Click Here to Listen to the Audio Version

I don’t get drum and bass

The future freaks me out.

“The Future Freaks Me Out”, Motion City Soundtrack

-or-

Oh please, tell me that you’re alright

Yeah, everything is alright

“Everything is Alright”, Motion City Soundtrack

Markets are in the business of discounting the future. For equity markets, most of the time that future is expected to be bright, or at least better than the recent past. After all, the history of the US equity market over the long-term shows that it increases in value 75% of time over twelve-month periods.

Occasionally, instead of being optimistic about the future, equity markets become thoroughly “freaked out” by the future (singing along to “The Future Freaks Me Out” with those slightly neurotic synth-punk-emo purveyors, Motion City Soundtrack).

There are times when this “freak out” is well warranted, such as in anticipation of a recession where earnings are expected to decline, liquidity is expected to contract, and overall risk appetite is expected to recede. Oftentimes in this scenario, prices correct first as valuations fall and then earnings/fundamental estimates are trimmed, causing the correction to be deeper and more protracted.

Then, there are times that this “freak out” is an overreaction, where prices correct far further (and faster) than what is warranted by fundamentals. Oftentimes in this scenario, prices correct first as valuations fall, but then earnings/fundamental estimates remain resilient, causing the correction to be shorter and shallower. Here, investors eventually swap Motion City Soundtrack tunes, ditching “The Future Freaks Me Out” for the closing-classic “Everything is Alright.”

This brings us to today’s “freak out” in markets. Over the last few weeks, we have seen a string of articles/anecdotes/addendums that have caused investors to grow increasingly concerned about how artificial intelligence could cause major disruptions to industries and the broader economy.

Investors have been quick to sell shares of companies at just an utterance of potential disruption from AI, but notably, this “freak out” has not yet resulted in a meaningful drop in the index level of the S&P 500, as it remains just 2% off of all-time highs (having hovered near these levels for the past four months).

This index level resilience is thanks to the pain of AI disruption losers being mostly offset by the celebration of both AI infrastructure beneficiaries and areas of the market that are deemed “safe” from AI disruption, like physical asset-intensive industries (now dubbed HALO: Heavy Asset Low Obsolescence).

Further, this “freak out” has not come with a deterioration in estimates for the US economy or corporate earnings, but instead has been driven solely by a large reset lower in valuations for AI disruption losers and reset higher in valuations for everywhere else that investors are “hiding out”. We do note that after some software reports this week that underwhelmed investors, we have started to see forward earnings estimates for some of the “disrupted” names begin to get trimmed.

But there is another layer to this market “freak out”, with more headlines this week about credit issues starting to percolate. In many ways, these credit concerns are far more pressing for markets, as they could spark a broader risk-off move vs. the “risk-swap” move we have seen with the recent leadership rotation.

So, this raises the question: what Motion City Soundtrack song should we be singing? Should we “bust a move” to “The Future Freaks Me Out”? Or, should be “be better at fighting the future” and sing “Everything is Alright”? To answer this, we will look at the AI fears, discuss the rotation in leadership and how it is supported by the current growth/data backdrop, and finish by looking at how credit fears are starting to flash risk-off warning signs.

“I’m On Fire and Now I Think I’m Ready to Bust a Move”: AI Fears

The most remarkable thing about the last few weeks of AI jump-scares is just how rapidly the viral articles (which we linked to above) have spread and how quickly investors have been to price in the potential, yet still nebulous, impacts of AI disruption into stock prices.

At first, the stock reactions were all about valuations. Look at the forward PE multiple of the Software industry dropping from 34x forward last fall to 22x forward today. A lower multiple reflects less confidence that the current run-rate of growth, sales, margins, and earnings can (or should) be extrapolated, or capitalized, into the future.

