Though you swear that you are true

I’d still pick my friends over you

“My Friends Over You”, New Found Glory

Sporting Vans sneakers, hair gel, cargo shorts, and a whole lot of teenage angst (all things that could be procured at suburban mall Hot Topic), New Found Glory stormed the rock airwaves with “My Friends Over You” and its iconic riff in 2002.

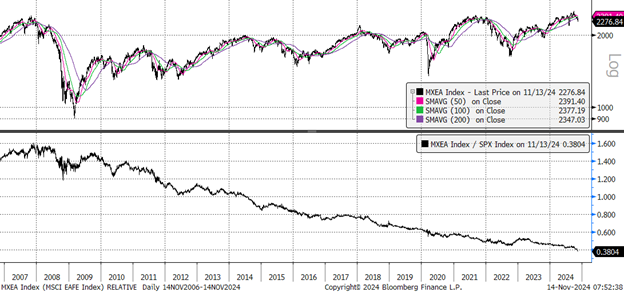

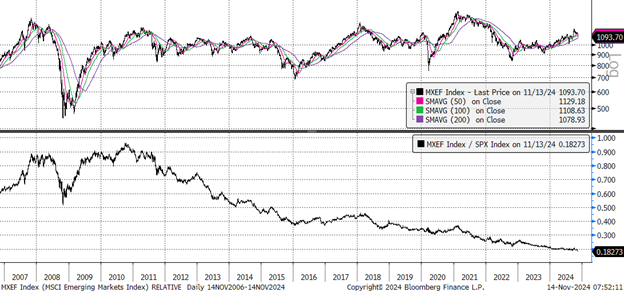

Over the last 17 years, U.S. investors have been well served by singing along, choosing my friends (domestic stocks) over you (international stocks). In this time, a home country bias with the S&P 500 has outperformed the MSCI International Developed Index (EAFE) by 320% and the MSCI Emerging Markets Index (EM) by 330%.

The charts below show this relentless downtrend of relative performance for these indices, but if you squint closely (maybe doing your best NFG front-man, Jordan Pundik, impersonation), you can see brief periods of non-U.S. outperformance over the course of this 17-year malaise.

MSCI International Developed Index Absolute (top) and Relative to S&P 500 (bottom)

MSCI Emerging Markets Index Absolute (top) and Relative to S&P 500 (bottom)

One of those brief periods of international outperformance was in 2017, the year of Trump’s first term. This outperformance in 2017 caught many investors by surprise, given the initial reaction to Trump’s victory in 2016 was sharp non-U.S. underperformance for the final two months of the year.

Relative Performance of MSCI International Developed (black) and Emerging Market (blue) Indices vs. S&P 500

As we wrote last week, this reversal of non-U.S. underperformance in 2016 into outperformance in 2017 was largely driven by the movement in the USD, with the USD rallying sharply in the last two months of 2016 (+7.15%) and then falling sharply over the course of 2017 and into early 2018 (-14.82%). Non-U.S. stocks’ performance relative to the U.S. has been correlated to movements with the USD, with a stronger USD negative for non-U.S. stocks and a weaker USD positive for non-U.S. stocks.

U.S. Dollar Spot Index (DXY)

But in 2018, these fortunes for the USD and non-U.S. stocks shifted again, with a resumption of USD strength and non-U.S. weakness as Trump began to increase tariffs in early 2018. Though these tariffs were narrow, Morgan Stanley estimates from early 2018 had these select tariffs as impacting only 4.1% of U.S. imports, they do appear to have impacted sentiment and trading of the USD and non-U.S. stocks.

This leads to the question about how non-U.S. stocks will perform in the second Trump term. We have certainly seen a similar initial reaction to Trump’s victory in 2016 and 2024: since the election, the USD is up +3.6% (it is up nearly 7% since the start of October), and EAFE and EM have underperformed the S&P 500 by 6% and 7.5%, respectively.

But will these trends of a stronger USD and weaker non-U.S. stocks reverse in 2025, as they did in 2017, or will we see a continuation of these recent trends? Should U.S. investors continue to choose “my friends over you” and stick with a home country bias?

This answer to this largely depends on the path forward for the USD and, relatedly, Trump’s tariff policies. We will explore both of these items in this week’s Weekly Edge.

“Just Maybe You Need This”: U.S. Dollar Dynamics

Analyzing and forecasting the outlook for the dollar is an exercise in finding “the confluence of evidence”, meaning focusing on one factor or driver alone can often lead to the wrong conclusions.

For example, a short/negative USD call was consensus at the beginning of 2021 due to the “twin deficits problem”, which is often considered to be dollar negative (though it is often misused, as deficit problems tend to be medium/long-term drivers, not short-term).

However, these forecasters calling for a weaker USD missed the dominant short positioning in the dollar, which meant that the call for a weaker USD was already well reflected in prices and positioning. What followed was a powerful rally in the USD over the course of 2021 and 2022 that was a surprise to many forecasters.

The chart below shows how lows in USD positioning coincide with lows in prices (late 2017, 2021), with the inverse of highs in positioning coinciding with highs in prices as well (early 2017, mid 2022).

