1. Wake Me Up When September Ends: September is widely known to have the worst seasonal headwinds for the U.S. equity market, meaning returns in September have been the weakest on average of any month in the year. We expect U.S. large cap equities to continue to churn sideways, stuck in a range in the short-term of 4,300-4,600. A break below this range would be driven by rising growth fears that filter into lowered earnings estimates and risk-off positioning. A break above this range would be driven by continued upside surprises to economic growth that spur continued earnings upgrades, while yields remain contained (likely requiring rapidly falling inflation) in order to not pressure valuations.

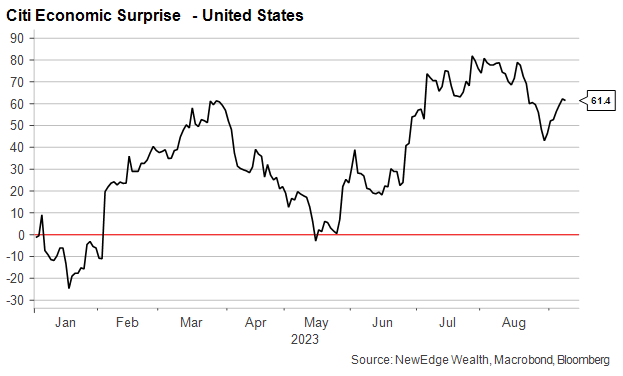

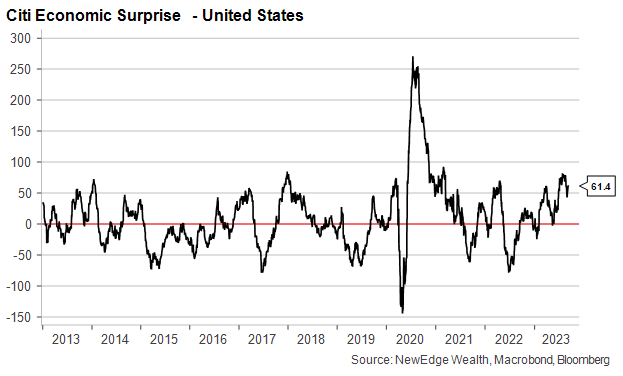

2. Surprise, Surprise: Underpinning the equity market strength coming out of the March lows has been a string of better economic data, surprising forecasters to the upside and spurring estimates to be revised higher. This is captured in economic surprise indices shown below (a reading above 0 indicates data coming in better than expected, often requiring analysts to raise their forecasts, while below 0 is data worse than expected). Note, the longer-term view of economic surprises reveals how these indices are mean reverting, meaning eventually analysts catch up to the economic reality and data begins to surprise in the opposite direction. We will watch for signs that economic surprises could begin to “roll over” and mean revert, meaning data begins to surprise to the downside instead of the upside.

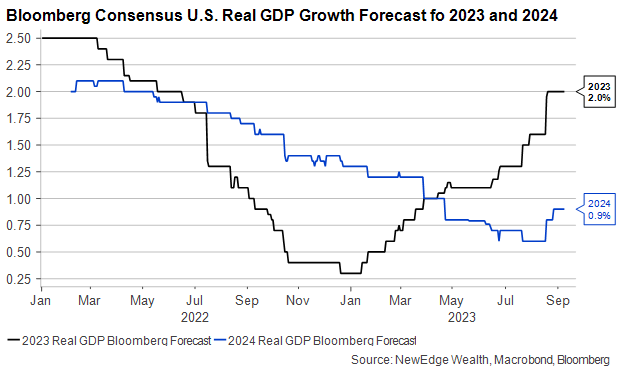

3. No Rain: This run of better economic data has forced analysts to raise their estimates for 2023 economic growth, pricing out a recession in 2H23 and incorporating the strong start to the year in 1H23. Interestingly, the rise in 2023 growth estimates came at the expense of 2024 estimates (meaning a stronger 2023 reduced the likelihood of a strong 2024) until recently, when analysts began to mark up 2024 forecasts as well.