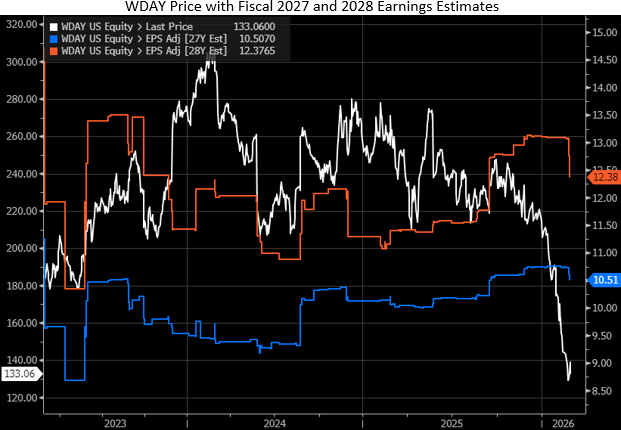

We always emphasize that price does, in fact, lead data, so seeing share prices react before fundamentals is perfectly normal. But this week, we actually began to see EPS forecast cuts for software names that reported earnings. For example, the chart below shows the earnings estimates for software company Workday (WDAY) and how they have been trimmed for calendar 2027 and 2028 (fiscal 2026 and 2027). Of course, the move in the stock is far larger than the cut in earnings estimate cuts, but, as we pointed out above, price drops reflect diminished market willingness to extrapolate today’s earnings power perpetually into the AI future.

Looking at these early estimate cuts raises an important point for the question about AI’s impact on markets versus the economy.

The AI dooms day articles (like Citrini’s) looked at both individual business and economic disruptions, but it would be reasonable to expect that business/stock-level disruptions will come far faster than potential broader economic disruptions.

It’s also becoming harder to identify whether AI-related (or supposedly AI-related) distortions will have a positive or negative impact on individual companies’ stock prices. Take this past week’s announcement from Block, a fintech firm led by former Twitter CEO, Jack Dorsey. The company announced it was laying off 40% of its workforce, given the possibilities to enhance the productivity of the remaining 60% with various AI tools. Whether truly AI-driven or simply an appreciated acknowledgment, the firm overhired in the early 2020s; this mass layoff announcement was greeted with a 16%+ rise in its share price.

In the past week alone, the prevailing market narrative has swung wildly from doom to euphoria to shrug (as seen in the weak reaction to NVDA’s blockbuster earnings) in relation to AI-exposed firms. Sometimes as investors, we must be humble enough to admit we don’t know what the impact of AI will be in the longer term or what the market reaction will be as we all discover the answers along the way. Overreacting to a single written piece or a four-day trend can cause one to miss the bigger picture. In our next section, we’ll talk about how major equity indexes have remained so resilient despite the wild swings under their surfaces.

“Oh Please, Tell Me That You’re All Right”: Macro Picture Helping Support Markets

Of course, any time there is a significant intra-market rotation, investors will tend to focus most keenly on what is happening to broad indexes like the S&P 500. And the answer there, since as far back as last October, has been “not much”. This may be hard to believe for anyone reading AI impact manifestos on X or Substack or watching individual sectors like Software lose up to a third of their value in the span of a few months.

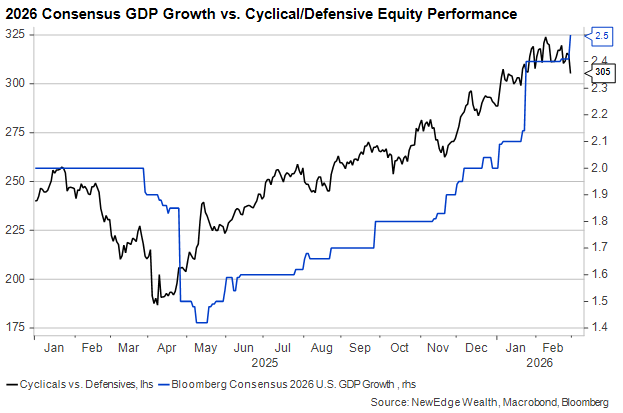

Crucially, the intra-market divergence has occurred in the context of a significant upward revision to consensus economic growth for 2026. This has allowed cyclical stocks – more exposed to economic phases but less exposed to AI – to rally, as seen in the chart below.

