Introduction: A New World for a New Fed

“You give my life direction. You make everything so clear.”

Inflation has accelerated. The labor market has stabilized. And a new Federal Reserve Chair is about to step into the spotlight to deliver his assessment of the economic situation and how, if at all, monetary policy needs to adjust to it. This edition of the Weekly Edge will preview next week’s debut FOMC meeting for Kevin Warsh through the lens of rapidly changing economic circumstances.

We’ll be using REO Speedwagon’s 1984 classic, “Can’t Fight This Feeling,” to illuminate the challenge Warsh and his colleagues face in resisting the pull toward higher interest rates. The outcome of the Fed’s June meeting will probably not be nearly as dramatic as this seminal power ballad. But updated forecasts and fresh commentary will be a “candle in the window” for investors seeking clarity on the path of policy.

Welcome Back, Chairman Warsh!

“Come crashing through your door…”

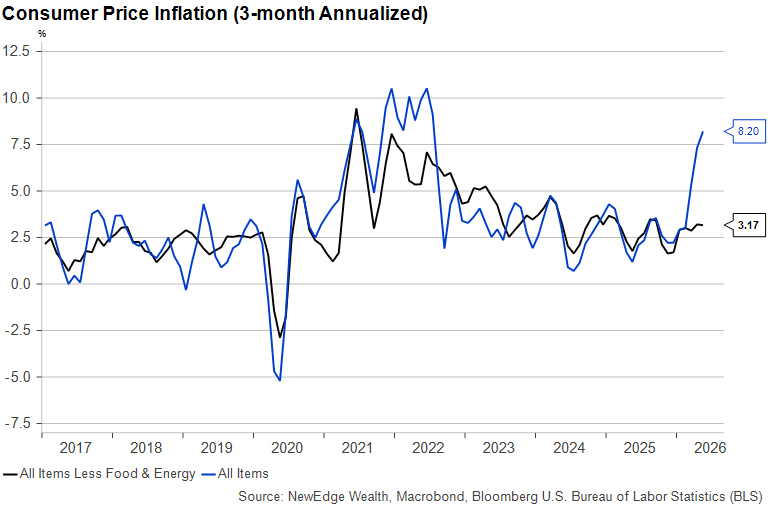

The world has changed dramatically since President Trump first named Warsh as his choice for Fed Chair back in January. While he initially indicated he favored interest rate cuts sooner than later, Warsh may have already “forgotten what he started fighting for” now that CPI inflation has annualized at an astounding 8.2% over the past three months:

As of May 2026

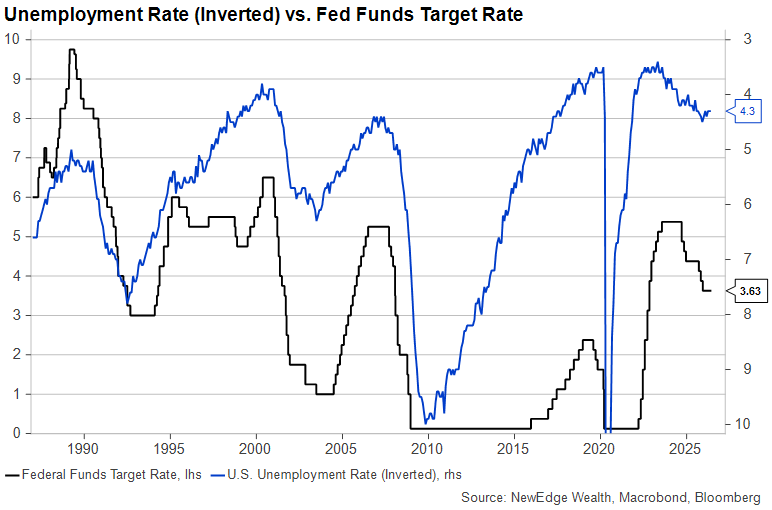

At the same time, major labor market indicators like the unemployment rate have stabilized or improved since the start of the year, reducing the urgency to provide further “insurance cuts”:

As of 6/12/26

Based on their public commentary, some of Warsh’s new colleagues are worried inflation will be persistent, while others see the Iran conflict’s effects wearing off sooner than later. To “get this ship into the shore” and achieve unanimity among what has recently been a rambunctious group of FOMC voters, Warsh will likely need to remove the longstanding bias in the Fed’s statement toward lowering interest rates. This would be a painful step for a Chair who was nominated with a clear mandate to lower rates. But rather than dissent from the majority in his first meeting, Warsh will likely allow the prevailing opinion to “take him to places that he alone would never find” and agree to a hawkish hold. If he wishes, he will have a chance to express more of his own views in the post-meeting press conference.

A Tough Job Ahead

“I’ve been running round in circles in my mind.”

