The Case for NewEdge Structured Note Strategies

“Everyone has a plan until they get punched in the mouth.” — Mike Tyson

While investors entered 2025 with Great Expectations for equity markets, the first quarter of 2025 has thrown its proverbial punch with equities struggling to reproduce the 2023/2024 return experience. The S&P 500 corrected ~10% between February 19 and March 13, resulting in notable increases in market volatility (an indication of investor fear) and a reminder to investors that equity risk still exists in markets. This rocky start to the year has resulted in some of the most bullish investors becoming unsettled around the direction of markets and the economy. With uncertainty on the rise and market sentiment faltering, investors may be starting to second-guess their portfolio risk to avoid future haymakers that equity markets may throw. Portfolio strategies that provide investors with a degree of downside protection against equity loss and defined return outcomes can be a powerful tool to keep otherwise fearful investors aligned with (their financial) plan.

Key Points

- Market volatility is trending higher, and the macro backdrop in 2025 presents an ideal setting for heightened volatility to continue.

- Investor sentiment has fallen off a cliff in the first quarter of 2025, but equity positioning remains very bullish through March.

- Trailing 5, 10, and 15 year US equity returns are well above longer-term averages, but more than “great expectations” will be needed to continue delivering these above average returns as historical data suggests a higher probability of lower forward returns starting from today’s valuations.

- Investors should prepare for the possibility of a lot of sideways, choppy equity returns in 2025 and consider defined outcome or uncorrelated investment strategies that may thrive in this environment.

- NewEdge Structured Note Strategies benefit from heightened volatility and focus on defined outcomes, seeking to provide equity-like returns while mitigating the uncertainty associated with unhedged equities through the usage of downside protection that can protect investor capital and returns.

- The potential combination of elevated forward strategy returns, managed downside risks and a macro environment that may result in strategy outperformance relative to benchmarks creates an appealing environment for NewEdge Structured Note Strategies.

What Investors are Feeling

With market volatility on the rise in the first quarter of 2025, we surveyed investors to understand their most pressing concerns. While there was a wide range of responses, there were some very clear themes that arose from the poll:

- Investors can feel that market volatility is back after being almost non-existent through much of 2024, and they want to understand how to insulate their portfolios or take advantage of it.

- Historically expensive equity valuations, interest rate uncertainty and slowing economic growth are bringing portfolio positioning and cash deployment options into question.

- Individuals are seeking guidance around alternative investments and how they should be utilized within portfolios.

These investor worries are topics we have been talking about since 2024 as our analysis indicated higher chances of future equity returns being challenged. With equity volatility back and market uncertainty rising, investors are looking for strategies that can help them navigate this new regime, which may stick around for a while.

Investor Positioning vs. Risk Tolerance

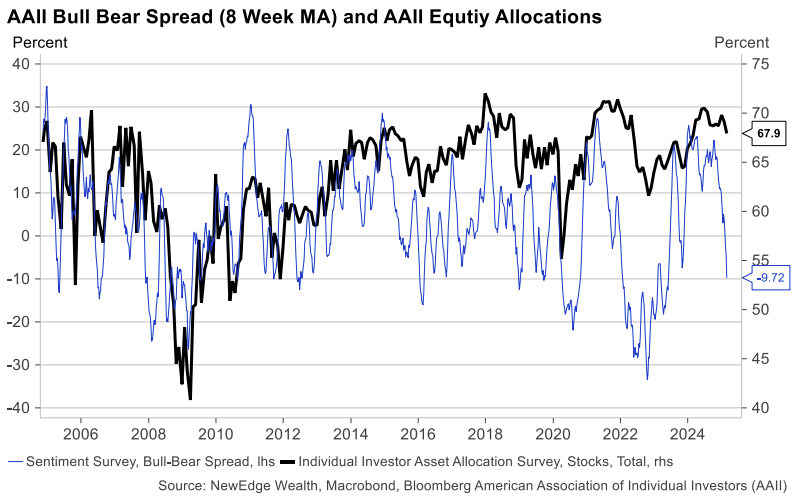

While uncertainty and volatility are a feature of equity market investing, 2023 and 2024’s strong equity returns and lack of meaningful market volatility put investors into a euphoric state, making pressing concerns around equity market risk a distant memory.

