So we keep waiting (waiting)

Waiting on the world to change

“Waiting on the World to Change” – John Mayer

Though John Mayer is currently busy being 240 feet tall at the Sphere (like a guitar-playing Stay Puft Marshmallow Man), he clearly has had the incessant underperformance of non-U.S. stocks on his mind in his solo work. His “Waiting on the World to Change” is an apt soundtrack for international investors who have experienced a decade and a half of underperformance versus the U.S. markets and are waiting for signs of a turn in performance.

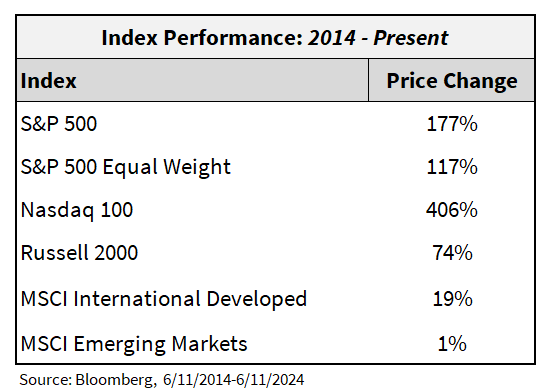

The table below paints a stark picture about the utter dominance that U.S. indices have displayed, alongside the challenges that non-U.S. markets have had in the last decade.

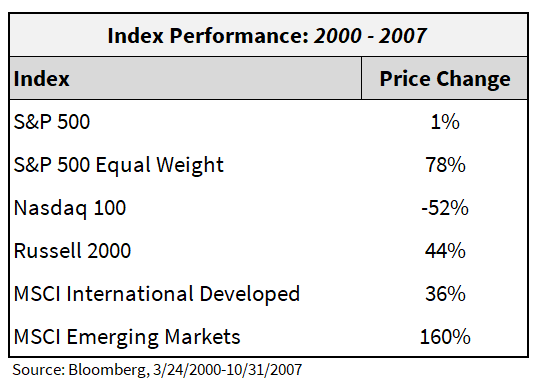

But it was not always this way. The table below shows the same indices’ performance from the peak in 2000 to the peak in 2007. You can see the leadership was reversed, with emerging markets trouncing the U.S. and its tech-heavy, Growth-sector-heavy indices, like the Nasdaq.

This early 2000s leadership was itself a rotation from the 1990s leadership, which mirrored today’s Growth and Nasdaq dominance.

The key takeaway from these tables is that, as hard as it can be to envision in the short term, secular leadership rotations do happen. These tectonic shifts often come after a market has experienced a bubble (like the Nasdaq in the 1990s or emerging markets in the 2000s), with the aftermath of the bubble causing years, and even decades (we’re looking at you, Japan) of underperformance.

This raises the question about the potential for tectonic shifts to occur again. Our conclusion is that there is not enough evidence to make the call for a massive leadership rotation away from U.S./Nasdaq/Growth/Tech into international/emerging/Value at this time. At some point we are likely to see leadership rotations, so we explore the catalysts for which we will look in order to make this call.

What You Get is What You Got: Valuation is Not a Catalyst

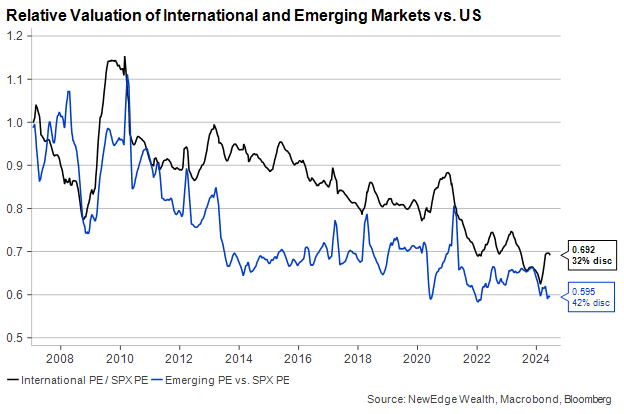

One of the greatest forecasting follies over the past decade has been to try to call the end of international and emerging markets’ underperformance due to cheap valuations. But as we often repeat, valuation is not a catalyst. Instead of valuation being the source of better return, the last decade has delivered widening valuation discounts and continued underperformance for non-U.S. markets (value traps sure are real!).

