Please come now, I think I’m falling

I’m holding on to all I think is safe

“One Last Breath”, Creed

After Friday’s disappointing jobs report, the U.S. economy feels a bit like this video of a precariously hanging slice of pizza singing Creed’s 2001 classic “One Last Breath”.

In a blink of an eye, the bulk of the job gains over the last three months were revised away in the July Nonfarm Payrolls print, taking the average payroll gain for the last three months from 150k to a mere 30k. This startled markets out of their cozy complacency (much like the startling moment when Scott Stapp chopped off his luscious aughts-era locks).

This week’s Edge will look at the economic and market implications of this week’s flurry of data and earnings reports, all set to dad rock. Let’s dive in.

“Please Come Now, I Think I’m Falling”: Cozy Calm Is Shattered

Prior to Friday, the prevailing consensus was that tariffs and their related uncertainty were having a negligible impact on the U.S. economy and corporate earnings, allowing U.S. equity markets to surge to new all-time highs and trade at recent record valuations (22.5x forward earnings for the S&P 500).

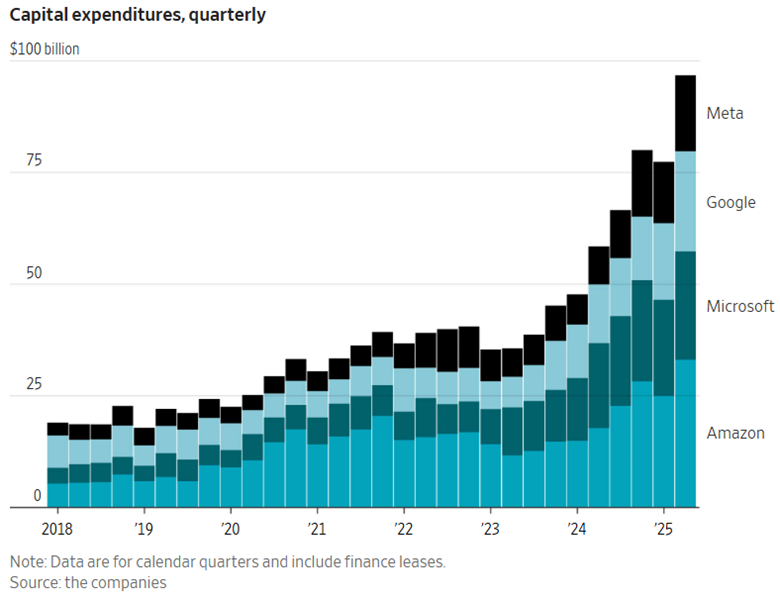

This sanguine consensus was bolstered by a week of powerful big-tech earnings, which saw markets celebrate massive capital expenditure budgets to fuel the artificial intelligence (AI) arms race (Meta, Amazon, Microsoft, and Alphabet announced plans to spend nearly $400B on AI infrastructure in 2025, an eye popping number for these once capital-light businesses).

But all of this optimism was dashed by the July jobs report, which not only came in below consensus (73k vs. 104k consensus), but also included a whopping -258k of negative revisions for the last two months, evaporating any notion of a robust summer economy that was as resilient to tariffs as markets hoped.

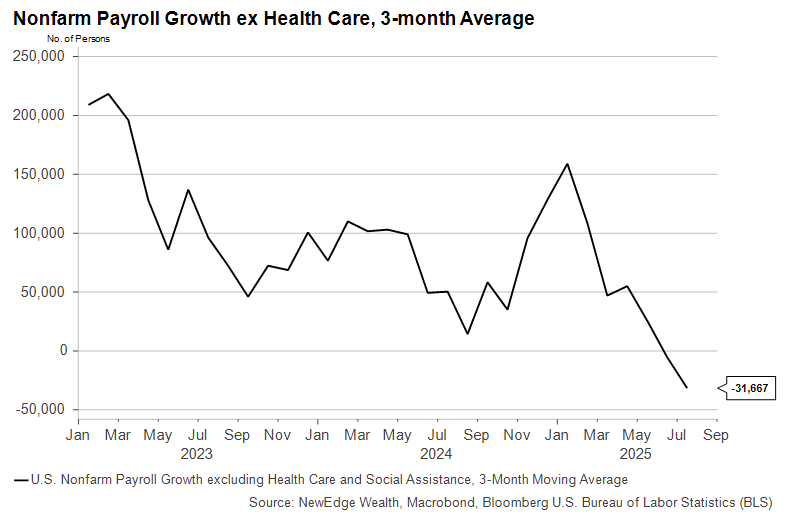

Looking under the hood of the jobs data reveals important details: the only sector that has produced significant job gains since April has been Health Care and Social Assistance, industries that are considered non-cyclical, meaning they are less sensitive to and reflective of underlying economy health. Employment everywhere else – including Information and Professional Services – has been stagnant or falling:

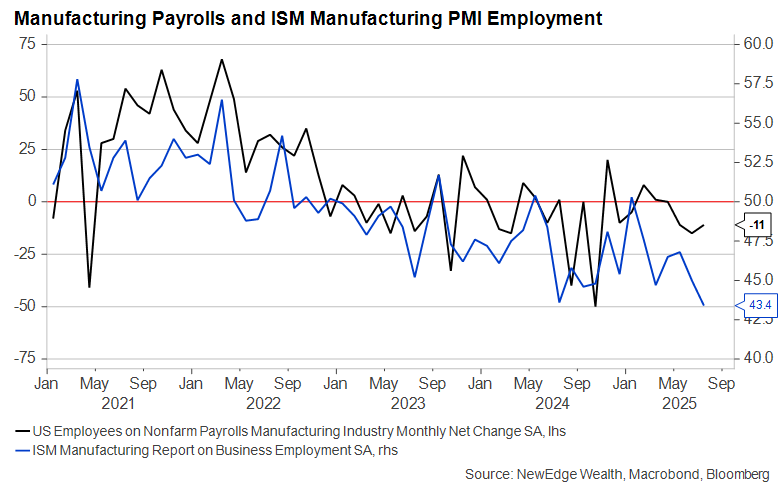

Further, manufacturing employment was weak once again in July. Though employment is an incredibly lagging indicator and we would not expect to see action towards reshoring any time soon (given tariff rate uncertainty and the lead time to planning physical expansions), it must be noted that the purported notion that tariffs have been “good” for the U.S. economy and its manufacturing base is not at all reflected in today’s data. The chart below shows manufacturing employment in Nonfarm Payrolls and the ISM Manufacturing PMI Employment index. Both reflect a contracting manufacturing workforce.

There is optimism that the combination of tariffs and the One Big Beautiful Bill tax provisions (such as accelerated depreciation) will spark a move toward reindustrialization in the U.S., but evidence of moving in this direction is scant for now (it is, arguably, way too early to judge, while as we noted above, any re-shoring will take a long time to materialize).

If there was a “bright spot” in the July U.S. employment report, it was that the unemployment rate did not increase by more (.2 bps more and it would have rounded up to 4.3% from 4.248%!). Part of this is due to the stagnant labor force size. As a combination of immigration policy and demographics have pulled down the labor force participation rate, we have seen less upward pressure on unemployment than we might otherwise in an environment in which payroll growth has dipped well below 100K per month.

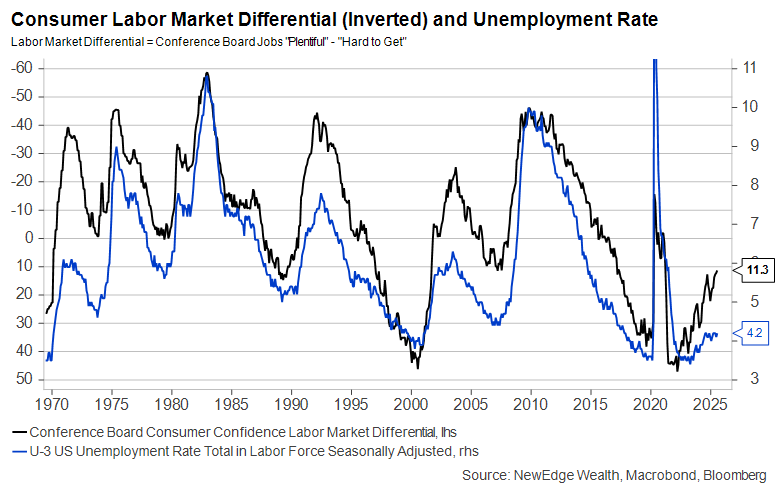

Lastly, we must flag that the quality and independence of all of this data moving forward is being thrown into greater question. First, due to layoffs, various data series have had to rely on more “imputed”, or estimated, data vs. collected observations. Second, President Trump moved to fire the head of the Bureau of Labor Statistics after the weak jobs report. While this does not necessarily mean that BLS data will be fudged or tainted moving forward, it will cause us to consult a wider variety of private sector measures of both inflation and labor market health. As it happens, private sector surveys of labor market sentiment such as the Conference Board’s Labor Market Differential point to even worse deterioration than the unemployment rate would indicate. Consumers, it seems, do not need the data to tell them what to think about the jobs market.