This euphoria resulted in individual investor equity allocations elevating to new highs (~70% of portfolio allocations at the start of 2025), reflecting very bullish investor positioning. Amid this backdrop of overweight equity positioning, the first quarter of 2025 caused investor sentiment to fall off a cliff as uncertainty returned to markets in a significant way. This has resulted in a significant mismatch between portfolio positioning and sentiment, and in the words of our Chief Investment Officer, Cameron Dawson, “watch what they do, not what they say”. The mismatch may be communicating that while investors are becoming increasingly concerned about the future of equity markets, some optimism likely remains, or investors do not want to downshift to traditional fixed income, even with traditional corporate bonds now offering higher yields that would have been unheard of a decade ago.

NewEdge Structured Note Strategies seek to provide investors with a middle ground between fixed income and equities by seeking equity-like returns with the return consistency associated with fixed income. A desire by a client to de-risk their portfolio, but an unwillingness to accept traditional bond returns is one of the most compelling reasons to consider utilizing a diversified, actively managed structured note strategy within a portfolio.

On the opposite end of the investor risk spectrum are individuals that are light on equity exposure but are also concerned about increasing their position due to the uncertainty associated with equities. NewEdge Structured Note Strategies’ focus on defined investment outcomes may provide the peace-of-mind needed to know that even if equities are challenged to perform going forward, the underlying note positions all have a degree of downside protection that could help mitigate the risk of poor investment performance during a market downturn.

Structured Note Strategies: The Alternative to Alternatives

Alternative Investments have long been leveraged by wealthier investors as a method to achieve portfolio risk and returns that may be unachievable through traditional stocks and bonds. One common vehicle used to pursue these returns are Hedge Funds. In theory, Hedge Funds offer investors the ability to achieve uncorrelated returns that were less reliant upon traditional equity markets, but in practice, there are numerous challenges that investors in Hedge Funds must face, such as:

- Inconsistent process and return outcomes

- Lack of holdings transparency

- Inefficient tax treatment

- Schedule K-1 tax reporting

- Expensive and unpredictable fees (i.e., management fees, carry, pass-through fees)

- Lack of liquidity through lock-up periods and liquidity gates

NewEdge Structured Note Strategies were born out of the desire to create a better alternative to these Hedge Funds, and to help alleviate or eliminate the challenges presented with them. Furthermore, Structured Notes have historically faced their own set of challenges when it came to utilization within a portfolio that NewEdge Structured Note Strategies aims to solve. When we began managing discretionary Structured Note portfolios in 2018, our goal was to offer individuals, financial advisors and institutions a better way to access differentiated return streams while fully leveraging the benefits of Structured Notes in their portfolios. Nearly seven years later, our objectives have not changed, and we continue to stand by that mission.

