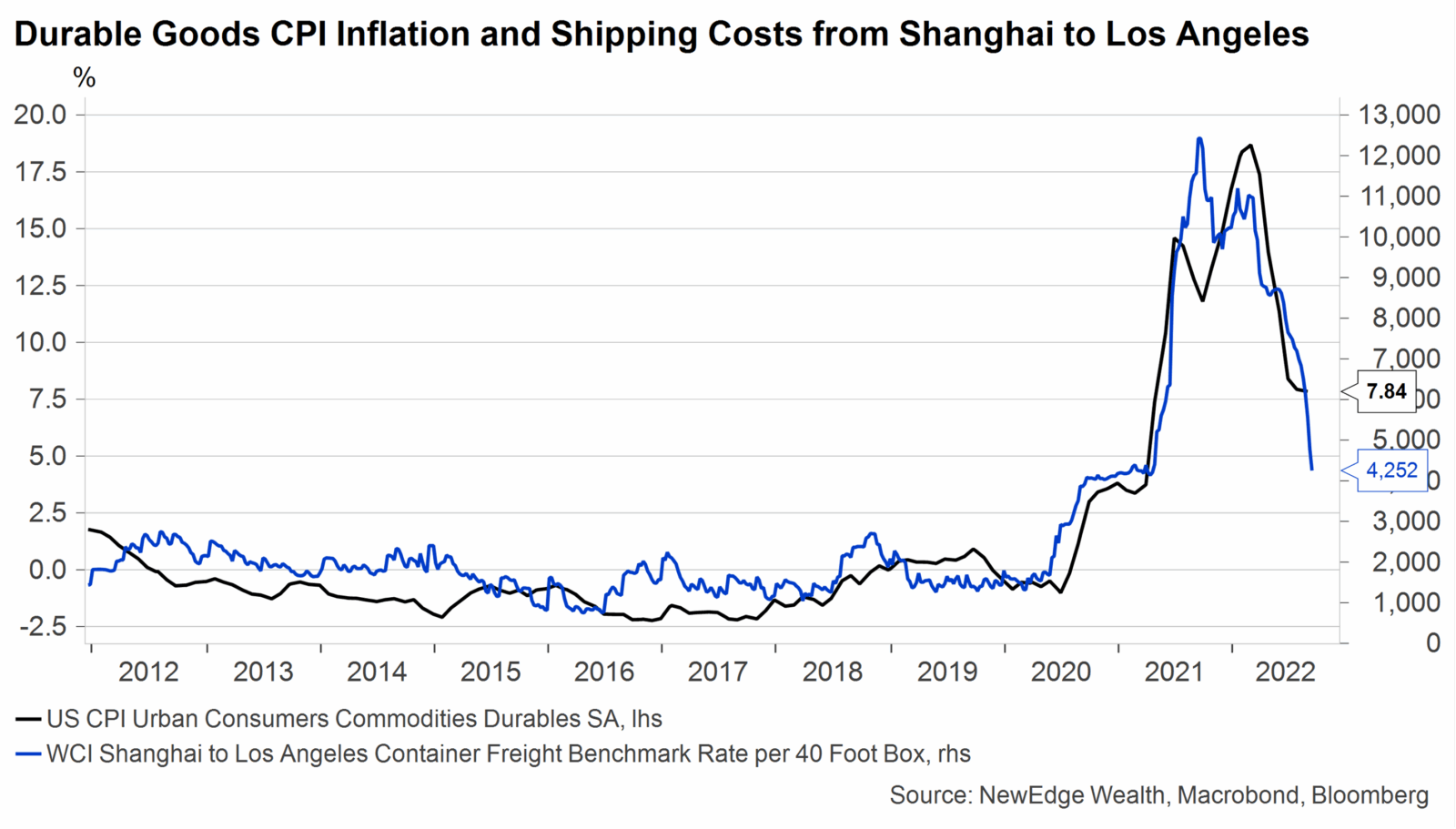

1. Passing the Buck from Goods to Services

The source of elevated inflation has shifted in recent months. The early days of inflation were driven by Goods inflation from surging Goods demand during lockdowns and supply chain stress. This source of inflation has moderated significantly as supply chains heal (lower shipping costs), demand patterns shift (consumers aren’t repeating big-ticket purchases like grills and furniture), and inventories build (companies thought elevated pandemic demand would stay but are now being forced to discount to move excess inventory).

