One of the many incisive lessons from Charles Dicken’s Great Expectations is how quickly a new environment can alter our perceptions and make us forget from where we came.

Just like young Pip who forgets his humble roots and comes to demand great things from his London high society life, only to be disappointed, today’s investors and forecasters have become accustomed to a high return, low volatility, upside-surprise-driven macro and market environment.

Coming into 2025, and previewed in December 2024, everywhere we look, we see evidence of great expectations that investors hold for the economy and markets.

From recession probabilities getting removed from forecasts, to Fed Chair Powell repeatedly expressing that he “feels really good” about the U.S. economy, to hopes for “just the right stuff” from DC policy, to equity strategists raising their S&P 500 targets by the greatest degree ever, to equities trading at stretched valuations, to aggressive flows into and positioning in equities, and finally, to credit spreads trading near multi-decade tight levels, it is clear that the spoils of the last two years have driven investors to expect great things from the economy and markets in 2025.

This is not to say that just because (almost) everyone is expecting great things that great things cannot happen this year. There are, after all, two whole economists calling for a recession and two entire strategists expecting a down year for the S&P 500 in 2025, and there could be zero (we say facetiously).

But in all seriousness, the U.S. economy and markets do have a lot of great things going for them, including the potential for profit-friendly policy and reforms, a still-tight labor market, the potential for the spark of animal spirits that could drive business investment, and the U.S. being the global epicenter of highly profitable technology innovation.

All of these factors suggest that optimism is warranted, but we must acknowledge that optimism is now crowded.

We often quip that for markets “starting points matter”. This is a way to encapsulate that markets are a constant dance between expectations and reality.

As any investor that has ever seen a stock go up on negative news and down on positive news knows, reality may play out as expected, but if markets have already fully priced in this reality, it is a non-event.

However, more often than not, reality surprises or significantly diverges from broadly held expectations, which is why we must question consensus when it is so crowded.

One of our favorite quotes, which we used for our 2H23 outlook, is Johann Wolfgang von Goethe’s opining that, “few people possess the imagination for reality”.

In 2023 and 2024, few people could imagine a reality of strong economic growth and robust risk asset returns. In 2025, it seems that few people can imagine a reality of weaker growth and soft risk asset returns.

Let us be abundantly clear, we are not calling for a recession or a cataclysmic market outcome for 2025 (we reserve the right to change our minds), but we do challenge the consensus notion of another relatively quiescent year of high returns and persistent, large upside surprises to growth.

Note that our view for the last two years has been that the U.S. economy would not experience a recession and that forecasters were significantly underestimating the economy’s growth potential due to the reduced sensitivity of the aggregate U.S. economy to short-term interest rates. Where we have been most surprised to the upside has been in the equity and credit markets’ ability to see an enormous re-rating higher in valuations, which are now pricing in, with great expectations, the continuation of this robust growth.

Our base case for 2025, which we detail below and in the linked charts, is for no U.S. recession this year but slower economic growth, with bond and equity markets trading in wide, choppy ranges through the year as they digest today’s high valuations and positioning.

We think that where the bond and equity markets end exactly on December 31, 2025, is far less important than how investors handle the volatility we expect to present itself over the course of the year.

The market has a way of tempering crowded great expectations (to the upside and the downside!), so as this process of tempering progresses in 2025, we do think that investors will be presented with opportunities to take advantage of volatility, as forward return prospects begin to improve.

In addition to seeing volatility as opportunity, we think that this lower return world for risk assets also makes two additional points increasingly important in 2025. The first is that asset classes that have less correlation to equity and credit risk are now more attractive given the starting point of valuations. The second is to acknowledge that what you keep at the end of the day could be just as important as the index level return, making tax and fee efficiency paramount and achieved through a comprehensive wealth strategy and asset allocation plan.

Overall, 2025 is bound to be a year of Dickensian-quality plot twists. As the data progresses, we could find ourselves updating our forecasts in material ways. The starting point of great expectations and distinct policy uncertainty makes keeping a level head in the face of volatility, remaining disciplined about investment styles and opportunities, and staying resolute in the pursuit of long-term plans as important of principles as they have ever been.

We wish you all a prosperous 2025 and look forward to working with you through what is bound to be a fascinating year.

-Cameron Dawson, CFA®

Chief Investment Officer, NewEdge Wealth

2025 Outlook Materials & Full Report

Written By: NewEdge Wealth Investment Team

Table of Contents

1. Economic and Policy Expectations

Economic and Policy Expectations

While we expect growth to moderate from 2024’s robust 2.7% pace, we do not expect a recession in 2025 at this time. Our 2024 construct of a Strange Landing still holds, as classic economic data relationships remain heavily distorted, making traditional indicators or cycle analysis a prone to delivering misleading signals.

The outlook for 2025 needs to begin with an acknowledgement of what kept real GDP growth strong in 2023 (+2.9%) and 2024 (+2.7%), while allowing inflation to moderate in the wake of an aggressive Fed hiking cycle. We see the following factors:

- The U.S. economy has exhibited less sensitivity to short-term interest rates this cycle

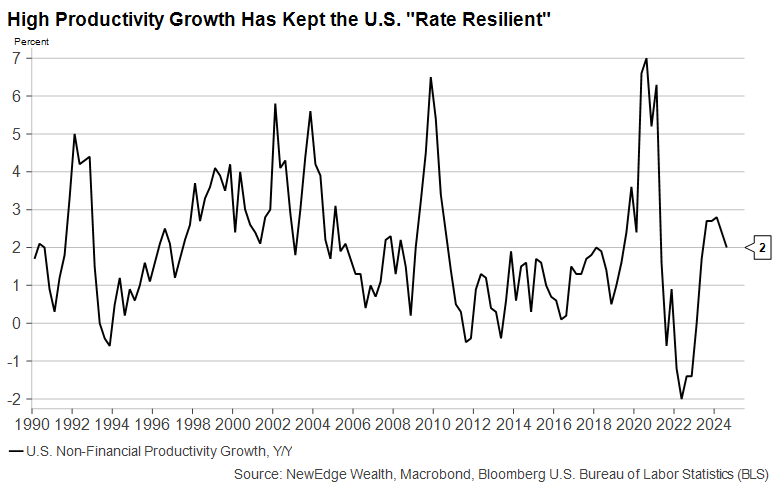

- Productivity growth surged following its COVID-era plunge during the “The Great Resignation”

- The working-age population soared due to an influx of immigrants supplying low-cost labor

- Treasury funding actions kept bank liquidity ample despite Fed tightening and high deficits, which allowed for strong asset prices that fueled a powerful wealth effect

- AI-related tech investment driving business investment

The great expectation of 2025 is that all, or at least most, of these factors will continue to help foster disinflationary economic growth.

