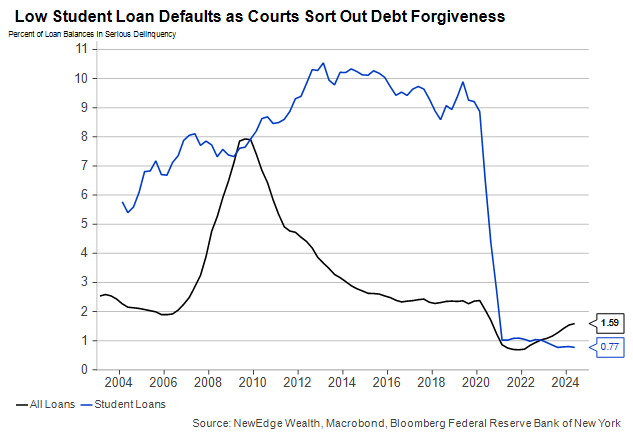

Student debt forgiveness is still being litigated in the courts, and its fate could be consequential for the consumer outlook. Outright cancellation of student debt would be a small economic stimulus, widening the federal deficit and likely forestalling a larger increase in consumer defaults.

Should debt forgiveness be struck down and loan repayment practices return to their pre-COVID norm, the impact on consumers could be significant.

A Harris administration facing an oppositional Congress would be challenged to produce the types of sweeping reforms that could move financial markets. However, her tax policies, if enacted as proposed, would have major implications for taxes on both earned income and investments. Our colleague in NewEdge’s Wealth Strategy Group, Lauren Detering Friday, has produced a comprehensive 2024 Presidential Tax Policy Showdown, a guide to the election and its tax implications that all investors should read.

“We’re seein’ things in a different way.”

Many investors are looking for angles to position for election results across a variety of markets like rates, oil, and even crypto. While some market volatility is to be expected following the passage of an event associated with so much uncertainty, the most lasting impact of this election might not be the market moves in its immediate wake but the longer-term changes to the tax code it eventually brings about.

Having a wealth strategy plan in place with advisors who understand changes to the tax code as they are being debated and passed can help preserve far more wealth than can be gained by being “right” on the coin toss that this presidential election outcome represents.

At the same time, while politics can be an emotional topic for investors of all ideological stripes, making large changes to an asset allocation in anticipation of an outcome is usually the wrong course of action. There is no historical correlation between investment returns and the presidential party in power.

IMPORTANT DISCLOSURES

The views and opinions included in these materials belong to their author and do not necessarily reflect the views and opinions of NewEdge Capital Group, LLC.

This information is general in nature and has been prepared solely for informational and educational purposes and does not constitute an offer or a recommendation to buy or sell any particular security or to adopt any specific investment strategy.

NewEdge and its affiliates do not render advice on legal, tax and/or tax accounting matters. You should consult your personal tax and/or legal advisor to learn about any potential tax or other implications that may result from acting on a particular recommendation.

The trademarks and service marks contained herein are the property of their respective owners. Unless otherwise specifically indicated, all information with respect to any third party not affiliated with NewEdge has been provided by, and is the sole responsibility of, such third party and has not been independently verified by NewEdge, its affiliates or any other independent third party. No representation is given with respect to its accuracy or completeness, and such information and opinions may change without notice.

Investing involves risk, including possible loss of principal. Past performance is no guarantee of future results.

Any forward-looking statements or forecasts are based on assumptions and actual results are expected to vary from any such statements or forecasts. No assurance can be given that investment objectives or target returns will be achieved. Future returns may be higher or lower than the estimates presented herein.

An investment cannot be made directly in an index. Indices are unmanaged and have no fees or expenses. You can obtain information about many indices online at a variety of sources including: https://www.sec.gov/answers/indices.htm.

All data is subject to change without notice.

© 2026 NewEdge Capital Group, LLC