This upward revision to economic growth has effectively given investors the comfort to “hide out” from AI disruption in parts of the market that historically considered riskier, lower quality, and more volatile/cyclical. This is why we are calling this backdrop not a “risk-off”, but a “risk-swap” environment. If we were to see a greater weakening in the economic outlook, whether it is due to AI disruption or credit/liquidity tightening, then we do not think these cyclical areas of the market would be able to sustain their leadership (which is another reason why relative strength in defensives like Staples, Utilities, and Healthcare must also be monitored closely).

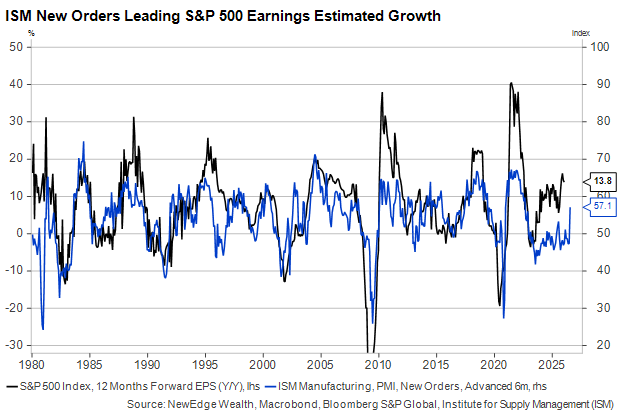

So-called “soft data” (gathered from surveys instead of measurable spending or output) has been an unreliable market timer in recent years, but the ISM Manufacturing survey’s New Orders component has a very strong track record in correctly forecasting earnings estimates:

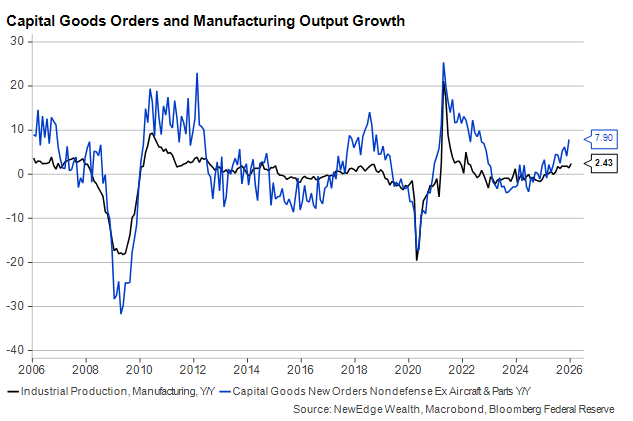

The positive vibes from business sentiment go beyond the single ISM poll and include the vast majority of regional Fed surveys taken each month. Companies are feeling better about the environment here in early 2026 for reasons that seem to have little to do with AI. Orders for capital goods have picked up, and even manufacturing output (measured in volume, not dollars) has escaped a multi-year period of stagnation:

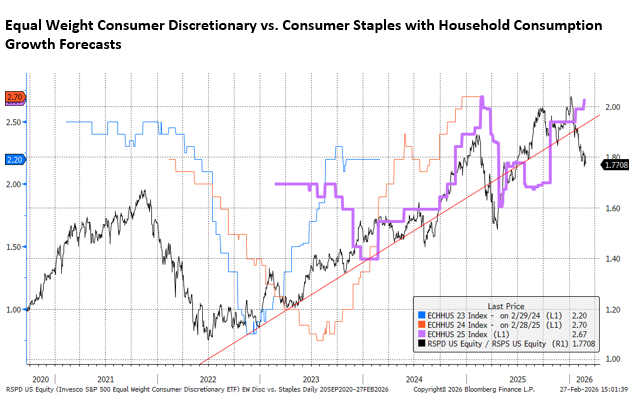

If there is one lingering concern we continue to harbor on the outlook, it is the further weakening of consumer spending growth (just 1.7% in 2025 after inflation) due to smaller wage increases and depleted household savings. Should next week’s February employment report corroborate the solid January print, it would raise the floor on just how far stocks are likely to fall should AI-related jitters remain prevalent among market participants.

