As we approach the end of another year, navigating an ever-evolving financial landscape, this whitepaper serves as a comprehensive guide to strategic year-end planning, offering insights, considerations, and expert perspectives to empower individuals, families, and businesses in optimizing their financial outcomes. Now is the time to take stock and assess whether your wealth strategy utilizes the appropriate methods to address the current tax law, volatile market, and any changes to your goals or family circumstances.

The tax landscape for 2023 was influenced by both recently implemented and well-established regulations. Particularly noteworthy was the impact of the year-end funding legislation, the SECURE 2.0 Act, which ushered in significant modifications to various retirement provisions. Moreover, the Inflation Reduction Act from the preceding year introduced incentives for green energy, encouraging investments in electric vehicles and home improvements. The notable inflation surge from the previous year resulted in substantial adjustments to income tax brackets and other inflation-related measures. Furthermore, what once felt distant is now becoming a reality, as we are approaching nearly two years until the expiration of the provisions outlined in the Tax Cuts and Jobs Act (TCJA).

While the deadline for implementing most strategies is December 31, 2023, due to the last-minute rush around the holidays, we anticipate a high volume of requests from clients, and you can expect your attorneys and accountants to be inundated with requests as well. If you require any year-end planning needs, please reach out to a member of your NewEdge team today to discuss your personal situation as soon as possible.

Investment and Income Tax Considerations

- Review your portfolio and rebalance if needed, aligning your investment objective with any changes to your wealth strategy goals.