Our view on 2025 is that many of these tailwinds will remain but their effects will diminish, meaning growth remains positive but at a slower pace. We do acknowledge, though, that there are risks that some of these factors turn into outright headwinds, mostly due to policy decisions.

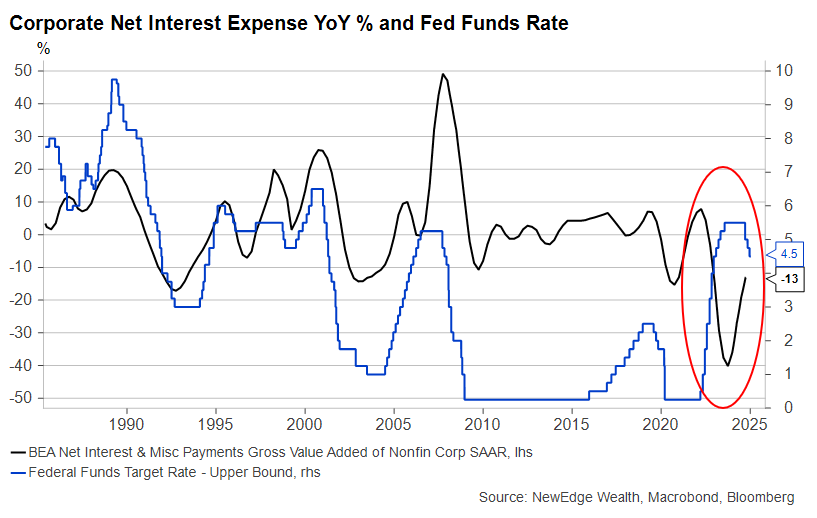

Let’s begin by assessing the dampened sensitivity to short-term interest rates. Our key thesis calling for stronger growth over the last two years has been that the U.S. economy is less negatively sensitive to short-term interest rates than it was in prior cycles due to corporations and households terming out of debt during the aggressive COVID-era easing that drove long-term interest rates to record lows.

For corporates, this dynamic caused a fruitful anomaly in 2023 and 2024, where Corporate Net Interest Expense (the difference between interest paid on debt and interest earned on cash) actually fell as the Fed raised rates, instead of rising as it had in prior cycles. In aggregate, borrowers are benefiting more from higher cash yields than they are seeing interest costs go up (there is a similar dynamic for households, given that 95% of mortgages were fixed rate at the start of the Fed’s hiking cycle).

As of 1/13/25

The chart above shows that this dynamic remains a tailwind, but it is less of a tailwind. This is partially due to the Fed cutting rates by 100 bps and reducing cash interest income, but we are also starting to see COVID-era debt begin to be refinanced at now much higher rates. This refinancing steps up in 2025, but the wall of refinancing isn’t huge until 2028 (S&P Global).

We have observed that there has been a “Survive to 2025” mentality for many borrowers who held hope for much lower rates in 2025 as the Fed delivered cuts. Now, as long-term yields have spiked higher post the Fed’s first set of cuts and further cuts are being questioned, we could begin to see high interest rates weigh more materially on investment and hiring decisions. This is certainly a risk for cyclical, interest-rate sectors like housing, construction, and manufacturing.

Looking to fiscal policy, these same high interest rates could potentially hinder policymakers’ abilities to deliver on great expectations for fiscal easing (such as big new deficit-expanding tax cuts). If long-term interest rates continue to rise on deficit fears, passing further stimulative legislation, given the current debt burden, is likely to be a distinct challenge.

As of 1/13/25

Further, just as Dickens’ Pip learned that great things often come at a cost, the benefits of deregulation and tax cuts from the new administration threaten to be offset by growth-disruptive, and potentially inflation-exacerbating, tariff and immigration policy, along with other “pay-fors”. This policy uncertainty is acute and does have the potential to significantly influence economic outcomes.

Outside of policy, driving our expectation of resilient, albeit slower, growth is the stability in the U.S. labor market that has fueled U.S. consumers’ buying power, as real wage growth has been positive in the last year.

There are two key requirements for this resilient consumer outcome to continue:

First, we likely need to continue to see improving productivity that allows corporate margins and profitability to expand. If productivity wanes, as it looks to have done in recent months, the slowdown in hiring we have seen over the last two years could morph into increased firing. This would then dent household incomes and could cause the current healthy consumer debt-to-income ratios to deteriorate materially. Increased firings, along with elevated interest rates, disproportionately hurt low-income consumers who rely more on wage income and revolving debt.

As of 1/13/25

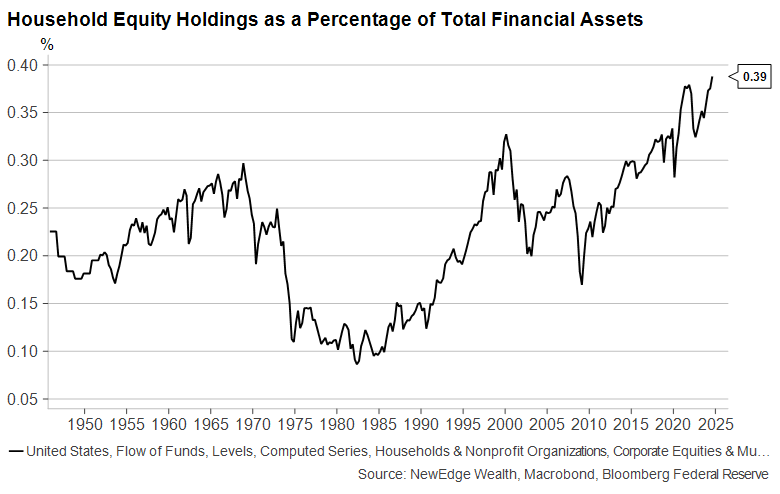

Second, for the U.S. consumer to remain resilient, we likely cannot experience a deep, protracted equity market correction. High-income consumers have been outpunching their weight in driving overall U.S. Household Consumption, with this strong spending behavior thanks in part to the powerful wealth effect achieved of the last five years. With household equity allocations at all-time highs and investor leverage levels elevated, a deeper equity market correction could be the biggest risk to high-income households’ willingness and ability to spend.