As a market gut-check for consumer concerns, we continue to watch this ratio of Equal Weight Consumer Discretionary vs. Consumer Staples. It has continued to be weak to start 2026, so if we were to see signs of a downtrend begin to emerge (lower highs and lower lows), we would likely raise our concern about the outlook for the consumer.

Equal Weight Consumer Discretionary vs. Consumer Staples with Household Consumption Growth Forecasts

“I’m Sick of the Things I Do When I’m Nervous”: Taking Credit Concerns Seriously

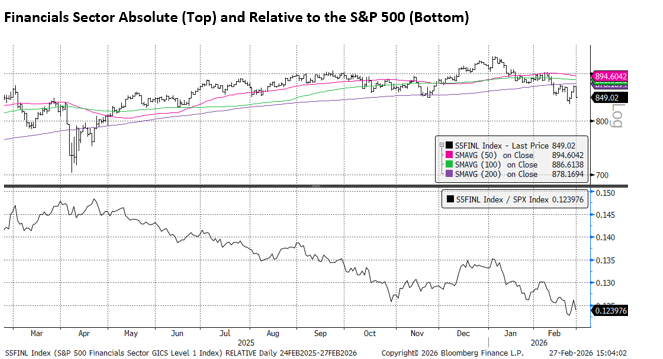

One of the factors working against the cyclical-led stock rally has been concerns about credit risk, which affects banks and diversified financial firms most acutely. The chart below shows the absolute and relative deterioration in the Financials sector (near relative lows and trading below its 200-day moving average).

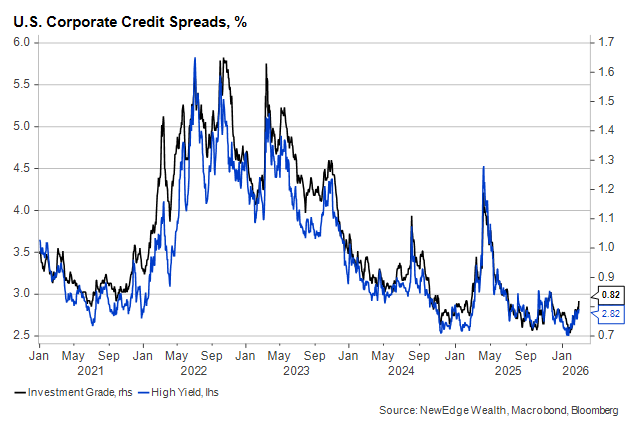

On the surface, public credit spreads are still quite tight, even if they did reach their widest points of the year last week:

But the bulk of credit concerns is coming from outside the corporate bond markets. Stocks of leading asset managers that focus on private credit have been pummeled for more than a year as investors try to mark to market these normally opaque portfolios. Strategists at UBS revised up their expected default rate on private loans to 15% for software exposure, which is enough to keep markets spooked and financial stocks under pressure.