Today, positioning based on CFTC futures, shown above, does not look stretched and, in fact, looks relatively light given the size of the recent jump higher in the USD.

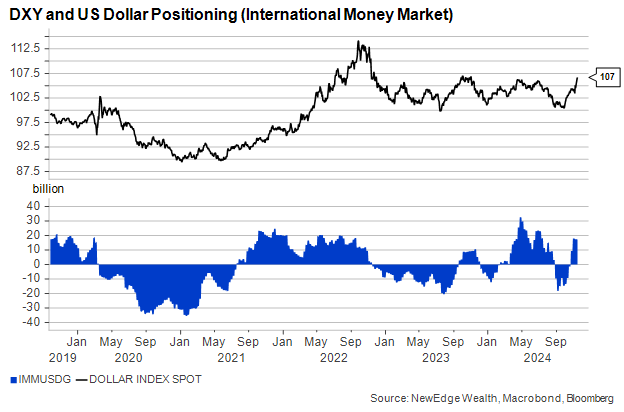

We also check the Chicago Mercantile Exchange’s International Money Market futures positioning (IMM) below, which paints a picture of somewhat longer USD positioning currently.

Our conclusion from these two readings is that USD positioning is not long enough yet to be a meaningful headwind to further upside in the USD.

Next, we have to check the technicals. The USD is overbought currently, which could set up for some near-term downside/consolidation. However, what should be noticed from the chart below is that overbought conditions do not always result in USD tops. Times like 2021 and 2022 stand out when the USD experienced seven overbought conditions over the course of its 27% rally. Thus, overbought conditions do not have to be fatal to a rally.

We do note fairly significant resistance for the DXY index at around 108, which will be an important test for the dollar index.

U.S. Dollar Spot Index (DXY)

This leads us to assess the source of USD upside, which we think is primarily coming from the relative strength of the U.S. economy compared to major peers. This economic resilience is potentially driving the Fed to be relatively more hawkish vs. other major central banks, who are expected to ease policy more aggressively in order to stabilize their weaker economies. Just Friday, we heard Fed Chair Powell support this view, saying there was no need to hurry rate cuts given the resilient U.S. economy.

Said another way, as long as U.S. economic growth continues to outperform major global peers, a stronger USD is supported. If data were to weaken in the U.S. and expectations for deeper Fed cuts were to return, we would expect the USD to reverse its recent strength.

Overall, we see reason for the USD to potentially consolidate in the very near term, but do not see, at this time, the conditions for a complete reversal and move lower in the USD given positioning and fundamentals. This outlook will likely evolve as we near 2025, mostly if positioning gets stretched or we see growth begin to soften. Remember that a weaker USD is a necessary condition for better non-U.S. equity performance. Note, we have also written about the long-term reserve currency status of the USD, which plays a role in our USD outlook beyond the short-term.

“Please tell me everything that you think that I should know about all the plans you made”: Tariffs into 2025

The impact of potential tariffs is being hotly debated by economists and market watchers on multiple levels.

First, there is high uncertainty of what, how, and when tariffs could be enacted in Trump’s second term. The big question is how much should campaign rhetoric, including 60% tariffs on Chinese imports and 10% tariffs on all imports, be taken seriously.

Second, even if we knew exactly what tariffs would be applied, there is great uncertainty as to how these tariffs would be absorbed by the economy and markets (Inflationary? Non-inflationary? A headwind to growth? A useful negotiating tool?).

Many analysts expect tariffs to be a USD-positive event, similar to the impact in 2018 and 2019 (the simple logic, and a throwback to ECON 101, is that higher tariffs result in reduced demand for exports, which reduces the supply of global dollars and results in a stronger USD).

However, some analysts, like Bloomberg’s Mark Cudmore, argue that the lessons from Brexit, which removed the UK from the EU free trade bloc and resulted in broadly higher trade costs, was actually a negative event for the pound (GBP). This is to say that if much broader tariffs are enacted in Trump’s second term and are met with retaliation from trading partners, the simple conclusion that this would drive a stronger USD may be worth questioning (but note the difference in reserve currency status of the US vs. the UK).

We also do not know how these tariffs could be enacted. If narrow, the Executive Branch can apply tariffs under “extraordinary circumstances”, such as for “national security”. There is talk that broader tariffs could be supported and thus imposed by Congress, which would be the first time Congress set tariff policy in nearly 100 years, according to Politico.

Analysts are watching closely for where Trump’s former Trade Representative, Robert Lighthizer, is appointed. According to the WSJ, Lighthizer is being considered for a post as trade czar, overseeing the administration’s entire trade policy (the Journal also notes that this post would not need Senate confirmation, so Lighthizer could, in theory, get to work immediately on implementing trade policy).

Lastly, we don’t know when tariffs will be implemented as well. In Trump’s first term, tariffs came in 2018 and 2019 after the good news of large tax cuts. With taxes set to be negotiated later in 2025, there is a chance that tariffs will come before any potential tax cuts this term.

“It Was Damaged Long Ago”: Non-U.S. Earnings Weak Already

Regardless of how aggressive tariff policy turns out to be and the impact it may have, when considering non-U.S. investments, we have to appreciate the current earnings and fundamental backdrop.