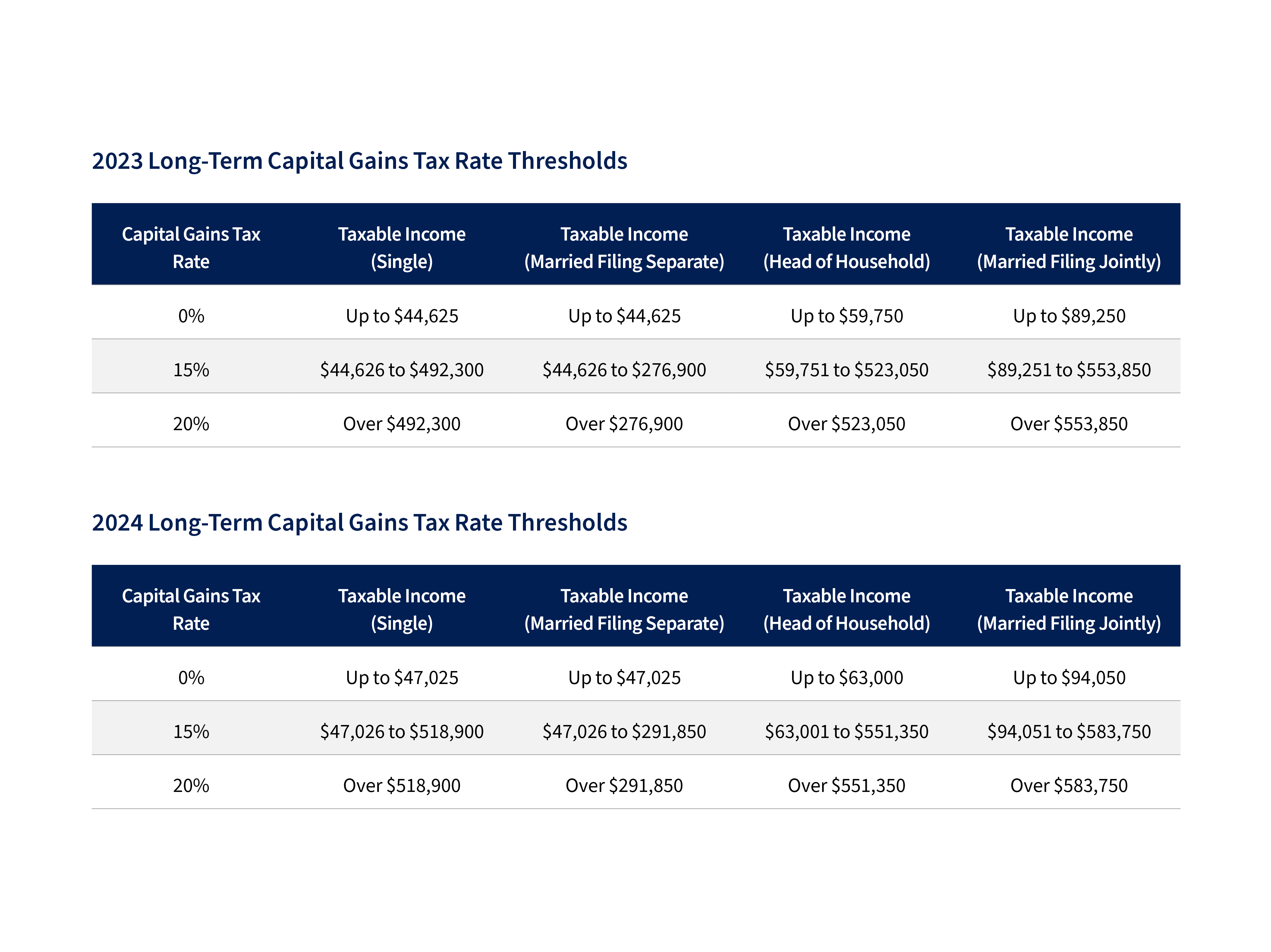

- Determine your capital gains tax rate and whether adjusting the timing of recognizing long-term capital gains makes sense. For example, if you have a highly concentrated position and are currently in a lower tax bracket, it may make sense to make additional sales in 2023. While tax brackets are not set to change in 2024, they are adjusted for inflation annually.

- Manage income tax brackets and consider accelerating income into years when you expect taxes to be lower. Review plans to sell assets, other than publicly traded securities, on an installment basis. Installment sales could result in deferring gains into higher income tax brackets.

- Tax-loss selling. Given the extent to which fixed income and REITs have declined this year, tax loss harvesting may be a practical but meaningful planning opportunity for investors holding positions with unrealized losses in taxable accounts. By tax loss harvesting now, there is the possibility of completing an additional round of loss harvesting prior to year-end should markets fall further. If your capital losses exceed your capital gains, you may use up to $3,000 in additional capital losses to reduce other types of taxable income and carry forward the remainder indefinitely.

- Avoid wash-sales. When tax-loss selling, it is important to be mindful of the wash-sale rules. A wash-sale occurs when you sell an asset for a loss and then repurchase a substantially similar asset within 30 days. In the case of a wash sale, the IRS prevents the taxpayer from taking the tax deduction for the security sold.

- Mitigate trust income tax and avoid the Medicare surtax with income tax planning. Medicare surtax of 3.8 percent is imposed on certain types of unearned income of individuals, trusts, and estates with income above specific thresholds. Non-grantor trusts should carefully evaluate beneficiaries’ circumstances and tax situations when considering making income distributions to beneficiaries. Trust beneficiaries may be taxed at a lower rate, especially due to the compressed income tax brackets applicable to non-grantor trusts. Additionally, a complex, non-grantor trust with an undistributed annual income of more than $14,250 in 2023 will be subject to the 3.8 percent Medicare surtax. However, some or all of the Medicare surtax may be avoided by distributing such income directly to beneficiaries who are below the individual net investment income threshold amount ($200,000 for single taxpayers, $250,000 for married couples filing jointly, and $125,000 for married individuals filing separately).

- SALT deduction cap workaround. The Tax Cuts and Jobs Act (TCJA) made significant changes to the federal income tax, including limiting the state and local tax deduction (the SALT deduction) to $10,000 for jointly filing taxpayers, unmarried taxpayers, and trusts. In response to the cap on the SALT deduction, many states began to allow qualifying entities required to file tax returns within the state to make an election to pay a pass-through entity tax (PTET), as opposed to the income tax being passed through to the individuals who own the entity. Owners of a pass-through entity can elect to pay tax at the entity level with a corresponding proportionate share of the PTET being claimed as a credit at the individual partner, member, or shareholder level for federal income tax purposes. The deadline to make this election differs by each state.

- Consider state income tax deductions for contributions to 529 plans. However, be aware that this counts towards your $17,000 annual exclusion gift per recipient. Depending on your situation, it may make sense to gift other assets to the recipient and pay tuition to the institution directly.

- Bonus Depreciation. In 2023, businesses have the option to deduct 80 percent of the cost basis of qualified property (computers or equipment, land improvements, and qualified improvement property) in service, with the percentage decreasing to 60 percent in 2024. Any portion of the cost basis not eligible for bonus depreciation will be subject to normal depreciation using normal lives and methods. If you anticipate a need for any of the mentioned assets in 2024, it is advisable to acquire and put them into service before the end of 2023. Factor in potential changes to tax rates in 2024 and assess how net operating losses might impact your tax planning. Regardless of bonus depreciation considerations, it is prudent to consult with your tax professional about any assets acquired in the current year. Additionally, discuss any ongoing or contemplated asset acquisitions for 2024; it may be strategic to expedite acquisitions into 2023 or defer them to 2024.

