Introduction – I’ve Learned to Slam on the Brake Before I Even Turn the Key

Before this week, the Federal Reserve had not released updated economic and interest rate forecasts since March 19th. That sure feels like a long time ago. While members of the central bank’s monetary policy committee (FOMC) speak publicly all the time, we finally received an update on Wednesday to their collective thinking about how the U.S. economy is performing and what measures might be needed to help keep it in balance.

If the FOMC’s March meeting seems like a distant memory, the Fed’s rate cuts in the second half of last year feel like ancient history. But those cuts, along with the environment in which they occurred and the market’s reaction to them, tell us much about both the likely timing and efficacy of policy changes in the current moment. What is the data telling the Fed to do? What else is influencing its decisions? And where might we continue to see pain for the economy while rates stay this high?

Dear Evan Hansen, a Broadway musical that opened in 2016 and was adapted into a 2021 film, has absolutely nothing to do with monetary policy. But had Fed Chair Jerome “Jay” Powell stood at the podium on Wednesday and sung the lyrics to one if the show’s signature tunes, “Waving Through a Window”, it might not have sounded that different from what he actually said. Is the Fed’s “window” for cutting interest rates about to open again? We’ll dive into the question more deeply below.

FOMC Meeting Recap: Better to Remain Silent…

Give them no reason to stare

No slipping up if you slip away

So I got nothing to share

No, I got nothing to say

The Fed delivered on expectations last week that it would hold rates steady. Its forecasts for growth and inflation continued to head, worryingly, in opposite directions, leading to a wide dispersion of views on the interest rate outlook. Market projections suggest another 100 basis points of rate cuts over the next 18 months, which would bring the federal funds target rate down close to the Fed’s 3% longer-run estimate of neutral. But the Fed itself views inflation as likely to stay higher for longer, limiting the extent to which it anticipates cutting rates through 2027.

Powell remained circumspect in his comments following the meeting. The opposing forces of higher inflation and weaker growth cloud his ability to steer policy. The Fed understandably lacks the conviction to reduce rates during a period in which most economists expect inflation readings to begin to bounce from multi-year lows.

What’s Happened to Rates Since the Fed Cut Last Year?

Step out, step out of the sun

If you keep getting burned

Step out, step out of the sun

Because you’ve learned

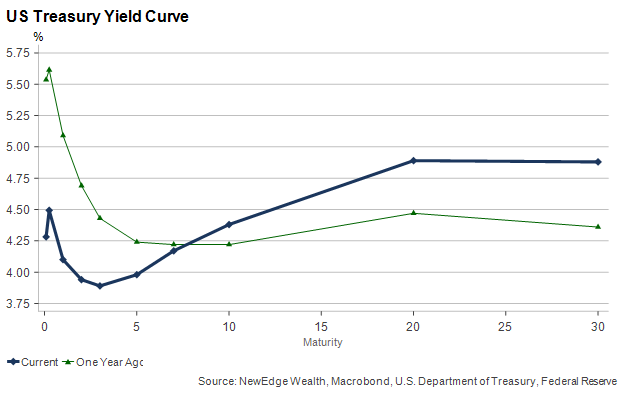

As we wrote above, the one percent drop in the federal funds target rate last year feels like it happened a century ago. That may be partly because it had no lasting effect on the interest rates investors and households care about most. The 10-year U.S. Treasury yield has actually risen by about 75 basis point since the first rate cut last September, and the average 30-year mortgage rate remains near 7%:

While it’s not unusual for the Treasury curve to steepen during a Fed easing cycle, the Zoo Steeper (bull steepening as short yields fall at the front, bear steepening as long yields rise in the back) is less a sign that monetary policy is working and more a sign that markets perceive a loss of monetary policy independence or, worse, a financial unraveling in the country.

The lesson of 2024 is that the Fed has firm control over short-term interest rates but far less control over longer-term rates. A steeper yield curve is not a sign of imminent recession, but the lack of response in longer-term yields to the large drop in cash rates is a sign investors remain skittish about owning bonds. There may not be much the Fed can do about that, but it risks losing its reputation as a powerful policymaking body if it continues to move short-term rates down without creating much if any stimulative effect on the economy.

What Does it Mean to be “Data-Dependent” in a Stagflationary Environment?

So, I wait around for an answer to appear

While I’m watch, watch, watching people pass

I’m waving through a window

The Fed’s forecasts continued to move in a stagflationary direction: higher inflation and weaker growth through next year. It’s difficult for a central bank tasked with both controlling inflation and supporting growth to know precisely what to do in such a situation except to wait for the data to send a clearer message. Let’s start with the growth data, which has been consistently falling short of expectations of late:

Even before the past week’s run of poor reports focused on housing and consumers, the labor market had returned to its softening trend dating back to 2022. Although the unemployment rate has increased by less than 1% from its cyclical low, rising unemployment claims and slowing wage growth suggest that the labor market is getting worse, not better.