“I Cried Out, ‘Heaven, Save me’”: AI Saves the Economy and Markets in 2Q

A fascinating contrast to the labor market data above, which shows an economy that is adding very few jobs in cyclical sectors and relying solely on job expansion in very defensive sectors (like healthcare), is equity market performance, which has been characterized in the last three months by cyclical outperformance over defensives. This pro-cyclical leadership is normal coming off of market lows (cyclicals tend to have higher beta and more risk-on characteristics), but it still paints an interesting contrast to the underlying economy.

Of course, this is where one would normally pull out the well-worn aphorism “the market is not the economy,” but in 2025, we are actually seeing major market and economic trends mirror each other. Most notably, we are seeing the widely appreciated narrowness of the equity market be reflected in a startling narrowness in U.S. economic growth.

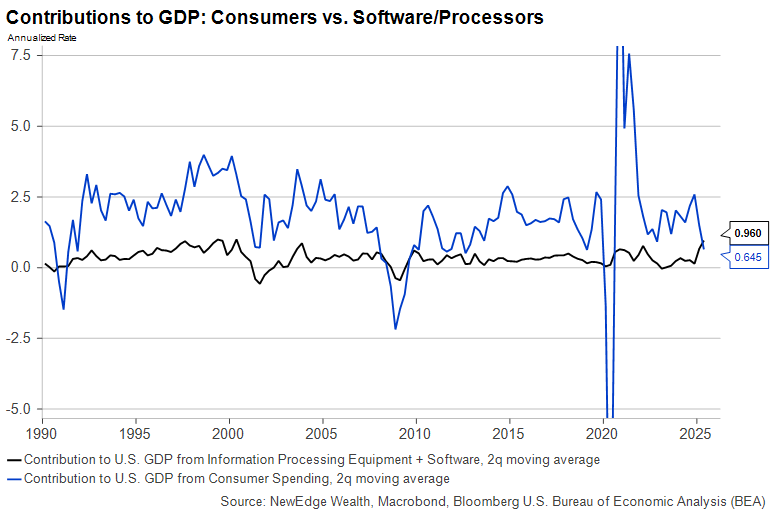

Renaissance Macro’s Neil Dutta alerted us to this fascinating inflection point. He highlighted that private investment in hardware and software, much of which is being devoted to AI development, has overtaken consumer spending as the largest contributor to GDP growth in the second quarter!

This is rare given the consumer’s importance to the U.S. growth model (household consumption typically drives more than 2/3 of GDP) and that consumer spending rarely drops meaningfully outside of recessions. But given the softness of consumer spending YTD (-0.4% annualized for 2025) contrasted with the sharp strength in AI-related spend, we are seeing a pronounced narrowness in what is driving U.S. economic growth.

This narrow economic growth is mirrored by narrow equity market returns: Nvidia (NVDA), which makes up ~14% of the Russell 1000 Growth Index contributed 40% of the index’s return in July and 35% of the index’s return thus far in 2025.

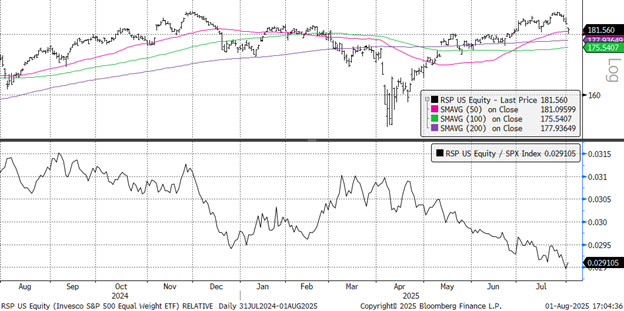

We can see this narrowness on display in another way, with the relative performance of the S&P 500 Equal Weight Index making new relative lows vs. the capitalization weighted S&P 500 this week.

Equal Weight S&P 500 Absolute (Top) and Relative to S&P 500 (Bottom)

This highlights that for both the economy and the U.S. equity market, were it not for the powerful AI investment spending and story, overall growth and returns would likely be far lower. This puts the onus on AI capex to continue to prop up US economic growth and raises the question of how long this feverish pace of CapEx growth can continue into the future (we think this depends on the Mag7’s ability to show robust top-line growth, but this is a broader discussion for next week!).

