Introduction

2026’s bumpy start is a good reminder that when markets are priced to perfection, they can be sensitive to “imperfect” events. Geopolitical events and fast-approaching policy changes are clouding the global outlook. Concerns about fiscal sustainability are also showing up, particularly in Japan.

At the center of this market chop, there’s been a sustained and significant rise in global long-term interest rates. In this piece, we’ll lay out the likely reasons for this, the importance of changing rates in the current environment, and how worried investors should be.

Ultimately, we find the recent rise in the 10-year U.S. Treasury yield to be “overdetermined”, meaning more conditions exist than are necessary to explain it. Bond prices can fall (yields can rise) for a variety of reasons, some good and some bad, and many of these are in effect right now. We’ll round up this list of usual suspects impacting rates by referencing the 1995 classic The Usual Suspects, whose title was likely inspired by the Captain Louis Renault’s famous line in Casablanca.

New Fed Chair, New Fed Policy?

“A man can convince anyone he’s somebody else, but never himself.”

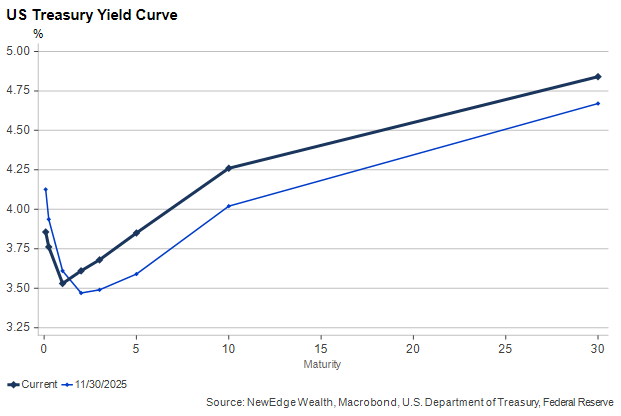

When analyzing interest rates, monetary policy is a good place to start. But while the Federal Reserve and its peers can set short-term rates with precision, they are but one of many factors driving long-term rates. The last few months of “Zoo Steepening” (falling short-term rates and rising long-term rates) demonstrates this well:

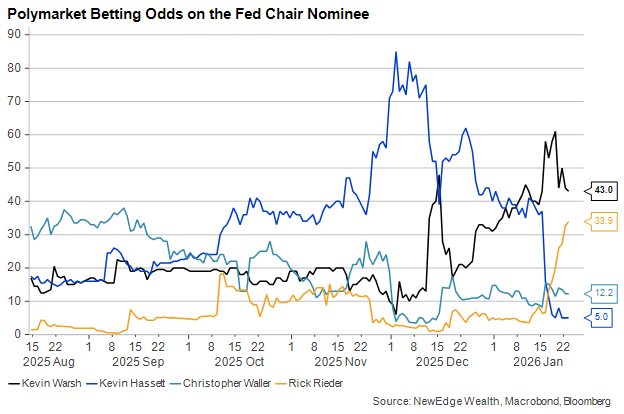

While the Federal Open Market Committee’s official bias is to cut rates again this year, the pending appointment and confirmation of a new Chair by the summer throws this view into considerable doubt. President Trump could nominate his replacement for current Chair Jay Powell as soon as next week, but the betting markets’ view of who that person will be is still swinging wildly, as it has done for the past several months:

Interestingly, the perceived odds of White House economic advisor Kevin Hassett being nominated peaked around the same time as the 10-year yield bottomed. The new most likely Chair, former Fed Governor Kevin Warsh, earned a reputation as an inflation hawk and a critic of balance sheet expansion in the years immediately following the global financial crisis. As his stock has risen, markets have been less convinced of significant rate cuts in 2026.

The Economy Simply Refuses to Crumble

“I’m telling you this guy is protected from up on high by the Prince of Darkness.”

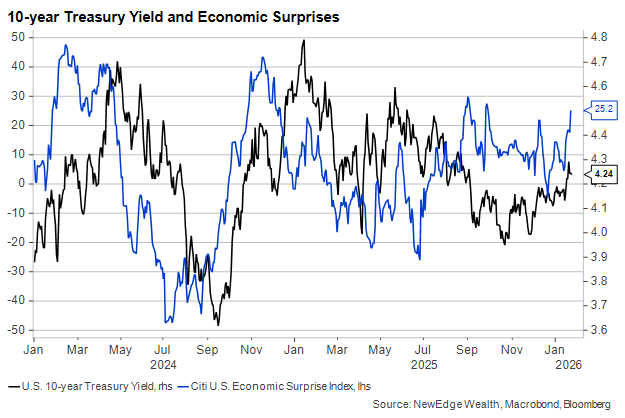

If the Federal Reserve holds dominion over changes in short-term rates, economic data typically has the largest influence on longer-term rates. The market-based interest rate for the next ten years incorporates views on both economic growth (a proxy for the opportunity cost of owning a bond versus a stock) and inflation (compensation for an expected loss in the principal’s purchasing power).

