Wrapping up the Summer of Mud

In our second half outlook, we previewed what we called the Summer of Mud (or Mudd if, like us, you draw your inspiration from 90s rock bands). We did so in expectation that the mix of economic data and policy measures would provide no clear picture regarding the overall direction of the economy, and we hypothesized that this would prove challenging for risk assets like stocks and corporate bonds.

Summer comes to an official close this weekend, and it turns out we were half right. Economic data has been a muddy mix, but stocks have roared, and credit spreads have tightened, nevertheless. Even U.S. Treasuries and Gold have gotten into the act. Indeed, it’s hard to name a single category of financial instruments that provided anything short of stellar returns over the summer.

The question as we move into autumn is whether enough mud has been cleared away to provide clarity on the way forward for corporate earnings and economic growth and, ultimately, more good returns for investors. The second single off of John Mayer’s 2004 sophomore studio album Heavier Things, “Clarity” and its lyrics will provide the theme for this Weekly Edge.

An unusually muddy economic story

Did I sail through or drop my anchor down?

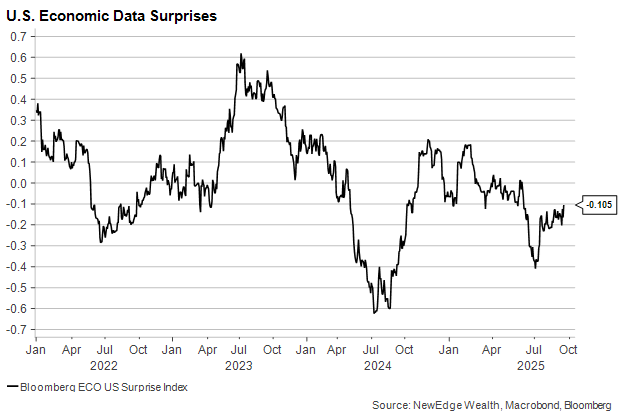

It’s certainly not unusual for forecasters to disagree about the outlook for the U.S. economy. Uncertainty about the future is part of the job for any macro economist. But today we are seeing wide disagreement about the present state of the economy. Economic data has generally surprised to the downside in Q3, but not to the same extent it did last summer.

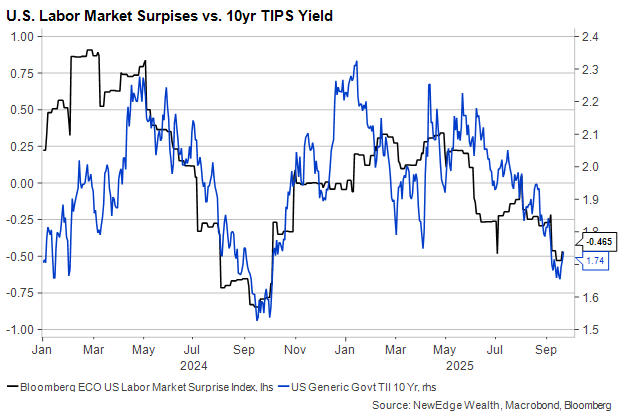

Look at the labor market and you’ll see clear signs of slower hiring and falling income growth. Throw in the fact that the job growth we thought we were seeing earlier in the year has been revised dramatically lower, underscoring that even previous economic conditions are not perfectly understood.

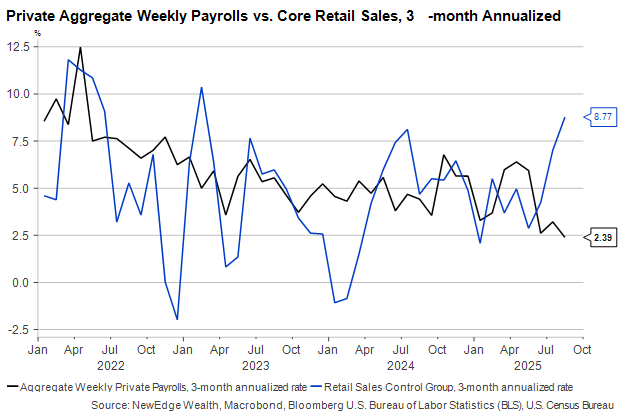

Look at the U.S. consumer and you’ll see mostly hopeful signs. Confidence measures are poor but have not (yet) translated into notably weaker spending. Retail sales growth was impressive in both July and August, even after accounting for the impact of tariffs on many goods prices. At the same time, aggregate private payroll growth (account for hours, wages and total jobs) has fallen to a multi-year low:

Divergences between consumer spending and wage growth do not tend to last long, as the graph below shows. But Moody’s this week released an update to its long running series estimating what share of total household spending is done by the top 10% of wage earners, who also tend to be homeowners with considerable savings. It’s now nearly 50% versus closer to one-third in the early 1990s. This means that consumer spending could remain more resilient than the labor market and rising household default rates would imply, as long as equity prices are rising. Households own a greater share of their wealth in stocks than ever before, and most of those holdings are concentrated at the top, making those earners less sensitive to a softer labor market.

