The space between

The tears we cry

Is the laughter – keeps us coming back for more

“The Space Between”, Dave Matthews Band

We are living in the space between.

The space between the initial shock of tariffs on the market and the potential/eventual real impact of tariffs on earnings and the economy.

The space between the announcement of aggressive tariffs and the ultimate application of tariff policy.

The space between a sharp drop in soft sentiment data and the potential/eventual deterioration in real hard data.

This in between space promises to be confusing (like DMB’s “fickle, fuddled words”), as data is distorted by natural lags, the pulling forward of spending to get ahead of tariffs, and the paralyzing uncertainty that is weighing on consumer and business expectations and decision making.

This in between space will also likely see equity and fixed income markets whipsawed by tariff negotiation headlines, swings in positioning and technicals, and the gradual defogging of the post-tariff economic outlook as real data trickles in.

Being in the space between should feel somewhat familiar to investors, as we experienced a space between back in 2022. Uncertainty and market volatility was pronounced that year, as investors debated how a rapid rise in Fed interest rates and the associated weakening in sentiment/soft data would weigh on real economic activity. Forecasters slashed estimates for U.S. GDP and S&P 500 EPS growth, broadly expecting a recession to be the end result of that space between, while equities experienced a bear market in anticipation of this weaker growth.

Of course, as we now know with hindsight, these consensus calls for recession and weaker corporate earnings proved to be misguided, with the U.S. economy surprising meaningfully to the upside in both 2023 and 2024. Pushing back against dire forecasts for U.S. economic growth and instead expecting a robust U.S. economy was the right call after a bruising 2022.

The charts below show this path of growth forecast getting slashed through 2022 and then staging a stunning volte face as forecasters began to appreciate the resilience of the U.S. economy.

So, here we find ourselves in the space between in 2025, with growth forecasts getting slashed due to anticipated tariff impacts and the cratering of soft sentiment data, while consensus has turned distinctly negative for the economy and markets.

This negativity raises the question of whether investors should adopt the winning optimism of 2023 and 2024 and bet on upsides to growth. We think the answer is that today’s consensus negativity allows for brief relief rallies in markets, but that the economic and earnings reality suggests that investors should continue “getting comfortable being uncomfortable” and expect continued volatility in markets. As we navigate this space between, there is necessary nuance to this noted negativity, which we will explore in the next two sections.

“I Hope We Don’t Take This Ship Down”: Unpacking Economic Negativity

On the economy front, recent commentary from macro forecasters has been resoundingly negative (all of our recent conversations with prognosticators have been bearish!), but the Street still estimates 2025 GDP growth at a somewhat healthy 1.7%, as shown above. For context, this compares to a low of 0.25% for 2023 growth forecasts. We still sense there is “hope to keep safe from pain” amongst many forecasters and investors that tariffs will be walked back, and that stimulative tax policy will get passed quickly (we are not so sure on either point).

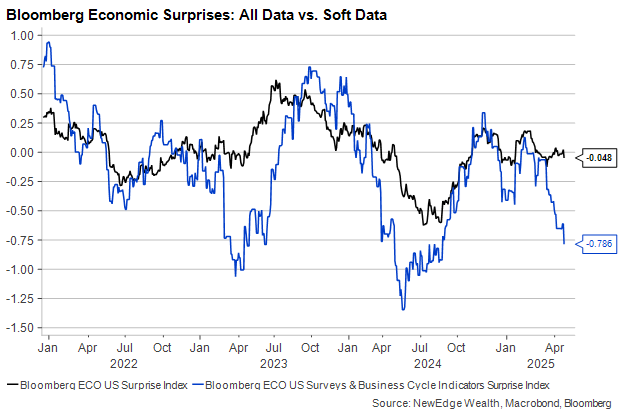

If soft data is to be believed, the U.S. economy is in for a troubling time with survey data about employment, inflation, manufacturing, and broader business outlook all painting a startling stagflationary picture (for all of these charts, see the attached 2Q25 slide deck and video). But it still remains to be seen if this cratering in soft data will ultimately result in a weakening in real, hard economic and earnings data. The chart below shows a similar plunge in soft data (blue line) at the beginning of 2023, just as hard data (included in the black line) was about to improve.

Over the last three years we have adopted a “watch what they do not what they say” mantra in interpreting soft data, as we have appreciated that soft data has sent a far more negative signal about the economy that the real hard data has corroborated (this was a key part of our “Strange Landing” thesis).

But we note that many of the drivers of hard data surprising to the upside in 2023 and 2024 (supportive fiscal stimulus, ample Treasury liquidity supporting a consumption-boosting wealth effect, strong labor growth and productivity, and falling net interest expense) have all either completely or materially faded as tailwinds in 2025.

