“Billy this is a large-cap software company used by 90% of the Fortune 500, trading at 15x earnings, with mid-teens long-term growth expectations. Their defect is that now anybody with AI tools can replicate their platform in 5 minutes.”

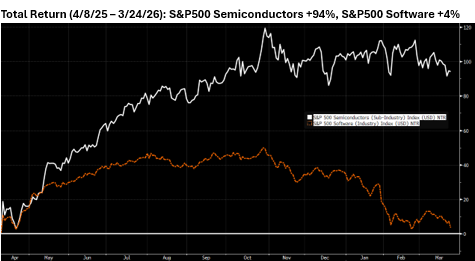

While our quote, referencing the above scene from the 2011 baseball movie Moneyball, is an oversimplification and exaggeration, in our view, it is a fitting analogy for the divergent fundamentals, narratives, and sentiment that surround the global software and semiconductor industries today. This combination of factors has led to a vast performance spread since the market lows of last April, with semiconductors outperforming their software peers by 90%, as seen in the chart below.

Similar to our equity investment philosophy at NewEdge, the movie Moneyball highlights the advantages of using data and multifaceted analysis to find value in a marketplace where prevailing sentiment and uncertainty can lead to mispricing. Using this approach, this week we will dissect the current trends and key performance metrics to watch in both software and semis to explain this divergence and uncover opportunities and risks under the surface.

Summary:

- The relative performance between the software and semiconductor industry groups has reached extreme levels, with narrative and sentiment largely influencing price action and overtaking fundamentals.

- We continue to prefer semis over software, given that the former offer more durable business models and lower risks of obsolescence, but we believe a more balanced allocation between the two groups is warranted at this point due to the wide divergence in sentiment, momentum, and expectations.

- Going forward, we expect some mean reversion in this performance spread and are likely to see greater dispersion within each industry group. As the AI CapEx cycle ages and software companies adapt to a more competitive environment, fundamentals should become a more powerful driver.

- Semiconductors: We expect the massive AI CapEx cycle to continue to power earnings growth for the industry, but we are seeing signs that the cycle is aging. As a result, we prefer more durable semi equipment companies over more cyclical memory companies.

- Key Watch Item: Gross Margins – An early indicator of demand softening, tight inventories normalizing, and pricing power waning.

- Software: Valuations are reasonable (median FP/E ratios are now on par with the broader S&P500), but questions about terminal growth and AI disruption risks will remain a headwind to valuation expansion. Ultimately, revenue and earnings growth will be the primary driver of return for the next several quarters. We prefer companies higher up in the technology stack, those focused on enterprise customers and that provide mission-critical services (like IT infrastructure and security), and those that manage systems of record (which are a resource for AI tools and applications). All of these should provide some relative insulation from AI disruption.

- Key Watch Item: Accelerating Revenue Growth and Positive Guidance as evidence of durability and successful AI integration as opposed to disruption.

Software vs. Semis

“I’m not paying you for the player you used to be, I’m paying you for the player you are now”

As delivered by General Manager Billy Beane in Moneyball, this quote references an aging player’s contract, and it serves as a great reminder that past performance does not guarantee or predict future returns. This is something to keep in mind given the robust profits and outperformance semiconductor companies have generated, and the valuation compression and underperformance we have seen in many software companies over the past few quarters.

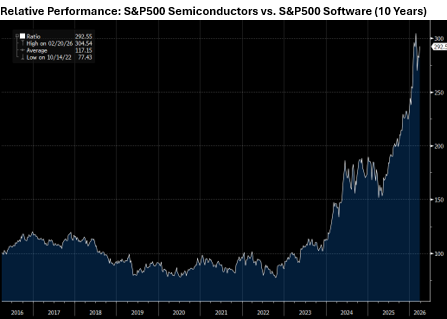

Historically, the performance of the software and semiconductor industries has been closely correlated (averaging 0.75 over the past decade), a function of their premium growth rates, essential products, and positioning at the leading edge of technological innovation. These characteristics have helped drive long-term outperformance for both groups relative to the broader market, yet over the last few years, we have seen a remarkable surge in semiconductors outperforming software companies (highlighted in the relative performance chart below). This outperformance has accelerated over the past year as AI CapEx has exploded higher, AI models have advanced, and questions have emerged about the valuations and durability of many software companies in a world of cheap and rapidly progressing competition from AI.

