This pain you gave to me

Can you take it all away?

– Blurry, Puddle of Mudd

“Time flies when you’re in interesting times.”

That is how we opened our mid-year 2025 Outlook this past Wednesday (you can watch the replay above) and boy isn’t it the truth!

Here we are already, a blink away from the beginning of July, and the year has positively flown by.

Investors have certainly had to stomach bouts of high volatility caused by these “interesting” times, but for all the chop and churn, returns have actually been rather healthy. In fact, a straight 60/40 portfolio, made up of 60% Equities in the All-Country World Index (ACWI) and 40% Fixed Income in the Bloomberg U.S. Aggregate Bond Index has returned a sturdy 7.2%!

In a departure from the last 15 years, and a welcome reward for diversified investors, the key boost to this 60/40 global stock and bond portfolio has been non-U.S. stocks. The EAFE International Developed Index has risen an impressive +18% YTD, the MSCI Emerging Markets Index +15%, and the S&P 500 a mere +5%.

We’ve been quipping that in 2025 diversification no longer means having to say, “you’re sorry”, it means getting to say, “you’re welcome” (for once!).

So, despite the headlines, the volatility, and the uncertainty, diversified portfolios have fared well in 2025. This, of course, raises the question of what the rest of the year has in store for investors. We aimed to address this question with five “big” questions in our mid-year outlook, with links to the video and the slide deck included below.

We titled our mid-year outlook “The Summer of Mudd”, in recognition of how muddy the data, policy outlook, and economic growth backdrop is likely to be in the coming months.

Data is getting muddied by distortions that tariffs have had on household and business buying behavior and sentiment. Policy is muddied by the decisions to “kick the can” on trade deals and tough negotiations around taxes and spending. Growth is muddied as the breakneck pace of 2023 and 2024 growth downshifts to a slower, muddle through type of environment, with limited near-term catalysts for reacceleration and continued signs of “fraying” in the labor market.

This muddiness paints an interesting backdrop for risk assets, which have roared higher since their early April lows, shrugging off headlines and uncertainty to return to prior highs.

We would like to take a moment to focus on one aspect of our outlook, in looking at the puts and takes for equity markets in the second half of 2025. We will do this today by contrasting today’s S&P 500 high with the high reached back in February.

If you recall, our 2025 Outlook was titled Great Expectations because everywhere we looked, that is what we saw. Stretched valuations, stretched positioning, ebullient sentiment, and high hopes for “only just the right stuff” out of DC and policy.

Fast forward to today, two items are relatively similar: stretched valuations and DC optimism.

The S&P 500’s 22.1x valuation has nearly returned to its late 2024 high of 22.6x forward (note that this is on a lower earnings base as estimates for 2025 and 2026 have been trimmed, but the 12-month forward numbers benefit from the inclusion of more of 2026’s expected rebound to 12%+ growth).

On DC optimism, the experience of “Liberation Day” has certainly sparked a more sober take on the policy possibilities coming out of DC, but we observe a return of optimism that trade deals will be penned, tax and spending plans will be negotiated (even if the end result is a net neutral to the economy), and that deregulation will provide a jolt to business activity.

