You might be surprised to learn that the market and the investment approach it demands in 2026 have a lot in common with Metallica. Yes, Metallica, the thrash metal band that formed in the 1980s and became known for its bone-rattling loudness, shows with flame-throwers, and (at the time) epic mullets.

The band’s early days remind us a lot of how the market progressed through the first half of 2026. Metallica was putting out great, quality thrash metal, but it took a decade until the release of their self-titled 5th studio album that they were properly appreciated by popular audiences.

In a similar way, the first half of 2026 saw fantastic positive earnings revisions in the early months of the year, but stocks did not appreciate these positive revisions until April, when the markets began to celebrate the ultra-powerful earnings growth coming from the “Nothing Else Matters”, dominant AI infrastructure trade.

S&P 500 Price and 12 Month Forward Earnings

Source: Bloomberg, NewEdge Wealth, as of 7-10-26

But as all musicians know, the hard part is not releasing the great, banger-filled album. That process often feels easy, natural, and startlingly clear. The hard part is creating the follow up to that successful album because the pressure for greatness has grown and expectations are high, setting a tougher environment for creativity and flow.

In Metallica’s case, their follow up 6th and 7th albums were panned by both fans and critics, as the band departed from its thrash metal roots (they cut off their mullets!) to embrace the hard rock sounds that were being made popular by bands like Soundgarden, Alice in Chains, and, dare we even say, Pearl Jam.

This awareness that following up success is often tougher than achieving the success in the first place is a helpful way to appreciate the dynamics of the second half of 2026.

The first half of 2026 had multiple record-setting strengths, such as the best positive earnings revisions when already in an expansion (earnings revisions are usually most positive when emerging from a recession), a 100th percentile run in high beta momentum stocks (meaning this cohort of stocks had one of its best winning streaks on record), and the best two month run for semiconductor stocks on record. This strength was chased and/or propelled by record-setting flows into leveraged ETFs and a historic drop in demand for downside protection (either through options or cash).

So, the question as we “Turn the Page” to 2H26 is if the US equity market can avoid the fate of mid-90’s Metallica and deliver a follow up 2H that is as strong as the 1H success.

We looked to answer this question as part of our 2H Outlook presented earlier this week (you can access the slides here and the replay of the presentation here), and here are a three key observations that are worth highlighting.

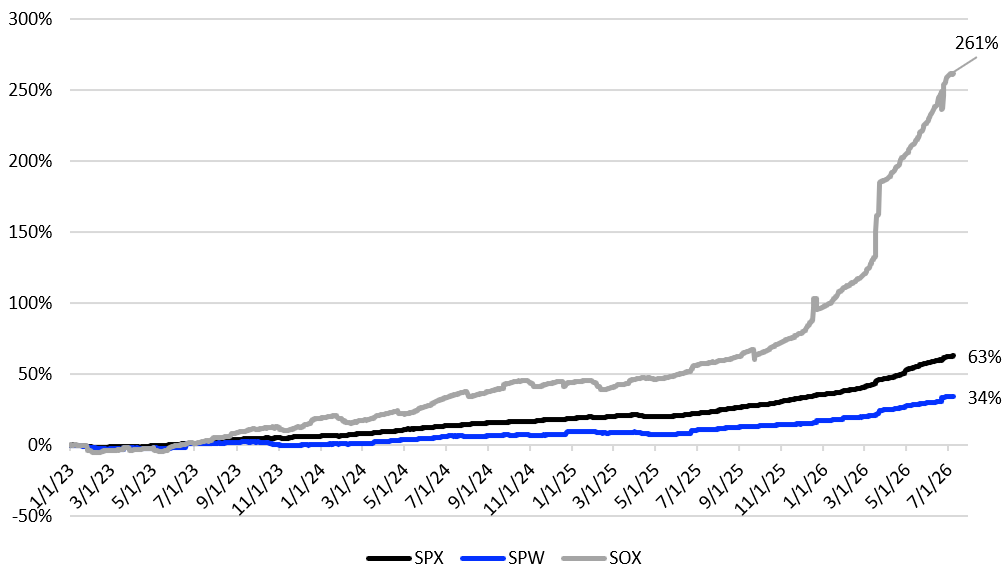

First, we detail how the 2H26 equity outlook is hinging on one key factor: the willingness of hyperscalers to continue to raise AI infrastructure capex guidance, which has been the fuel for the market’s earnings growth given semiconductors’ outsized weight (markets tend to rally with earnings estimates are being revised higher). The fate of semiconductor performance has never been more important for the US equity market, as the industry has grown to a 19% weight in the S&P 500 (up from 2% 15 years ago) and has been dominant force behind robust earnings growth in recent years, as seen in the chart below.