As of 1/13/25

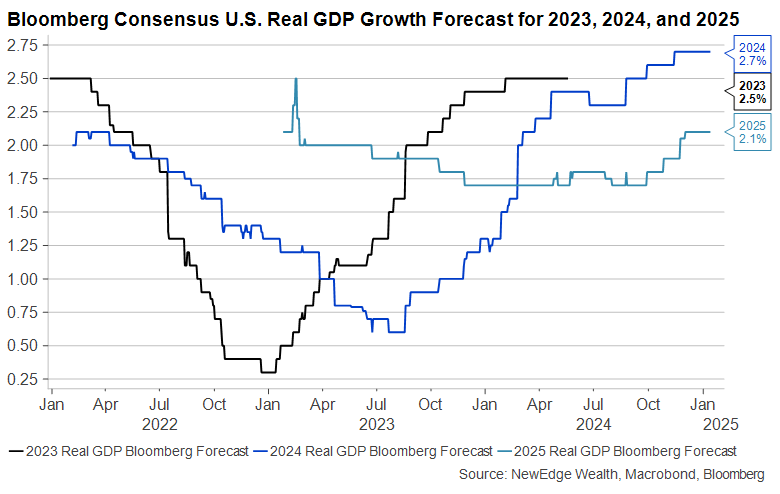

Overall, we continue to see the chart below as “the most important chart for markets”. It shows the progression of GDP forecasts for 2023, 2024, and 2025. The persistent climb in GDP forecasts was the underpinning driver of powerful equity and credit returns over the last two years. At this time, we do not see evidence of significant downside to the current 2.1% forecast for 2025 GDP, but we also see far less upside to forecasts compared to where 2023 and 2024 began. Remember, starting points matter!

As of 1/13/25

Upside Scenario: Just the Right Stuff

To get to the upside scenario of this 2.1% forecast, we likely need to see long-term interest rates moderate in order to reduce pressure on interest rate-sensitive, cyclical parts of the economy like housing. (Can yields fall as growth forecasts rise? They did in May-September last year, when the 10 Year fell 110bps, during which there was a brief growth scare, but GDP forecasts ended the period 20bps higher.)

Other factors that could contribute to higher growth include a continued boom in tech/AI investment, another jump in productivity, strong asset price returns sustaining consumers, and a surge in animal-spirits/deregulation-driven business investment.

We also think that policy needs to thread a tight “just the right stuff” needle to be beneficial to growth, where pro-growth tax cuts, deregulation, and fiscal stimulus is prioritized over tariffs, immigration, “pay-fors”, and fiscal prudence. We think markets currently have great expectations that they will get “just the right stuff” based on equity and credit risk pricing and forecasts for growth.

Downside Scenario: Whoops!

We are calling the downside scenario for growth, Whoops!, as policy could play a distinct role in driving a descent into weaker growth.

This Whoops! could include the Fed being behind the curve with a “higher for longer” interest rate stance just as rates are beginning to bite broad growth in a more material way. Relatedly, we could see the long end of the bond market become untethered due to tone-deaf deficit spending or challenges in funding deficits (new Treasury Secretary Bessent’s Bills, Bills, Bills predicament). Higher long-term rates would further weigh on interest rate-sensitive parts of the economy, such as housing and manufacturing. The 110 bps jump in 10 Year Treasury yields since the Fed began its 100 bps of rate cuts in September is a real-time example of this untethering.

As of 1/13/25

We do not see the political will or voter demands to pursue austerity at this time. However, if this became a goal, budget cuts would weigh on GDP growth in the near term.

In more potential Whoops! drivers, tariff and immigration policies all have the potential to weigh on growth and/or fan inflation by roiling supply chains and labor.

An exogenous inflation shock from rising oil prices would be a distinct headwind to the powerhouse U.S. consumer, who has been enjoying falling energy prices over the last two years.

As of 1/13/25

A rising USD due to fiscal or monetary policy decisions, both at home and abroad, could also weigh on corporate profitability and export growth.

We do not see a credit crisis emerging yet in 2025, but we are keeping a close eye on deteriorating credit standards, stable-for-now leverage levels, and increasingly aggressive risk-repackaging activities, like Synthetic Risk Transfers bought by private credit managers.

On inflation, we are expecting inflation to slowly moderate but remain sticky above the Fed’s 2% target. At this time, we do not see signs of an endogenous reacceleration of inflation, with key inputs like wages and rents showing signs of moderation. As mentioned above, we do not rule out an exogenous inflation shock, like rising oil prices or tariff/immigration policy. This shock could significantly restrict the Fed’s “degrees of freedom” to ease policy any further and potentially reintroduce interest rate hikes to the conversation.

Fixed Income Expectations

10 Year

We expect the wide, volatile range for the 10 Year Treasury yield that framed 2024 to persist in 2025.

We see potential for a retest of the 2023 high of 5% or even higher in the event of the fiscal policy “Whoops!” scenario outlined above. At some point, we expect the U.S. economy to experience a growth scare in 2025, which will likely be the source of an eventual, potentially temporary, downside to yields.

As we will discuss in equities, this creates an environment for bond investors, both taxable and municipal, to potentially buy and extend duration on yield spikes, and to exercise patience when yields fall. We are beginning the year with a yield spike, which has made select after-tax municipal yields increasingly attractive for buy-and-hold investors.