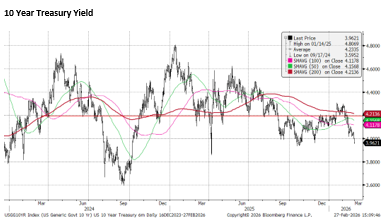

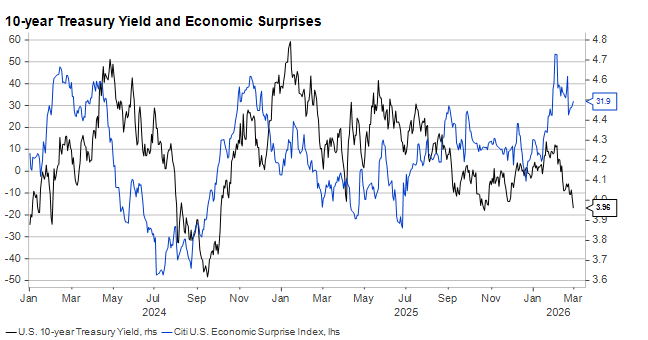

The headlines about private/illiquid credit woes continue to pile up (a smattering of the headlines from the last three days alone: here, here, here, here) and likely are contributing to the safe-haven, risk-off bid we are seeing in Treasury markets, where the 10-year has resolutely broken below 4%, as seen below.

If the Treasury market was truly contemplating an acceleration in nominal GDP growth, we doubt that we would be seeing the 10 year with a “3-handle”. But given the deterioration in credit conditions and spreads that are still historically tight, we could be seeing bond investors prefer the relative safety of Treasuries, thus pushing yields lower.

As described in the prior section, the current data does not suggest a current deterioration in the data, which makes this drop in yields/rally in bonds all the more peculiar. To see this, look at the chart below showing the divergence between economic surprises and the 10-year yield. At least from this lens, the bond market seems to be singing “The Future Freaks Me Out” even though in the present, the data suggests “Everything is Alright.”

“But I’m Getting Better at Fighting the Future”: Conclusion?

The S&P 500 is at a critical juncture as of the close on Friday. It has traded down to support at its 100-day moving average, with a break below this putting the 200 day moving average and October/November lows as the next support level.

But as has been customary for the market in 2026, this softness in the capitalization weight index stands in contrast to the relative resilience of the Equal Weight S&P 500, shown below at just a hair under new all-time highs and in a much more distinct uptrend.

This is made possible thanks to the “risk-swap” vs. “risk-off” nature of this market, where investors have rotated out of AI-disrupted names and into any area that is perceived to be relatively immune to these technological tectonic shifts. These winning areas are inherently risky themselves, but investors are taking solace in still-resilient economic data that makes having cyclical exposure more palatable.

It is this last point that reinforces why we have to watch credit woes so closely, as credit issues do have the potential to dent risk appetite and morph this “risk-swap” move into a broader “risk-off” move.

If all of this is making you feel slightly neurotic, then you will feel right at home listening to Motion City Soundtrack, and it is probably best to go ahead and listen to both songs, as both “The Future Freaks Me Out” and “Everything is Alright” appear to describe today’s market environment.

IMPORTANT DISCLOSURES

The views and opinions included in these materials belong to their author and do not necessarily reflect the views and opinions of NewEdge Capital Group, LLC.

This information is general in nature and has been prepared solely for informational and educational purposes and does not constitute an offer or a recommendation to buy or sell any particular security or to adopt any specific investment strategy.

NewEdge and its affiliates do not render advice on legal, tax and/or tax accounting matters. You should consult your personal tax and/or legal advisor to learn about any potential tax or other implications that may result from acting on a particular recommendation.

The trademarks and service marks contained herein are the property of their respective owners. Unless otherwise specifically indicated, all information with respect to any third party not affiliated with NewEdge has been provided by, and is the sole responsibility of, such third party and has not been independently verified by NewEdge, its affiliates or any other independent third party. No representation is given with respect to its accuracy or completeness, and such information and opinions may change without notice.

Investing involves risk, including possible loss of principal. Past performance is no guarantee of future results.

Any forward-looking statements or forecasts are based on assumptions and actual results are expected to vary from any such statements or forecasts. No assurance can be given that investment objectives or target returns will be achieved. Future returns may be higher or lower than the estimates presented herein.

An investment cannot be made directly in an index. Indices are unmanaged and have no fees or expenses. You can obtain information about many indices online at a variety of sources including: https://www.sec.gov/answers/indices.htm.

All data is subject to change without notice.

© 2026 NewEdge Capital Group, LLC