They Say There’s Nothing New Under the Sun. But Under the Ground…

“Hey, did you notice anything weird a minute ago?”

As we enter the final few weeks of 2025, investors have ridden a wave of optimism propelled by economic resilience and rising corporate profits. As we wrote last week, however, this bull market is beginning to look brittle. Assets tied to unprofitable entities, many of which have rallied powerfully in recent months, are off their highs, and overall market volatility is up.

On a related note, financial system liquidity looks less abundant. Banks and other financial institutions have been borrowing cash overnight from the Federal Reserve. While these volumes have not yet approached their 2020 peaks, they represent yet another tremor – along with changing market leadership and widening credit spreads – telling us to be on watch.

Tremors, the 1990 horror-comedy cult classic starring Fred Ward and Kevin Bacon, spawned a slew of direct-to-video sequels and remains a reliable late-night streaming option for monster movie fans to this day. We’ll be borrowing some of its campy dialogue to illuminate our analysis this week as we evaluate what’s happening under the surface of financial markets and what investors can focus on while they wait for the shakes to die down…or get worse.

Data Darkness Has Markets on Edge

“Who died and made you Einstein?”

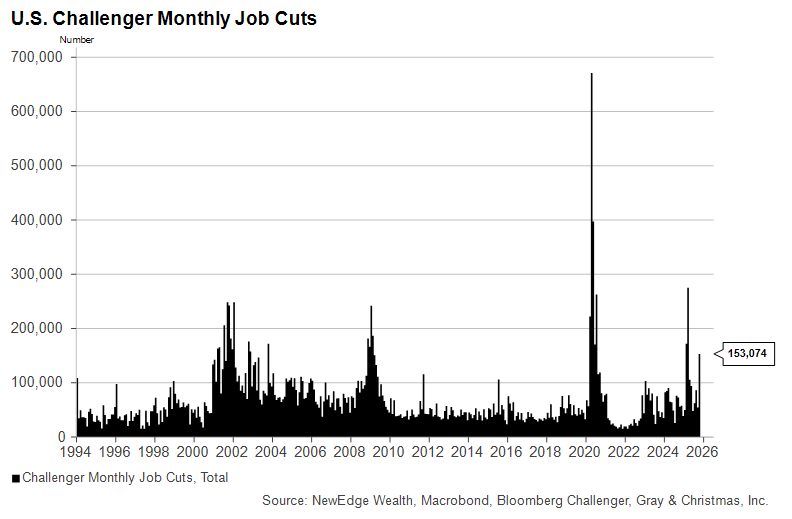

We’ll start with the state of the economy, which, honestly, is hard to gauge given that it’s been over a month since any new government data was published. Private data has generally indicated the economy has remained on its slowing trajectory since the government shut down on October 1st. But the October report on layoffs from Challenger, Gray & Christmas showed the most job cuts at this time of year since 2003:

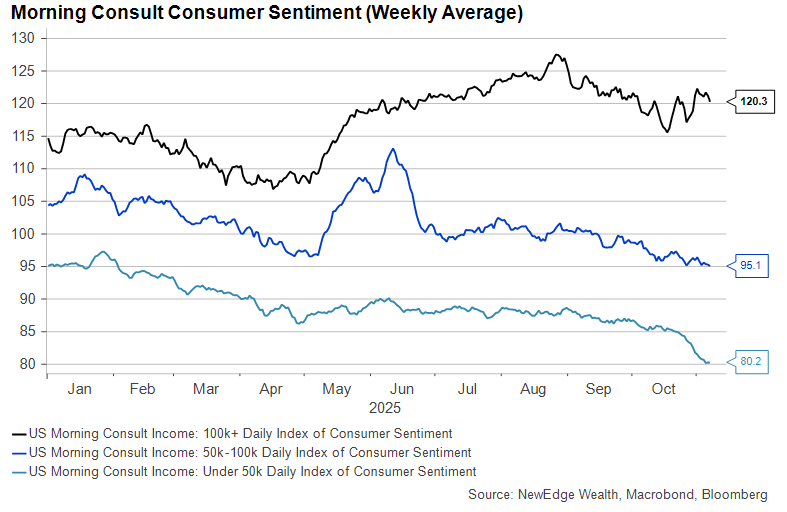

Auto sales were down in October, and both the Manufacturing and Services ISM business surveys showed that the labor market remains soft. High-frequency surveys of consumer sentiment have frayed at the lower end of the income scale, potentially related to the cessation of federal benefits connected to the shutdown.