2 Year

The 2 Year will be the Fed’s storyteller in 2025. With the current Fed Funds upper bound at 4.5%, today’s 4.38% is pricing in little incremental easing and even the potential for further hikes. Inflation fears will cause the 2 Year to jump higher (pricing in hikes), while growth fears will cause the 2 Year to plunge lower (pricing in cuts). We expect volatility to remain elevated and the wide trading range to persist as the market debates the Fed’s next steps amidst the fog of DC/fiscal policy uncertainty.

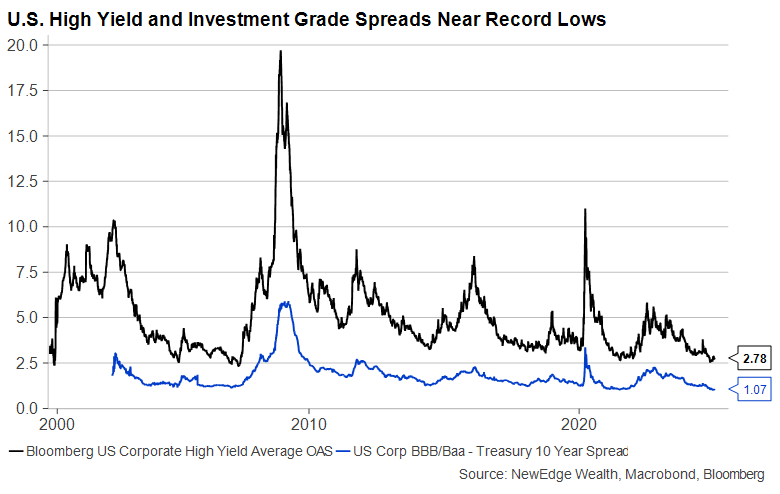

Credit

For credit, we continue to see spreads priced for perfection, contemplating no growth slowdown whatsoever. This sets up for higher spreads and potential credit underperformance in the event of a mild growth scare.

As of 1/13/25

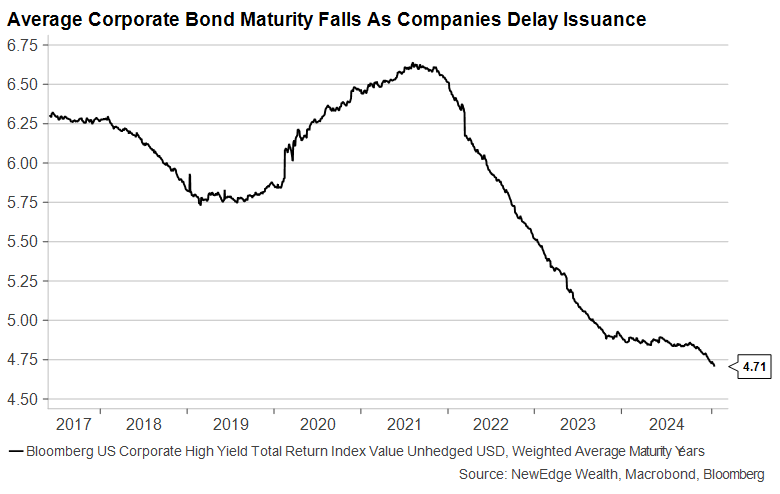

Tight spreads are partially a function of high demand for still-elevated all-in yields, met with scarce supply as corporate borrowers delay issuance in hopes for lower rates. As the chart below shows, the average high yield corporate bond maturity has fallen to a new record low as more companies wait to refinance/raise new debt. The “Waiting for Godot” effect of hoping for lower rates that now may not materialize could force companies that must refinance soon to offset higher borrowing costs with slower capital and labor investments.

As of 1/13/25

Equity Expectations

The all-important starting point for equities in 2025 is filled with great expectations.

Signs of these great expectations include:

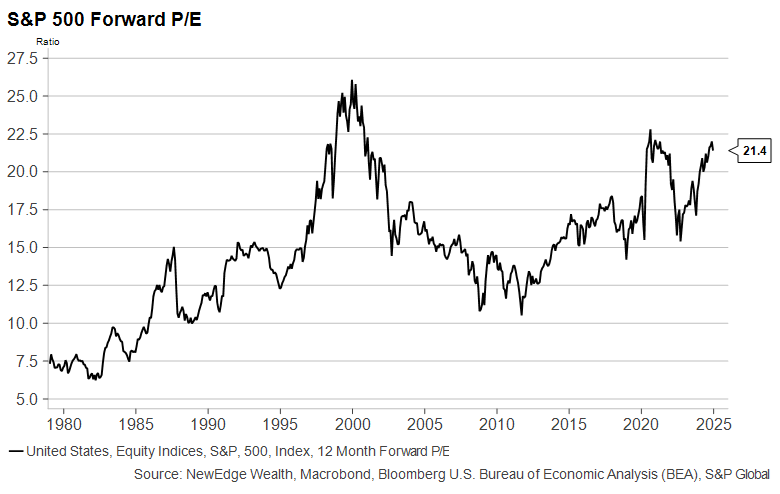

- Elevated PE multiples at 21.4x forward for the S&P 500 (as of 1/13/25)

- Fulsome EPS growth forecasts of 15% (FactSet)

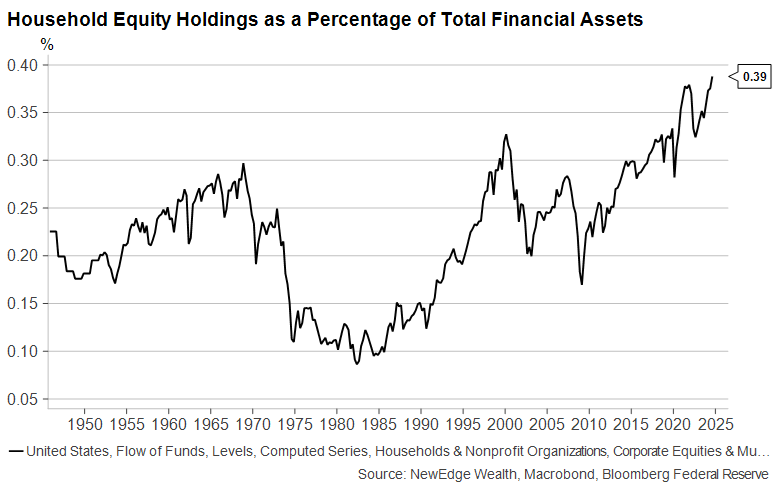

- Household equity allocations near 20-year highs for AAII (1/13/25) and all-time highs in Fed Flow of Funds data (12/24)