2. Tight Labor Market, High Wages, High Services Inflation

Now that Goods inflation has moderated, today’s elevated inflation is being driven by Services, which are heavily influenced by wages. Given the tight labor market, wages are growing at +6.7% YoY, feeding into higher Services prices. Services inflation, along with wages, tends to be “sticky,” meaning it will take time for this inflation to moderate back to the Fed’s 2% target. This keeps the Fed from pivoting to accommodation and is why the Fed is expressing willingness to see higher unemployment in order to control inflation.

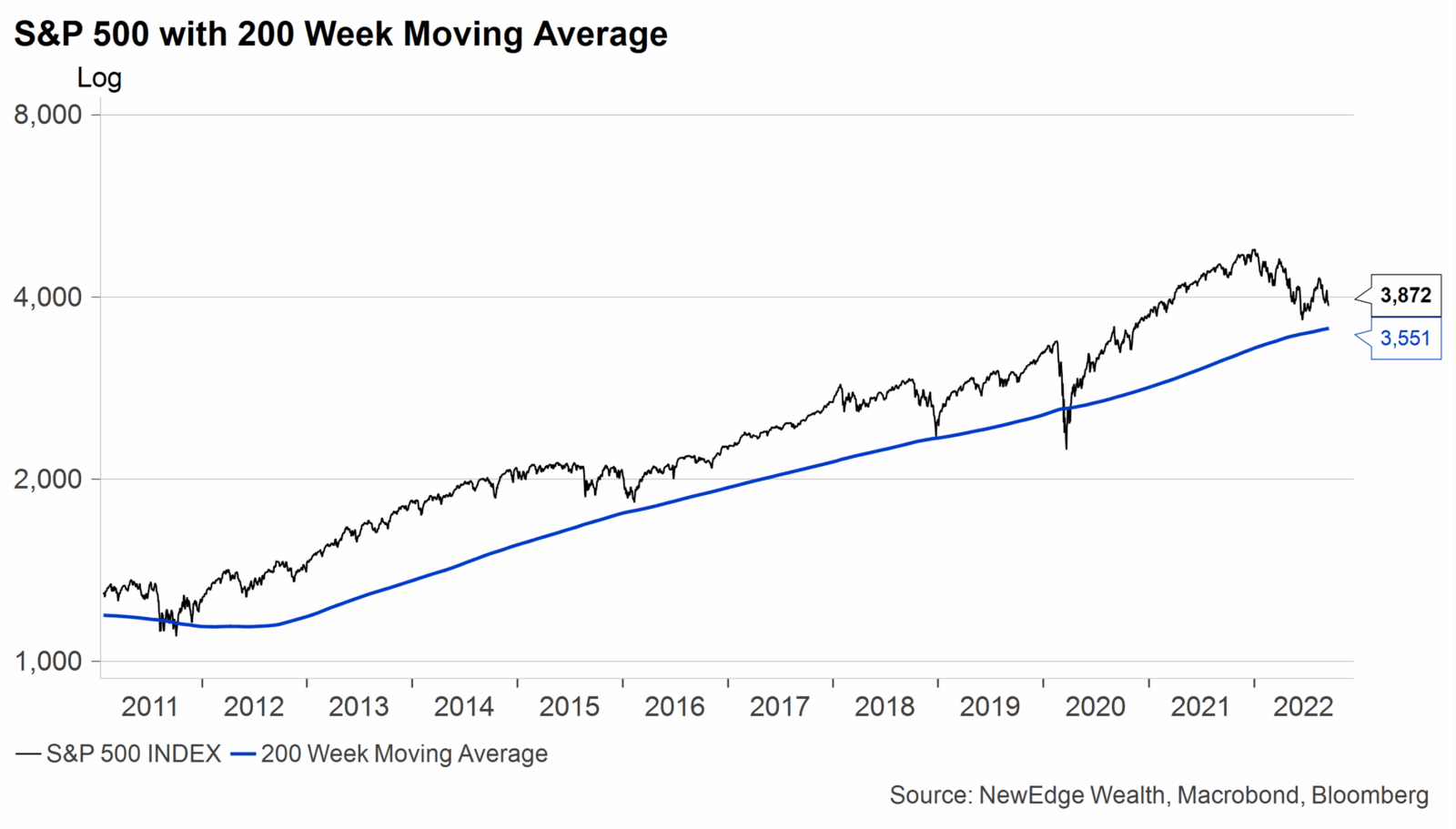

3. A Retest of the June Lows in Play?

We have been watching 3,900 on the S&P 500 as a key battleground area for bulls and bears all summer. Friday’s break below 3,900 puts a retest of the June lows near 3,600 in play. Also near 3,600 is the 200-week moving average, which has been an important support level for the market coming out of the Great Financial Crisis. Though the Fed’s accommodative posture is different compared to the post-GFC bull run and this may not be the ultimate low for this year, we think the risk-reward for long-term investors looking out 12-24 months gets much more attractive near these levels.

