I used to think that we were forever, ever

And I used to say, “Never say never”

“We Are Never Ever Getting Back Together”, Taylor Swift

Cameron Dawson

“I mean, this is exhausting.” -Taylor Swift and everyone who has been following financial markets

The month of April has had the tumultuous, erratic, and inane nature of a young adult relationship on the rocks. Flip flopping fights, name calling, on-again, off-again status, and exasperated proclamations of “this is it, I’ve had enough!”, all culminating in a late-night dumping of clothes (read: Treasuries and USD) out the window.

This week felt like a breakup on two fronts: first, the trading relationship between the U.S. and China on the trade front, and second, the financial relationship between U.S. financial assets and the rest of the world’s desire to hold them.

To put this two-front breakup in technical terms, the U.S. seems to be experiencing a current account war with China and a capital account war with the rest of the world (the evidence of this is still anecdotal, but we will explore more below).

The first break was sparked by the U.S. ratcheting up tariffs on China to a whopping 145% and China retaliating by raising tariffs on U.S. imports to 125% (while also saying it would ignore further increases in tariff rates and saying that the U.S. “will become a joke in the history of the world economy”).

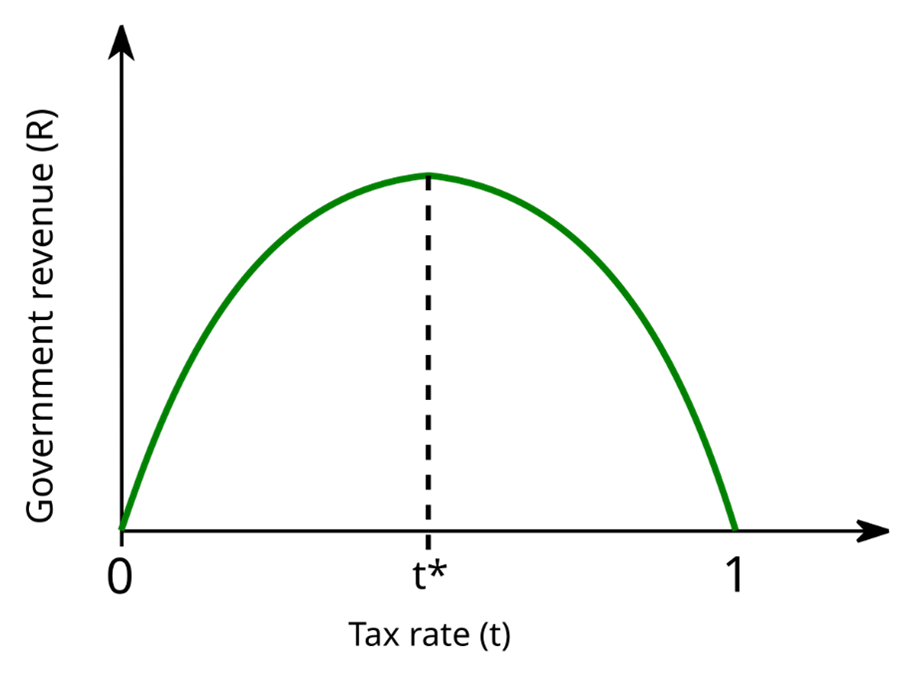

Tariff rates this high, if maintained, are likely to grind U.S.-China trade to a near halt. This limits the amount of revenue they’re likely to raise, in a classic Laffer Curve dynamic: Beyond a certain point (t* on the graph below) higher tax rates deter activity and collect diminishing amounts of revenue.