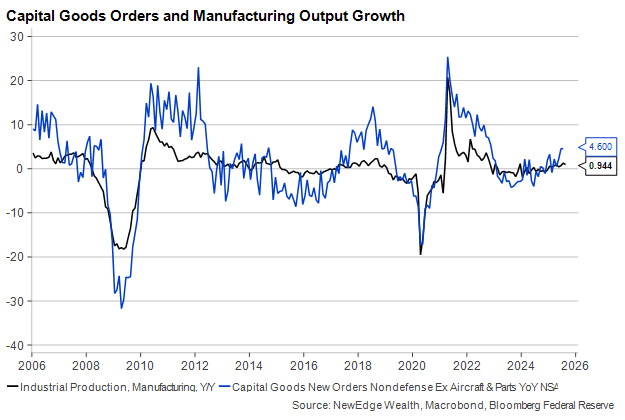

In the commercial sectors of the economy, there is a mix of hope and despair. Manufacturing output rose in August against expectations of a decline, and orders for capital goods have picked up.

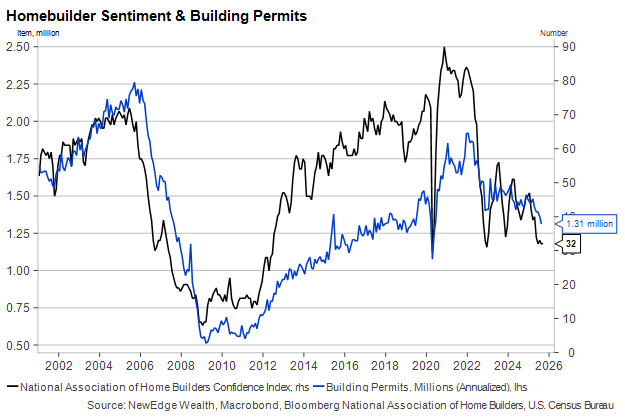

But, in the same month, residential construction fell deeper into recession. The summer drop in mortgage rates appears to have stirred a wave of refinancings, but homebuyer demand has not meaningfully picked up, and construction employment remains vulnerable.

But financial market returns have been uniformly positive

There’s a calm I can’t explain

Just about every major asset class we track has had a banner third quarter. Believe it or not, that includes U.S. Treasuries and TIPS, which had been out of fashion for nearly three years before rallying this year, especially over the summer. Here, it’s easiest to identify the driver of the performance: a softer labor market “unlocking” lower interest rates.

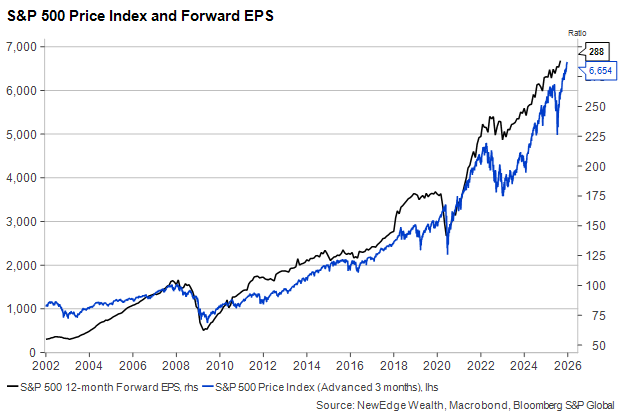

Large swaths of the equity market from Utilities to Homebuilders also benefit from lower interest rates, but we see earnings growth and upward revisions to that growth as the primary reasons stocks have performed so well over the summer. While it’s true that stock prices tend to lead earnings estimates, the Q2 reporting season beginning in July was one of the best in recent memory compared to expectations, propelling analysts’ estimates higher and providing support of valuations even at these lofty levels. We covered most of this story in last week’s report.

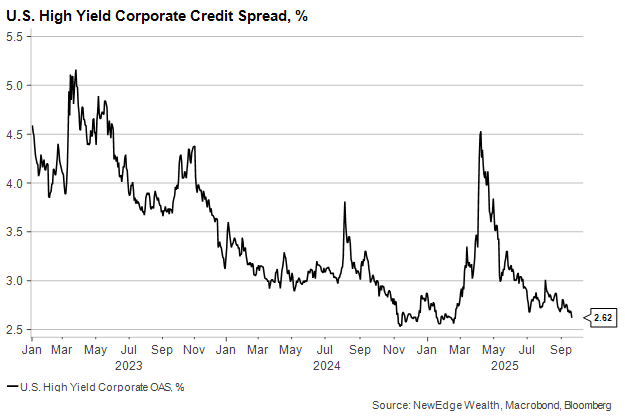

Lower borrowing costs and strong earnings growth is a solid macroeconomic backdrop for corporate balance sheets and investor risk appetite. Sure enough, spreads on below-investment grade corporate bonds have tightened nearly all the way back to where they started the year after the major disruption in April. Both investment grade and high yield corporate bonds have beaten U.S. Treasuries in Q3, because they benefit from both falling interest rates and narrowing spreads.