- Institutional positioning in the 90th percentile (Deutsche Bank, as of 12/12/24)

- Margin loan debt +45% in the last year (FINRA)

- Huge inflows into options and leveraged ETFs

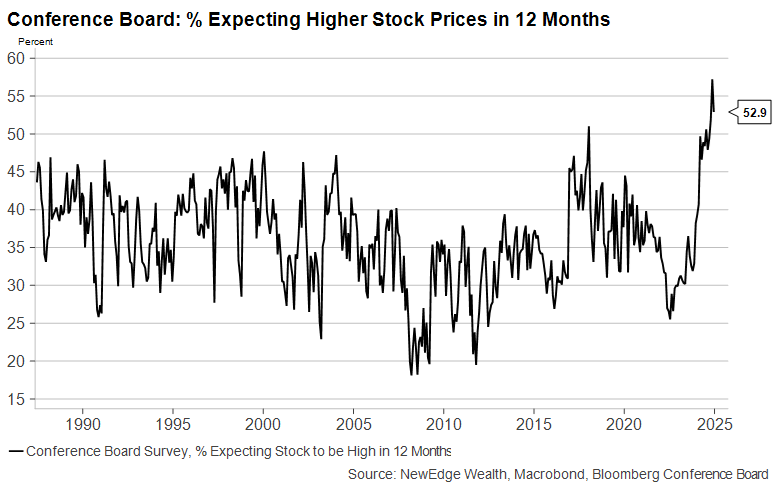

- Record sentiment readings of investors expecting positive returns (Conference Board, as of 12/24)

Sentiment, valuations, and positioning are poor timing tools, as extreme readings can persist and get even more extreme, but it is fair to say that the starting point for 2025 has far loftier expectations than 2023 and 2024.

As of 1/13/25

As of 12/2024

Renaissance Macro’s Jeff DeGraff has also made an important point to go along with the acknowledgement of stretched sentiment: momentum as faded. Late 2023 had a huge momentum surge that set the stage for 2024’s blockbuster year. 2025 begins with high hopes but no momentum surge, suggesting potential chop ahead.

2025 Brings Back the 80’s Greats

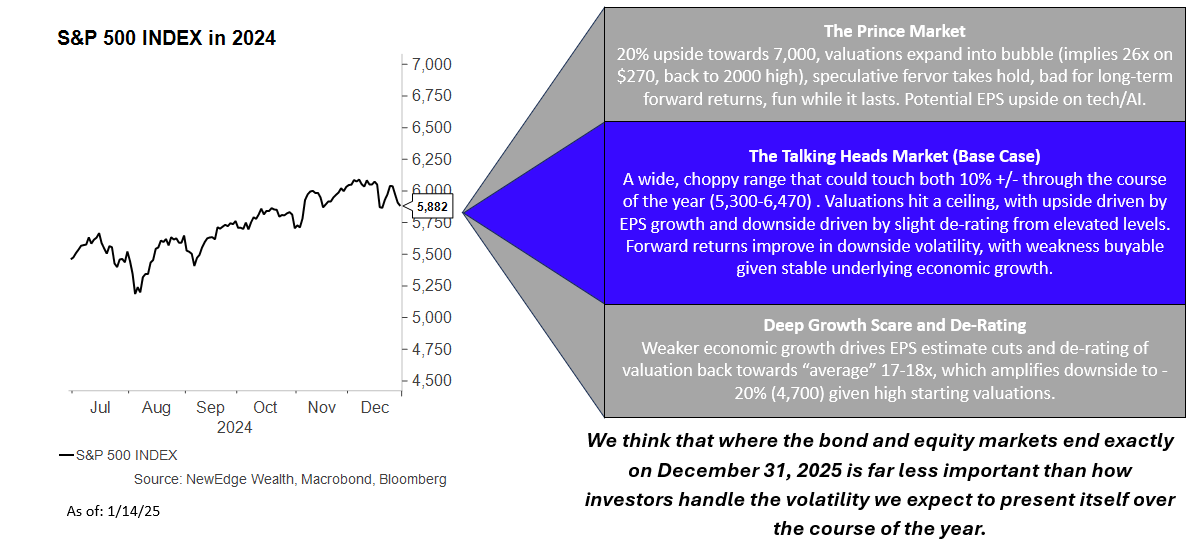

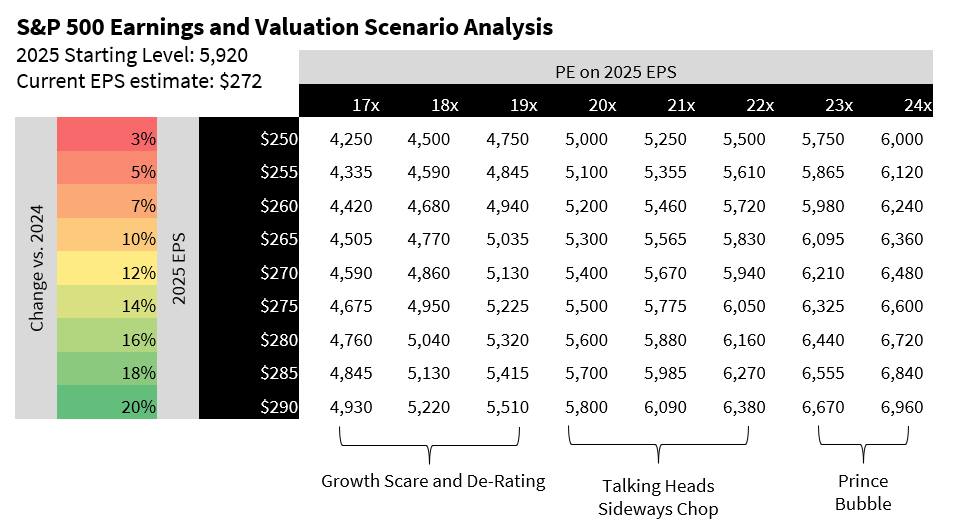

We see two scenarios for equity returns in 2025: our base case is a wide, choppy range with moderate returns at best, but we also see a lower probability potential for another 20%+ year that propels us into bubble territory.