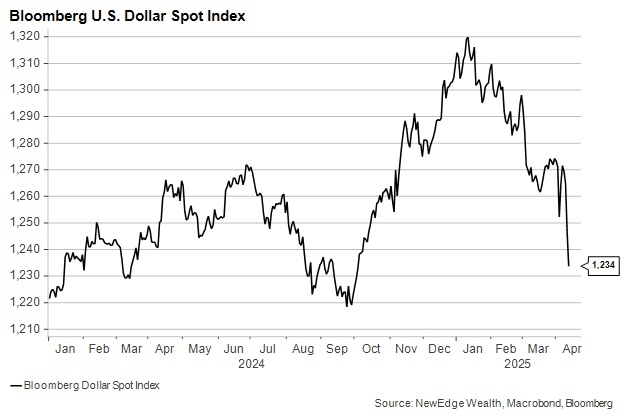

The second breakup has shown up in volatile and strained U.S. Treasuries and U.S. dollar behavior. Despite risk-off sentiment and rising recession risks, U.S.-based “safe haven” assets have not rallied as one might expect. Instead, the 10-Year Treasury yield rose 60 bps on the week (meaning bond prices fell) and the USD fell over 3%.

Why is this happening? It’s clear several markets are suffering from impaired liquidity. Municipal and corporate credit markets both “seized up” earlier in the week, and overnight moments of stress brought up memories of past Liquidity Cascades. We also see evidence that an unwind in levered hedge fund bets contributed to the bond price weakness/yield rise. However, there also appears to be, at least at the margin, less demand among foreign buyers to hold U.S. assets, judging from the concomitant selling of both Treasuries and the USD.

This second breakup raises an important point about one of the greatest challenges when assessing financial markets: discerning the difference between a short-term, temporary change in price action and the start of a long-term trend change.

Rumors and inferences of foreign investors’ fading desire for U.S. assets have filled the airwaves this week, which makes sense in the context of the poor price action and the disruption that tariff headlines have caused around the world.

But discerning between this price action being short-term and liquidity/positioning-driven, and this being the start of a prolonged “conscious uncoupling” of foreign investors and U.S. assets will take time (our favorite plant-based market analyst has incisively written about this dynamic).

As we assess this week’s “breakups”, the price action of equities both plummeting and soaring on tariff headlines raises the important point that, given the concentrated nature of tariff decision-making (entirely in the hands of President Trump), there are significant and potentially imminent two-way risks for all major asset classes. Just like turbulent young adult relationships, Trump could quickly change his mind on tariffs, and these current and capital account “breakups” could get back together (it would go something like: “I hate you, we break up, you call me, I love you“).

To better understand the dynamics and implications of these breakups, our Head of Portfolio Strategy, Brian Nick, details the China trade war and Treasury/USD sell-off below, along with an assessment of recent inflation data and the challenge of lingering resilience in hard data. He pointedly concludes by outlining the investment implications of this morass of moving parts.

Brian Nick

“I remember when we broke up the first time.” – China and the U.S. Trade Relations Implode

President Trump announced substantial changes to the tariff plan he originally unveiled on April 2. The net result is that while the average U.S. tariff rate remains close to 20%, the impact is now disproportionately on China, whose imports will now be taxed at 145%. China has retaliated by raising to the same level the rate it charges on the smaller-but-still-large basket of goods it buys from the U.S. Some orders will still move forward on essential goods with no obvious substitutes. But these prohibitive tariff rates will effectively halt trade between the world’s two largest economies. Will the U.S. and China ever, ever, ever get back together?

We remember when the U.S. and China broke up the first time back in the late 2010s. That dispute, which was incredibly disruptive to markets at the time and likely contributed to a brief manufacturing recession in 2019, now seems almost quaint, settled as it was by China’s agreement to buy more soybeans from American farmers.

This time, the stakes are far higher, and each side is beckoning their largest trading partners (“you go talk to your friends, talk to my friends, talk to me”) to strike separate agreements meant to isolate the other. This isolation is manifesting in the capital flight out of the U.S. The other side of the “shrinking trade deficits” coin is a shrinking capital account surplus. And all evidence is that the U.S.’s offensive on trade deficits is being met by a counteroffensive against the U.S. dollar and U.S. Treasuries. But that deserves its own section.

“This is it. I’ve had enough.” – International Investors

Back in September, we used our 2024 Election preview to point out the dangers of a politicized monetary policy: higher interest rates, higher inflation, and a weaker currency. Well, the Fed still has its independence, but the Trump administration’s punitive and erratic trade policy has caused a similar kind of flight from U.S. assets. On Thursday, U.S. stocks, long-term U.S. Treasuries, and the U.S. dollar all suffered significant selloffs.

