“Oh, here we go again”

Taylor Swift, My Boy Only Breaks His Favorite Toys

Global bond markets let out a primal scream this week that was reminiscent of a fully-“seen” millennial singing along to The Tortured Poets Department at max volume (IYKYK).

Long bond yields spiked higher (prices fell) around the globe as a confluence of events conspired to dampen demand for duration risk and even cause (some) equity markets to lurch lower.

The key point here is that it was, in fact, a confluence of events (or, as TSwift sings, “a litany of reasons why”) and not just one driver behind this jump higher in yields. These reasons include:

• The Moody’s downgrade of U.S. federal debt last week caused the U.S. to lose its second-to-last AAA rating. Some Treasury market investors, like Hong Kong pensions, could be forced sellers were the U.S. to lose its last AAA rating (though there would likely be workarounds if this were to transpire).

• The House passed a deficit-ballooning reconciliation bill that’s projected to add $3.3 trillion to the deficit over the next 10 years. This bill has to go to the Senate, which is likely to mark it up significantly with fewer tax breaks (there is not as much pressure in the Senate to raise SALT caps, for example) but also fewer spending cuts (there is little appetite in the Senate to push through big cuts to Medicaid, for example). On balance, given the Senate’s distaste for spending cuts, its version could be even more deficit-amplifying than the one voted out of the House.

• A weak 20-year U.S. Treasury auction on Wednesday raised questions about investor appetite for duration.

• A very weak 20-year bond auction in Japan, the weakest demand since 1987, amplified questions about the future path of the Bank of Japan’s tapering of bond purchases (recall the BOJ owns half of the outstanding JGBs!)

• Canadian core inflation came in hot.

• Ditto in the UK.

• U.S. manufacturers continue to experience and expect further price increases. The S&P Global Prices component rose to its highest level since 2022. We should note that actual inflation data has cooled recently, but that tells us little about whether higher inflation could be around the corner.

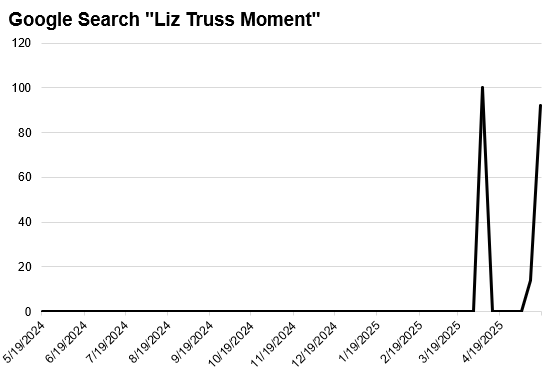

• Broad concerns about fiscal sustainability are likely putting upward pressure on global bond term premium, which is the extra compensation investors demand to lend for longer periods of time (see below for the chart of Google searches for “Liz Truss Moment” spiking, proving that the legacy of her budget deficit “yip” from 2022 has more staying power than a head of lettuce).

• Yields tend to be correlated across developed markets, meaning a move in the U.S. Treasury market can impact German bunds or JGBs, and vice versa.

• Global recession odds have fallen somewhat as worst-case trade fears abate (we typically see increased demand for “safe haven” government debt when concerns about economic growth rise, so if economic growth concerns are fading, there is less demand for safe bonds at the margin). Corroborating this, we see some global equity indices, like the MSCI EAFE International Developed Index, hitting new all-time highs. This would not be the case if global recession odds were rising.

All of this can be simply encapsulated in basic supply and demand terms. As we learn in ECON 101, when supply increases and/or demand decreases, prices fall. For bonds, falling prices translate to higher yields.

In today’s bond market, we are seeing both increased supply (higher fiscal deficits/spending from the U.S. and Europe, mainly Germany) and decreased demand (falling recession odds, worries about stickier inflation, worries about fiscal sustainability, and reduced buying from central banks, like the BOJ).

This all raises a few BIG questions for investors, including:

a) How much higher could yields go in the short term?

d) Will long bonds be as good of a source of diversification against risk assets in the next recession (will they fall as much) as they did in prior periods of weakness?

c) What are the economic implications of higher for longer yields?

d) Will higher yields “intimidate” governments into constraining spending?

All of these questions strike an important chord: falling yields has been a “Favorite Toy” of the global economy over the last 40 years, allowing for ever-rising public deficits and providing a powerful tailwind to investment returns across risk spectrums (read: Howard Marks’ “Sea Change”).

But have “our boys”, meaning global policy makers, “broken their favorite toy” with hefty deficit spending and a sharp reorientation of global capital flows (thanks to the trade war), where hopes for falling yields (such as Treasury Secretary Bessent’s begs and boasts for a lower 10-year yield) are likely to be dashed until more serious economic weakness revives a powerful flight to safety?

