But oh, it’s heaven

Nowadays

“Nowadays”, Roxie Hart, Chicago the Musical

It’s good, isn’t it?

“Let me start by saying that we think the economy is in a really good place, and we think policy is in a really good place.”

Grand, isn’t it?

“The economy is strong overall and has made significant progress toward our goals over the past two years.”

Great, isn’t it?

“So, I feel very good about where the economy is and the performance of the economy, and we want to keep that going.”

Swell, isn’t it?

“Again, the U.S. economy has just been remarkable, and in these international meetings that I attend, this has been the story is how well the U.S. is doing.”

Fun, isn’t it?

“I feel—I feel very good about where the economy is. Honestly, I’m very optimistic about the economy. And it’s—we’re in a really good place. Our policy is in a really good place. I expect another good year next year.”

Nowadays…

All these quotes, interspersed with Ms. Roxie Hart’s purring, were from Federal Reserve Chairman Jerome Powell’s Wednesday press conference. Powell was so confident, so optimistic about the US economy, a notable evolution from his relatively guarded and hedged assessments of economic health in recent years, you could almost hear him sing “oh it’s heaven nowadays”.

Powell isn’t wrong in his assessment of the U.S. economy, as it has displayed resilient growth in recent years, defying consensus (and his own) expectations for a weaker growth environment.

But as Roxie Hart warns, “nothing stays,” meaning we must ask the question if Powell’s proclamations of optimism are an accurate assessment of the future path of the economy in 2025 or if they are potentially ill-timed, coming right as growth could potentially disappoint (effectively the inverse of recession fears in late 2022 as growth was reaccelerating).

We are not currently making a recession call for 2025, as we see plenty of reasons to be optimistic about the U.S. economy (such as a still-relatively tight labor market, animal spirits driven by the hopes and execution of policy change, technology spend, and the resulting productivity, etc.).

But we also see reasons to question an acceleration in growth in 2025 (such as higher for longer rates preventing a recovery in cyclical sectors and beginning to bite companies that are refinancing, the pursuit of fiscal prudence that weighs on near-term growth, the potential for growth-dampening policies with tariffs or immigration reform, etc.).

Renaissance Macro’s Neil Dutta’s recent comments do cause our ears to perk up, given his accurate optimism in 2022-2024:

“Two years ago, back in 2022, I recall the consensus was largely on the recession train for the coming year (I took the other side) even though labor markets were fine and homebuilding stocks were outperforming despite rate hikes. Today, the consensus is fairly sanguine on growth next year. However, labor markets have been cooling, and homebuilding stocks are presently underperforming despite the reduction in rates. I see myself on the more cautious side of the consensus at present.”

Just because it is consensus does not mean it has to be wrong, meaning we can still experience healthy growth even if it is broadly expected, but we should also note that the bar for upside to growth is somewhat higher after the last two years.

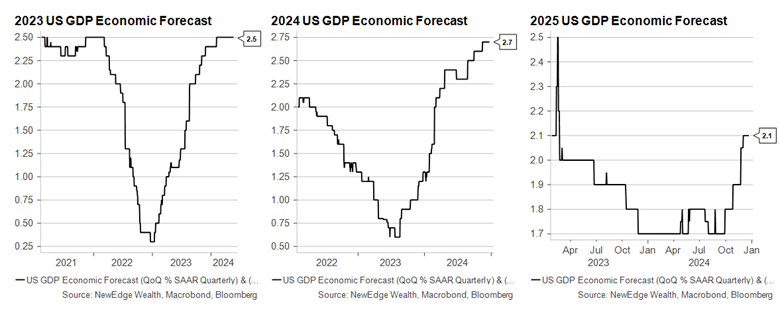

Growth estimate revisions higher have been the underpinning driver of the bull run in equities and credit over the last two years. As the charts below show, annual GDP being revised from 0.25% to 2.9% (final figure) over the course of 2023 and 1% to 2.7% over the course of 2024 has been a key reason why equities and credit have staged such powerful rallies.

2025 begins with estimates for 2.1% growth, which would be a meaningful deceleration from the last two years but not nearly as much of a low bar as 2023 and 2024. We see the path of this growth estimate, whether it is higher, lower, or sideways, as a major determinant of the path of equity returns as well.

Thus, if Powell’s optimism is misplaced for 2025, then it could have a substantial impact on investors who are “all in” on growth remaining grand.

