Read Instructions Carefully

The investing world has awoken from a two-week holiday slumber, and a new year has begun. 2025 starts, as most years do, with more questions than answers. But the outcome for the global economy and financial markets seems unusually uncertain to us. High valuations and market concentration combined with softening economic data and rising policy uncertainty mean the picture is murky, at best.

In the 1995 film Jumanji, Robin Williams’ character, Alan Parrish, spends twenty-six years inside an enchanted jungle-inspired board game and emerges with an obvious question: “What year is it?” We’ll be using his query in this edition of the Weekly Edge to draw lessons from history on what 2025 might have in store, examining four previous calendar years for clues.

2022: “Guide gets lost, lose one turn.”

In 2022, policy errors and geopolitical calamities created the worst environment for diversified portfolios in decades. Those circumstances were somewhat unique: the post-Covid reopening, Russia’s invasion of Ukraine, snarled supply chains, and trillions in fiscal stimulus all contributed to spiking inflation and forced global central banks to tighten policy quickly.

The chief lesson for investors from 2022 is that there are very few assets that perform well when monetary policy is struggling to catch up to inflation. This is why markets remain so sensitive to inflation data and why the Fed’s reaction function to potentially inflationary policies from the incoming Trump administration is so important.

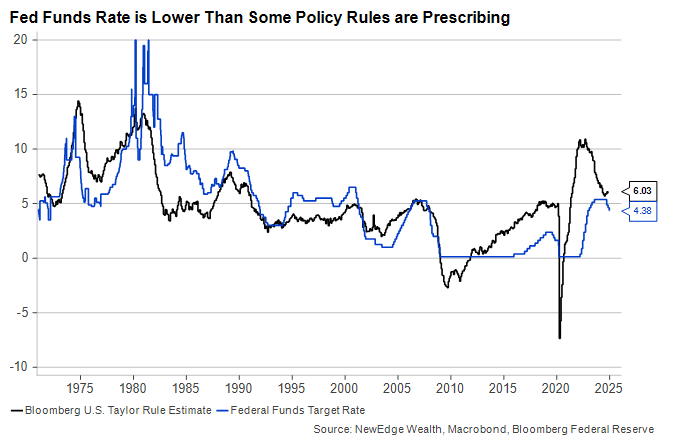

Is there reason to worry that inflation will menace markets again in 2025? Yes, but not as much as there was (with the benefit of hindsight, clearly) in 2022. Fed policy looks only slightly accommodative compared to classic benchmarks like the Taylor Rule, a monetary policy framework that suggests how central banks should adjust interest rates in response to economic activity and inflation:

As the graph above shows, policy was much more out of step with reality coming into 2022 than it is today. And leading indicators of inflation like current rents, labor market conditions and consumer expectations are all flashing green, betraying little hint of building price pressures.

It’s a good thing we’re not worried about inflation this year because positioning for it is difficult. Holding cash works well when inflation is rising quickly because the rates on short-maturity instruments adjust quickly.

Stocks might beat bonds if inflation and rates rise this year, but nearly all asset classes will struggle to produce positive returns in such a scenario. If investors perceive that high or rising rates will lead to slower growth – as they did in 2022 – equity valuations could come under significant pressure.

2000: “Beware of the ground on which you stand; the floor is quicker than the sand.”

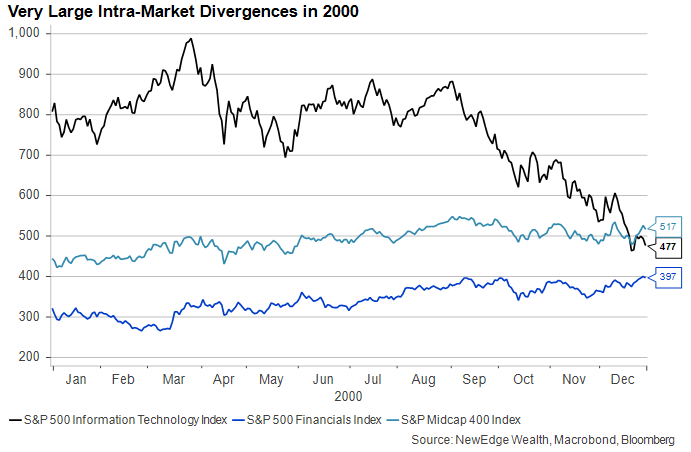

High stock market valuations driven by a small number of companies and sectors inevitably recall the technology boom and bust of the late 1990s and early 2000s. 2000 was a pivotal year for stocks, with the S&P 500 hitting an all-time high in September before entering a multi-year bear market.