Through the onset of significant tariffs, the prolonged government shutdown, and the stalled hiring rate, the U.S. economy was impressively resilient in 2025. Data is still arriving with a considerable lag, but reports from November have come in better than expected, helping rates find a floor:

Recent data releases, including the solid consumer spending reports from October and November, have probably not been the primary driver of rates lately, but they have been good enough to permit other factors – namely broad overseas markets and U.S. policy concerns – to have a larger influence.

Japanese (Yes, Japanese) Rates are Spiking

“You will repay your debt.”

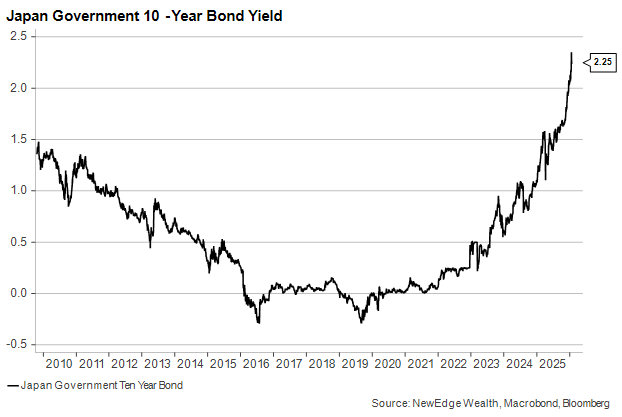

Japan’s government worked for decades to help its economy escape from a zero-interest rate liquidity trap. It’s getting results, and it’s getting them good and hard:

Japan’s bond market does not necessarily drive U.S. Treasury yields, but the most extreme moves (the 30-year JGB yield rose 27bps in a single session last week) are often the most contagious. Japan runs large budget deficits with no plan for closing them, and monetary policy is still accommodative despite gradual tightening from the Bank of Japan. The Japanese yen has lost considerable value. These moves resemble those often seen in emerging markets.

The risk to global bond markets comes not from Japanese contagion but from a domino effect in which other countries with slightly less dire fiscal imbalances experience a similar revolt from their bond vigilante at some point soon. The U.S. is not yet experiencing this phenomenon, but rates are likely already higher than they would be if the U.S. fiscal situation looked more sustainable.

Buy Greenland, Sell America?

“This whole thing was a shakedown.”

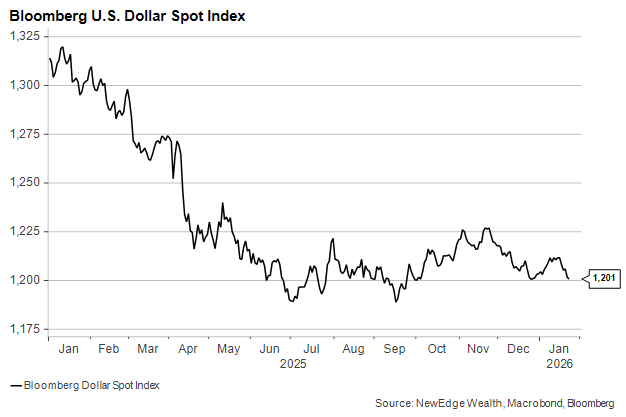

Erratic U.S. foreign policy, including yet another pointed-but-ephemeral tariff threat, drove a substantial part of last week’s interest rate volatility. The Trump administration’s attempt to obtain Greenland from Denmark using punitive tariffs as leverage has been abandoned for now. But the U.S. dollar weakness prior to the walk back resembles the price action early last year during the initial onset of tariffs:

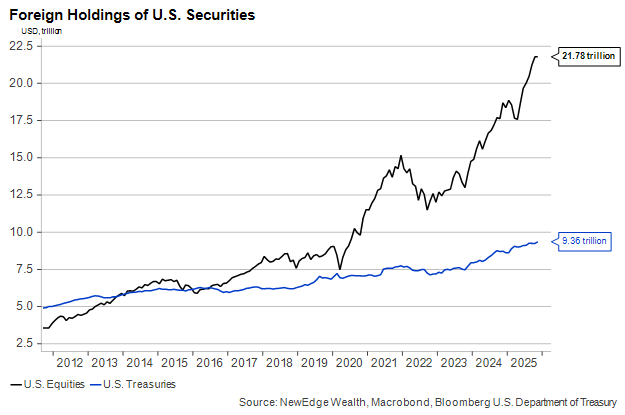

An extreme geopolitical event like the breakup of NATO would normally create a flight to safety, sending the dollar higher and Treasury yields lower. In this case, however, we saw the opposite reaction, suggesting some investors used the occasion to unload U.S. Treasuries. Note that the long-term trend has been greater foreign ownership of Treasuries, not to mention equities. International investors have not been moving out of U.S. assets, and this week’s turmoil was probably not long-lasting enough to change that:

What’s Wrong with Rates Going Up?