Ultimately, AI adoption and innovation have been the key drivers of this divergence, as they continue to fuel a massive appetite for compute and feed the AI infrastructure beneficiaries like semiconductors. At the same time AI innovation has led to legitimate questions about valuations, terminal growth, and business moats for nearly all software companies.

As we commonly see at times when narrative and secular themes are top of mind, both buying and selling in these industry groups have become increasingly indiscriminate and less based on fundamentals. In our view, this may be masking some cyclical risks in the semiconductor industry and creating some attractive opportunities in the software industry.

Semiconductors: A Historic Boom

As illustrated in the previous chart, it has been a remarkable few years of profit generation and performance for the semiconductor group. Many experts believe this CapEx cycle aimed at building the foundation for the future of AI will be the largest structural boom in the history of the industry.

This boom is leading to massive increases in semiconductor-reported earnings and future expectations (chart below), which is causing valuations to look much cheaper today than we would expect in a more normal environment. Case in point, Micron Technologies, one of the largest memory chip makers in the world and a highly cyclical business, is trading today at just 5x FP/E despite shares returning more than 300% over the past 12 months. This has been driven by a surge in annual EPS, expected to rise from $8 in 2025 to $55 in 2026.

While earnings momentum is clearly strong and accelerating today, at some point this cycle will mature, spending and growth will begin to normalize, and an eventual reversion in profitability will occur. Ultimately, the most cyclical segment, memory chip makers, could be the first to turn lower, as is often the case in semiconductor cycles. Today, this memory chip segment is producing remarkable earnings growth due to limited inventories, surging demand, and aggressive price increases. These factors will begin to normalize in the coming quarters as production increases, inventories normalize, and high prices begin to weigh on demand. While peak earnings for the group may be several quarters away, the share prices of memory chip companies have historically peaked 9-12 months before reported earnings. This supports our more cautious stance towards the memory segment today, despite what appears to be attractive valuations.

At NewEdge, we have generally preferred the more durable dynamics offered by semiconductor equipment companies for this exact reason. These businesses, which are quasi-monopolies and provide the critical tools used to produce chips, are generally less exposed to the industry’s boom-and-bust nature. Revenues are driven by a combination of products and ongoing service, and critical equipment is usually one of the last places customers look to curtail spending. While they are not immune from the cycle, they are generally disciplined capital allocators, with healthy free cash flow and consistent profitability relative to their memory peers.

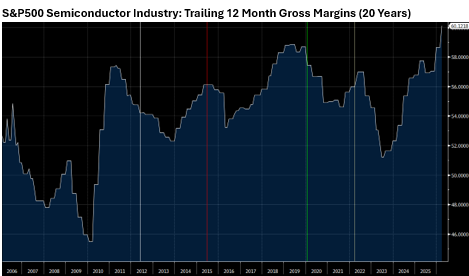

The key watch item for the semiconductor industry is gross margins, historically a strong indicator of the state of the cycle and forward performance. Today, trailing 12-month gross margins are at a record 60%, surpassing the prior peaks seen in 2010 and 2020. This indicates the current cycle has reached a more mature phase, making the forward risk and return less compelling, and suggests investors focus on more durable segments within the group.

Software: Increased Competition Resets Valuations, But Not All Will Be Disrupted

In Moneyball, general manager Billy Beane explains the rationale for his unique analytical approach to player evaluation by saying, “adapt or die.” While this is an extreme analogy, we believe the message for incumbent software companies is valid given the rapid advancements AI models and tools have achieved in just a few short years.