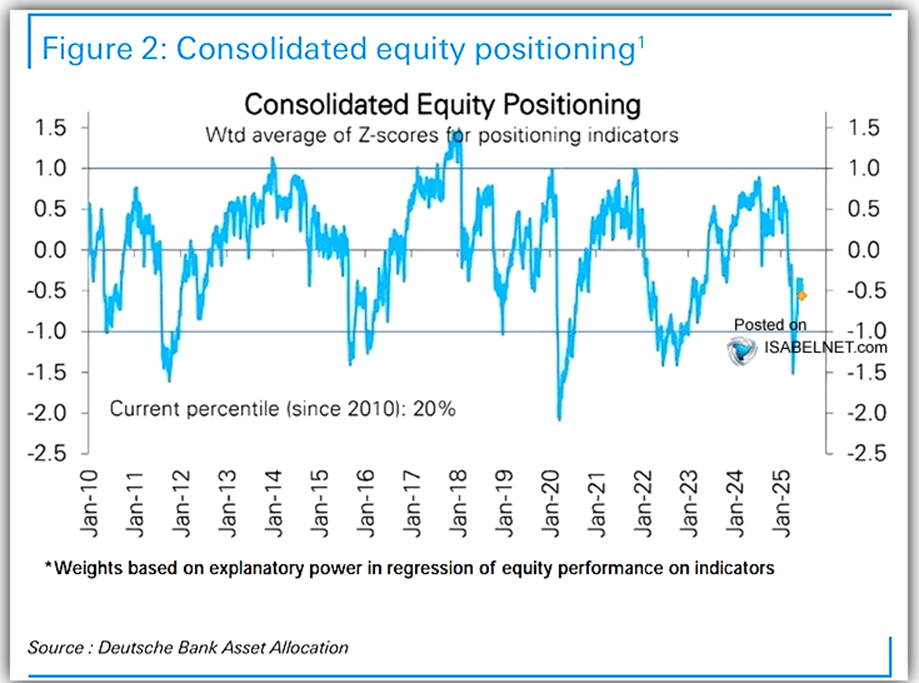

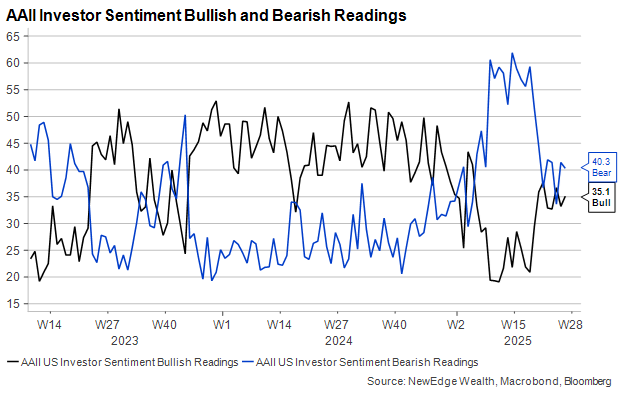

But the differences between today’s high and February’s high is where things get much more interesting. Despite the 27% rally on the S&P 500 from the intraday low on April 9, we still observe positioning that remains light and sentiment that remains constrained. The Deutsche Bank Consolidated Equity Positioning Index had its latest update last Monday and is merely in the 20th percentile, still in relatively underweight territory (the hesitance of this index to rebound at least to neutral has been the most surprising characteristic of this rally). The AAII Investor Sentiment Survey still has Bears outnumbering Bulls. Both measures are shown in the charts below.

This set up of positioning and sentiment suggests that the “pain trade”, the direction of travel for stocks that catches the most investors flat footed, is still higher for the U.S. equity market. This does not mean that equities are not subject to bouts of indigestion, volatility, and surprise, which could be amplified by these lofty valuations, but it means that many investors are still in a position where they may have to chase markets higher in order to get fully invested. This creates an environment where dips are bought quickly and “melt ups” may ensue.

Unlike the policy, growth, and data backdrop, “muddy” may not seem to be the exact word to describe this equity market, which seems so resolute in its march to new highs. But we think that the medium-term outlook could be muddied, once light positioning and subdued sentiment are pulled higher and valuations find themselves at even-more-stretched levels. At this point, the earnings backdrop will be the key determinant if new highs can continue to be achieved, or if volatility will come for the “priced for perfection” market. Of course, the muddied data and muddle through growth environment will be an important consideration for earnings.

There is much more to unpack about our outlook for the remainder of the year, so take a look through the slides or even better, watch the presentation for a deeper dive about how we are seeing the economy and markets in this muddy but interesting remainder of 2025.

IMPORTANT DISCLOSURES

NewEdge Wealth is a division of NewEdge Capital Group, LLC. Investment advisory services offered through NewEdge Wealth, LLC, an investment adviser registered with the US Securities and Exchange Commission. Securities offered through NewEdge Securities, LLC, Member FINRA/SIPC.

The views and opinions included in these materials belong to their author and do not necessarily reflect the views and opinions of NewEdge Wealth, LLC.

This information is general in nature and has been prepared solely for informational and educational purposes and does not constitute an offer or a recommendation to buy or sell any particular security or to adopt any specific investment strategy.

The trademarks and service marks contained herein are the property of their respective owners. Unless otherwise specifically indicated, all information with respect to any third party not affiliated with NewEdge has been provided by, and is the sole responsibility of, such third party and has not been independently verified by NewEdge, its affiliates or any other independent third party. No representation is given with respect to its accuracy or completeness, and such information and opinions may change without notice.

Investing involves risk, including possible loss of principal. Past performance is no guarantee of future results.

Please remember that different types of investments involve varying degrees of risk, and there can be no assurance that the future performance of any specific investment or investment strategy (including those undertaken or recommended by NewEdge) will be profitable or equal any historical performance level(s). Clients should carefully consider their own investment objectives and never rely on any single chart, graph or marketing piece in making investment decisions.

Any forward-looking statements or forecasts are based on assumptions and actual results are expected to vary from any such statements or forecasts. No assurance can be given that investment objectives or target returns will be achieved. Future returns may be higher or lower than the estimates presented herein.

An investment cannot be made directly in an index. Indices are unmanaged and have no fees or expenses. You can obtain information about many indices online at a variety of sources including: www.sec.gov/answers/indices.htm.

All data is subject to change without notice.

© 2025 NewEdge Wealth, LLC