The following chart shows the relative valuation of international and emerging markets vs. the U.S. S&P 500. The last decade and a half have been unkind to these non-U.S. valuations, going from parity/premium at the peak of the 2000s cycle, to significant discounts today.

The entire way down, and most certainly over the last five years, the argument for “cheap” valuations could have been made, however the underperformance has ruthlessly continued, as shown below.

It’s Not That We Don’t Care: It’s All About Earnings

U.S. markets, though stunningly expensive compared to their international counterparts, continue to deliver superior earnings growth and earnings quality, which has been the key driver of their relative outperformance (we argue that stronger and more stable earnings growth has allowed for these higher valuations in the U.S. as well).

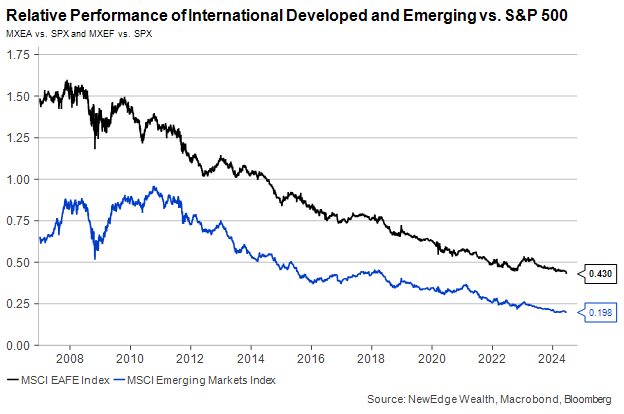

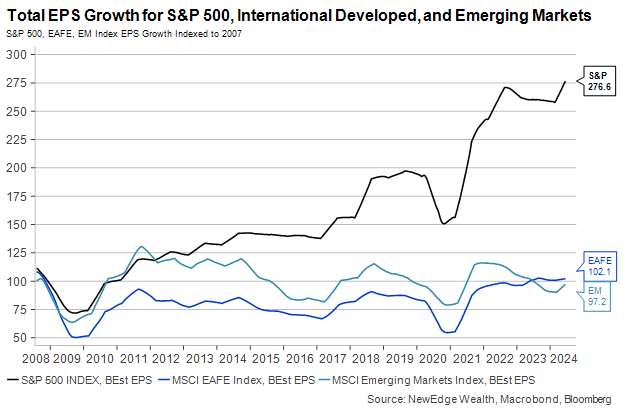

The chart below shows how, since the 2007 peak, the S&P 500 has grown its earnings per share by a total of 176%. Compare this to international developed (EAFE), which has grown its EPS by a whopping 2% since 2007, while emerging (EM) still has earnings 3% lower!

The next chart shows sales growth and is a reminder that “over earning” can be a major headwind to forward growth. Arguably, international and emerging markets “over earned”, or pulled forward demand, in the 2000’s given the boom in commodities, banking, infrastructure investment, capital flows, and more. This set the stage for lackluster growth since the 2007 peak.

These two charts are incredible in the context of the source of global GDP growth over the last decade, where the U.S. contributed 9.6% to global GDP growth, all the while emerging markets contributed 66% of global GDP growth.

This evidence should shatter popular thematic arguments from the past decade that the source of global GDP growth is a driver of markets returns. This performance is a great reminder that the market is not the economy, mostly internationally, where markets are less developed, corporate governance is lacking, and business laws can be murky/unfriendly.

There, of course, are potential exceptions to the earnings growth front going forward. For example, Japan’s substantial corporate governance reforms could drive an inflection in earnings growth and shareholder returns in the country if companies follow-through with these governance changes.