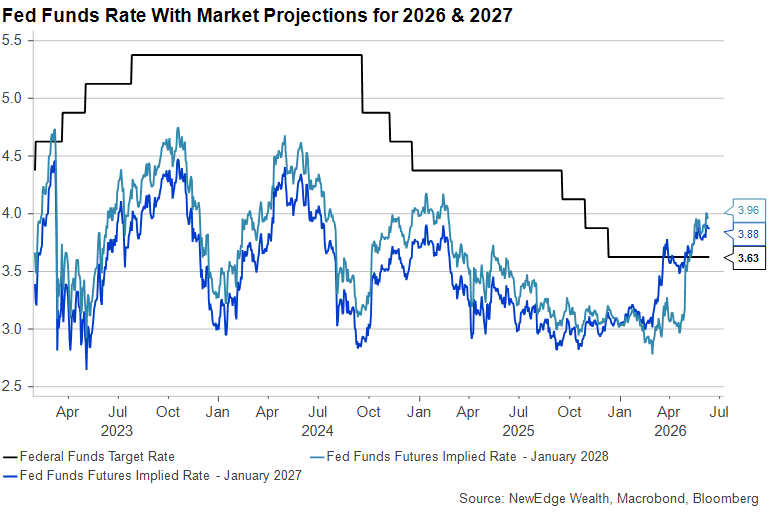

Unlike most other major central banks, the Fed has a dual mandate to keep inflation contained while promoting maximum employment. These two goals aren’t in obvious conflict today. Inflation is too high and unemployment is still low. The market has completely reversed expectations for Fed policy from “cutting” to “hiking” since the start of the Iran conflict, indicating that inflation has been the central driver for policy rate expectations:

As of 6/11/26

At the start of May, while rate cuts had been largely priced out, markets were not pricing in a substantial chance of a rate hike over any time horizon. But since then, better than expected labor market readings and small business surveys – in addition to the prolonging of the Iran conflict and its resulting upward pressure on energy prices – have caused investors to price in close to a 100% chance of a hike by December:

As of 6/11/26

December is still a long way away, and higher energy prices alone are not currently pressuring the Fed to hike rates. (Indeed, the European Central Bank’s decision to tighten policy this week may look like a policy error sooner than later.) But if energy price inflation gets worse or begins to trickle into prices of other things, the Fed will find that it “can’t hold out forever” in keeping interest rates on hold.

What to Expect from a Warsh-led Fed

“Throw away the oars forever.”

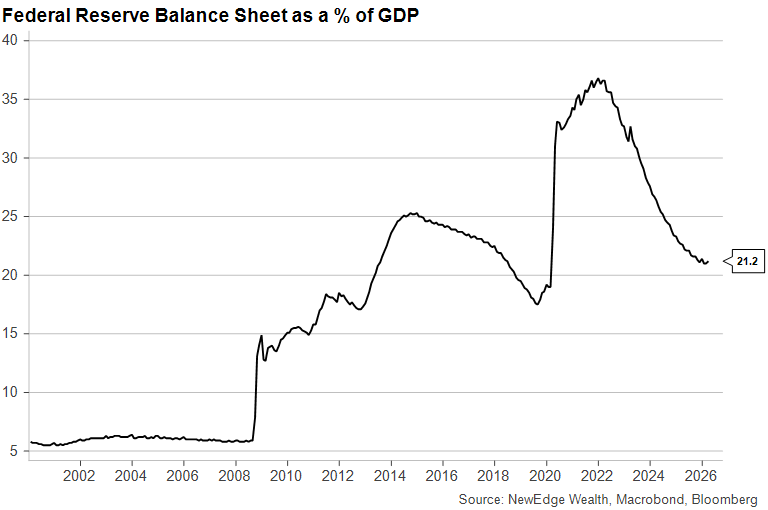

As we wrote back in February when he was first tapped for Fed Chair, Kevin Warsh comes to the Fed with a set of lofty goals, including the Fed’s presence in the bond markets, both the frequency of purchases and the size of its holdings. Up until very recently, the Fed’s balance sheet had been shrinking under the Quantitative Tightening regime, reducing the amount of liquidity in the financial system. But the Fed announced the end of that program late last year, and its portfolio remains historically large as a percentage of GDP:

As of 6/11/26

With barely a month under his belt as Chair, we aren’t expecting Warsh to make any big announcements at the June meeting. Going forward, however, we are expecting changes in a few key areas:

Forward guidance: Warsh has been critical of the Fed’s tendency in recent years to communicate the likely future path of interest rate policy. Like everyone else, the Fed has highly imperfect forecasting powers, which have often made the “dot plot” and other public predictions look wildly wrong in retrospect. We could see communications scaled back both in frequency and depth.

Greater coordination with the executive branch: Both Warsh and Secretary Scott Bessent have indicated that the Fed and Treasury (which have been working closely at least since the 2008 Financial Crisis) could see even greater collaboration on the issuance and ownership of Treasury debt.

Shrinking the balance sheet: This might be done with the Treasury’s help, but Warsh sees the ballooning Fed ownership of Treasury and mortgage-backed securities dating back to 2008 and, more recently, 2020 as warping the market. The challenge is doing this without draining financial system liquidity too much and causing another spike in short-term rates a la 2019.