The Reports of Volatility’s Demise Were Greatly Exaggerated

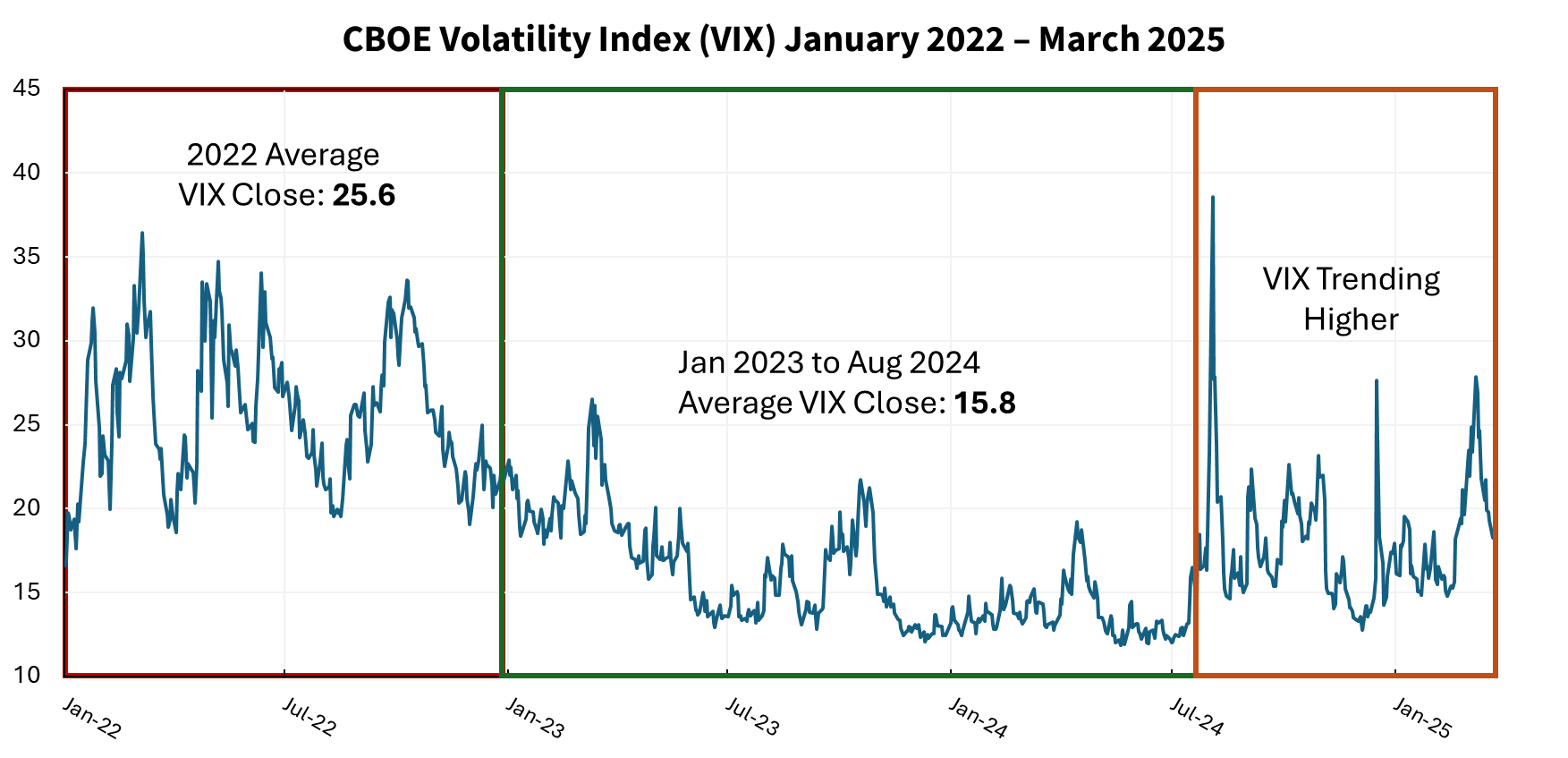

Equity market volatility ebbs and flows, and it is common for investors to experience the emotional highs and lows that come with it. However, the muted volatility experienced throughout most of 2023 and 2024 was far from normal, providing investors with nearly endless amounts of returns and pushing equity market valuations to historically expensive levels. These years were so good for investors that most quickly forgot that the challenging market of 2022, headlined by rising inflation and credit concerns, ever existed and buried the thought of negative returns in 2025. While volatility was down in these years, it never disappeared, and the quiet regime began to unwind in the back half of 2024. Since August of 2024, volatility has revived from its slumber and is climbing back to reclaim its title of being on the forefront of investor’s minds.

Volatility has proven that it is indeed “back”, and we expect that for a good portion of 2025, it is here to stay. The economic, macro and policy backdrop for 2025 is one conducive for heightened, sustained equity market volatility. NewEdge’s 2025 market outlook called for higher volatility and for equities to trade in a wide, choppy range. While 2025 is far from a complete story, it didn’t take longer than a single quarter for the market to realize some of the predictions stated in our outlook.

Equity market corrections can be stressful for investors as their portfolio values decline, sometimes at a rapid pace. Staying invested through these periods rather than trying to time a market exit and re-entry can be critical to maintaining long-term portfolio returns, particularly on an after tax basis. However, this can be easier said than done when the fear of even greater losses during a downtown takes over.