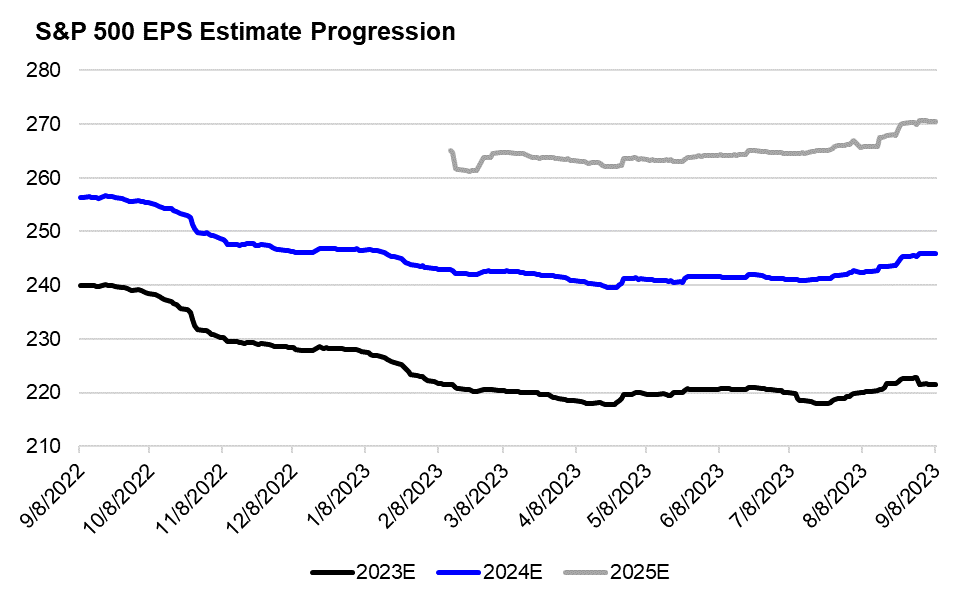

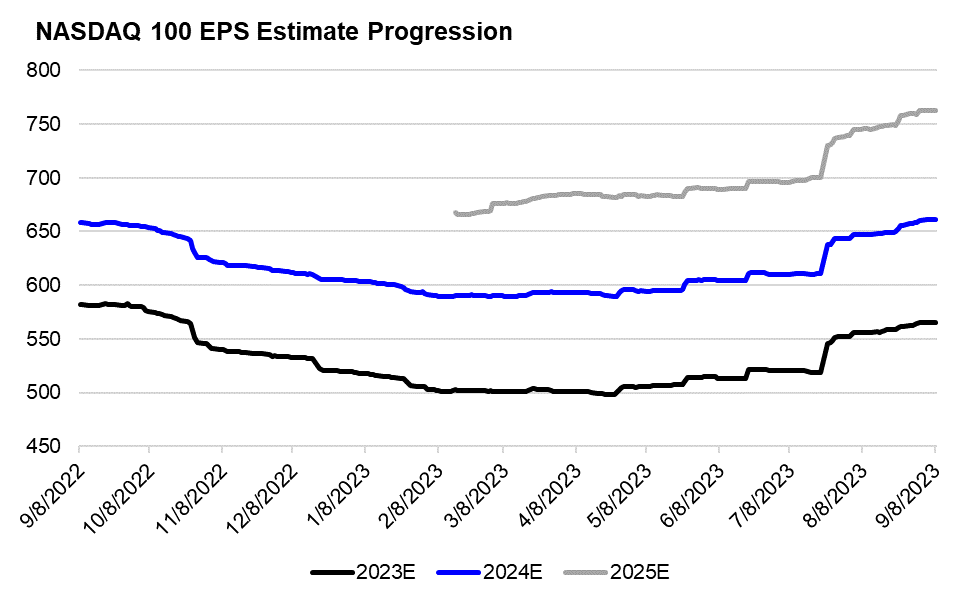

4. Keeps Getting’ Better: Boosted by better economic data and another better-than-expected earnings season for 2Q23, estimates for corporate earnings for 2023, 2024, and 2025 have been on the rise over the past two months. This is in contrast to 2022 and the first half of 2023 when EPS estimates were continuously cut. These EPS revisions higher are likely the driver of recent equity resilience (meaning the August correction was not about growth fears, and more about positioning, interest rates, and valuations). We will watch estimate revisions closely, as a return to estimate cuts would likely be the necessary condition for a deeper equity correction. We do not see evidence of a shift to lower revisions yet.

