Feed the flame ’cause we can’t let go

Run away, but we’re running in circles

“Circles”, Post Malone

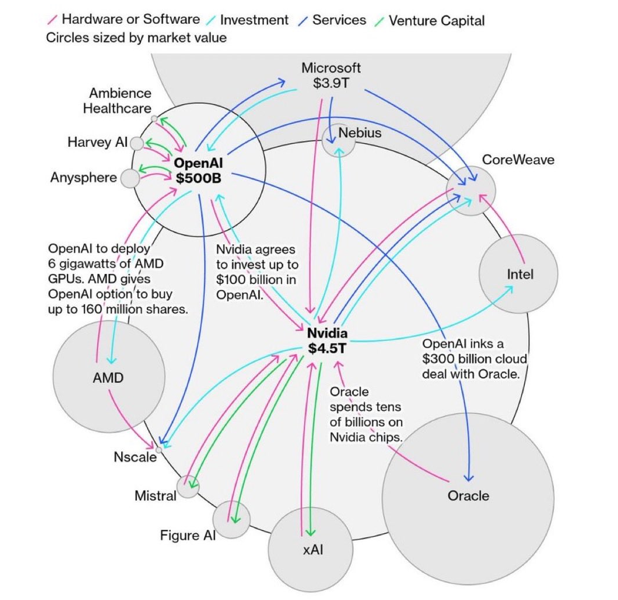

The last few weeks of AI-infrastructure deal announcements have raised many an eyebrow about the circular nature of these deals (ex. Nvidia investing in $100B in OpenAI so that OpenAI can buy NVDA chips, alongside a $300B OpenAI deal with Oracle that will purchase even more NVDA chips), and stirred up memories of the ill-fated vendor financing boom of the 1990’s tech bubble.

This kind of circular investment is nothing new for the likes of NVDA, who has long been investing in AI startups, which in turn rely upon NVDA chips for their technology. However, it is the massive scale of these investments and how they are funded (more debt and external funding vs. a reliance on internal cash flows) that is sparking concern amongst investors/bubble watchers.

The chart below from a great Bloomberg article illustrates this circularity and the huge dollar values that go along with it.

This swelling “node link diagram” reminds us of an important takeaway from Andrew Lo’s Adaptive Markets Hypothesis(AMH). Within his AMH, Lo writes about the benefits and risks of interconnectivity in financial systems (the set of relationships between different players in a financial system).

Lo argues that in good times interconnectivity can strengthen and boost a system, but in bad times, the greater the interconnectivity, the greater risk for systemic shock or collapse. To say it plainly, if everyone owes each other money, then the failure of one can cause a cascade of failures for others that are exposed (you’re seeing a microcosm of this with the recently bankrupted First Brands).

Mark Buchanan might refer to this as a “finger of instability”, with interconnectivity serving as a driver of growth and upside in good times, but eventually becoming the source of fragility in the future.

To bring this back to AI, this virtuous, circular feedback loop is helping to fund trillions of dollars of physical investment in technology infrastructure, and it is undeniable that this overlapping investment is having positive impacts on both the US equity market and US economy.

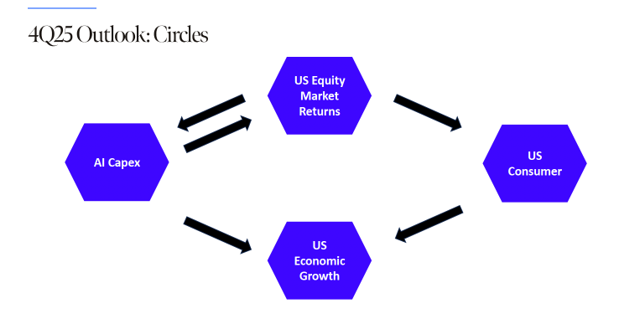

This last point is vital and was the focus of our 4Q25 outlook, which we titled “Circles”, not just in reference to the circular financing of AI deals, but also the circular relationship between AI capex, the US economy, the US consumer, and US equity markets.