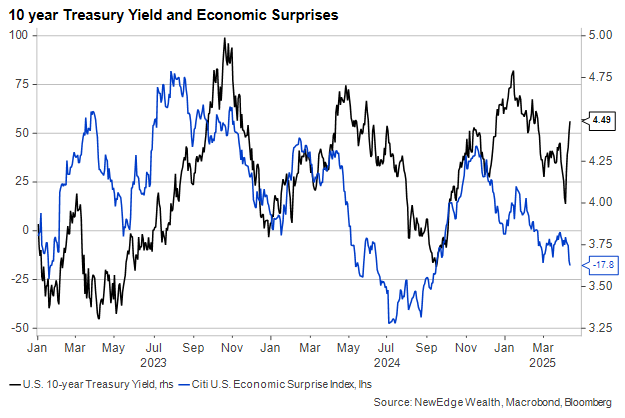

The past week’s rise in interest rates has been particularly troubling, coming amid growing calls for a U.S. recession and a surprisingly tame inflation report. This is usually a time when we see flights to quality, and U.S. Treasuries have been synonymous with quality for a century or more. But things may be changing:

It’s worth pausing to analyze just what, exactly, has been happening in the U.S. Treasury market in recent days. Short-maturity Treasury yields are down while longer-dated yields are up, a dynamic we have dubbed the “zoo steepening” in the curve with both a bull steepening at the front as short rates fall and a bear steepening at the back as long-rates rise (when yields fall, bond prices go up like in a bull market, and when yields rise, bond prices go down like in a bear market).

Front-end yields are driven by the Fed, and investors expect rate cuts in the next few months as growth slows. Longer rates are driven by, well, just about everything (growth expectations, inflation expectations, Treasury supply, demand from investors seeking safety, global monetary policy differentials, international capital flows, and more).

It troubles us to point out that the rise in longer-dated yields does not seem to reflect an increase in growth or inflation expectations but a lack of market liquidity. This is unusual for Treasuries, to say the least. The rare simultaneous rise in yields and drop in the dollar tells us that U.S. debt has become a less attractive place for overseas capital:

Treasury market liquidity is nearly always taken for granted, given the unique position of the U.S. dollar in international commerce, the U.S. Treasury’s credibility to repay the debt, and the Fed’s implicit promise to keep markets stable. The first two have come into question, while the third has yet to be tested this year. Fed speakers were notably hawkish in their rhetoric last week, which may be due to uncertainties about the tariffs’ impact on inflation as well as the institution’s desire not to be seen as politically independent.