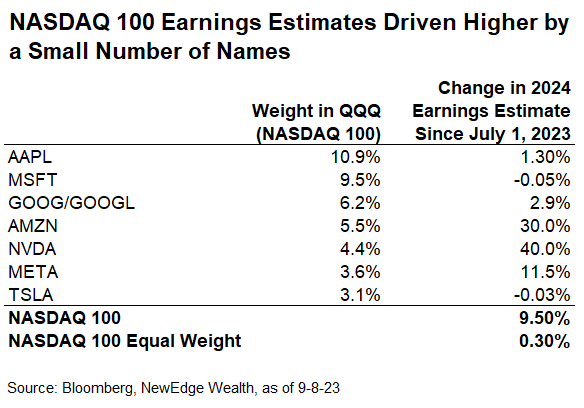

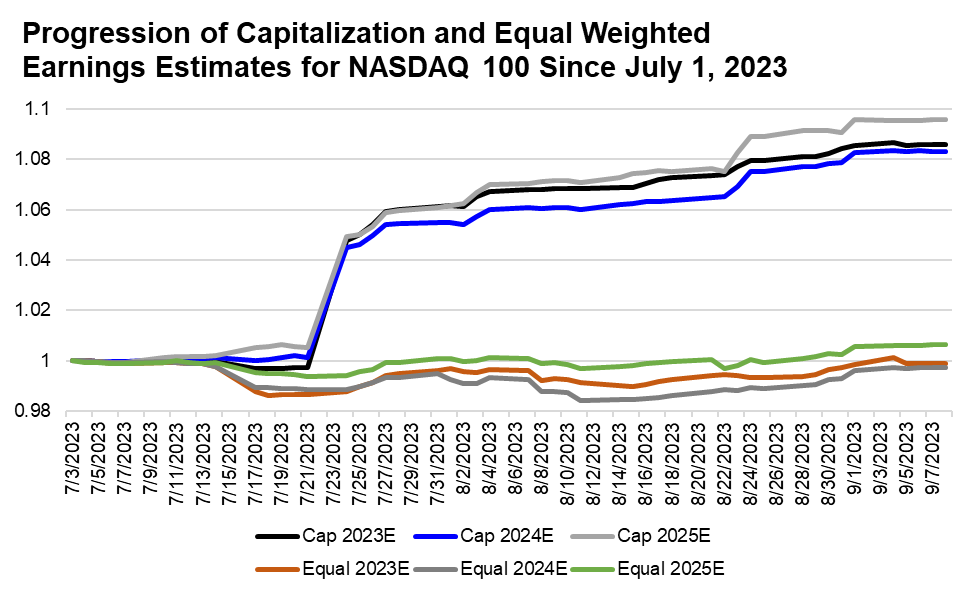

5. Only the Lonely: Before we get too excited about NASDAQ 100 (NDX) EPS revisions higher, investors must appreciate how concentrated the upside to EPS estimates has been, even for a concentrated index like the NDX. Only three names, NVDA, AMZN and META, account for the vast majority of the +9.5% upside revision to NDX estimates since early July, with the equal weight NASDAQ 100 only seeing its EPS estimates +0.3% in that time. Even amongst the “Magnificent Seven”, it is a lonely number of stocks driving earnings estimates higher.