Even before that peak, however, tectonic shifts in the underlying market leadership were taking place. The S&P 500 Technology sector peaked in March, six months before the market, but its initial plunge did little to roil nascent rallies in financials or even mid-cap stocks, both of which finished 2000 with healthy gains:

We don’t expect anything as calamitous as the Tech Wreck to befall the U.S. equity market or, more pointedly, the so-called “Magnificent 7” stocks that dominate the tech and consumer market caps. However, momentum has taken the valuations of many growth stocks to extreme levels, just as we saw in the late 1990s.

Investors who have been benchmarking to the S&P 500 may find that they have become overly concentrated in a handful of stocks. Making a timing call on a reversal in market leadership is perilous, but history suggests that winds can shift even without a big change to the macro environment. Broader equity market exposure will be an asset to portfolios in 2025 if we get even a whiff of the dynamics that took hold in 2000.

1996: “In the jungle, you must wait until the dice read 5 or 8.”

Of course, the extreme equity market valuations of 2000 required a torrid run of market performance that began in the mid-1990s. If we are, indeed, closer to the middle of a run like that than the end of it as we enter 2025, this year could feel like a replay of the last two: unexpectedly strong growth, high interest rates, and excellent but concentrated stock returns. That doesn’t sound awful. But there are costs to being “stuck” in one place, as Alan Parrish learned when this roll got him sucked into Jumanji for the next few decades.

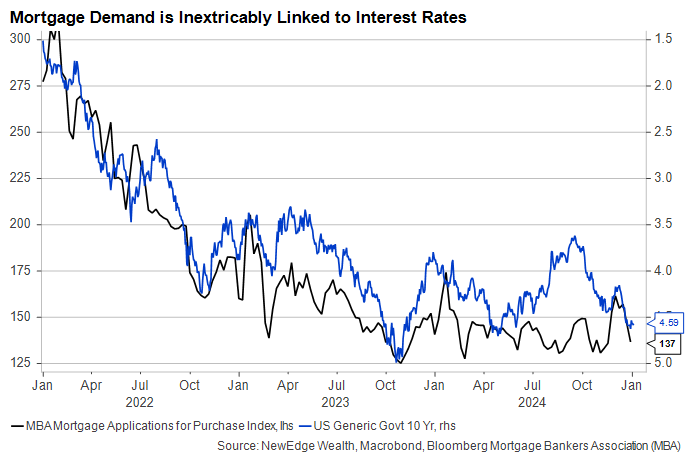

In this case, the “5” and “8” could be the mortgage rates necessary to kick-start the cycle (falling to 5%) into a higher gear with better market breadth or to tip us firmly into recession (rising to 8%) should conditions tighten again. With rates now in the low 7s, demand for mortgages has all but dried up again, and home sales – and the economic activity that tends to follow them – will be weak for the foreseeable future.

While equity investors have reaped the benefits of speculative behavior in a small number of market segments, large swaths of the broader economy are creaking under the weight of higher-than-expected interest rates.

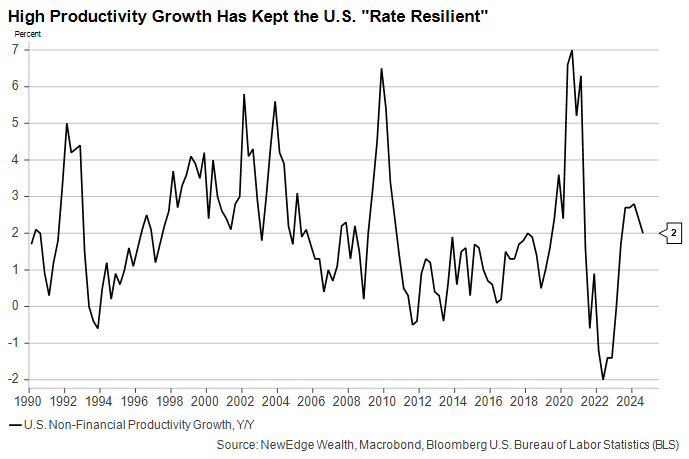

Better worker productivity mitigated the effect of high rates in the 1990s and helped us avoid recession in 2023 and 2024. But productivity growth has already begun to decelerate over the past several quarters, which could lead to slower real GDP growth and higher wage costs.