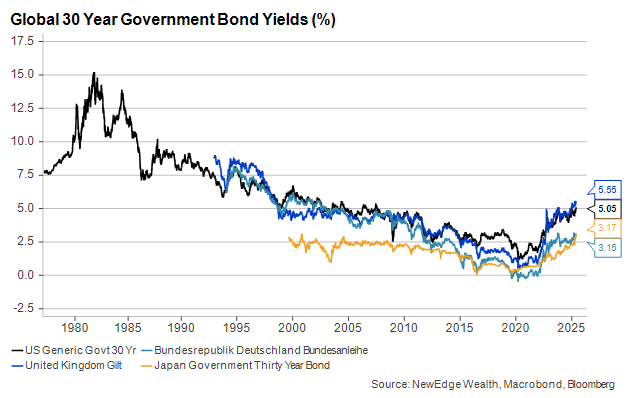

The answer to this “broken toy” question appears to be “yes,” given the 40-year bull market in long bonds is clearly over.

That brings us back to our four BIG questions, which all arguably deserve their own piece, but we will answer in brief below.

“Called the rain to end our days of wild”: How much higher could yields go in the short term?

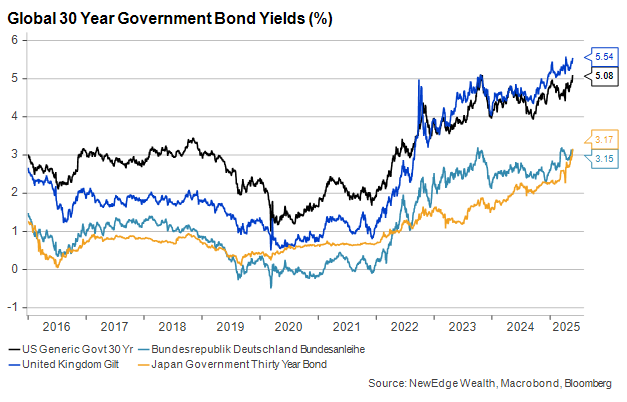

The great market technician, John Roque, wrote recently about the chart of global 30-year yields, “if these were stocks, you’d be long”, effectively saying yields are biased higher.

As 30-year bond yields break out and make new multi-decade highs, it raises the question of how high U.S. 10-year Treasury yields could go as well. 10-year yields remain below their recent highs, but we would not be surprised to see a retest of 4.8-5% on the 10-year given recent price action.

Recall our outlook for the 10-year at the beginning of 2025 was a wide, choppy range (like equities), where we saw the yield potentially touching both 3.5% and 5% over the course of the year on the potential of experiencing both growth fears (pushing yields lower) and deficit fears (pushing yields higher).

U.S. 10-Year Treasury Yield with RSI

But just as the old commodities phrase goes, “the cure for high prices is high prices”, we would likely see structural buyers of bonds near 5%, as the high yields would provide a substantial buffer for potential further price loses (we saw buyers step in at 4.80% and 5% over the past two years).

Given the moves to new cycle highs for 30-year bonds, we can’t rule out a breakout above 5% on the 10-year (this would likely require a reacceleration in growth and/or inflation, plus a fiscal deficit bonanza). This would be a thoroughly jarring development for global markets, making a close monitoring of the 10-year yield at these various resistance levels an imperative.

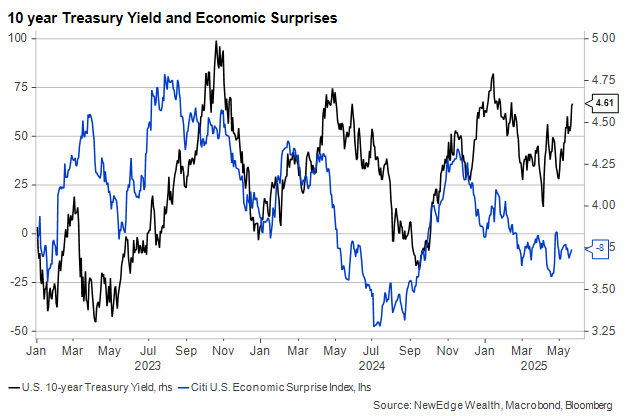

On the flip side, we must note that rates could show renewed sensitivity to incoming economic data if it begins to weaken over the summer under the weight of tariffs. As the chart below shows, rates have diverged from Economic Surprises in recent months. This could reflect the deficit concerns, but also likely reflects that most of the economic data weakness has been contained in “soft data” that has not made its way into real “hard data” yet.