“Everywhere Life, Everywhere Joy”: Investors Share the Optimism

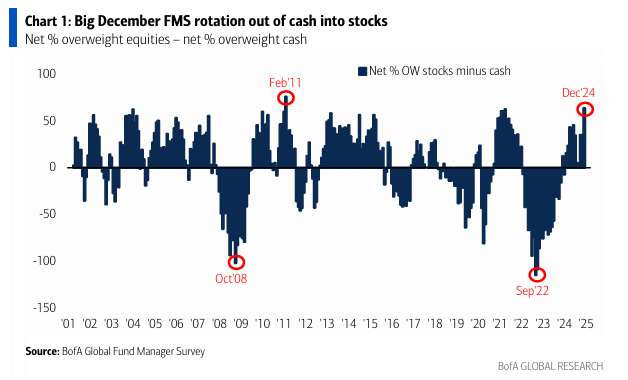

Powell is not alone in his rosy assessment of the economy’s growth prospects. The chart below from this week’s Bank of America Fund Manager Survey shows that nearly 60% of respondents do not expect a recession in the next 18 months.

This rosiness is reflected in fund managers’ allocation decisions, with the next two charts showing a recent large rotation out of cash into stocks and cash allocations falling to a record low.

Investors are “all-in” on U.S. economic growth remaining robust and U.S. markets continuing their epic run of the last two years (it’s like they are waving jazz hands that would make Bob Fosse proud).

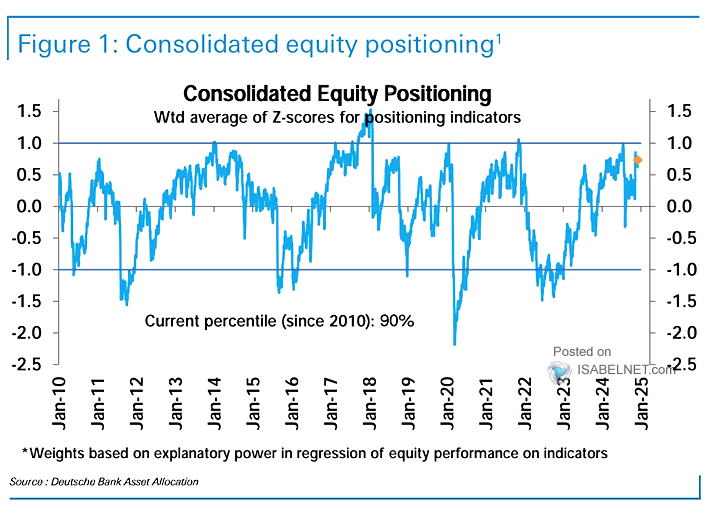

Other measures of positioning reflect this “all-in” attitude, such as the +45% jump in FINRA margin loan balances YTD, the surge in call buying and leveraged ETFs, and the Deutsche Bank Consolidated Positioning Index being in the 90th percentile, as shown below.

This is not to say that investor optimism is not warranted (there are plenty of reasons to be optimistic, as we outlined above!), but investors should know that everyone else seems to agree that it is heaven nowadays.

“In 50 Years or So, It’s Gonna Change You Know”: Conclusion

If there is one lesson that has been drilled into investors’ psyches in recent years, it is that it behooves us to challenge crowded consensus conclusions. When these conclusions feel so right, with few willing/able to argue against them, it is a good time to pause and reassess the thesis and what is already being priced in.

With today’s optimism about growth and equity returns, this pause and reassess does not mean we have to call for an imminent recession or deep market downturn “just because” it is contrarian, but it does mean that we have to be vigilant about potential surprises to these rosy expectations.

As we wrap up 2024 and enter 2025, we will be providing deep dives into these considerations about growth, upside, and downside as part of our 2025 Outlook (be on the lookout for a save the date!).

IMPORTANT DISCLOSURES

The views and opinions included in these materials belong to their author and do not necessarily reflect the views and opinions of NewEdge Capital Group, LLC.

This information is general in nature and has been prepared solely for informational and educational purposes and does not constitute an offer or a recommendation to buy or sell any particular security or to adopt any specific investment strategy.

NewEdge and its affiliates do not render advice on legal, tax and/or tax accounting matters. You should consult your personal tax and/or legal advisor to learn about any potential tax or other implications that may result from acting on a particular recommendation.

The trademarks and service marks contained herein are the property of their respective owners. Unless otherwise specifically indicated, all information with respect to any third party not affiliated with NewEdge has been provided by, and is the sole responsibility of, such third party and has not been independently verified by NewEdge, its affiliates or any other independent third party. No representation is given with respect to its accuracy or completeness, and such information and opinions may change without notice.

Investing involves risk, including possible loss of principal. Past performance is no guarantee of future results.

Any forward-looking statements or forecasts are based on assumptions and actual results are expected to vary from any such statements or forecasts. No assurance can be given that investment objectives or target returns will be achieved. Future returns may be higher or lower than the estimates presented herein.

An investment cannot be made directly in an index. Indices are unmanaged and have no fees or expenses. You can obtain information about many indices online at a variety of sources including: https://www.sec.gov/answers/indices.htm.

All data is subject to change without notice.

© 2026 NewEdge Capital Group, LLC