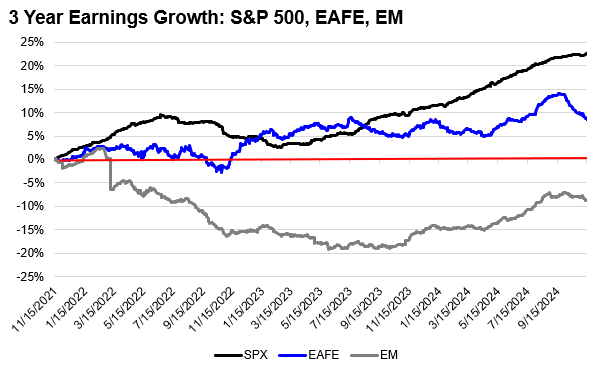

Notably, relative earnings growth for non-U.S. indices has been much weaker compared to the S&P 500, even without significant incremental tariffs. The chart below shows earnings growth over the last 3 years for the S&P 500, EAFE, and EM indices and how the U.S. has positively trounced the rest of the world in earnings growth. No wonder U.S. stocks have been such leaders!

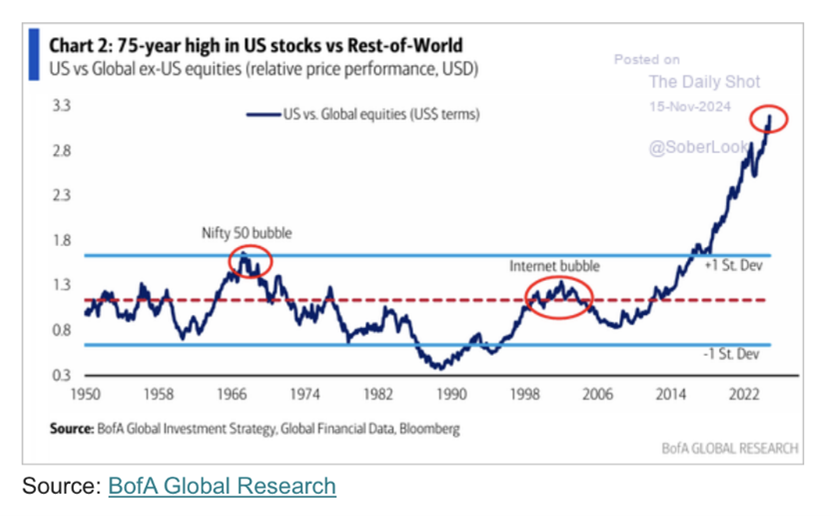

This U.S. earnings exceptionalism and growth dominance over the rest of the world has resulted in historically stretched readings of both the share of U.S. stocks vs. the global equity market capitalization and the degree of outperformance, as shown in the charts below.

Eventually, non-U.S. stocks may have their time in the sun, resulting in some kind of mean reversion in these readings, but we continue to argue that there needs to be a major catalyst to justify making a call that this mean reversion will happen (as we wrote in June, the cheap can just keep getting cheaper). One of these catalysts could be a major USD bear market, which is why a view on the USD is critical to the outlook for non-U.S. stocks.

“I’d Still Pick My Friends Over You”: Conclusion

Given this backdrop of a stronger USD, tariff uncertainty, and weaker earnings, we see reason for U.S. investors to continue to broadly pick my friends (domestic stocks) over you (non-U.S. stocks). As we wrote in June, we think there is ample opportunity for selection within international markets, given lower concentration and pockets of more attractive valuations, meaning we don’t think that investors can eschew international stocks altogether. This view may evolve as we near 2025, mostly for a short-term outlook, if we see signs of coming USD weakness that could shift the fates of these laggard stocks.

IMPORTANT DISCLOSURES

The views and opinions included in these materials belong to their author and do not necessarily reflect the views and opinions of NewEdge Capital Group, LLC.

This information is general in nature and has been prepared solely for informational and educational purposes and does not constitute an offer or a recommendation to buy or sell any particular security or to adopt any specific investment strategy.

NewEdge and its affiliates do not render advice on legal, tax and/or tax accounting matters. You should consult your personal tax and/or legal advisor to learn about any potential tax or other implications that may result from acting on a particular recommendation.

The trademarks and service marks contained herein are the property of their respective owners. Unless otherwise specifically indicated, all information with respect to any third party not affiliated with NewEdge has been provided by, and is the sole responsibility of, such third party and has not been independently verified by NewEdge, its affiliates or any other independent third party. No representation is given with respect to its accuracy or completeness, and such information and opinions may change without notice.

Investing involves risk, including possible loss of principal. Past performance is no guarantee of future results.

Any forward-looking statements or forecasts are based on assumptions and actual results are expected to vary from any such statements or forecasts. No assurance can be given that investment objectives or target returns will be achieved. Future returns may be higher or lower than the estimates presented herein.

An investment cannot be made directly in an index. Indices are unmanaged and have no fees or expenses. You can obtain information about many indices online at a variety of sources including: https://www.sec.gov/answers/indices.htm.

All data is subject to change without notice.

© 2026 NewEdge Capital Group, LLC