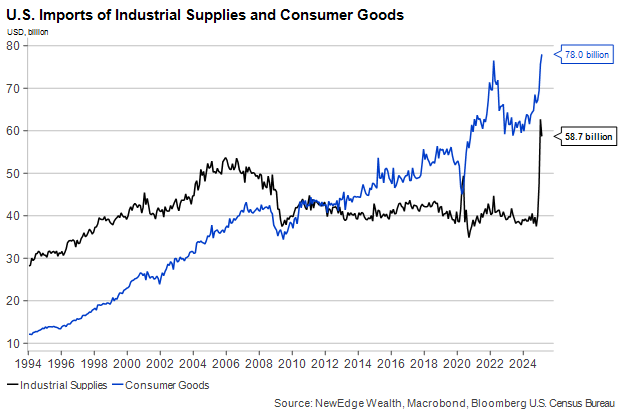

We also think that it could take time for the hard data to accurately reflect the underlying economic reality. Consumers and businesses are clearly pulling forward demand in order to get ahead of tariffs, as seen in the import data below, which is temporarily flattering current economic data.

Businesses are also not turning to layoffs yet in anticipation of weaker sales growth or softer margins (more on this below), which is keeping the jobs market in its “less hire/little fire” state.

Being in this space between the announcement of tariffs and the impact of tariffs, as well as the deterioration of soft data and the reaction of hard data, is not just confusing for forecasters and investors, but it is befuddling for the Fed. This slow but stable jobs market in the very near term, along with concerns about tariff-driven inflation, is why we think the Fed (with its current leadership!!!) intends to stay on hold until more distinct signs of economic weakness potentially emerge.

The key message on the economic front is that we do expect tariffs, in their current form, to weigh on economic growth, but note that this slowing could take longer than expected, while the relationship between soft and hard should be considered “unproven” until we begin to see further post-tariff hard data.

“Look at Us Spinning Out in the Madness of a Roller Coaster”: Unpacking Market Negativity

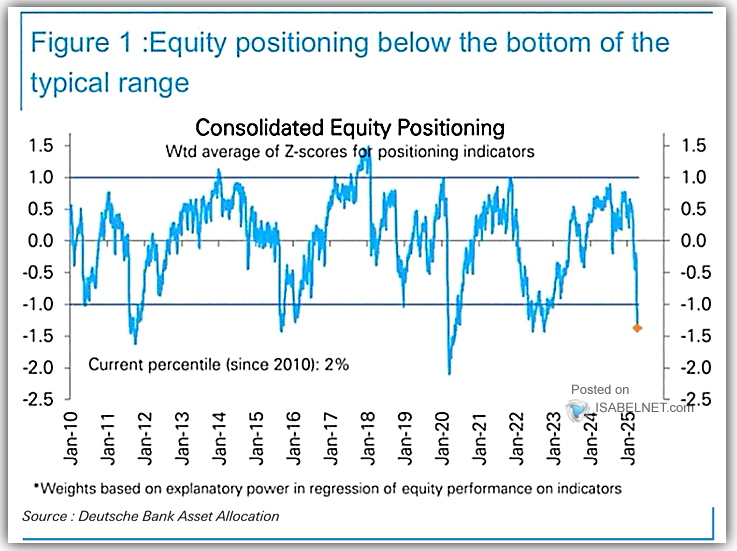

On the market front, investor sentiment surveys like AAII and Investors Intelligence show extreme bearishness, while institutional positioning measures like Deutsche Bank Consolidated Positioning have fallen to a notably underweight 2nd percentile. Positioning and sentiment readings at these washed-out levels have often been followed by above-average forward returns, as low expectations are easily bested.

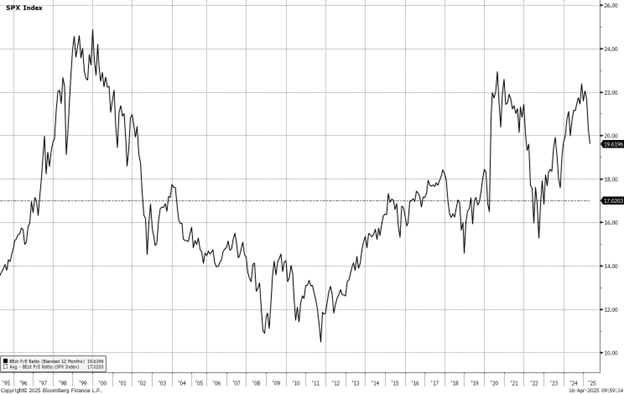

However, despite these low sentiment and positioning measures, the S&P 500 still trades at an above average valuation (19.5x forward vs. 17x average over the last 30 years) on earnings estimates that remain optimistic if economic growth were to disappoint (9% growth to $270 in 2025 and 12% growth to $302 in 2026), or if margins were to come under pressure due to tariffs.