Align Your Estate Plan With Your Goals and Aspirations

- Review and reconfirm that your foundational estate planning documents are executed and up to date, including a review of asset titling and beneficiary designations. It is important to revise these documents as your life and priorities change.

- Meet with the NewEdge Wealth team to revisit your cash flow and the projected growth of your taxable estate to reconfirm or implement a wealth transfer strategy for both your personal and business assets.

- Review insurance coverage and reevaluate whether it is owned properly and meets your family’s survivorship and estate tax planning needs. Your NewEdge team and its partners can help perform a life insurance analysis and coordinate a review.

- In addition to life insurance, revisit your property and casualty insurance periodically as your personal and business circumstances change, such as getting married, having children, acquiring new property, upgrading existing properties, or expanding your business. It’s important to conduct a risk assessment to review coverage adequacy, cost management, and the policy terms and conditions.

- Discuss developing a family education plan to communicate your implemented strategies to the next generation and prepare them for the wealth with your NewEdge team. Families tend to get together over the holidays, which creates an ideal time to start the conversation.

- Don’t forget estate planning “freebies.” The annual exclusion gift limit remains at $17,000 per donor in 2023. However, in 2024, the annual exclusion for gifts will increase to $18,000. Recall that 529 College Savings Plans provide an opportunity to front-load 5 years of annual exclusion gifts in a single year (thus, up to $85,000). Your NewEdge Wealth team can help you determine whether it makes sense to fund a 529 Plan, pay tuition directly, or a combination thereof. Many factors impact this decision including the size of your taxable estate and projected growth, grandparents or other individuals who may plan to pay tuition directly to lower their taxable estates, and your goals for your wealth as it relates to the next generation.

- The limitation on tax-free annual gifts made to noncitizen spouses will increase from $175,000 in 2023 to $185,000 in 2024. Please reach out to your NewEdge team early to avoid the year-end rush.

- Medical and education expenses can be paid without gift tax limitation as long as you pay the medical provider/institution directly. There is no cap on this amount.

Evaluate Advanced Estate Planning Techniques

- For 2023, the federal estate, gift, and generation-skipping transfer (GST) applicable exclusion amounts are $12.92 million per person ($25.84 million per married couple). The maximum rate for federal estate, gift, and GST taxes is 40 percent, meaning an individual can gift up to $12.92 million in 2023 before triggering the 40 percent federal tax rate. For 2024, the federal estate, gift, and GST applicable exclusion amounts have increased to $13.61 million per person ($27.77 million per married couple). Consider utilization of the increased federal estate, gift, and GST tax applicable exclusion amounts before they are reduced by the earlier proposed legislation or at the end of 2025 to historical norms.

- Gift assets that have a high likelihood to grow significantly to remove any future appreciation from your taxable estate but recognize the recipient will lose the current benefit of receiving a step-up in cost basis upon your death.

- You may want to consider retaining low-cost basis assets, which would then be included in their taxable estates and receive a step-up in income tax basis while prioritizing high-income tax basis assets for potential lifetime gift transactions.

- In addition, if a trust beneficiary has unused federal estate tax exemption, it may make sense to consider including flexible language in the trust document that would allow the beneficiary to exercise a general power of appointment, resulting in the low-cost basis assets being included in the beneficiary’s taxable estate. We are available to discuss this analysis with you in more detail.

- For clients who wish to take advantage of the favorable exemption amount but are concerned about the possibility of running out of money, work with your NewEdge team to run an in-depth liquidity analysis. Our team will work closely with your trusts and estates attorney to evaluate advanced estate planning techniques and educate you on the technical aspects of how they operate. Including, but not limited to, intra-family loans and installment sales to intentionally defective grantor trusts (IDGTs), grantor retained annuity trusts (GRATs), irrevocable life insurance trusts (ILITs), and spousal lifetime access trusts (SLATs). With these grantor trusts, they can be drafted in such a way to provide not only asset protection but flexibility to the grantor. For example, the grantor may swap or buy back appreciated low-basis assets, borrow from the trust, or name their spouse as a permissible beneficiary.