12 Month Forward Earnings Growth Since 2023 S&P 500 (SPX), Equal Weight (SPW), Semicoductors (SOX)

Source: Bloomberg, NewEdge Wealth, as of 7-10-26

We are hesitant to take a “Nothing Else Matters” approach to equity catalysts, but given how the powerful AI infrastructure earnings revisions allowed the 1H equity market to shake off any and all kinds of challenging developments, we must appreciate that this tailwind persisting or fading will be of the utmost importance for performance in the 2H.

Second, we highlight that the “double-platinum” first half for stocks and earnings was not reflected in the U.S. economy. Through the first half, GDP forecasts were trimmed in the face of the energy price shock, GDP nowcast results showed tepid-at-best growth, and the labor market remained resilient but not robust (as displayed by anemic wage growth that is not keeping pace with inflation).

The reason for boom-like earnings growth and stock performance in contrast to an uninspiring economic backdrop is the well-appreciated idiosyncratic driver of AI infrastructure spending, which is massively boosting corporate profits (mainly for semiconductor companies) but not boosting GDP as much because semiconductor imports drag down GDP statistics thanks to the ever-growing trade deficit.

This combination of sticky inflation and muddle-through growth has certainly clouded the outlook for Fed policy as well, with new Fed Chair Warsh choosing a taciturn (we are saying he’s not a hawk or a dove, but a tacitern) approach to communication, a convenient withdrawal of guidance in a particularly uncertain time.

Third, we take inspiration from Metallica’s own origin story to look for opportunity created by challenges. Metallica members used their own challenged upbringings to inspire great music, so we can use the current challenges markets are facing to make impactful investment decisions.

Whether it is using the sticky inflation/higher rate environment to optimize cash portfolios and build thoughtful muni bond portfolios, or using periods of amplified market uncertainty to execute Volatility Strategies, or using the distinct 2Q underperformance of high quality/strong cash generating equities as an opportunity to build exposures, or finding ways to embrace idiosyncratic risk in private markets, this market continues present ample opportunities to take advantage of and benefit from disruption.

Just as this market will be half way through trying to follow up its strong 1H with a strong 2H, Metallica will be kicking off its month-long residency at the Sphere in Las Vegas. In our ticket resale channel check, there were very few tickets listed for under $1,000, not bad for a band that has been making music for 45 years (and a sign that this consumer remains resilient!).

We are confident that Metallica will “stick to the hits” in this residency (likely meaning very few songs from Load and Reload, the 6th and 7th follow up albums), which is good advice for investors as well, with “the hits” being diversified portfolio allocations, disciplined through-cycle due diligence, and constantly looking to see periods of volatility as opportunity.

Have a great second half of 2026 and keep on rockin’!

IMPORTANT DISCLOSURES

The views and opinions included in these materials belong to their author and do not necessarily reflect the views and opinions of NewEdge Capital Group, LLC.

This information is general in nature and has been prepared solely for informational and educational purposes and does not constitute an offer or a recommendation to buy or sell any particular security or to adopt any specific investment strategy.

NewEdge and its affiliates do not render advice on legal, tax and/or tax accounting matters. You should consult your personal tax and/or legal advisor to learn about any potential tax or other implications that may result from acting on a particular recommendation.

The trademarks and service marks contained herein are the property of their respective owners. Unless otherwise specifically indicated, all information with respect to any third party not affiliated with NewEdge has been provided by, and is the sole responsibility of, such third party and has not been independently verified by NewEdge, its affiliates or any other independent third party. No representation is given with respect to its accuracy or completeness, and such information and opinions may change without notice.

Investing involves risk, including possible loss of principal. Past performance is no guarantee of future results.

Any forward-looking statements or forecasts are based on assumptions and actual results are expected to vary from any such statements or forecasts. No assurance can be given that investment objectives or target returns will be achieved. Future returns may be higher or lower than the estimates presented herein.

An investment cannot be made directly in an index. Indices are unmanaged and have no fees or expenses. You can obtain information about many indices online at a variety of sources including: https://www.sec.gov/answers/indices.htm.

All data is subject to change without notice.

© 2026 NewEdge Capital Group, LLC