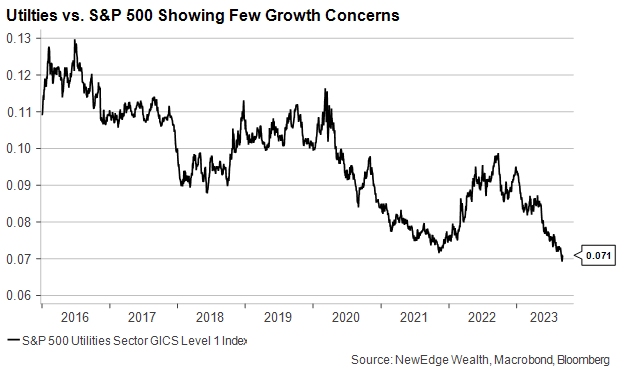

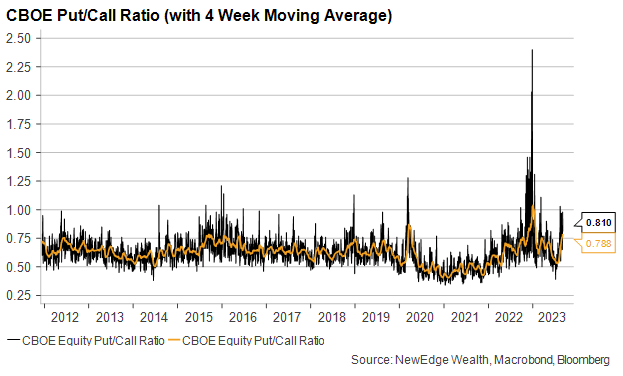

6. Watching Signs of “Gimme Shelter”: As one way to gauge investor sentiment, we look for evidence that they are crying “Gimme Shelter” by looking at the performance of defensive sectors, like Utilities and Consumer Staples, and demand for downside protection, like the Put/Call ratio (measures demand for downside protection with put options versus upside optionality with call options). Defensive performance continues to lag the market materially, showing few signs of growth fears (confirmed by EPS revisions moving higher above). Demand for downside protection has risen, after nearing the 2021 “complacent” lows back in July but is not back to peak “fear” levels yet.

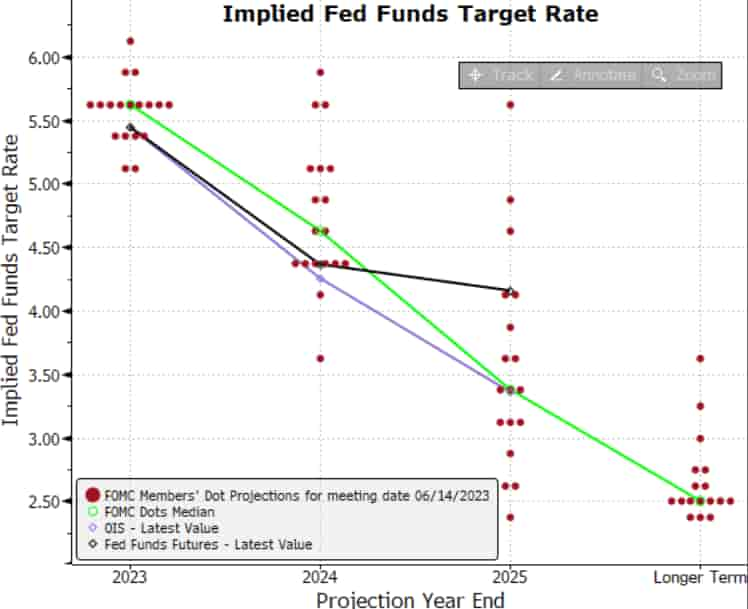

7. Hold the Line: Fed speakers are sounding less urgent on continuing to hike interest rates further, opting for either a skip of the September meeting or a “wait and see” approach to judge if further hikes are needed. However, Fed members continue to argue for keeping rates “higher for longer” to ensure inflation’s demise. Looking to upcoming meetings, we think what matters more than the terminal rate discussion is the discussion about the 100 bps of cuts for 2024 currently forecasted by the Fed’s Dot Plot and the bond market. We discussed the dovish rationale the Fed is using to justify this projection and how the data may not support this “golden” policy path in a recent Weekly Edge.

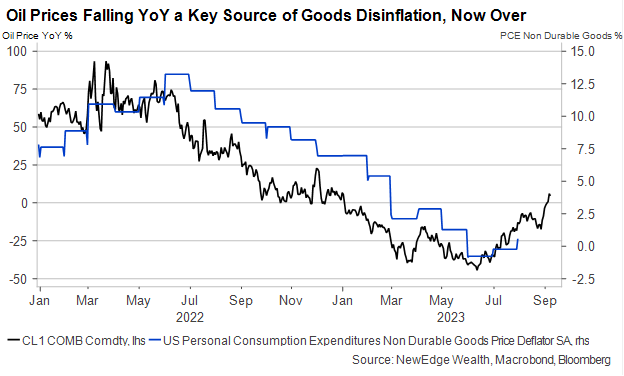

8. Dog Days are Over: Since March 2022, oil prices have been on the retreat, with a deceleration and then all-out decline in the year-over-year (YoY) change in oil prices. This descent was a key contributor to falling non-durable goods inflation. However, this descent reached its nadir in June 2023 as oil prices began to climb again and are now positive on a YoY basis. This will likely contribute to higher YoY and MoM readings for headline inflation in coming months.

9. Slow Down, You’re Doin’ Fine: The USD has staged a strong +5.5% rally since mid-July, pushing the index into “overbought” territory (using a relative strength index). Given this technical backdrop, it would not be surprising to see the USD consolidate the recent move to the upside.