- With the help of a qualified appraiser, consider obtaining valuation discounts prior to gifting assets. The goal of applying discounts with family or closely held businesses is typically to reduce valuations for gift and estate tax purposes while allowing gifts of an ownership percentage to the next generation at a reduced rate. They are commonly used for business appraisals for private investment partnerships, minority interests in LLCs, and Family Limited Partnerships (FLPs).

- Given market volatility, if your existing estate plan utilizes trusts that are subject to GST tax (GST non-exempt trusts), consideration should be given to allocating some or all of your increased GST exemption amount to such trusts.

- Take advantage of the current interest rate environment by using a Qualified Personal Residence Trust (QPRT). A QPRT is an irrevocable trust that allows the grantor to move a real primary or secondary home out of their personal estate. This is done for the key benefit of transferring the home to a future beneficiary with gift tax savings. With a QPRT, the higher the rate, the higher the value of the grantor’s right to use the residence as his or her own during the term of years and the lower the value of the gift of the future remainder interest. So as the §7520 rate increases, the taxable gift decreases, making the QPRT a more attractive strategy with higher interest rates.

- If you are holding promissory notes from prior estate planning transactions, from loans to family members, or otherwise, you may consider using some or all of the increased lifetime exemption amounts to forgive these notes.

- For married taxpayers, if the value of the assets owned by one spouse is greater than the increased federal exemption amounts and greater than the value of the assets owned by the other spouse, you may want to consider balancing or equalizing the estates. By transferring assets, both spouses would be able to tax advantage of the increased federal exemption amounts, especially the increased GST exemption, which is not portable to the surviving spouse upon the first spouse’s death. Taxpayers should be mindful, however, that transfers to non-U.S. citizen spouses are not eligible for the unlimited marital deduction for federal gift tax purposes, and such transfers should stay within the annual exclusion for such gifts ($175,000 in 2023) to avoid federal gift tax.

Charitable Giving Plan Considerations

While charitable donations by check or cash are the most common, there are many more tax-efficient approaches that may be used to increase your giving power and substantially impact your charitable giving. The amount of charitable donations you can deduct may range from 20% to 60% of your Adjusted Gross Income (AGI) depending on the type of contribution and the organization.

- Donate long-term appreciated assets instead of cash when possible. If you donate long-term appreciated assets such as stocks, bonds, or real estate to charity, you generally do not have to pay capital gains. You can also take an income tax deduction up to the full fair-market value, subject to AGI limitations. The recipient charity receives the full value of the asset and will not be subject to taxes upon any subsequent sales.

- Consider utilizing a Donor Advised Fund (DAF) and evaluate “bunching” multiple years of charitable contributions into the current year to increase your itemized deductions above the standard deduction threshold in 2023 ($13,850 for Single; $27,700 for MFJ). You will receive a charitable deduction in the year of contribution but may defer distribution to a public charity to a later year.

- If over age 70 ½, evaluate the tax benefit of using a Qualified Charitable Distribution (QCD) to satisfy up to $100,000 of your required minimum distribution (RMD). The qualified charitable distribution (QCD) rule allows traditional IRA owners to satisfy a portion of their RMD, exclude up to $100,000 from income, and contribute funds directly to charities without itemizing.

- Note, you cannot make a QCD to donor-advised funds, private foundations, supporting organizations, or other grant-making organizations.

- Take advantage of the higher interest rate environment, relative to what investors have experienced over the last decade, by using charitable trusts such as a Charitable Remainder Annuity Trust (CRAT). With a CRAT, the value of the remainder, calculated using the §7520 rate at the time the grantor creates the trust, gives the grantor an income tax charitable deduction. The value of the remainder must reach a minimum threshold; the higher the §7520 rate, the higher the value of the charitable interest.

- Give away the gain. If you expect to realize significant gains this year from investment transactions or a sale of a business or real estate, consider implementing a charitable strategy to reduce your tax bill on these gains in advance of the sale.

Retirement Plans

Maximize contributions to employer retirement accounts and Health Savings Accounts (HSAs). If contributing to your IRA, the deadline is April 15, 2024.

For IRA owners and plan participants, who MUST take a Required Minimum Distribution (RMD) in 2023:

- If you were born in 1951 or later, you use age 73 to start taking RMDs as under the SECURE 2.0 Act, age 73 applies to anybody who turns 72 in 2023 or later. If you turned 72 in 2023, your first distribution year is when you turn 73 next year in 2024, which means your required beginning date won’t be until April 1, 2025.