In our experience working with advisors and their clients, investing in Structured Note Strategies may help investors re-frame these periods of volatility as not a time to fear the market, but rather, a time to take advantage of the opportunities available. The strategies deploy investor capital tactically, often capitalizing on market dislocations, which may lead to better terms and potential future returns for investors. This focus on capital deployment during periods of volatility suggests that 2025 could present a wealth of new investment opportunities within the managed portfolios.

Great Expectations or Great Disappointments?

In our introduction, we highlighted how investors broadly came into 2025 with some Great Expectations for markets. Our outlook discussed the many hurdles that markets would face to meet these great expectations and believed that investors were likely to set themselves up for some Great Disappointments as markets struggle to meet the high bar set for them. While the first quarter’s correction may have brought down US market valuations a bit, equities may still face several headwinds in their fight for positive returns going forward:

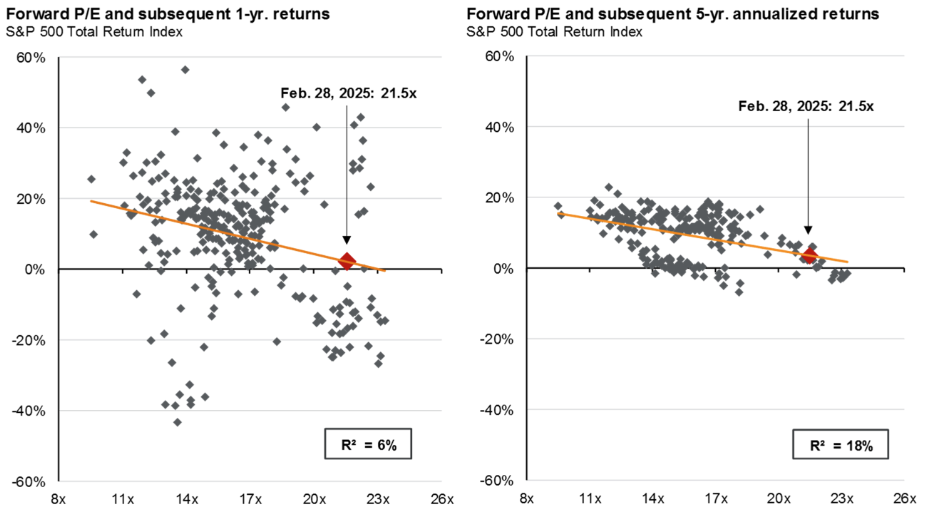

- Equity Valuations: As of February 28, 2025, US market valuations, represented by the S&P 500, were trading at roughly 21.5x forward earnings. While valuation alone may not prevent the index from accomplishing a three-peat of 2023/2024’s returns, they could make it increasingly difficult to do so. As equity valuations grow, so do expectations of future earnings growth, amplifying any negative news that may disrupt the market’s ability to achieve that future growth.

As of 2/28/25

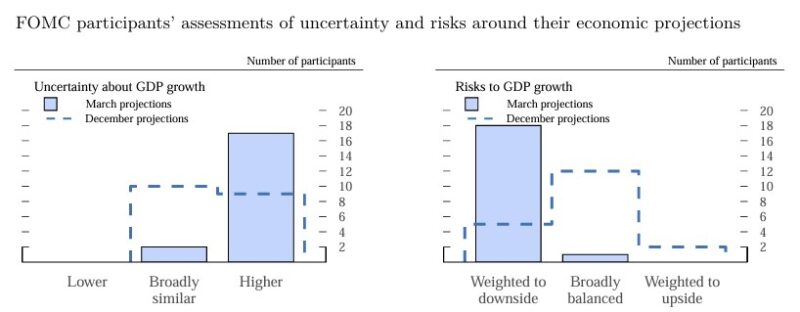

- Slowing Economic Growth: While corporate profits have been strong throughout 2023 and 2024, future estimates are being trimmed down to our economic reality since 2024. Future growth of US GDP has also come under pressure recently as certain economic data softens, and even the Federal Open Market Committee (FOMC) that controls US interest rates, expressed greater uncertainty on GDP growth. In March, the group communicated a near consensus that the risks to future GDP growth are weighted to the downside (March 19, 2025, FOMC meeting).