Not all the published data has been bad. Private sector job growth turned modestly positive again in November, according to ADP, after two months of contraction. While employment remains a weak point, new orders for services firms jumped in the October ISM report, indicating demand has not fallen off a cliff. Most importantly, companies’ earnings reports have been strong for the third quarter, helping support markets. We should caveat, however, that several companies have posted better-than-expected results only to see their share prices hit. Apparently, the bar for further rewards from markets has been raised.

Markets Jittery But Not Cracking

“What the hell’s in those things, Burt?”

“A few household chemicals in the proper proportions.”

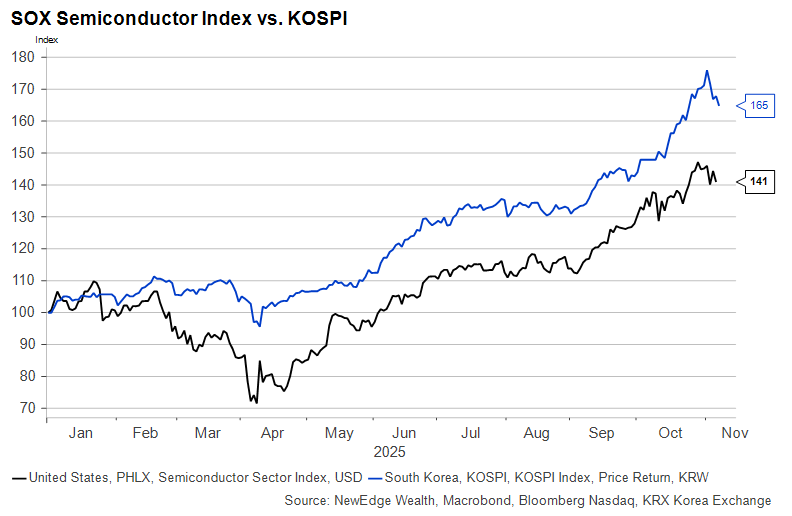

The S&P 500 continues to trade just below its all-time high, and areas of the global market that had rocketed higher over the past two months have taken a breather. Semiconductor stocks and South Korea’s KOSPI index were poster children for the late summer melt up. Their pullbacks look far less worrying in the context of their returns over the course of 2025:

Credit markets look similar. The rapid spread tightening following the Liberation Day blowout was impressive, but corporate bonds have underperformed Treasuries this quarter as spreads have blipped wider on several occasions related to trade and liquidity concerns.

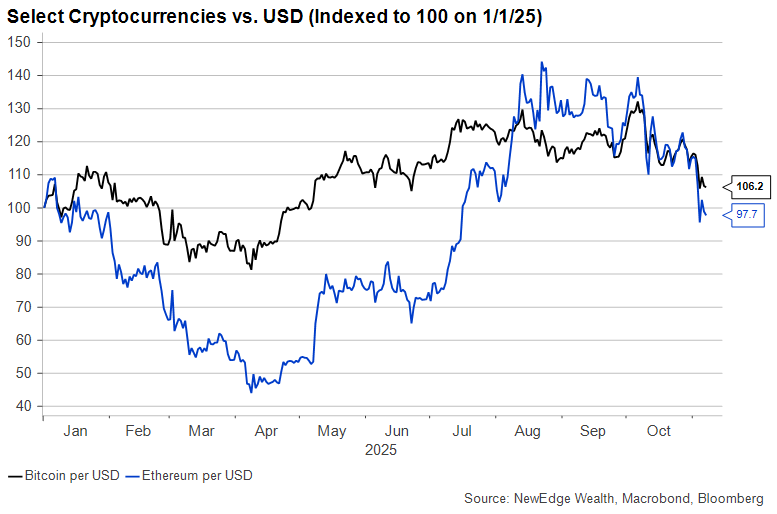

Investors in cryptocurrency have rightly come to expect considerable volatility, especially over short time horizons, in exchange for the promise of longer-term appreciation (“No, you don’t understand, these creatures are absolutely unprecedented.”) We noted over the summer that Bitcoin was failing to make new all-time highs even as other assets were breaking out. Last weekend’s significant crypto correction following a hawkish Fed meeting and concerns about liquidity (which we’ll get to below) was just the latest reminder that these assets have symmetrical price risks.

“But what if they don’t get scared, what if they don’t run?”

Investors concerned that stocks may have just passed their cycle peaks have a few reasons for optimism. Policy support is on the way in the form of the lagged effects of lower interest rates from both 2024 and the more recent cuts. Fiscal stimulus from the One Big Beautiful Bill Act (OBBBA) should hit in the first half of 2026, helping support certain segments of consumers who may currently be experiencing financial stress.