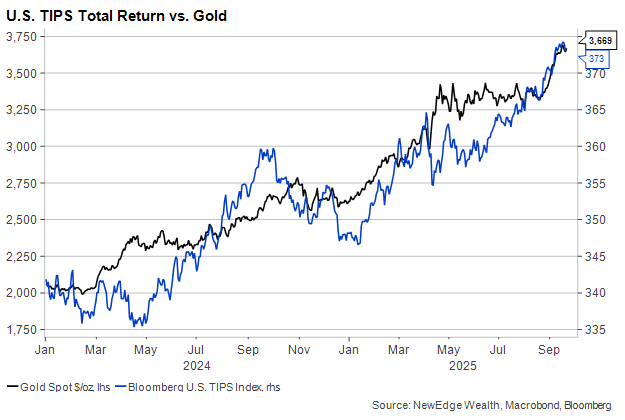

In the “other” category, real assets like gold and Treasury Inflation-Protected Securities (TIPS) have been among the biggest winners of the Summer of Mud.

Fed hopes have helped keep markets afloat as data has softened

And I will waste no time

Times of slowing economic growth can be consistent with surging market returns, providing the central bank is helping to boost confidence. The Fed’s summer pivot toward policy easing has been largely responsible for the rallies in Gold and sectors of the equity market like Homebuilders. The dream scenario in which the Fed lowers interest rates enough and in time to avert disaster has become reality since recession risks were seemingly at their most acute in early 2023.

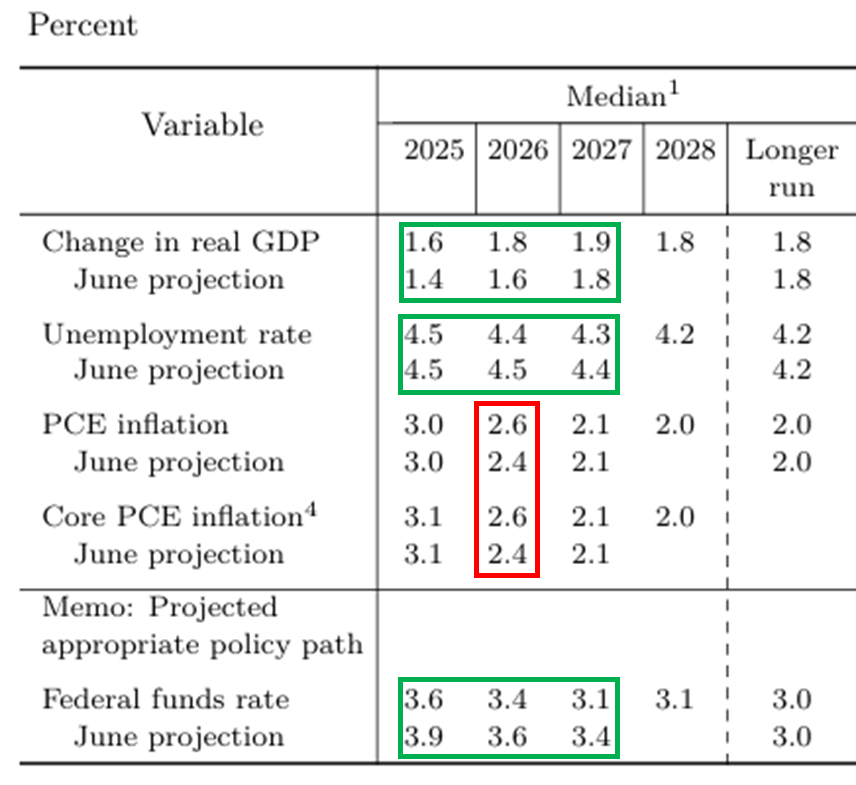

As the Fed embarked on its latest rate cutting effort last week, it delivered a set of forecasts that adds more mud than clarity to its reaction function. The median forecast is for stronger growth, lower unemployment and higher inflation through 2026 than was the case in June, yet the median path of interest rate cuts is deeper with a faster start. In other words, the need for rate cuts – in the Fed’s own eyes – has not changed materially since June, but their willingness to deliver the cuts has increased.