FOMC Participants’ Assessments of Uncertainty and Risks Around Their Economic Projections

As of 3/19/25

- Policy Uncertainty: Since 2024, we have been discussing the increased likelihood of policy uncertainty and its potential negative impact on market returns. It would be difficult to say that March 2025’s correction was not, in large part, linked to the barrage of tariff announcements that dominated headlines throughout the month. Should the current style and volume of tariff communications continue throughout 2025, markets should buckle up for what could be a wild ride of uncertainty.

In our view, these headwinds have meaningfully increased the likelihood that equities will experience a lot of sideways chop in 2025. These types of challenged environments can be difficult for equity investors, especially those whose portfolios rely heavily on equities to generate positive returns. Strategies that can reduce a portfolio’s dependency on equity returns work best in environments where equities underperform. NewEdge Structured Note Strategies seek to achieve positive returns, even if markets experience sideways chop or negative returns across a market cycle.

While the strategies do not aim to consistently outperform unhedged equities (they benchmark against a combination of the MSCI All-Cap World Index and the Bond Aggregate Index), the higher probability of challenging equity returns increases the likelihood that the strategies will outperform equity returns.

Conclusion

“He who is not courageous enough to take risks will accomplish nothing in life.” — Muhammad Ali

We agree that investors must be willing to endure some degree of risk to achieve success in their portfolios. However, strategies exist that can help balance the desire for higher investment returns with the need for more predictable outcomes or defined returns. NewEdge Structured Note Strategies look to balance those objectives, aiming to provide stability to portfolios throughout periods of market uncertainty.

With 2025 already off to a volatile start and equity markets facing headwinds that may challenge future returns, there have been few better periods to consider integrating NewEdge Structured Note Strategies into investor portfolios.

IMPORTANT DISCLOSURES

NewEdge Wealth is a division of NewEdge Capital Group, LLC. Investment advisory services offered through NewEdge Wealth, LLC an investment adviser registered with the US Securities and Exchange Commission. Securities offered through NewEdge Securities, LLC, Member FINRA/SIPC.

The information in this Presentation has been prepared solely for discussion purposes and is not intended as an offer or solicitation of an offer with respect to the purchase or sale of any security and should not be relied upon by you in evaluating the merits of investing in any securities.

Investing involves risk, including possible loss of principal. Past performance is no guarantee of future results.

NewEdge and its affiliates do not render advice on legal, tax and/or tax accounting matters to clients. Any investment, tax, marketing, or legal information contained herein is general and educational in nature and should not be construed as advice. Please consult your tax advisor for matters involving taxation and tax planning and your attorney for matters involving trusts, estate planning, charitable giving, philanthropic planning, and other legal matters.

The trademarks and service marks contained herein are the property of their respective owners. Unless otherwise specifically indicated, all information with respect to any third party not affiliated with NewEdge has been provided by, and is the sole responsibility of, such third party and has not been independently verified by NewEdge, its affiliates or any other independent third party. No representation is given with respect to its accuracy or completeness, and such information and opinions may change without notice.

Certain information contained in this Presentation constitutes “forward-looking statements,” which can be identified by the use of forward-looking terminology such as “may,” “will,” “should,” “expect,” “anticipate,” “project,” “estimate,” “intend,” “continue,” or “believe,” or the negatives thereof or other variations thereon or comparable terminology. Due to various risks and uncertainties, actual events, results or the actual performance of the

Adviser’s investments may differ materially from those reflected or contemplated in such forward-looking statements. Nothing contained in this Presentation may be relied upon as a guarantee, promise, assurance or a representation as to the future.

Gross returns do not reflect the deduction of fees, commissions or other charges, which reduce returns (e.g., an investment management fee of 0.50% will reduce a 10% return to a 9.5% return). The compounding effect of such fees over time can be substantial and should be taken into consideration when viewing these materials. Net (%) was calculated using the highest advisory fee of 1% applied annually for each year the note has been outstanding. If you have any questions concerning the fee calculation and deduction method, please contact your Private Wealth Adviser.