“The explanation is never that complicated. It’s always simple. There’s no mystery to the street.”

After years of Growth dominance, 2026 has opened with more Cyclical areas of the market in the lead. This shift is based on expectations for broader economic activity thanks to new tax incentives and falling interest rates. The tax changes have happened, but, as we wait to gauge their effect, rising interest rates will challenge housing and broader private investment.

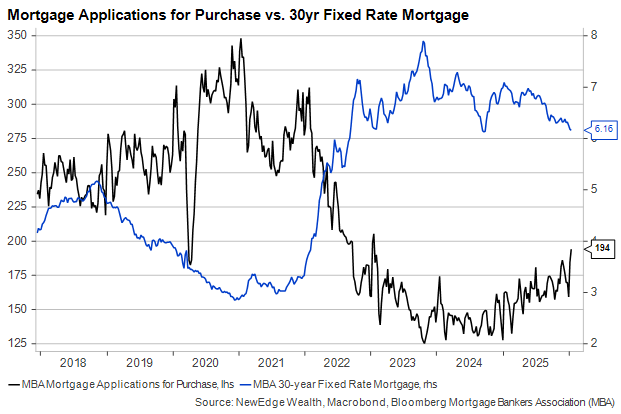

Falling mortgage rates had been encouraging more potential homebuyers to apply for mortgages throughout the second half of 2025. But with rates well off their recent lows, a burst of homebuying (or home listing) may prove elusive.

The Trump administration has rolled out several measures to help improve home affordability, including having Government-Sponsored Entities, including Fannie Mae and Freddie Mac, buy up to $200 billion in Mortgage-Backed Securities to lower spreads and bring down mortgage rates. But falling spreads won’t do much to help affordability if underlying rates are rising.

What Can Get Us Out of This?

“After that, my guess is that you’ll never hear from him again.”

After swooning on the announcement that the U.S. would be erecting more tariffs on European goods, markets cheered when that threat was pulled back scarcely a day later. This as much a signal that markets want steady economic policy as it is that policymakers will be responsive to market reactions as they roll out potential changes.

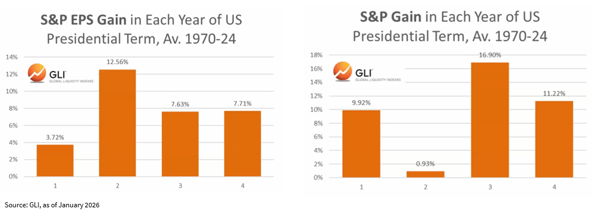

Amid erratic policymaking, strong corporate earnings and determined consumers were the two pillars of market resilience last year. The challenge to preserving those pillars in 2026 is that earnings expectations are already quite high and households’ savings rates have fallen close to all-time lows. In addition, history shows that while stimulative policies in midterm election years have generally succeeded in raising corporate profits growth, they have been less effective at generating positive market returns:

Already this year, we’ve seen several companies’ stock prices fall despite better-than-expected Q4 revenue and profits. The bar for earnings is higher – and the sensitivity to outside events is greater – when analysts already expect stronger revenue growth and expanding profit margins.

We believe stock prices need to rise further to keep consumer spending growth up. That means economic policy will need to be carried out in a predictable and generally market-friendly way while also avoiding a further steepening in the yield curve. Maintaining this delicate policy balance will not be easy. And it’s only January.

IMPORTANT DISCLOSURES

The views and opinions included in these materials belong to their author and do not necessarily reflect the views and opinions of NewEdge Capital Group, LLC.

This information is general in nature and has been prepared solely for informational and educational purposes and does not constitute an offer or a recommendation to buy or sell any particular security or to adopt any specific investment strategy.

NewEdge and its affiliates do not render advice on legal, tax and/or tax accounting matters. You should consult your personal tax and/or legal advisor to learn about any potential tax or other implications that may result from acting on a particular recommendation.

The trademarks and service marks contained herein are the property of their respective owners. Unless otherwise specifically indicated, all information with respect to any third party not affiliated with NewEdge has been provided by, and is the sole responsibility of, such third party and has not been independently verified by NewEdge, its affiliates or any other independent third party. No representation is given with respect to its accuracy or completeness, and such information and opinions may change without notice.

Investing involves risk, including possible loss of principal. Past performance is no guarantee of future results.

Any forward-looking statements or forecasts are based on assumptions and actual results are expected to vary from any such statements or forecasts. No assurance can be given that investment objectives or target returns will be achieved. Future returns may be higher or lower than the estimates presented herein.

An investment cannot be made directly in an index. Indices are unmanaged and have no fees or expenses. You can obtain information about many indices online at a variety of sources including: https://www.sec.gov/answers/indices.htm.

All data is subject to change without notice.

© 2026 NewEdge Capital Group, LLC