- If you were born in 1950 or earlier, you stick to your old schedule. So, if you turned 72 in 2022, you still have to take RMDs this year.

- However, individuals in company plans who are still working may qualify to delay RMDs until they retire, if the plan allows this (which most do).

For IRA designated beneficiaries, who MUST take an RMD in 2023:

- Any designated IRA or Roth IRA beneficiary who inherited before 2020 (before the original SECURE Act became effective) qualified for the stretch IRA and is permitted to continue that. They must stay on that RMD schedule. They will still be subject to RMDs this year and they do not qualify for any IRS RMD relief for 2023.

- Eligible designated beneficiaries (EDBs) under the SECURE Act still qualify for the stretch IRA and they must stay on that RMD schedule. They do not qualify for any IRS RMD relief for 2023.

EDBs are:

- Surviving spouses,

- Minor children of the deceased IRA owner (but only up to age 21),

- Disabled or chronically ill beneficiaries, or

Non-spouse beneficiaries who are not more than 10 years younger than the deceased IRA owner (or if they are older).

- For IRA designated beneficiaries, who is NOT subject to RMDs in 2023:Designated beneficiaries who inherited in 2020 or later, from an IRA owner who died before reaching his or her Required Beginning Date (RBD). These beneficiaries are subject to the 10-year rule, meaning that all inherited funds must be withdrawn by the end of the 10th year after death. But since they inherited from an IRA owner who had not yet begun RMDs, they are not subject to RMDs for years 1-9 of the 10-year term, so those in this group are not subject to RMDs by the end of this year.

- Designated beneficiaries who inherited in 2020 or later, from an IRA owner who died after reaching his or her RBD. These beneficiaries are subject to the 10-year rule, like the group above, but since they inherited from an IRA owner who had already begun RMDs, they must take annual RMDs for years 1-9 of the 10-year term. These RMDs are based on their own age. Because there was so much confusion, the IRS said that these RMDs will be waived for 2023. So, this group is not subject to RMDs by the end of this year. This RMD relief was announced earlier this year (Notice 2023-54).

- Designated Roth IRA beneficiaries who are not EDBs and inherited in 2020 or later are not subject to RMDs this year. Roth IRA beneficiaries are still subject to the 10-year rule, but they are not subject to RMDs for years 1-9 of the 10-year term, regardless of the age of the Roth IRA owner they inherited from. That’s because under the law, all Roth IRA owners are deemed to have died before reaching their required beginning date, since Roth IRA owners are not subject to lifetime RMDs.

- Review beneficiary designations for retirement plans.

- Consider Roth conversions or backdoor Roth IRA contributions. See our article on this subject.

Sources

https://taxfoundation.org/2023-tax-brackets/

https://taxfoundation.org/data/all/federal/2024-tax-brackets/

https://www.irs.gov/newsroom/irs-provides-tax-inflation-adjustments-for-tax-year-2024

IRS Notice 2022-53

IMPORTANT DISCLOSURES

The views and opinions included in these materials belong to their author and do not necessarily reflect the views and opinions of NewEdge Capital Group, LLC.

This information is general in nature and has been prepared solely for informational and educational purposes and does not constitute an offer or a recommendation to buy or sell any particular security or to adopt any specific investment strategy.

NewEdge and its affiliates do not render advice on legal, tax and/or tax accounting matters. You should consult your personal tax and/or legal advisor to learn about any potential tax or other implications that may result from acting on a particular recommendation.

The trademarks and service marks contained herein are the property of their respective owners. Unless otherwise specifically indicated, all information with respect to any third party not affiliated with NewEdge has been provided by, and is the sole responsibility of, such third party and has not been independently verified by NewEdge, its affiliates or any other independent third party. No representation is given with respect to its accuracy or completeness, and such information and opinions may change without notice.

Investing involves risk, including possible loss of principal. Past performance is no guarantee of future results.

Any forward-looking statements or forecasts are based on assumptions and actual results are expected to vary from any such statements or forecasts. No assurance can be given that investment objectives or target returns will be achieved. Future returns may be higher or lower than the estimates presented herein.

An investment cannot be made directly in an index. Indices are unmanaged and have no fees or expenses. You can obtain information about many indices online at a variety of sources including: https://www.sec.gov/answers/indices.htm.

All data is subject to change without notice.

© 2026 NewEdge Capital Group, LLC