Our base case of a wide range and moderate-returns-at-best scenario is likely the healthiest outcome for the long-run bull market, even though it may not feel great in the short run. This sideways action would allow equity markets to grow into their elevated valuations, assuming continued solid earnings growth. We are calling this The Talking Heads Market, as equites go on “The Road to Nowhere”, but experience volatility throughout the year that creates opportunities for investors to rebalance. We think 2025 could look like 2015 or 2018 in its volatility. Overall, the long-term U.S. large-cap uptrend is still intact, and the economic backdrop, though moderating, is still broadly supportive of risk assets, but the great expectations starting point creates a setup for choppy trading.

As mentioned in the introduction, we think that where the bond and equity markets end exactly on December 31, 2025, is far less important than how investors handle the volatility we expect to present itself over the course of the year.

Our second, lower probability scenario is the potential for another gangbusters year of returns driven by technological optimism, supportive/stimulative policy, ample liquidity, and a spark of speculation. We are calling this The Prince Market, as investors “Party Like it’s 1999” and sing “Let’s Go Crazy” to accompany equities entering bubble territory. The historical parallel is 1998’s Fed easing that catalyzed the parabolic move in the Nasdaq to a peak in March of 2000, a high that was not surpassed until 2014.

In this Prince Market scenario, investor discipline is paramount given the temptation to chase low quality, runaway asset prices and even juice returns with leverage. Participating in market upside through beta (until trend breaks occur), maintaining focus on long-term quality and valuations, and controlling leverage risk levels would be important principles in this bubble scenario, which we do see as a lower probability.

We note the key downside risks for equities in 2025, beyond our expected choppy volatility, would be deeper downturn in growth that causes both EPS estimate cuts and valuation multiple de-rating on growth fears and risk aversion.

Source: NewEdge Wealth, Bloomberg, as of 1/13/25

Valuations

The difference between the sideway chop and bubble scenarios is how equity valuations will track in 2025. Simply, if 2024’s 22.5x forward PE multiple on the S&P 500 acts as a ceiling, then the Talking Heads will prevail, however, if multiples blow past the 2020 highs and trade to 23x or higher, it’s time to break out the purple velvet jacket.

As of 1/13/25

Consensus is calling for “stable” PE multiples through the year to allow for ~15% equity returns driven primarily by EPS growth. History suggests that PE multiples are rarely stable, though (they are, after all, fickle compilations of expectations for earnings growth, returns, interest rates, and those pesky emotions of fear and greed).

Since 2000, the average annual range of the S&P 500’s PE multiple has been 22% of the average multiple for the year, meaning even in a year like 2015 where valuations ended roughly where they began, the range experienced in the year was a volatile 16%. The one exception to this was the low volatility year of 2017, where PE multiples only ranged 8% and steadily climbed along with EPS estimates throughout the year. However, if the average range of 22% were to be experienced in 2025, on $270 of EPS for the year, it would imply a 1,000-point range for the S&P 500 through the year.

We do acknowledge (and have written about) the superior constitution of today’s S&P 500 with its larger weights to higher quality and vastly more profitable companies, which suggests that maybe average valuations can trend higher through cycles, but that does not mean we should cast historical valuation ceilings to the side.

Overall, today’s high starting valuations leave little cushion to absorb growth scares or interest rate spikes, as we have seen recently, with the S&P 500’s PE multiple falling nearly 6% in the last month as yields have jumped higher.

Earnings

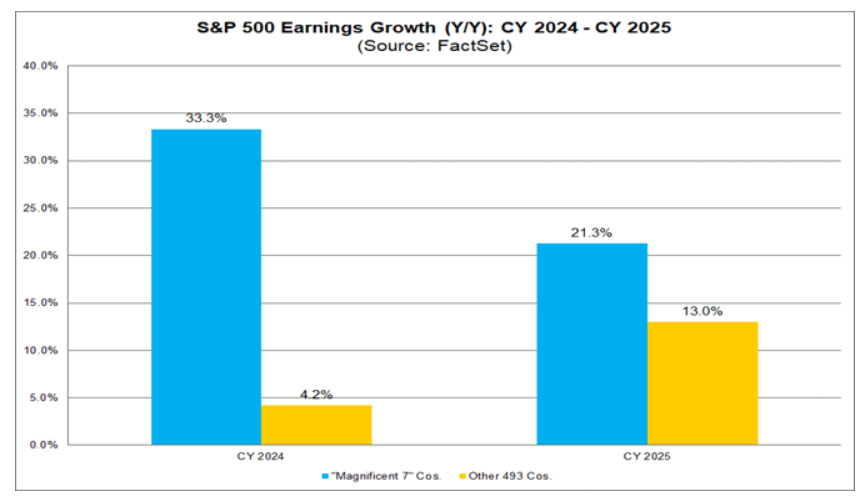

On earnings, we note that aggregate S&P 500 earnings have been largely stable and accurate in recent years. 2023 estimates were revised lower by just 3% throughout that year, and 2024 estimates ended the year exactly where they began. The current 2025 consensus is for $272/share, implying accelerating earnings growth from 9% in 2024 to 15% in 2025 (FactSet).

This forecast bakes in great expectations of both accelerating revenue growth to nearly 6% and a 100 bps jump in operating margins to a record high. Both of these components could be a challenge in a decelerating nominal GDP growth environment, but after many years of upside margin surprise (mostly from Magnificent Seven profit machines), corporate America likely deserves the benefit of the doubt for now.