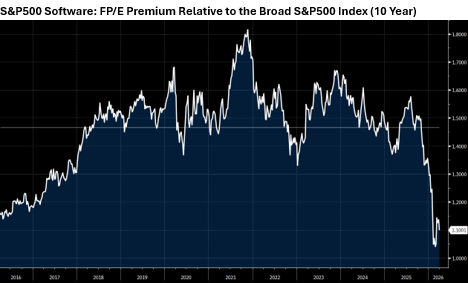

The global software industry has long commanded a valuation premium in equity markets (averaging 50% over the past 10 years). This is the result of attractive growth rates and profit margins. These firms have tended to have wide business moats that include pricing power and high switching costs, as well as the ability to continuously create and deliver innovative platforms and services. In short, they are essential tools for most corporations and employees.

The rise of AI, however, has called into question many of these features over the past several quarters and led to a remarkable revaluation of the industry. Software now trades on par with broad equity markets despite many key fundamental metrics like annual recurring revenue growth, retention rates, and profitability remaining relatively stable. This valuation compression, despite healthy fundamental metrics, largely reflects investor concerns about the impact of AI on long-held business moats and terminal growth rates.

While many are suggesting the software business model is dead or will be significantly disrupted in the future (as valuations now imply), we believe the impact will be more nuanced and that there will be winners and losers in the industry as AI advances and software companies adapt to this new world of increased competition.

The Technology Stack Explained Using a Restaurant Analogy

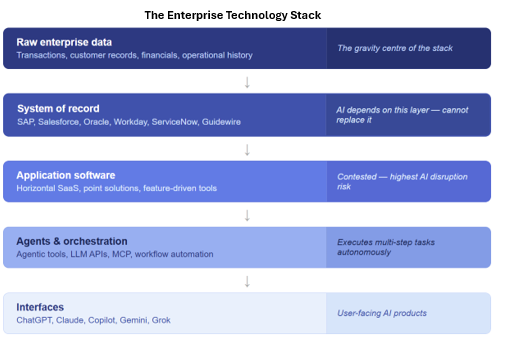

To help explain what parts of the industry may or may not be at risk of disruption, it helps to think of a corporate technology stack like a restaurant. At the bottom of the stack (or front of the house) sits the interface layer. This is the restaurant menu and customer experience where humans interact with technology. It is an area that was already commoditized even prior to AI, and it is where AI products like ChatGPT, Copilot, and Gemini are already increasing worker productivity and handling more routine tasks.

The next level up is the orchestration layer, the waitstaff that takes instructions from the interface layer and coordinates the type of meal to be prepared. This is where we find AI agents and workflow tools like Claude Code that can not only provide information and context about a meal, but also make sure it is prepared and delivered to your table correctly.

Moving another level up and into the kitchen, where software’s moat starts to deepen further, is the application layer. This is the chef who is a master at his craft, knows the recipes, and expertly prepares the meal being requested. While AI is already handling aspects of the application layer like writing code or allowing users to build custom tools, it has not yet reached the level of mastery that comes from decades of experience and product refinement. The moat is also stronger at this layer due to the degree of complexity and the critical demands of reliability and accuracy. At the top of the technology stack sits the system of record layer. This is the vault, pantry, and accounting ledger of the restaurant. It is the hard data of a company or physical restaurant inventory that AI tools can rely on, but ultimately will struggle to displace. AI tools (a waiter in this analogy) can look in the pantry and predict when something may run out. However, the system of record (and companies that securely store, manage, and analyze this data) is the final authority on this information. This makes it an essential source for AI tools that sit at the lower layers and suggests this layer could be a beneficiary of AI innovation as opposed to being displaced by it.

We recognize that it is certainly possible to pick apart our restaurant analogy and the durability and nuances of these various layers. This is partly why we have seen such broad-based selling pressure across the industry over the past several quarters. However, we think this framework is a helpful starting point, and it leads us to explore how software companies at each of these layers may be able to adapt to a new, more competitive environment.