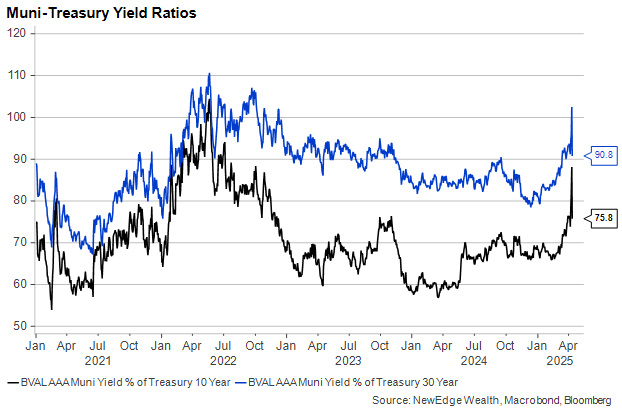

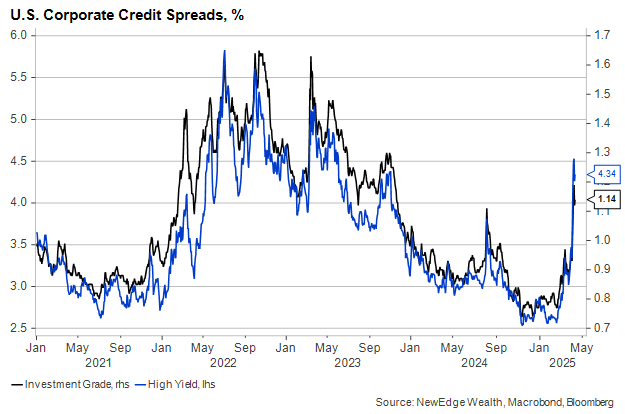

With no backstop at the moment, the recent fall in Treasury prices has, at times, been disorderly, spilling over into less liquid corporate and municipal credit markets, which had some of their worst days in recent memory in just the past several sessions. Municipal bonds, in particular, have cheapened against Treasuries and (even after their Thursday rally) offer attractive after-tax yields for investors given their very low historical default rates.

“Remember how that lasted for a day?” – Wait! Inflation was Tame in March?!

In most other weeks, a surprisingly soft U.S. inflation report would have been greeted with jubilation: stock prices up, interest rates down, and consumers feeling better about their finances. This week, though, consumer price data gave investors what they’ve been craving for years, and the response was a shrug.

Given the volatility of the past ten days, we can hardly blame them. A report that shows falling car prices feels like a fad that’s about to go out of style (Taylor’s Version). Twenty-five percent tariffs on autos and auto parts went into effect on April 3, which very likely means car prices are going up in the near future. Multiply this effect across all imported goods (most of which are taxed at 10% except those from China, which are taxed at nearly fifteen times that rate), and the March CPI report is likely to be the best inflation news we get for a long time.

“And me falling for it, screaming that I’m right.” – Data Could Get Better Before It Gets Worse

With such a sharp policy turn in such a short period of time (yes, even after President Trump delayed the so-called reciprocal tariffs this week), recent “hard” economic data is even staler than it would normally be. Even surprising strength in this spring’s retail sales or capital goods orders, should we see it, could be a misleading sign. Tariff threats clearly pulled forward many goods purchases, setting us up for weakness in the near future.

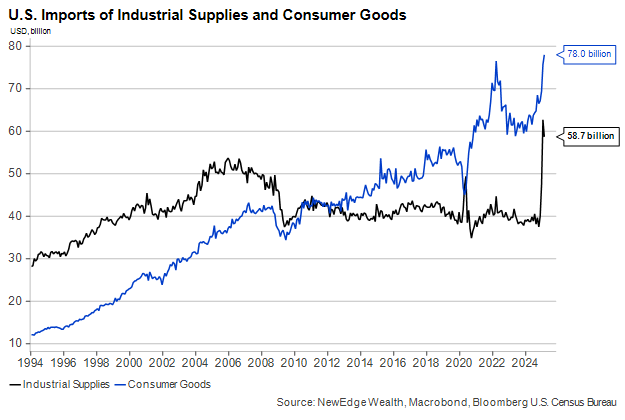

Once it became clear at the end of last year that tariffs would figure prominently into the policy mix of the new Trump administration, we warned investors to expect “lumps” in the economic data. Tariffs and other trade barriers warp economic behavior well before they ever take effect. We saw this in the surge of durable goods purchases in the final two months of 2024 and in the surge in imports in the first two months of 2025.

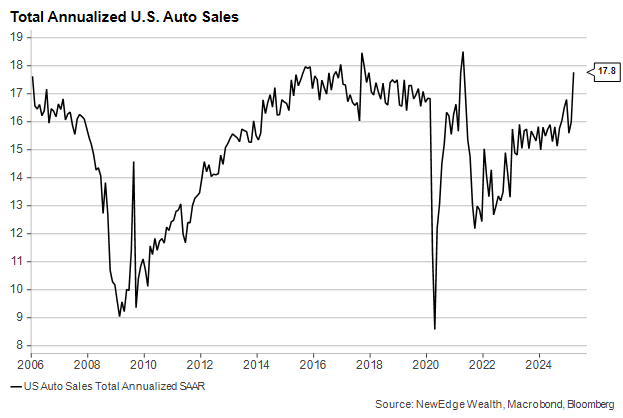

As much as consumers and businesses planned ahead wisely, as it turns out, most did not plan for the size and scope of the tariffs that have now gone into effect, let alone the sectoral tariffs on pharmaceuticals and semiconductors that have been promised. Auto sales were close to their strongest ever in March, which makes sense given the auto tariffs that began on April 3. We also see evidence of solid activity, if not a slight acceleration, in the Dallas Fed’s index of weekly economic activity, as well as the February bump in UK Industrial Production.