Companies with high secular earnings growth – the ones concentrated at the top of the index – are probably best-positioned for a repeat of the mid-cycle period of the late 1990s. For everyone else, it could be another frustrating year.

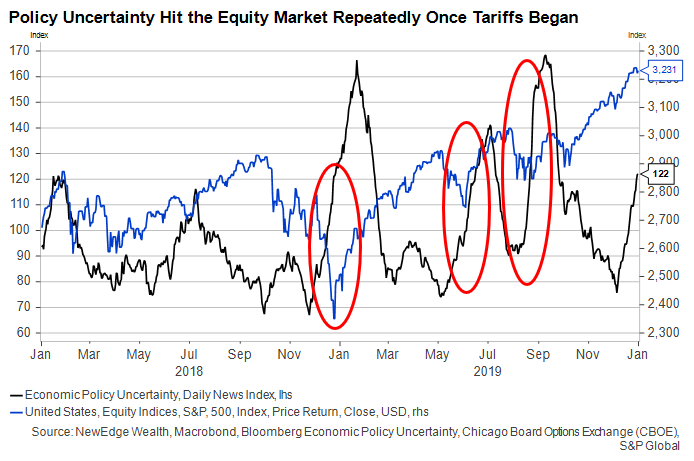

2018: “You’re almost there with much at stake; now the ground begins to shake.”

We haven’t necessarily saved the best for last, but a return to the volatile and uncertain conditions that prevailed in 2018 might, of the four, mostly closely resemble what we get in 2025. Trade-related uncertainty, in particular, could lead to volatility across markets if and when new policies are announced.

There are key differences, of course. While 2018 came on the heels of a major fiscal expansion and during a period of monetary tightening, this year arrives as short-term interest rates have begun to fall, and Congress and the new administration must pass a bill to avoid massive fiscal tightening by the end of the year. The narrow Republican majority in the House may be a source of periodic policy uncertainty.

Valuations are also higher today than they were heading into 2018 (12-month forward price-to-earnings ratio of 21.8 vs. 18.3), but interest rates are, as well. The “almost” bear market (a 19.8% S&P 500 correction) that eventually arrived in Q4 came with a swoon in interest rates that helped diversified portfolios amid policy and economic uncertainty. When policy uncertainty is high and growth is under threat, the correlation between stocks and bonds tends to move strongly negative.

Reaching the Golden City in 2025

Of course, investing is not a board game. There is no final moment of glory (“JUMANJI!”) when success is ensured and riches can be collected. We’ve identified some key risks – inflation concerns, concentrated markets, policy challenges – and examined years in which each of them affected market outcomes to provide lessons about how best to position portfolios.

As we move forward in 2025, new and unexpected pitfalls will emerge, but history will remain an important guide as we manage portfolios and provide ongoing commentary about the state of the world.

IMPORTANT DISCLOSURES

The views and opinions included in these materials belong to their author and do not necessarily reflect the views and opinions of NewEdge Capital Group, LLC.

This information is general in nature and has been prepared solely for informational and educational purposes and does not constitute an offer or a recommendation to buy or sell any particular security or to adopt any specific investment strategy.

NewEdge and its affiliates do not render advice on legal, tax and/or tax accounting matters. You should consult your personal tax and/or legal advisor to learn about any potential tax or other implications that may result from acting on a particular recommendation.

The trademarks and service marks contained herein are the property of their respective owners. Unless otherwise specifically indicated, all information with respect to any third party not affiliated with NewEdge has been provided by, and is the sole responsibility of, such third party and has not been independently verified by NewEdge, its affiliates or any other independent third party. No representation is given with respect to its accuracy or completeness, and such information and opinions may change without notice.

Investing involves risk, including possible loss of principal. Past performance is no guarantee of future results.

Any forward-looking statements or forecasts are based on assumptions and actual results are expected to vary from any such statements or forecasts. No assurance can be given that investment objectives or target returns will be achieved. Future returns may be higher or lower than the estimates presented herein.

An investment cannot be made directly in an index. Indices are unmanaged and have no fees or expenses. You can obtain information about many indices online at a variety of sources including: https://www.sec.gov/answers/indices.htm.

All data is subject to change without notice.

© 2026 NewEdge Capital Group, LLC