Ultimately, the traditional seat-based software pricing model is likely to change to an output or consumption-based pricing model. The productivity gains from AI innovation are likely to act as a headwind to corporate headcount, and, as a result, software companies will need to shift towards a revenue model driven by what tasks are completed and how many tasks are completed vs. how many employees use the software. This should ultimately allow for more durable revenue growth and assigned value from customers exploring lower-cost AI alternatives. In addition to adapting their revenue models, we believe software companies that focus on enterprise customers will be relatively more insulated from AI disruption. Enterprise customers are highly complex organizations, with vast employee bases that utilize a web of technology to handle mission-critical tasks. This combination will make it harder but not impossible for AI to displace software incumbents in this space.

When evaluating opportunities in the software industry, we would prioritize companies focused on applications and systems of record, those that are transitioning to a consumption-based pricing model, those that primarily focus on enterprise customers, and those that are able to successfully integrate AI products and resources across their platforms.

While software stocks have recently reached a deeply oversold state, making them prone to a bounce or modest recovery in the near-term, a more durable recovery will require fundamental results. Historically, the best measure of success and the one that has rewarded investors the most following industry downturns has been accelerating revenue growth and improved guidance.

Many software companies have posted mid-teens or even 20%+ revenue growth in recent quarters, yet investors have discounted this, likely because overall growth rates continue to moderate and AI disruption fears remain top of mind. In our view, it will take time for companies to turn this narrative around, meaning valuations are likely to remain compressed. Companies that can demonstrate sequential revenue acceleration and underscore business momentum with increased guidance are likely to be rewarded.

Bottom Line

The recent bifurcation between the software and semiconductor industries and the debate over which group will ultimately win out is likely to continue to be a fascinating discussion and key consideration in equity markets for the next several quarters. In our view, investors today should seek balanced exposure between the two index heavyweights (both of which offer healthy fundamentals relative to the broader market), but also be more surgical and disciplined with exposure to either group. For semiconductors, the profitability story remains a key driver as does the clear industry correlation with the growth of AI adoption (AI can’t make its own chips…yet). Those factors should continue to be a pillar of support for the group as AI technology evolves, although investors should be mindful that share prices may peak before underlying earnings, as the end of the AI CapEx cycle appears on the horizon. For software, the disruption narrative is likely to continue to act as an anchor on valuations. However, for companies that can adapt their business models and focus on more defensible areas within the technology stack, profitability may eventually be rewarded, and we may look back on today’s valuations for some as a generational opportunity.

IMPORTANT DISCLOSURES

The views and opinions included in these materials belong to their author and do not necessarily reflect the views and opinions of NewEdge Capital Group, LLC.

This information is general in nature and has been prepared solely for informational and educational purposes and does not constitute an offer or a recommendation to buy or sell any particular security or to adopt any specific investment strategy.

NewEdge and its affiliates do not render advice on legal, tax and/or tax accounting matters. You should consult your personal tax and/or legal advisor to learn about any potential tax or other implications that may result from acting on a particular recommendation.

The trademarks and service marks contained herein are the property of their respective owners. Unless otherwise specifically indicated, all information with respect to any third party not affiliated with NewEdge has been provided by, and is the sole responsibility of, such third party and has not been independently verified by NewEdge, its affiliates or any other independent third party. No representation is given with respect to its accuracy or completeness, and such information and opinions may change without notice.

Investing involves risk, including possible loss of principal. Past performance is no guarantee of future results.

Any forward-looking statements or forecasts are based on assumptions and actual results are expected to vary from any such statements or forecasts. No assurance can be given that investment objectives or target returns will be achieved. Future returns may be higher or lower than the estimates presented herein.

An investment cannot be made directly in an index. Indices are unmanaged and have no fees or expenses. You can obtain information about many indices online at a variety of sources including: https://www.sec.gov/answers/indices.htm.

All data is subject to change without notice.

© 2026 NewEdge Capital Group, LLC