S&P 500 12 Month Forward PE with 30 Year Average

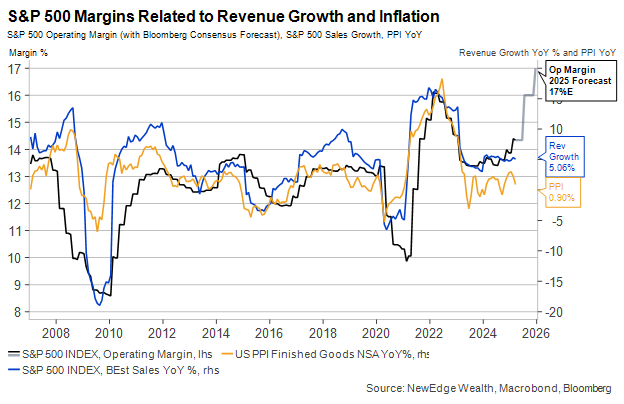

It is this last point that is of critical importance for the equity outlook in 2025. We often quip, “never bet against the great American might of margin expansion”, a trope that has proven accurate for the last nearly four decades of ever-expanding corporate profitability.

But as we look at consensus forecasts for record S&P 500 operating margins in 2025 and 2026, amidst a backdrop of rising input costs (not just from tariffs but broader deglobalization) and dubious pricing power, we are concerned that these still-rosy forecasts are too aggressive. Of course, the hope of productivity from technology could “bail out” these margin forecasts, but we have yet to see material evidence that AI use cases are bending the curve on broad cost structures yet.

We think the elevated state of both valuations and earnings estimates means that markets could remain volatile in the coming months. We think that light positioning and bearish sentiment allow for relief rallies, but that earnings estimate cuts and valuation derating keep equity markets choppy and with downside potential.

We also note that equity market momentum has faded over the last 9 months (we have been flagging the weak signal from the Weekly MACD), while the S&P 500’s trend has deteriorated materially, with a “death cross” experienced this week as the 50-day moving average crossed below the 200-day moving average. Both of these momentum and trend observations suggest that the index could have a tougher time bouncing back, supporting our view that an imminent V-shaped recovery is unlikely (unless we get a complete walk-back of tariff policy!).

“You Cannot Quit Me So Quickly”: Conclusion

The first few weeks of 2Q25 have proven to be exhausting for investors and market watchers as they have been thrown into an uncertain space between tariff announcements and future impacts of these policies. This trying time has resulted in a sharp deterioration in sentiment and a reduction in positioning, an important silver lining that we must appreciate, but also must contrast with still-high GDP estimates, equity/credit valuations, and earnings estimates.

We do think this space between will linger as hard data will take time to reflect the economic reality, while policy could remain erratic and uncertain. This suggests a continuation of volatility across markets.

IMPORTANT DISCLOSURES

NewEdge Wealth is a division of NewEdge Capital Group, LLC. Investment advisory services offered through NewEdge Wealth, LLC, an investment adviser registered with the US Securities and Exchange Commission. Securities offered through NewEdge Securities, LLC, Member FINRA/SIPC.

The views and opinions included in these materials belong to their author and do not necessarily reflect the views and opinions of NewEdge Wealth, LLC.

This information is general in nature and has been prepared solely for informational and educational purposes and does not constitute an offer or a recommendation to buy or sell any particular security or to adopt any specific investment strategy.

The trademarks and service marks contained herein are the property of their respective owners. Unless otherwise specifically indicated, all information with respect to any third party not affiliated with NewEdge has been provided by, and is the sole responsibility of, such third party and has not been independently verified by NewEdge, its affiliates or any other independent third party. No representation is given with respect to its accuracy or completeness, and such information and opinions may change without notice.

Investing involves risk, including possible loss of principal. Past performance is no guarantee of future results.

Please remember that different types of investments involve varying degrees of risk, and there can be no assurance that the future performance of any specific investment or investment strategy (including those undertaken or recommended by NewEdge) will be profitable or equal any historical performance level(s). Clients should carefully consider their own investment objectives and never rely on any single chart, graph or marketing piece in making investment decisions.

Any forward-looking statements or forecasts are based on assumptions and actual results are expected to vary from any such statements or forecasts. No assurance can be given that investment objectives or target returns will be achieved. Future returns may be higher or lower than the estimates presented herein.

An investment cannot be made directly in an index. Indices are unmanaged and have no fees or expenses. You can obtain information about many indices online at a variety of sources including: www.sec.gov/answers/indices.htm.

All data is subject to change without notice.

© 2025 NewEdge Wealth, LLC