When referencing asset class returns or statistics, the following indices are used to represent those asset classes, unless otherwise notes. You cannot invest directly in an index. Index returns shown are total returns which includes interest, capital gains, dividends, and distributions realized over a given period of time. An individual who purchases an investment product which attempts to mimic the performance of a benchmark or index will incur expenses such as management fees and transaction costs which reduce returns.

A complimentary copy of our current Form ADV Disclosure Brochure that describes the advisory program and related fees is available through your Private Wealth Advisor. Please contact your Private Wealth Advisor if you have any questions.

Certified Financial Planner Board of Standards, Inc. (CFP Board) owns the CFP® certification mark, the CERTIFIED FINANCIAL PLANNER™ certification mark, and the CFP® certification mark (with plaque design) logo in the United States, which it authorizes use of by individuals who successfully complete CFP Board’s initial and ongoing certification requirements.

Risks Related to Structured Products

Investments in structured products are subject to several risks, including credit risk, market risk and liquidity risk. Structured products typically have a specified maturity date and payout profile determined by the performance of an underlying, or basket of underlying, market measures. Structured products are generally designed to provide some level or combination of principal protection, downside market risk mitigation, enhanced income or enhanced returns relative to the performance of the underlying market measure. As a senior unsecured debt obligation, the payout at maturity is dependent on the issuer’s ability to pay off its debts as they mature. While there is generally liquidity provided by the issuer of a structured product prior to maturity, there is no guarantee of a secondary market. In the case that there is a secondary market provided, the sale price may be significantly less than what would be the maturity value due to factors such as volatility, interest rates, credit quality and risk appetite. The value of an investment in a structured product will reflect the then-current market value of the structured product as calculated by the issuer and will be subject to all the risks associated with an investment in the underlying market measure along with the risks and factors described above. Investors in structured products will not own or have any claim to the underlying market measure directly and will, therefore, not benefit from general rights applicable to the holders of those assets, such as dividends and voting rights. Notes are not insured through any government agency or program and the return of principal and fulfillment of the terms negotiated by NewEdge on behalf of its clients is dependent on the financial condition of the third party issuing the note and the issuer’s ability to pay its obligations as they become due.

Structured notes purchased for you will not be listed on any securities exchange. There may be no secondary market for such structured notes, and neither the issuer nor the agent will be required to purchase notes in the secondary market. Some of these structured financial products are callable by the issuer only, therefore the issuer (not you) can choose to call in the structured notes and redeem them before maturity. In addition, the maximum potential payment on structured notes will typically be limited to the redemption amount applicable for a payment date, regardless of the appreciation in the underlying index associated with the note. Since the level of the underlying index at various times during term of the structured notes held by you could be higher than on the valuation dates and at maturity, you may receive a lower payment if redeemed early or at maturity than if a client would have invested directly in the underlying index. While the payment at maturity of any structured notes would be based on the full principal amount of any note sold by the issuer, the original issue price of any structured notes purchased for you includes an agent’s commission and the cost of hedging the issuer’s obligations under the note. As a result, the price, if any, at which an issuer will be willing to purchase structured notes from clients in a secondary market transaction, if at all, will likely be lower than the original issue price and any sale before the maturity date could result in a substantial loss. Structured notes will be designed to be short-term trading instruments so you should be willing to hold any notes to maturity.

Definitions

1Maturity Date: The date at which the Note must redeem and the investor receives the amount due based on the contractual amount in the Prospectus.

2Downside Protection: The level at which investors are exposed to the negative performance of a reference asset. A Soft protection will specify the level at which investors will begin to participate in the full negative performance of a reference asset. Any principal repayment is subject to the credit risk of the issuer and any guarantor.

3Downside Threshold: The level of the underlying/reference asset at which the investor is exposed to the negative performance of a reference asset; based on the Protection (number 2).

4Tax Treatment: Manner in which income or proceeds from a Note are taxed based on IRS regulations.

5Market Value: Represents the number of shares held multiplied by the valuation.

6Par Value: Represents the number of shares held multiplied by the cost basis.

7Principal Protection: Represents the percentage to breach minus the underlying return.

Index Information

Index returns shown are total returns which includes interest, capital gains, dividends, and distributions realized over a given period of time. You cannot invest directly in an index. An individual who purchases an investment product which attempts to mimic the performance of a benchmark or index will incur expenses such as management fees and transaction costs which reduce returns.