Maybe Six Cuts Ain’t So Far Down?: Fed Rate Path

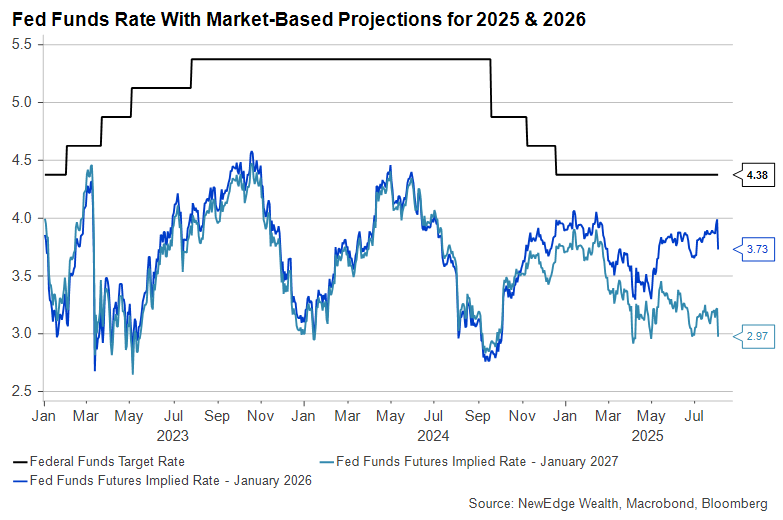

The Fed missed its chance to cut rates this week, electing instead to keep policy unchanged and await more data before its next meeting on September 19th. Would Jay Powell have cut rates had he known how bad the jobs report would be? We’ll never know, but the odds of a September cut, which reached as low as 40% on Thursday, more than doubled off that low following the negative payroll revisions.

But as we’ve pointed out in the past, the market’s changing view on Fed cuts is less about how much the Fed will cut and more about when the Fed will cut. January 2027 Fed Funds Futures still show rates falling to 3% (effectively the Fed’s long run neutral rate) in the next eighteen months or so, not much different than the prevailing view at the April bottom:

One late-breaking item that will add intrigue to the remaining FOMC meetings this year: Governor Adriana Kugler has elected to resign her Board seat six months early, allowing President Trump to appoint a new Governor immediately. This candidate will be the strong favorite to succeed Chair Powell when his term expires next spring. And he or she could add to the growing chorus of members preferring more aggressive interest rate cuts.

“I’m Holding On To All I Think Is Safe”: Conclusion

After a roaring rally over the last three and a half months, we have been flagging in our Monday charts the reasons why we thought markets might be in for a choppier August. These reasons include:

• A sharp overbought condition earlier this week (the market moved too far too fast to the upside), as measured by the relative strength index

• Positioning that reverted to being slightly overweight (Deutsche Bank’s Consolidated Equity Positioning index now in the 59th percentile vs. the 1st percentile at the April lows)

• The end of a run for high beta and low quality names after these areas got to the 100th percentile of relative returns

• Stretched sentiment as captured by rabid risk taking in speculative areas, a spike in call option volumes betting on upside, a spike in retail investor leverage, and more

• Sell-side strategists chasing the market higher, raising their price targets to reflect recent strength

• Seasonality headwinds with Jeff DeGraff from Renaissance Macro flagging that three-month forward returns from this point usually trail other calendar periods, while we also note that volatility seasonality is also a headwind

• Complacency on economic and earnings strength into 2026, as investors were choosing to ignore 2025 and put lofty estimates on 2026 growth

• Major index valuations back to prior highs

These observations do not mean that this bull run is over, but it is likely to take a breather in these late summer days. Whether this breather turns into a deeper correction depends on whether or not the U.S. economic growth is, in fact, taking “One Last Breath”, or if we will see strength resume in the second half of this year.

IMPORTANT DISCLOSURES

The views and opinions included in these materials belong to their author and do not necessarily reflect the views and opinions of NewEdge Capital Group, LLC.

This information is general in nature and has been prepared solely for informational and educational purposes and does not constitute an offer or a recommendation to buy or sell any particular security or to adopt any specific investment strategy.

NewEdge and its affiliates do not render advice on legal, tax and/or tax accounting matters. You should consult your personal tax and/or legal advisor to learn about any potential tax or other implications that may result from acting on a particular recommendation.

The trademarks and service marks contained herein are the property of their respective owners. Unless otherwise specifically indicated, all information with respect to any third party not affiliated with NewEdge has been provided by, and is the sole responsibility of, such third party and has not been independently verified by NewEdge, its affiliates or any other independent third party. No representation is given with respect to its accuracy or completeness, and such information and opinions may change without notice.

Investing involves risk, including possible loss of principal. Past performance is no guarantee of future results.

Any forward-looking statements or forecasts are based on assumptions and actual results are expected to vary from any such statements or forecasts. No assurance can be given that investment objectives or target returns will be achieved. Future returns may be higher or lower than the estimates presented herein.

An investment cannot be made directly in an index. Indices are unmanaged and have no fees or expenses. You can obtain information about many indices online at a variety of sources including: https://www.sec.gov/answers/indices.htm.

All data is subject to change without notice.

© 2026 NewEdge Capital Group, LLC