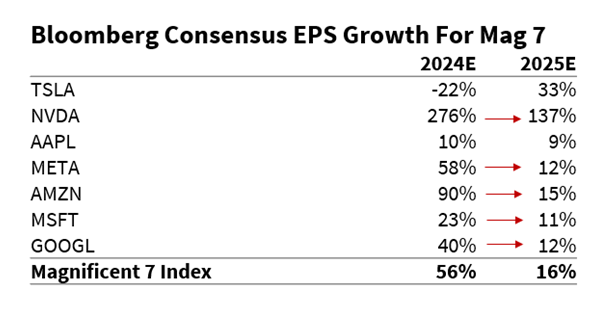

Where things get even more interesting is under the surface of the market, where analysts are forecasting a big recovery in the non-Magnificent Seven, 493 stocks; all the while, the Magnificent Seven is expected to decelerate its pace of growth materially.

Source: FactSet, as of 12-20-24

This “everything else” earnings recovery relies on big swings to growth for 2024’s disappointed sectors like Healthcare (expected to go from 4% in 2024 to 20% growth in 2025) and an acceleration in Technology earnings ex-NVDA’s decelerating growth (NVDA is 18% of the sector and its earnings are expected to decelerate from 144% to 50% in CY2025, but Technology sector earnings are expected to accelerate from 17% to 23%). We think this degree of broadening in earnings growth remains a “show me” story for the market as a whole.

Magnificent Seven and AI Watch Items

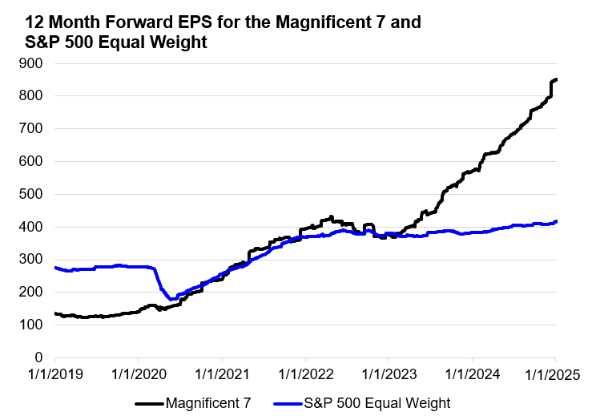

Given the Magnificent Seven’s 33% weight in the S&P 500 and the fact that these stocks accounted for over half of the S&P 500’s gains in 2024, the cohort is worth a closer look into 2025.

The Magnificent Seven’s dominant returns in recent years are thanks to the group’s dominant earnings growth compared to the rest of the index. Since the beginning of 2023, the Magnificent Seven has grown earnings by a massive 125%, compared to just 9% for the “average stock” Equal Weight S&P 500. Returns have been narrow because earnings growth has been narrow.

Source: Bloomberg, NewEdge Wealth, as of 1/4/25

As was outlined in the prior section, the pace of Magnificent Seven earnings growth is expected to moderate in 2025, while there are great expectations for a recovery in the average stock earnings growth. This suggests a moderation in the outperformance of the Magnificent Seven if both of these shifts occur.

Source: Bloomberg, NewEdge Wealth, as of 1/7/25

We see two key questions facing Magnificent Seven earnings growth in 2025. First, how sensitive are Magnificent Seven earnings to a cyclical economic slowdown, given their primary exposure to end markets that are sensitive to underlying growth like advertising and high-end consumer products (ex., 99% of META’s revenue is advertising)? The Magnificent Seven’s incredible profitability machine turns a good demand backdrop into fantastic earnings growth, but as we saw in 2022, if broader growth does slow, these businesses are not immune.

Second, when will we begin to see a return on invested AI capital, and how patient will investors be in waiting for this profitability? Hyperscalers like GOOGL, MSFT, AMZN, and META spent an estimated $250B on capex in 2024 and are expected to spend $300B in 2025, with these players also serving as NVDA’s largest customers and source of earnings growth upside. Mike Goldstein of Empirical Research Partners notes that these CapEx levels as a percentage of free cash flow are actually in line with market averages, but some profitability metrics have started to fray. If the return on AI investments is slower than expected, could we begin to see investors punish big AI spending? From another angle, we think a lower-than-expected CapEx guidance from one of the hyperscalers could be a potential negative market event to watch for in 2025, as it would imply a broader slowing in tech CapEx (which has been a key upside driver to both economic and earnings growth in 2024).

Leadership

In the sideways and choppy market scenario for 2025, we do see potential for leadership rotations, but the durability of these rotations depends largely on the trajectory of relative earnings growth.

The chart below shows the current consensus expectations for various indices, which firmly bake in great expectations for a broadening out of earnings growth to include a much better performance from equal weight, value, and small-cap indices. However, as investors have learned time and again, just because consensus expects something, it does not mean it is going to happen.

Source: Bloomberg, NewEdge Wealth, as of 1/7/25

For example, the small-cap Russell 2000 had a similar setup to start 2024, with an expectation for +26% EPS growth. Instead, the index ended the year with earnings -19% (meaning the entire 2024 rally was multiple expansion largely on the hopes of lower rates in 2025). The Street is back at it again, with an expected recovery to +38% growth in 2025, but with persistently high interest rates and the potential for a moderating growth backdrop, we may be set up for another round of EPS estimate cuts in 2025.

Source: Bloomberg, NewEdge Wealth, as of 1/7/25

The end of 2024 also saw extreme outperformance from growth, momentum, Magnificent Seven, beta, and low-quality stocks/factors. This has created the potential for snapbacks in the relative performance of unloved, left-behind groups (such as Value), but as the small-cap example warns, in order for these rotations to be durable, earnings have to deliver on the great expectations shown in the table above.

These earnings dynamics lead to the following expectations for leadership and thoughts on positioning:

- We continue to emphasize the Quality factor, which lagged to the end of 2024 but has started 2025 strong as traits like consistent profitability, high free cash flow generation, and low leverage levels become increasingly attractive in a high interest rate, slower growth economic backdrop.

- We think investors can be balanced between Growth vs. Value, with Growth’s outperformance likely to moderate in 2025 given the Magnificent Seven’s (55% of the Russell 1000 Growth index) moderating earnings growth. As expected, we are seeing a snapback in value relative performance at the start of the year, but the durability of this rotation will depend on sectors like Financials, Healthcare, Industrials, and Energy to deliver on earnings growth. Valuation discipline within Growth is imperative given the risk of sharp multiple de-rating if interest rates remain elevated.