The Cboe Volatility Index, better known as VIX, projects the probable range of movement in the U.S. equity markets, above and below their current level, in the immediate future. Specifically, VIX measures the implied volatility of the S&P 500® (SPX) for the next 30 days. When implied volatility is high, the VIX level is high and the range of likely values is broad. When implied volatility is low, the VIX level is low and the range is narrow.

S&P 500 (Total Return) is a total return index that reflects both changes in the prices of stocks in the S&P 500 Index as well as the reinvestment of the dividend income from its underlying stocks.

Credit Rating: A Credit Rating is an opinion regarding the creditworthiness of an entity, a debt or financial obligation, debt security, preferred share or other financial instrument, or of an issuer of such a debt or financial obligation, debt security, preferred share or other financial instrument, issued using an established and defined ranking system of rating categories. The creditworthiness of the issuer does not affect or enhance the likely performance of the investment other than the ability of the issuer to meet its obligations.

CREDIT RATINGS ISSUED BY MOODY’S INVESTORS SERVICE, INC. AND ITS RATINGS AFFILIATES (“MIS”) ARE MOODY’S CURRENT OPINIONS OF THE RELATIVE FUTURE CREDIT RISK OF ENTITIES, CREDIT COMMITMENTS, OR DEBT OR DEBT-LIKE SECURITIES, AND MOODY’S PUBLICATIONS MAY INCLUDE MOODY’S CURRENT OPINIONS OF THE RELATIVE FUTURE CREDIT RISK OF ENTITIES, CREDIT COMMITMENTS, OR DEBT OR DEBT-LIKE SECURITIES. MOODY’S DEFINES CREDIT RISK AS THE RISK THAT AN ENTITY MAY NOT MEET ITS CONTRACTUAL, FINANCIAL OBLIGATIONS AS THEY COME DUE AND ANY ESTIMATED FINANCIAL LOSS IN THE EVENT OF DEFAULT. CREDIT RATINGS DO NOT ADDRESS ANY OTHER RISK, INCLUDING BUT NOT LIMITED TO: LIQUIDITY RISK, MARKET VALUE RISK, OR PRICE VOLATILITY. CREDIT RATINGS AND MOODY’S OPINIONS INCLUDED IN MOODY’S PUBLICATIONS ARE NOT STATEMENTS OF CURRENT OR HISTORICAL FACT. MOODY’S PUBLICATIONS MAY ALSO INCLUDE QUANTITATIVE MODEL-BASED ESTIMATES OF CREDIT RISK AND RELATED OPINIONS OR COMMENTARY PUBLISHED BY MOODY’S ANALYTICS, INC. CREDIT RATINGS AND MOODY’S PUBLICATIONS DO NOT CONSTITUTE OR PROVIDE INVESTMENT OR FINANCIAL ADVICE, AND CREDIT RATINGS AND MOODY’S PUBLICATIONS ARE NOT AND DO NOT PROVIDE RECOMMENDATIONS TO PURCHASE, SELL, OR HOLD PARTICULAR SECURITIES. NEITHER CREDIT RATINGS NOR MOODY’S PUBLICATIONS COMMENT ON THE SUITABILITY OF AN INVESTMENT FOR ANY PARTICULAR INVESTOR. MOODY’S ISSUES ITS CREDIT RATINGS AND PUBLISHES MOODY’S PUBLICATIONS WITH THE EXPECTATION AND UNDERSTANDING THAT EACH INVESTOR WILL, WITH DUE CARE, MAKE ITS OWN STUDY AND EVALUATION OF EACH SECURITY THAT IS UNDER CONSIDERATION FOR PURCHASE, HOLDING, OR SALE.

All Fitch Ratings (Fitch) credit ratings are subject to certain limitations and disclaimers. Please read these limitations and disclaimers by following this link: https://www.fitchratings.com/understandingcreditratings. In addition, the following https://www.fitchratings.com/rating-definitions-document details Fitch’s rating definitions for each rating scale and rating categories, including definitions relating to default. Published ratings, criteria, and methodologies are available from this site at all times.