US Dollar (DXY Index)

Top Points of the Week

By Ben Lope

1. Equities start September in the red – Global equities followed up a losing August with a losing week to begin September. Within the US, the Dow Jones Industrial Average suffered the smallest loss, while tech and small cap names, as measured by the NASDAQ and Russell 2000 indices, respectively, each shed over 2% of their values through the week. International developed and emerging markets were each down modestly over the same period.

2. Yield Curve inversion moderates slightly – Yields on 2-year Treasury bills increased by more than yields on 10-year Treasury bills throughout the week, slightly decreasing the extent to which the 2-10 yield curve remains inverted. The degree of yield curve inversion is more than 30bp off peaks seen in March and July but remains nearly 20bps higher than the level of inversion exhibited at the start of the year.

3. Oil crosses $90/barrel threshold – The price per barrel of Brent crude oil eclipsed $90 this week after announcements from Russia and Saudi Arabia that the two nations would extend their supply cuts through the end of the year. This is the highest that oil prices have been this year and sparked commentary from the White House that President Biden would use “everything within his toolkit” to aid Americans in the likely event of increased fuel costs.

4. ISM Services PMI increased in August – The Institute for Supply Chain Management’s (ISM) August Services PMI came in at 54.5, an increase of almost two points from July, which defied economists’ expectations for a slight month-over-moth decrease and pushed the measure to its highest reading since February. Following the announcement stocks moved lower and yields moved higher. These market movements are likely a signal that despite the Services PMI’s positive indication of a resilient services sector, additional data points from August that indicated higher prices paid by businesses continue to stoke inflationary fears, and by extension, the prospect of additional Fed rate hikes.

5. US Jobless Claims reach lowest level since February – US jobless claims fell for the fourth week in a row, totaling 216,000 for the week ended September 2. Economists had expected jobless claims for the week to total 234,000, which would have marked a 5,000 increase from the previous week’s reading. This is the measure’s lowest level since February.

6. US Q2 Productivity revised downward, but still highest in nearly three years – The Labor Department revised an initial reading for US Q2 Productivity down from 3.7% to 3.5%, which is still the highest productivity reading since Q3 2020. Following the announcement, the dollar moved higher while the Euro moved lower, pointing to the potential that a sustained productivity surge could strengthen the USD and drive divergences between the USD and overseas currencies.

7. China’s Services PMI falls in August – The Caixin China Services PMI, a private survey of business activity in the services sector, decreased to 51.8 for the month of August from July’s reading of 54.1. Although the PMI reading is still above 50 and therefore in expansion territory, the month-over-month slip points to weak domestic demand that has thus far been unresponsive to recent fiscal and economic stimulus measures enacted by Chinese authorities.

8. Europe PMI creeps further into contractionary territory – The S&P Global’s August measure of Eurozone PMI slipped further into contractionary territory. The composite PMI fell nearly two points from July’s reading, from 48.6 to 46.7, and reached the lowest reading since November 2020. The measure of Services PMI recorded a monthly decline even greater than the Composite PMI and officially entered contractionary territory as consumers lowered spending to offset the headwinds of higher living and borrowing costs.

9. Earnings next week – Next week’s earnings calendar is light but includes announcements from two major software companies: Oracle (ORCL) and Adobe (ADBE). Both stocks are up over 50% year-to-date as enthusiasm surrounding the application of artificial intelligence initiatives has fueled investor optimism.

10. Data next week – August CPI will be released next Wednesday and is sure to be the most anticipated economic announcement of the week, followed by data for August PPI and Retail Sales, which will be released on Thursday. FOMC members enter their “quiet period” on Saturday, meaning that there will be no official communications until the committee’s two-day policy meeting that begins September 19.

Song Reference Artist Answers Key:

- Green Day

- Bruce Springsteen (or The Starting Line for the deep track)