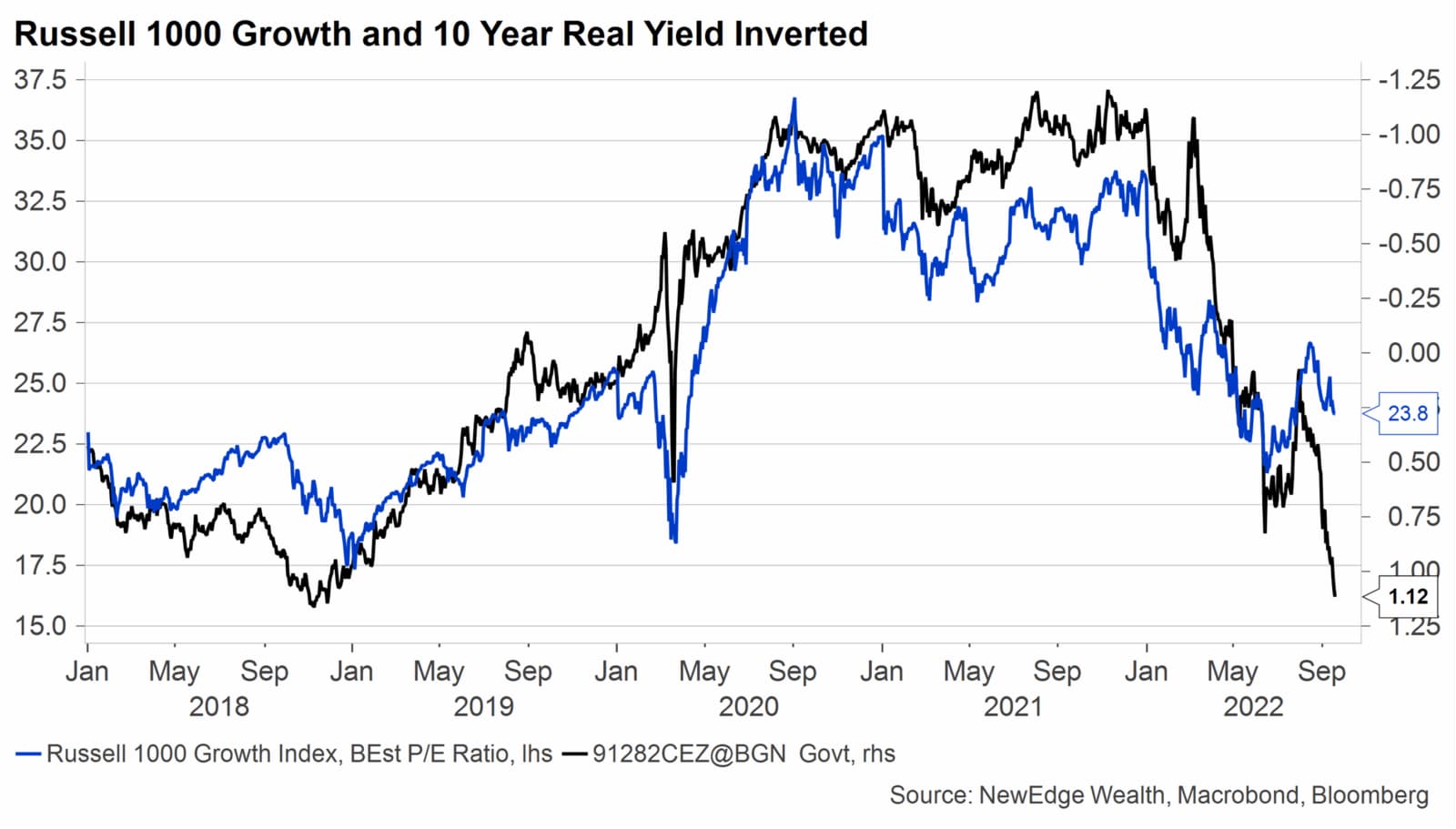

4. Growth Stocks Are Too Expensive Given Liquidity Backdrop

We continue to see valuations as a risk for this market, both capping the upside for rallies and potentially being a source of downside if valuations fall below average as they typically do during tightening cycles and recessions. Growth stocks are particularly challenged, trading near 24x forward earnings. Growth stocks are too expensive given the tight liquidity backdrop and higher rate environment.