For its part, inflation was notably soft in both April and May, which coupled with softer growth would seem to give the Fed a window to cut rates if it wanted to. Yet survey-based inflation expectations remain high, businesses are saying they plan to raise prices, and the sharp rise in oil prices we covered in last week’s Edge isn’t likely to help matters.

If the Fed is “looking through” the soft spring inflation months to what it knows is coming this summer, will it also “look through” the tariffs as one-off price hikes unlikely to generate self-sustaining inflation? It will likely have to, to some degree, to justify cutting rates again before the end of the year. But the Fed says it now expects core PCE inflation to remain as high as 2.4% through the end of next year, making it hard to imagine significant rate cuts are coming.

Political Pressure to Cut Rates

And no one tells you where you went wrong

The Fed has endured withering criticism from President Trump during this prolonged pause in its easing cycle. Trump seems particularly focused on the U.S. debt burden, commenting often that the Fed needs to cut rates to bring down the U.S. Treasury’s interest expense.

We believe it is correct that given the large amount of Treasury debt currently financed with short-term Treasury Bills, a series of Fed cuts would immediately ease the U.S. debt service costs. However, this is not likely to be a major consideration for the Fed, which strives to avoid the perception it is shaping policy at the behest of the president and not in service of its Congressional mandates: stable prices and maximum employment.

More importantly, as we pointed out earlier, it’s not clear that Fed cuts would make it easier for the Treasury to “term out” its debt given the likelihood that longer-term rates could rise further if the Fed is seen as tolerant of inflation. The increasing likelihood of deficit-expanding tax cuts entering 2026 may also keep long-end yields higher. Cutting rates at the wrong moment could even exacerbate the debt burden over the longer run.

The Fed is also under political pressure to cut rates to ward off a recession. Compared to last summer when rate cuts were priced in as the data turned softer, there has been almost no hint in either Fed rhetoric or market pricing in reaction to suggest rate cuts are imminent:

Significant rate cuts are most likely in the event the labor market deteriorates faster and more significantly. Short of that, given how sacredly the Fed guards its hard-earned independence, the more the Fed feels politically pressured to act, the longer it may take for the cuts to arrive.

Conclusion: Consequences of “Higher for Longer” From Here

When you’re falling in a forest and there’s nobody around

Do you ever really crash, or even make a sound?

While we wait for the Fed to cut rates in September…or December…or 2026, it’s important to observe the things that are happening – or not happening – right now because of high interest rates. The U.S. housing market remains largely closed to new buyers because of a lack of affordability. New listings and inventories are finally heading back to more normal levels, but buyers will remain scarce unless prices decline and/or interest rates fall.

In the meantime, the rising supply of existing homes is making it even less attractive to build new ones. Construction was already weak given high rates, rising input costs, and concerns about a lack of workers. But building permits fell in May to their lowest level since 2019. Even with fewer new homes, national home prices have been flattening out. That could cause existing homeowners to become more cautious consumers even as more buyers can access the market.

Economist Milton Friedman popularized the idea that interest rate changes exert pressure on economies with long and variable lags. Three years removed from the cycle’s first Fed rate hikes, his proposition is being put to the test. Lower equity market returns and plateauing home prices are predictable consequences of tight monetary policy.

For a moment last year, it seemed the Fed might be able to bring rates down significantly without a recession, but that window appears to have closed. Hoping for lower rates now is akin to hoping for higher unemployment. The two are likely to go hand in hand. For now, the Fed is still “Waving Through a Window” at investors, homebuyers and business owners hoping for a better outcome.

IMPORTANT DISCLOSURES

All data is as of June 20, 2025, unless otherwise noted.

The views and opinions included in these materials belong to their author and do not necessarily reflect the views and opinions of NewEdge Capital Group, LLC.

This information is general in nature and has been prepared solely for informational and educational purposes and does not constitute an offer or a recommendation to buy or sell any particular security or to adopt any specific investment strategy.

NewEdge and its affiliates do not render advice on legal, tax and/or tax accounting matters. You should consult your personal tax and/or legal advisor to learn about any potential tax or other implications that may result from acting on a particular recommendation.

The trademarks and service marks contained herein are the property of their respective owners. Unless otherwise specifically indicated, all information with respect to any third party not affiliated with NewEdge has been provided by, and is the sole responsibility of, such third party and has not been independently verified by NewEdge, its affiliates or any other independent third party. No representation is given with respect to its accuracy or completeness, and such information and opinions may change without notice.

Investing involves risk, including possible loss of principal. Past performance is no guarantee of future results.

Any forward-looking statements or forecasts are based on assumptions and actual results are expected to vary from any such statements or forecasts. No assurance can be given that investment objectives or target returns will be achieved. Future returns may be higher or lower than the estimates presented herein.

An investment cannot be made directly in an index. Indices are unmanaged and have no fees or expenses. You can obtain information about many indices online at a variety of sources including: https://www.sec.gov/answers/indices.htm.

All data is subject to change without notice.

© 2026 NewEdge Capital Group, LLC