“Put me back on my shelf”: Will long bonds be as good of a source of diversification against risk assets in the next recession (will they fall as much) as they did in prior periods of weakness?

The answer to this is yes, eventually, but also maybe not for long.

We do expect that if the economy were to weaken substantially, it would spark a flight to safety out of risk assets (like equities and credit) and into “safer” assets like government bonds. Further, with acute economic weakness, we would likely see a response by central banks, such as the Fed, to return to Quantitative Easing, buying bonds to pump liquidity into the economy.

The challenge (it is actually a good thing!) in the near term is that the data simply has not been weak enough to cause investors to substantially flock to safety, nor for central banks to come to the rescue. So, eventually, we expect bonds to rally and provide a ballast to portfolios, but it will come with a much weaker growth backdrop (be careful what you wish for?).

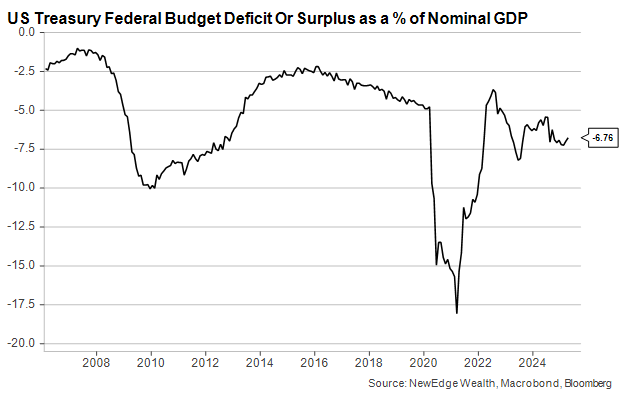

We also think this rally into U.S. bonds in the next recession/growth panic could be short-lived, given the high starting point of deficits in a strong growth environment (currently 6.7% deficit to GDP). Weaker economic growth in even a mild recession could result in a jump in the deficit to GDP ratio to prior crisis levels, such as the 10% reached during the Great Financial Crisis, due to falling tax receipts and automatic spending stabilizers, like unemployment. This could cause yields to spike soon after dropping at the start of a recession if investors grow even more concerned about fiscal sustainability (though the Fed will likely be monetizing this debt through QE as well!).

“Should have known it was a matter of time”: What are the economic implications of higher for longer yields?

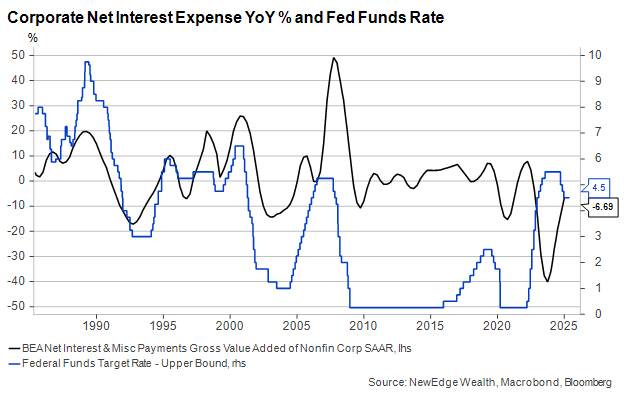

The longer long rates stay high, the more they will weigh on the real economy. We have written extensively over the last 2.5 years that a key reason for economic resilience in the U.S. was the terming out of debt when rates plunged post-COVID. This immunized broad corporate and household borrowers against the sharp rise in short-term rates, allowing the U.S. economy to remain resilient in the face of rapid Fed rate hikes.

But as some of this COVID-era debt begins to mature (the average maturity on a high yield bond is ~5 years), we are likely to begin to see these higher rates impact aggregate borrowing costs in a more meaningful way. This is exacerbated by falling short rates, which lower cash interest income, potentially causing a more restrictive rise in net interest expense (a sharp contrast to the stimulative plunge in net interest expense in recent years).

This is the dynamic of the “Zoo Steepener” we have written about, which also impacts consumers: falling yields on the short end pinch cash interest incomes while rising yields on the long end hurt housing activity.