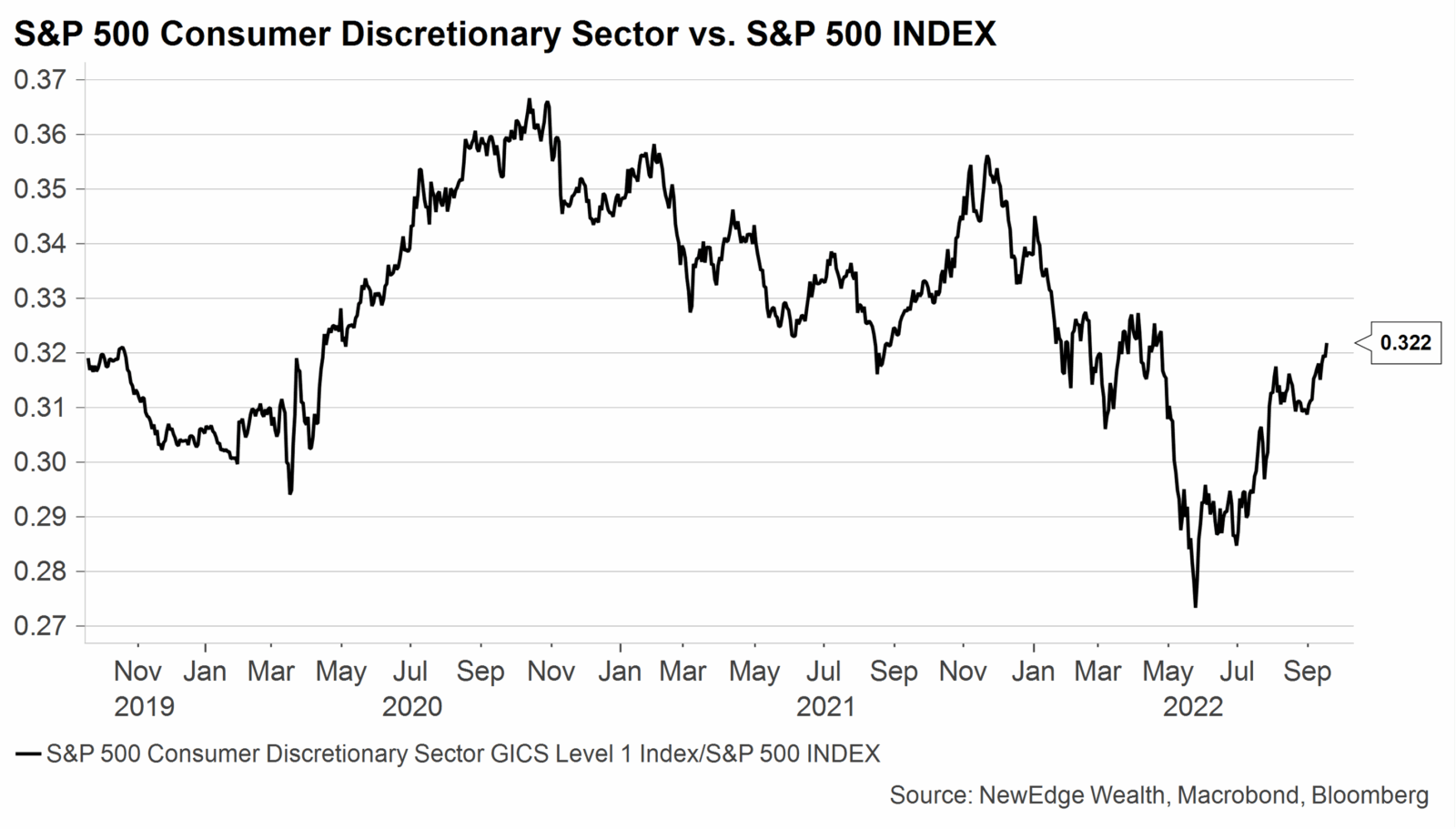

5. All is Not Bad! Surprising Strength Out of Consumer Discretionary

There are two key bright spots for this market with light/short/bearish positioning (see the full slide deck) and the relative performance of cyclical/risk-on parts of the market, like Consumer Discretionary. Usually, Discretionary outperforms in the early days of a recovery as the stocks sniff out that the worst is behind us. They are contrarian performers (good when things feel bad and bad when things feel good. Recent outperformance in Discretionary is skewed by major index weights (AMZN and TSLA are 44% of the index), however even when equally weighted, Discretionary is performing better than might be expected given news flow. Contrarians take note.

IMPORTANT DISCLOSURES

The views and opinions included in these materials belong to their author and do not necessarily reflect the views and opinions of NewEdge Capital Group, LLC.

This information is general in nature and has been prepared solely for informational and educational purposes and does not constitute an offer or a recommendation to buy or sell any particular security or to adopt any specific investment strategy.

NewEdge and its affiliates do not render advice on legal, tax and/or tax accounting matters. You should consult your personal tax and/or legal advisor to learn about any potential tax or other implications that may result from acting on a particular recommendation.

The trademarks and service marks contained herein are the property of their respective owners. Unless otherwise specifically indicated, all information with respect to any third party not affiliated with NewEdge has been provided by, and is the sole responsibility of, such third party and has not been independently verified by NewEdge, its affiliates or any other independent third party. No representation is given with respect to its accuracy or completeness, and such information and opinions may change without notice.

Investing involves risk, including possible loss of principal. Past performance is no guarantee of future results.

Any forward-looking statements or forecasts are based on assumptions and actual results are expected to vary from any such statements or forecasts. No assurance can be given that investment objectives or target returns will be achieved. Future returns may be higher or lower than the estimates presented herein.

An investment cannot be made directly in an index. Indices are unmanaged and have no fees or expenses. You can obtain information about many indices online at a variety of sources including: https://www.sec.gov/answers/indices.htm.

All data is subject to change without notice.

© 2026 NewEdge Capital Group, LLC