We Just Know That the Fight Ain’t Fair: Sector Weights

The lack of international and emerging earnings growth since 2007 stands in stark contrast to the powerful earnings growth experienced in the U.S. during this time.

This, of course, is a display of the incredible innovations in the U.S., the benefits of which have flowed enjoyably down to earnings thanks to the near-monopolistic and high cash/low capital-intensity nature of these dominant innovators.

This point about mega-monopoly Growth companies is important, because not all U.S. indices have been as powerful in the past decade. Look back at the first table of this piece and note the weak relative performance of small caps. The U.S. may be innovative, but it does it in a “winner takes all” way.

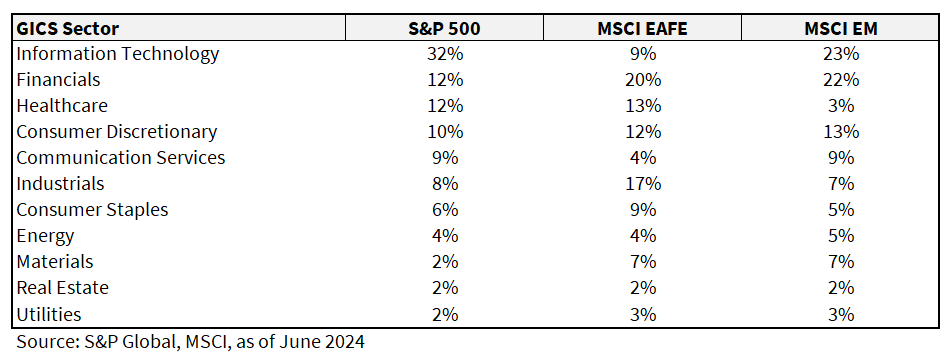

These earnings, returns, and valuation features of the indices also reflect different sector weightings in the S&P 500 versus international (EAFE) and emerging markets (EM).

The table below shows how the S&P 500 is disproportionately weighted to Technology at 30% vs. EAFE at 9%.

EM has a higher weighting to Tech at 23%, thanks to Taiwanese and Korean semiconductor companies, but these companies alone have not been able to pull the EM index higher. Note many of the large Chinese “tech” companies are classified as Communication Services (i.e., Tencent) and Consumer Discretionary (i.e., Alibaba).

The other observation from the table below is the relatively higher weighting that the EAFE and EM indices have to Value/old-economy sectors like Financials, Materials, Industrials, and Energy.

These sector weights have contributed to and perpetuated the divergence of both earnings and valuation performance in the U.S. vs. non-U.S. markets.

We Just Feel Like We Don’t Have the Means: Catalysts for Better Non-U.S. Performance

This leads us to a talk of catalysts and what could drive improved performance out of the non-U.S. indices. A reminder that we do not see enough evidence to suggest a major shift in outperformance away from the U.S. into non-U.S. markets, but we are on the lookout for signs that tectonic shifts could be happening.

We think that in order to see a major and sustained shift in leadership away from the U.S. into international and emerging markets you would need to see: a major U.S. dollar bear market, a major commodity bull market (potentially super cycle), and a significant change in the earnings generation capacity of large U.S. tech/Growth companies (possibly through regulatory/anti-trust crackdown).

The first two catalysts are intertwined. A major weakening in the U.S. dollar has historically been bullish for international and emerging stocks (major non-U.S. bull markets have only occurred during major dollar bear markets, such as in the late 1980s and the 2000s), because this weakness often coincides with capital flows leaving the U.S. and stronger commodity prices. These stronger commodity prices benefit the Value-oriented, old-economy sector weights of the non-U.S. indices.

The last catalyst about the earnings power of dominant U.S. Growth companies needs nuance versus the last Growth unwind post the 1990s Tech bubble. During the Tech bubble unwind in the 2000s, earnings growth for the nascent Tech companies was still robust, however overly concentrated positioning and astronomical valuations had to be rationalized, making the strong earnings growth a moot point.