When trying to detect any change to the underlying economic trends this year, using a month-to-month approach will lead to misinterpretation and whiplash. Retail sales may surge in April on pre-tariff hoarding only to moderate significantly in May or June once the higher prices kick in. And with wage growth falling and inflation likely back on the rise, consumer spending on services, whose prices are not even directly affected by tariffs, may be due for a pullback, as well.

While we wait to see just how bad the bad news will get in the data, we are likely to be treated with anecdotes about small businesses quickly rerouting their supply chains or, failing that, shutting down due to the trade war. Over 40% of imports from China are capital or intermediate goods, meaning they are used by U.S. companies in their production processes. Coupled with higher steel and aluminum costs, the outlook for U.S. manufacturers has dimmed.

Consumers will begin noticing price increases, as well, especially on goods that are produced almost entirely overseas. Coffee and bananas are two of the foods likely to increase in price as a result of the 10% across-the-board tariffs, but the prices of finished goods from China, like toys and apparel, will rise more.

“Hide away and find your peace of mind.” – Conclusion

With barely a moment’s peace to reflect on the market behavior of the past several weeks and chart a path ahead, investors probably feel uncertain about how to proceed. We don’t see any need to panic, either to rapidly deploy cash into risk assets for fear of missing out (except on large down days when oversold/washed out signals flash) or to liquidate holdings as many investors seem to be doing.

Investors are being well compensated for incurring virtually every type of risk at the moment, from liquidity and credit risk to macroeconomic and earnings risks and even the risk of rising interest rates. A well-designed portfolio will seek to incorporate all these risks, but we have higher conviction at the moment that the liquidity shortage that has affected bond markets will pass, even as the grey economic clouds remain overhead to threaten stocks. We believe that this should mean we see interest rates on highly-rated bonds fall as we enter at least a moderately weaker growth environment, which should help returns on municipal bonds bounce back.

Equity positioning is more fraught as the U.S. dollar has allowed international stocks to continue their run of outperformance, while the most consistent U.S. sector of late – financials – is also one of the most at risk of cyclical slowing despite a good start to earnings season. We are sticking to our philosophy of identifying profitable companies with strong cash flows across the global market, which has a demonstrated history of outperforming in down markets while capturing most of the upside in relief rallies.

IMPORTANT DISCLOSURES

The views and opinions included in these materials belong to their author and do not necessarily reflect the views and opinions of NewEdge Capital Group, LLC.

This information is general in nature and has been prepared solely for informational and educational purposes and does not constitute an offer or a recommendation to buy or sell any particular security or to adopt any specific investment strategy.

NewEdge and its affiliates do not render advice on legal, tax and/or tax accounting matters. You should consult your personal tax and/or legal advisor to learn about any potential tax or other implications that may result from acting on a particular recommendation.

The trademarks and service marks contained herein are the property of their respective owners. Unless otherwise specifically indicated, all information with respect to any third party not affiliated with NewEdge has been provided by, and is the sole responsibility of, such third party and has not been independently verified by NewEdge, its affiliates or any other independent third party. No representation is given with respect to its accuracy or completeness, and such information and opinions may change without notice.

Investing involves risk, including possible loss of principal. Past performance is no guarantee of future results.

Any forward-looking statements or forecasts are based on assumptions and actual results are expected to vary from any such statements or forecasts. No assurance can be given that investment objectives or target returns will be achieved. Future returns may be higher or lower than the estimates presented herein.

An investment cannot be made directly in an index. Indices are unmanaged and have no fees or expenses. You can obtain information about many indices online at a variety of sources including: https://www.sec.gov/answers/indices.htm.

All data is subject to change without notice.

© 2026 NewEdge Capital Group, LLC