Growth in the money supply has become a quaint indicator, but it has done reasonably well at tracking the performance of non-profitable companies’ stocks. M2 growth turned positive in early 2024 and has been accelerating ever since. Another lurch higher thanks to a more dovish turn from the Fed may help sustain lofty valuations for now, preventing the kind of violent market rotation we often see at peaks.

Will the Fed Help Keep the Party Going?

“Damn it, listen to me. I’m older and wiser.”

“Yeah, well you’re half right.”

The Fed’s refusal to promise further rate cuts is likely behind some of the recent pullback in liquidity-starved assets, but it has generally moved in a market-friendly direction since the summer. Its promise to stop shrinking its balance sheet at the end of this month may help alleviate some of the stress we flagged in our introduction. There is, however, still a risk that liquidity has become too scarce, and this has historically had a negative effect on equity returns:

The question of whether rates are going much lower from here – and whether that will be helpful to liquidity conditions and overall market health – is hard to answer without a steadier data flow. Traditional “rules” governing Fed policy are all over the map. The Taylor Rule, which uses GDP growth and inflation to recommend a Fed Funds target rate, has fallen out of fashion in recent years but currently calls for rate hikes, which are obviously unlikely:

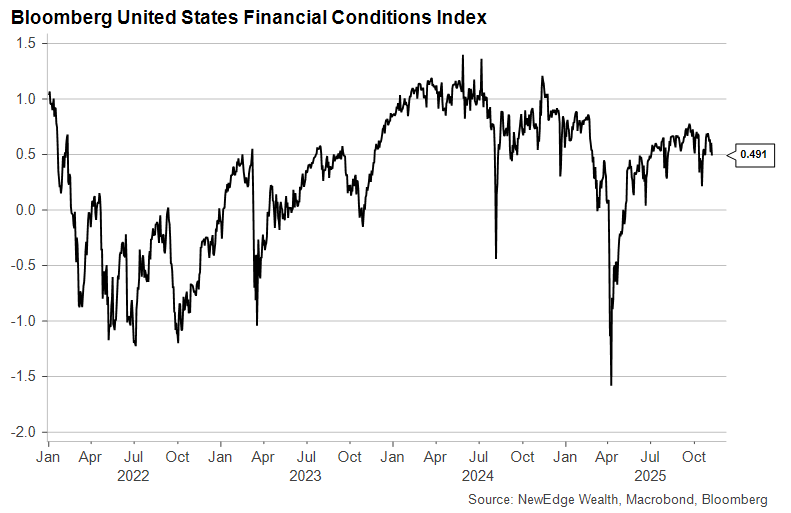

Market-based measures of financial health – the past few weeks notwithstanding – continue to suggest that conditions are quite easy overall, meaning further rate cuts may not be necessary in the absence of more solid evidence that inflation and employment are falling:

Ways to Protect Portfolios Against Tremors

“Run for it? Running’s not a plan! Running’s what you do once a plan fails!”

“See, we plan ahead. That way we don’t do anything right now.”

As we said above, we don’t see many signs that this bull market is coming to an end, but this also does not mean that the low volatility “up and to the right” price action since April will continue unabated. There are still changes investors can make to their portfolios to better position themselves. One of our key themes this quarter was that while U.S. growth stocks leveraged to A.I. investment may continue to lead, investors should consider reducing highly concentrated positions and avoiding stocks of companies with the highest valuations (often because their earnings are modest or nonexistent).

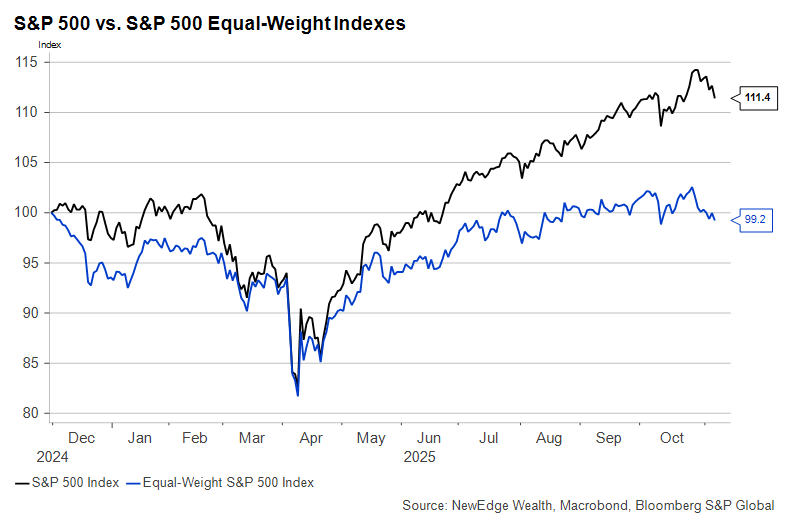

At the same time, there are risks in taking too egalitarian an approach to equity portfolio management. As the graph below shows, the equal-weighted S&P 500 Index is flat over the past year while the market-cap weighted index has soared thanks to a small handful of stocks. Some of this is due to the earnings disparity, which has also been top-heavy in 2025:

We believe the right approach to equity investing is to focus on stocks with reasonable valuations, low leverage, and durable profitability. This style, knowing broadly as “quality investing” has demonstrated an ability to add value over time. Moreover, we have found that periods when low-quality stocks have been leading the market present opportune moments to re-emphasize profitability, capital efficiency, stability in portfolios.

A second thing investors can do is find ways to better manage their cash. When short-term deposits were paying north of 5%, it was easier to justify large cash holdings. Now with rates below 4% and likely dropping further, investors can consider either holding less cash or finding cash-like investments that provide more income.

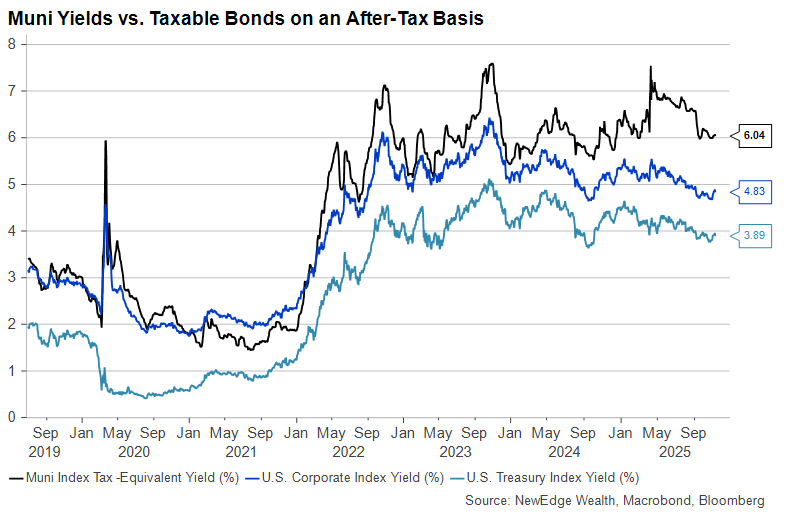

Third, we see excellent opportunities in longer-duration segments of the municipal bond market. Overall tax-equivalent yields on municipals are still north of 6%, but the steepening of the yield curve means that longer-dated bonds have cheapened the most. More importantly, correlations are returning to their pre-COVID normal. Bonds are rallying when stocks are down because broader macro concerns are affecting markets.

History shows that when tremors start to hit markets, pivoting to reasonably priced defensive assets has been a good portfolio strategy. Trimming areas that have worked well and allocating more to areas with better-forward looking returns can help to shock-proof asset allocations for the balance of the year into 2026.

IMPORTANT DISCLOSURES

The views and opinions included in these materials belong to their author and do not necessarily reflect the views and opinions of NewEdge Capital Group, LLC.

This information is general in nature and has been prepared solely for informational and educational purposes and does not constitute an offer or a recommendation to buy or sell any particular security or to adopt any specific investment strategy.

NewEdge and its affiliates do not render advice on legal, tax and/or tax accounting matters. You should consult your personal tax and/or legal advisor to learn about any potential tax or other implications that may result from acting on a particular recommendation.

The trademarks and service marks contained herein are the property of their respective owners. Unless otherwise specifically indicated, all information with respect to any third party not affiliated with NewEdge has been provided by, and is the sole responsibility of, such third party and has not been independently verified by NewEdge, its affiliates or any other independent third party. No representation is given with respect to its accuracy or completeness, and such information and opinions may change without notice.

Investing involves risk, including possible loss of principal. Past performance is no guarantee of future results.

Any forward-looking statements or forecasts are based on assumptions and actual results are expected to vary from any such statements or forecasts. No assurance can be given that investment objectives or target returns will be achieved. Future returns may be higher or lower than the estimates presented herein.

An investment cannot be made directly in an index. Indices are unmanaged and have no fees or expenses. You can obtain information about many indices online at a variety of sources including: https://www.sec.gov/answers/indices.htm.

All data is subject to change without notice.

© 2026 NewEdge Capital Group, LLC