Conclusion: No rate hikes…yet

“I’m getting closer than I ever thought I might”

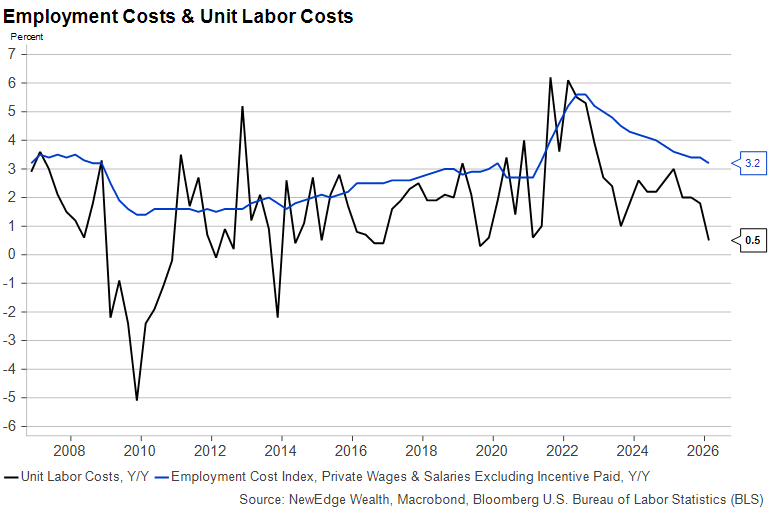

At the start of the year, we were not predicting an active summer debate over Fed rate hikes. But here we are. Fortunately, it does not appear that any members of the FOMC are anxious to raise rates right now. And while labor market data has been strong in recent months (e.g., low unemployment and solid hiring), it is not currently registering as hot. Wage growth is still decelerating and growth in unit labor costs (what employers need to pay to generate one unit of output) has been very low.

As of Q1 2026

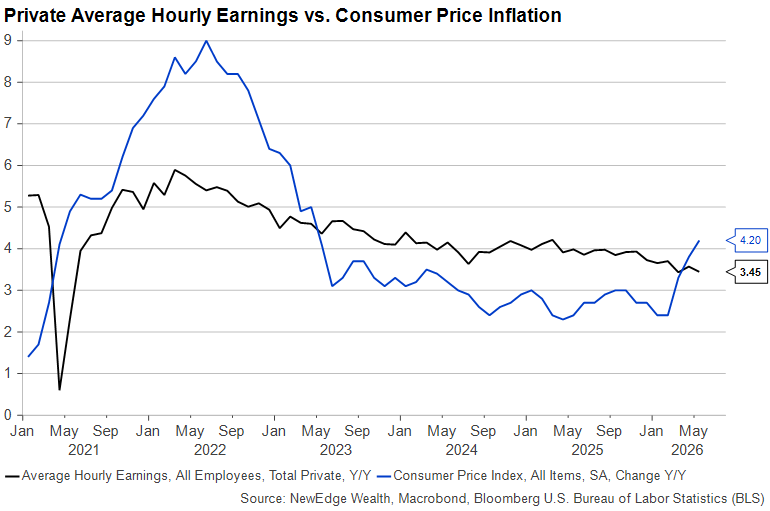

Moreover, there is no sign that the recent surge in inflation is feeding through into higher wages, meaning personal spending growth will, if anything, be weaker on a go-forward basis.

As of May 2026

This last graph may be keeping Chair Warsh up at night. Energy-led inflation is a tax on consumers and their wages. Real incomes are falling, as are personal savings rates. Tightening policy into an environment that is already set up for weaker consumption would be an ignominious way to start a tenure as head of a central bank. But Warsh and his colleagues are, like it or not, hostage to events in the Middle East and policies coming out of the White House as they search for the right direction and timing on rates.

IMPORTANT DISCLOSURES

The views and opinions included in these materials belong to their author and do not necessarily reflect the views and opinions of NewEdge Capital Group, LLC.

This information is general in nature and has been prepared solely for informational and educational purposes and does not constitute an offer or a recommendation to buy or sell any particular security or to adopt any specific investment strategy.

NewEdge and its affiliates do not render advice on legal, tax and/or tax accounting matters. You should consult your personal tax and/or legal advisor to learn about any potential tax or other implications that may result from acting on a particular recommendation.

The trademarks and service marks contained herein are the property of their respective owners. Unless otherwise specifically indicated, all information with respect to any third party not affiliated with NewEdge has been provided by, and is the sole responsibility of, such third party and has not been independently verified by NewEdge, its affiliates or any other independent third party. No representation is given with respect to its accuracy or completeness, and such information and opinions may change without notice.

Investing involves risk, including possible loss of principal. Past performance is no guarantee of future results.

Any forward-looking statements or forecasts are based on assumptions and actual results are expected to vary from any such statements or forecasts. No assurance can be given that investment objectives or target returns will be achieved. Future returns may be higher or lower than the estimates presented herein.

An investment cannot be made directly in an index. Indices are unmanaged and have no fees or expenses. You can obtain information about many indices online at a variety of sources including: https://www.sec.gov/answers/indices.htm.

All data is subject to change without notice.

© 2026 NewEdge Capital Group, LLC