- Blind Melon

- Christina Aguilera

- Roy Orbison

- The Rolling Stones

- Toto

- Florence & The Machine

- Billy Joel

IMPORTANT DISCLOSURES

Abbreviations/Definitions: Brent blend: a blend of crude oil extracted from oilfields in the North Sea between the United Kingdom and Norway. It is an industry standard because it is “light,” meaning not overly dense, and “sweet,” meaning it’s low in sulfur content; China Caxin Services PMI: Caixin China General Services PMI seeks to provide the most up-to-date possible indication of what is happening in the country’s growing services industry by tracking variables such as sales, employment, inventories and prices; CPI: Consumer Price Index; Dot Plot: The Fed dot plot is published quarterly as a chart showing where each of the 12 members of the FOMC expect the federal funds rate to be for each of the next three years and the long term; EPS: earnings per share; FOMC: Federal Open Market Committee; ISM Services PMI: The Institute of Supply Management (ISM) services PMI (formerly known as Non-Manufacturing Index) is an economic index based on surveys of more than 400 non-manufacturing (or services) firms’ purchasing and supply executives; PPI: Producer Price Index; Retail Sales: represents a key macroeconomic metric that tracks consumer demand for finished goods and acts as a key economic barometer and whether inflationary pressures exist. Retail sales are measured by durable and non-durable goods purchased over a defined period of time; S&P Global Services PMI: the S&P Global US Services PMI is compiled by S&P Global from responses to questionnaires sent to a panel of around 400 service sector companies; S&P Global Composite PMI: the S&P Global Composite PMNI is the weighted average of manufacturing and service sector PMIs for a given geography or economy;

Index Information: All returns represent total return for stated period. S&P 500 is a total return index that reflects both changes in the prices of stocks in the S&P 500 Index as well as the reinvestment of the dividend income from its underlying stocks. Dow Jones Industrial Average (DJ Industrial Average) is a price-weighted average of 30 actively traded blue-chip stocks trading New York Stock Exchange and Nasdaq. The NASDAQ Composite Index measures all NASDAQ domestic and international based common type stocks listed on the Nasdaq Stock Market. Russell 2000 is an index that measures the performance of the small-cap segment of the U.S. equity universe. MSCI International Developed measures equity market performance of large, developed markets not including the U.S. MSCI Emerging Markets (MSCI Emerging Mkts) measures equity market performance of emerging markets. Russell 1000 Growth Index measures the performance of the large- cap growth segment of the US equity universe. It includes those Russell 1000 companies with relatively higher price-to-book ratios, higher I/B/E/S forecast medium term (2 year) growth and higher sales per share historical growth (5 years). The Russell 1000 Value Index measures the performance of the large cap value segment of the US equity universe. It includes those Russell 1000 companies with relatively lower price-to-book ratios, lower I/B/E/S forecast medium term (2 year) growth and lower sales per share historical growth (5 years). The BBB IG Spread is the Bloomberg Baa Corporate Index that measures the spread of BBB/Baa U.S. corporate bond yields over Treasuries. The HY OAS is the High Yield Option Adjusted Spread index measuring the spread of high yield bonds over Treasuries. S&P Equal Weight Index (S&P EWI) is the equally-weighted version of the widely regarded S&P 500® Index, which measures 500 leading companies in leading U.S. industries. The S&P EWI has the same constituents as the capitalization weighted S&P 500® Index, but each company in the S&P EWI is allocated a fixed weight, rebalancing quarterly.

Sector Returns: Sectors are based on the GICS methodology. Returns are cumulative total return for stated period, including reinvestment of dividends.

The views and opinions included in these materials belong to their author and do not necessarily reflect the views and opinions of NewEdge Capital Group, LLC.

This information is general in nature and has been prepared solely for informational and educational purposes and does not constitute an offer or a recommendation to buy or sell any particular security or to adopt any specific investment strategy.

NewEdge and its affiliates do not render advice on legal, tax and/or tax accounting matters. You should consult your personal tax and/or legal advisor to learn about any potential tax or other implications that may result from acting on a particular recommendation.

The trademarks and service marks contained herein are the property of their respective owners. Unless otherwise specifically indicated, all information with respect to any third party not affiliated with NewEdge has been provided by, and is the sole responsibility of, such third party and has not been independently verified by NewEdge, its affiliates or any other independent third party. No representation is given with respect to its accuracy or completeness, and such information and opinions may change without notice.

Investing involves risk, including possible loss of principal. Past performance is no guarantee of future results.

Any forward-looking statements or forecasts are based on assumptions and actual results are expected to vary from any such statements or forecasts. No assurance can be given that investment objectives or target returns will be achieved. Future returns may be higher or lower than the estimates presented herein.

An investment cannot be made directly in an index. Indices are unmanaged and have no fees or expenses. You can obtain information about many indices online at a variety of sources including: https://www.sec.gov/answers/indices.htm.

All data is subject to change without notice.

© 2026 NewEdge Capital Group, LLC