Source: Federal Reserve

Markets are still expecting two more cuts this year and a few more in 2026, leaving the terminal rate below 3%, lower than the Fed plans to go. We give the market somewhat more credence than the “dot plot” for now, because a) the Fed is going to be under new management by next Spring with at least one more dovish governor; and b) we are more concerned about the state of the labor market than current chair Jay Powell seemed to be at his post-meeting presser this week.

Despite Powell’s relatively hawkish tone, investors found nothing in the outcome of the Fed meeting to dissuade them from the view that policy will continue to ease, hopefully providing a lift to dormant sectors of the economy like housing.

A Nice Set Up for the Fall or for a Fall?

And I will wait to find if this will last forever

We haven’t heard (or used) the term “soft landing” in almost a year, but it may be time to break it out again with markets pricing in a 3% federal funds rate, stronger earnings growth and moderate inflation in 2026, with fiscal stimulus set to kick in a few months from now. A softer landing could scarcely be drawn up, even if the flight pattern to get us there was highly unorthodox.

As investors, however, we must ask what could go wrong from here. Given how optimistic market pricing and growth forecasts are, the risks to the outlook are skewed to the downside of current expectations. One way this could appear is through the consumption-income relationship reasserting itself and pulling down the consumer. In this scenario, stocks and rates could fall in concert if growth forecasts were trimmed.

The risk of tariffs squeezing corporate profit margins and denting household real incomes is also not going away anytime soon. Goods price increases are unlikely to peak until the third quarter of 2026, an unusual breed of inflation that lasts a long while but eventually leaves on its own. The damage in the interim, however, could come in the form of a weaker dollar and challenges to small businesses with tight margins and little recourse from import duties.

Rates might not fall in this scenario as much as they would in a soft landing, at least at first. But small-cap stocks supported by recent upward adjustments to earnings estimates could be most affected.

A final risk case, one that appears less likely to us but needs to be addressed, is one in which inflation returns organically in the form of higher services prices and the Fed is unable to “look through” inflation to cut rates. This scenario could undo a lot of rally in…well…just about everything since June. But it would be especially challenging for rate-sensitive bonds.

Upside risks to the outlook would come chiefly, we think, through the productivity channel. Some aspects of the One Big Beautiful Bill Act (OBBBA) encourage capital investment, and massive amounts are already being spent on potentially industry-changing alternative investment technology. Higher productivity could help offset the effects of slower job growth and keep wages high and margins wide.

Conclusion: Where we need the mud to clear

By the time I recognize this moment, this moment will be gone

If we could have one question magically answered for us about what’s to come in the fourth quarter, it would be this: Will U.S. payroll growth settle in a new lower steady state (a product of sharply lower population growth) or descend into negative territory, causing a sharp rise in unemployment?

Beyond that, we would like greater visibility on corporate earnings for Q3 and changes in guidance to the Q4 and 2026 outlook, mostly in the context of rising consensus forecasts for 2026 earnings. Another quarter of excellent results would at least, we think, prevent a meaningful correction in stock prices and ultimately raise the ceiling for equity index levels at year end.

Lastly, we’d like to know who will be running the Fed and how many allies the new Chair will have on the committee by next summer. A Fed majority intent on getting rates down quickly no matter what will have to contend with potentially unfriendly reactions in the currency and fixed income markets. This could cause brief periods of market volatility that threaten to become more prolonged if Fed credibility is seen to be at stake.

We expect more clarity as the summer mud washes away in the next few months, and we hope investors like what they find underneath.

IMPORTANT DISCLOSURES

The views and opinions included in these materials belong to their author and do not necessarily reflect the views and opinions of NewEdge Capital Group, LLC.

This information is general in nature and has been prepared solely for informational and educational purposes and does not constitute an offer or a recommendation to buy or sell any particular security or to adopt any specific investment strategy.

NewEdge and its affiliates do not render advice on legal, tax and/or tax accounting matters. You should consult your personal tax and/or legal advisor to learn about any potential tax or other implications that may result from acting on a particular recommendation.

The trademarks and service marks contained herein are the property of their respective owners. Unless otherwise specifically indicated, all information with respect to any third party not affiliated with NewEdge has been provided by, and is the sole responsibility of, such third party and has not been independently verified by NewEdge, its affiliates or any other independent third party. No representation is given with respect to its accuracy or completeness, and such information and opinions may change without notice.

Investing involves risk, including possible loss of principal. Past performance is no guarantee of future results.

Any forward-looking statements or forecasts are based on assumptions and actual results are expected to vary from any such statements or forecasts. No assurance can be given that investment objectives or target returns will be achieved. Future returns may be higher or lower than the estimates presented herein.

An investment cannot be made directly in an index. Indices are unmanaged and have no fees or expenses. You can obtain information about many indices online at a variety of sources including: https://www.sec.gov/answers/indices.htm.

All data is subject to change without notice.

© 2025 NewEdge Capital Group, LLC