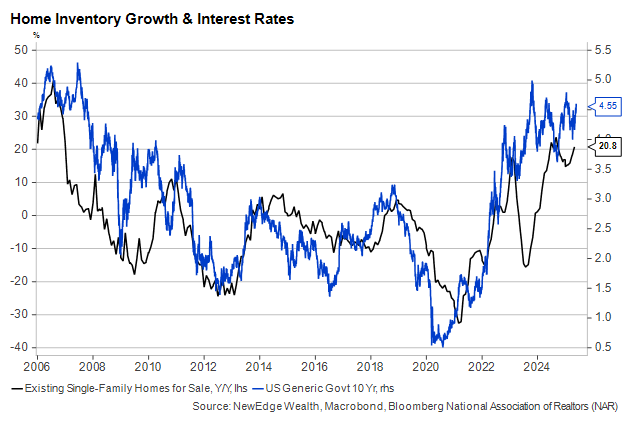

The chart below shows the impact of high rates on housing activity, with high mortgage rates keeping upward pressure on unsold home inventories. High rates are exacerbating affordability challenges, and while they likely deter some existing homeowners from selling, they have a larger impact on demand.

Overall, we think that the U.S. economy’s sensitivity to the level of interest rates increases as we get further away from the COVID yield lows. This means that a continued/sustained rise in interest rates is likely to tighten real financial conditions more than it has over the past few years, but still with a significant lag given term-out long-term mortgages and investment-grade credit.

“There was danger in the heat of my touch”: Will higher yields “intimidate” governments into constraining spending?

The answer this question is once again “it has to get worse before it gets better”, meaning the current level of yields is likely not enough to get the attention of policy makers, but a surge of the 10-year above 5% (oh so “yippy”), for example, likely could cause policy makers to take the message of markets more seriously.

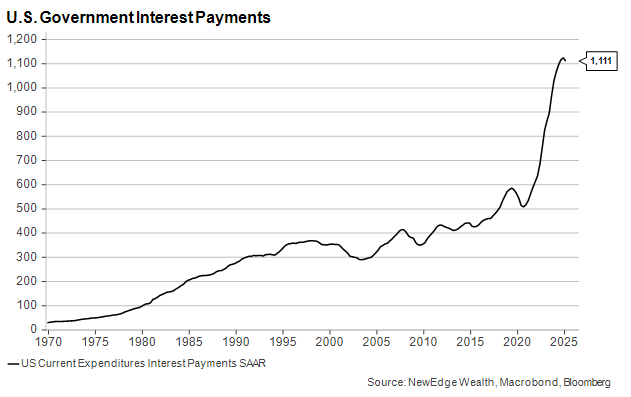

The reality is that interest costs are a real constraint on policymakers. In the U.S., the cost to service the government debt is now over $1 trillion. Further, Dan Clifton of Strategas notes that interest cost has now reached 18% of total tax revenues, even higher than the 14% level that has historically triggered efforts to rein in budgets and pursue austerity.

“Once I fix me, he’s gonna miss me”: Conclusion

We have been calling the last few years of higher inflation and higher interest the “Era of Consequence” (before the Eras Tour was a thing, for the record!). The Era of Consequence acknowledges that decisions to both spend and invest were made easier by a world with falling inflation and interest rates. However, in a world where these two factors are high or rising, decisions about public spending and private investment have greater consequences and constraints.

We think investors need to remain nimble with bond markets, where sharp sell-offs driven by frightful narrative can be used to put cash to work (just like in equity markets), with the full awareness that further downside risks are possible given all of the dynamics listed above. In the short term, we see the potential for further upside to yields, as we watch prior levels of resistance closely for signs of a bigger shift in yield trends.

IMPORTANT DISCLOSURES

The views and opinions included in these materials belong to their author and do not necessarily reflect the views and opinions of NewEdge Capital Group, LLC.

This information is general in nature and has been prepared solely for informational and educational purposes and does not constitute an offer or a recommendation to buy or sell any particular security or to adopt any specific investment strategy.

NewEdge and its affiliates do not render advice on legal, tax and/or tax accounting matters. You should consult your personal tax and/or legal advisor to learn about any potential tax or other implications that may result from acting on a particular recommendation.

The trademarks and service marks contained herein are the property of their respective owners. Unless otherwise specifically indicated, all information with respect to any third party not affiliated with NewEdge has been provided by, and is the sole responsibility of, such third party and has not been independently verified by NewEdge, its affiliates or any other independent third party. No representation is given with respect to its accuracy or completeness, and such information and opinions may change without notice.

Investing involves risk, including possible loss of principal. Past performance is no guarantee of future results.

Any forward-looking statements or forecasts are based on assumptions and actual results are expected to vary from any such statements or forecasts. No assurance can be given that investment objectives or target returns will be achieved. Future returns may be higher or lower than the estimates presented herein.

An investment cannot be made directly in an index. Indices are unmanaged and have no fees or expenses. You can obtain information about many indices online at a variety of sources including: https://www.sec.gov/answers/indices.htm.

All data is subject to change without notice.

© 2026 NewEdge Capital Group, LLC