This time around, when Growth does eventually unwind (trees can grow a lot longer than you think, but they typically stop short of the sky), we think that their monstrous cash and earnings generation will likely have to be challenged. Tech earnings were challenged briefly in 2022, but to see the kind of tectonic shifts we saw in prior international/Value cycles, we think these companies’ long run earnings potential would need to come into question (such as through regulation/anti-trust).

It’s Hard to Beat the System: Selectivity is Key

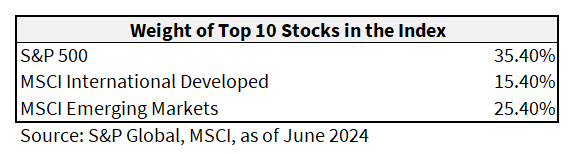

Though the catalysts for broad, rising tide lifts all boats outperformance for international indices may not be present, this does not mean that investors should eschew the asset class altogether.

The lower concentration in the non-U.S. indices, as shown in the table below, creates more opportunity for the potential to add value through stock selection.

In our own work, we also see greater dispersion between the characteristics of high and low quality names within the international indices. Avoiding low quality, highly indebted, sometimes state-owned, overly cyclical business has the potential to enhance international returns in a way that can even keep pace with U.S. indices.

Now We See Everything That’s Going Wrong: Conclusion

This piece has allowed us to “see everything that’s going wrong” with non-U.S. investing. Though we do not see evidence that the three catalysts identified (dollar weakness, commodity strength, and magnificent earnings power challenges) are present or powerful enough to cause a sustained inflection in the dominance of U.S. earnings growth/quality, and thus valuations, we continue to be on the lookout for evidence that tectonic shifts in leadership are brewing.

Eventually, one day, a bias away from the U.S. will be warranted, but that day is not today. That leaves us singing along to giant John Mayer that we are just “waiting on the world to change.”

IMPORTANT DISCLOSURES

Index Information: All returns represent total return for stated period. S&P 500 is a total return index that reflects both changes in the prices of stocks in the S&P 500 Index as well as the reinvestment of the dividend income from its underlying stocks. The NASDAQ Composite Index measures all NASDAQ domestic and international based common type stocks listed on the Nasdaq Stock Market. Russell 2000 is an index that measures the performance of the small-cap segment of the U.S. equity universe. MSCI International Developed measures equity market performance of large, developed markets not including the U.S. MSCI Emerging Markets (MSCI Emerging Mkts) measures equity market performance of emerging markets. The Nasdaq-100 is a stock market index made up of equity securities issued by 100 of the largest non-financial companies listed on the Nasdaq stock exchange. It is a modified capitalization-weighted index

The views and opinions included in these materials belong to their author and do not necessarily reflect the views and opinions of NewEdge Capital Group, LLC.

This information is general in nature and has been prepared solely for informational and educational purposes and does not constitute an offer or a recommendation to buy or sell any particular security or to adopt any specific investment strategy.

NewEdge and its affiliates do not render advice on legal, tax and/or tax accounting matters. You should consult your personal tax and/or legal advisor to learn about any potential tax or other implications that may result from acting on a particular recommendation.

The trademarks and service marks contained herein are the property of their respective owners. Unless otherwise specifically indicated, all information with respect to any third party not affiliated with NewEdge has been provided by, and is the sole responsibility of, such third party and has not been independently verified by NewEdge, its affiliates or any other independent third party. No representation is given with respect to its accuracy or completeness, and such information and opinions may change without notice.

Investing involves risk, including possible loss of principal. Past performance is no guarantee of future results.

Any forward-looking statements or forecasts are based on assumptions and actual results are expected to vary from any such statements or forecasts. No assurance can be given that investment objectives or target returns will be achieved. Future returns may be higher or lower than the estimates presented herein.

An investment cannot be made directly in an index. Indices are unmanaged and have no fees or expenses. You can obtain information about many indices online at a variety of sources including: https://www.sec.gov/answers/indices.htm.

All data is subject to change without notice.

© 2026 NewEdge Capital Group, LLC