- We prefer Mid over Small-cap companies given the higher profitability and lower debt levels in Mid-Cap indices, which makes Mid-Cap stocks less acutely sensitive to the path of interest rates.

- We continue to prefer the U.S. over the rest of world, despite the international valuation discount, due to vastly superior earnings growth in the U.S. A reversal in the strong USD, along with a commodity rally, would be two factors we would need to see to grow more sanguine on non-U.S. equities.

- We think sector selection could be used to hedge portfolios against two-tail risks for 2025. To hedge against an exogenous inflation shock from oil prices, the Energy sector is key. To hedge against a growth scare/slowdown, stable/defensive sectors (Healthcare, Staples, Utilities), which have lagged significantly, could play a role. In both groups, selecting for earnings quality and durability is of the utmost importance, as all of these sectors are also home to “value traps” and weak return on invested capital stocks.

Alternatives Expectations

As we approach the investment landscape for the distinctly broad set of asset classes considered “alternatives”, we have outlooks for each individual asset class (which can be accessed in our chart deck), but we also see the following major themes driving the alternative investment landscape in 2025:

Our Overall Sentiment is Cautious Optimism: We are cautiously optimistic throughout private markets. We continue to see opportunities where unique manager skills and inefficient markets can drive enhanced returns.

Opportunities to Diversify into Uncorrelated Asset Classes: Given the great expectations set up for public equity and credit markets in 2025, we see merit in finding return streams that are much less sensitive to the vagaries of these public markets. We make a clear distinction between “crisis alpha” (assets like managed futures that do well when other markets do poorly), which we do not favor at this time, and “uncorrelated assets” (those that derive returns from factors unrelated to equity risk premium).

The Cost of Capital Has Shifted Investment Approaches: Across a variety of asset classes, from Private Equity to Private Real Estate, the effects of the higher rate environment continue to ripple through private markets. A higher cost of capital continues to put a greater onus on manager skill in operations and deal structuring, where classic financial engineering (counting on the cheap and ever-lower cost of funds to make return targets) is more challenging. We think the higher cost of capital also increases risk for previously overpriced or overleveraged deals that could buckle under the weight of higher for longer interest rates.

Disruption in Fundraising Cycles Creates Opportunities for Secondaries: Fundraising will continue to be challenged. As the IPO market and M&A activity have remained under pressure, exit activity has been stifled, thus preventing funds from making distributions necessary to maintain the “velocity of capital.” There is hope that M&A and IPO markets will defrost in 2025, but this return to dealmaking has been long delayed. Secondaries have been the beneficiary of this increasing need for liquidity, and we will continue to see opportunities across the LP-led and GP-led spaces.

Greater Manager Dispersion: We believe dispersion across manager performance will continue to widen, making the manager due diligence and selection process even more important. The higher interest rate, slower velocity of capital, tougher fundraising, and more uncertain operating environment will likely drive an even wider gap between top and bottom quintile performers.

Nimbleness is Rewarded: Investors with dry powder and fresh capital available in 2025 will be able to take advantage of investing in higher-quality assets at more attractive valuations and entry points.

AI/Technology Creates Opportunities and Pitfalls: AI is starting to be adopted across the spectrum. From the earliest stage, companies running leaner and doing more with less to large enterprises, finding ways to automate processes and increase efficiency. While providing many massive benefits, there are also some drawbacks, such as data security, as these platforms collect and warehouse massive amounts of data, which could be potentially harmful if stolen.

Thesis Driven Infrastructure: Infrastructure has emerged as an area of interest, exhibiting resilient cash flows in the face of public market volatility. The acyclical nature of infrastructure assets may present further opportunities through continued market uncertainty. This can include classic infrastructure, power generation (which is seeing a sharp increase in data center demand), digital infrastructure, transportation, and water rights.

Big Trends Create Big Opportunities: With shifting demographics and an aging population, there will be greater opportunities in healthcare, particularly healthcare enhanced by emerging technologies. Real estate as the need for senior living facilities continues to grow.

Selectivity in Democratization: The democratization of private markets has led to more investment vehicles with increased liquidity as well as lower investor qualifications as sponsors attempt to expand beyond institutional capital and access private wealth customers. There are risks inherent in broadening the audience for these investments, along with packaging illiquid assets in semi-liquid vehicles. The most benign of these risks is dampened returns, while the most severe could be fund liquidity crunches and forced asset sales.

Watching Regulations: Regulatory changes and increasing compliance requirements are influencing market operations, particularly around reporting, transparency, and data privacy, affecting deal structuring and compliance costs.

IMPORTANT DISCLOSURES

The views and opinions included in these materials belong to their author and do not necessarily reflect the views and opinions of NewEdge Wealth, LLC.

This information is general in nature and has been prepared solely for informational and educational purposes and does not constitute an offer or a recommendation to buy or sell any particular security or to adopt any specific investment strategy.

NewEdge and its affiliates do not render advice on legal, tax and/or tax accounting matters. You should consult your personal tax and/or legal advisor to learn about any potential tax or other implications that may result from acting on a particular recommendation.

The trademarks and service marks contained herein are the property of their respective owners. Unless otherwise specifically indicated, all information with respect to any third party not affiliated with NewEdge has been provided by, and is the sole responsibility of, such third party and has not been independently verified by NewEdge, its affiliates or any other independent third party. No representation is given with respect to its accuracy or completeness, and such information and opinions may change without notice.

Investing involves risk, including possible loss of principal. Past performance is no guarantee of future results.

Any forward-looking statements or forecasts are based on assumptions and actual results are expected to vary from any such statements or forecasts. No assurance can be given that investment objectives or target returns will be achieved. Future returns may be higher or lower than the estimates presented herein.

An investment cannot be made directly in an index. Indices are unmanaged and have no fees or expenses. You can obtain information about many indices online at a variety of sources including: https://www.sec.gov/answers/indices.htm.

All data is subject to change without notice.

© 2026 NewEdge Wealth, LLC