This diagram, which is included in the chart deck and webinar linked below, shows this circular interconnectivity: AI capex is helping to drive US equity market returns, which is helping to drive further AI capex, and strong equity returns are boosting US consumers (through the wealth effect for high income, high consuming consumers), which is helping to keep US economic growth healthy, with US economic growth also being buoyed by AI capex (phew!).

What this all implies is a circular interconnectivity with the US economy and market’s reliance on AI capex built upon another circular interconnectivity between AI players themselves.

We do not write this to imply an imminent collapse. After all, AI-driven compute demand is still outstripping supply, supporting a continuation of this investment spree (the details of which are included in the outlook slides). However, we do think it is prudent to appreciate how much of the US economy and markets are relying on this circular, interconnected AI boom continuing.

If AI capex were to slow materially, the market and the economy would lose its largest driver of idiosyncratic excellence, thus challenging other market factors like today’s high valuations (22.9x forward for the S&P 500) and rosy earnings estimates (current consensus expects low double digit growth the next two years, driven by revenue acceleration and powerful margin expansion).

But the “if” in that prior sentence is vitally important. What will drive AI capex to slow materially?

Some, like Jordi Visser, see this as an insatiable race to super-intelligence supremacy that is driving exponential growth that cannot be contemplated by traditional models/forecasts.

Others are not so comfortable extrapolating the recent super-normal growth rates into the future. Two great pieces from the Financial Times unpack and question recent reports from Barclays and Morgan Stanley that argue AI is not in a bubble, that investment will continue, and the return on these investments will be powerful (the Morgan Stanley piece makes the bold assumption that today’s $50B of AI revenue will grow to $1T by 2028 (though Jamie Dimon of JP Morgan did recently say that the $2B the bank has spent on AI is starting to pay off).

There is an old phrase in markets that says “dance while the music is playing” (we prefer the ABBA version: “Dance (While the Music Still Goes On”), which encourages investors not to sit on the sidelines during bull runs/booms. This goes alongside another markets phrase, “being early is the equivalent of being wrong”, which means that you might be able to identify the fingers of instability in a market or economy, but that does not mean a collapse or a change is imminent (just ask The Big Short guys who were early to identifying issues with US mortgages before the Great Financial Crisis and almost got forced out of the short trade).

For now, it appears that the music is blaring for the circular AI capex trade and that it is likely too early to bet against this powerful trend. However, eventually this capex will slow, potentially succumbing to the law of large numbers, technological change, overbuilding, rising funding costs, or deterioration in hyperscaler returns (one of our key observations is that hyperscalers are using profits from their legacy capital-light, near monopoly businesses to fund investments in capital intensive, highly-competitive AI businesses, which implies lower returns in the future).

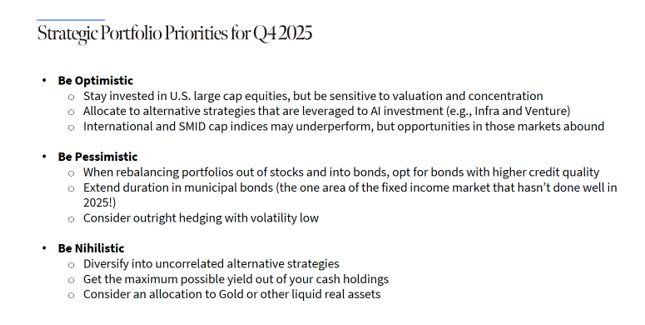

This suggests that we need to take a highly balanced approach to navigating this environment, not being too optimistic that we become overextended to brewing risks, but not being too pessimistic that we sit on the sidelines for the continuation of a megatrend.

We presented this balanced set of portfolio priorities in our outlook, which we lovingly called the “Me, Myself, and Irene” approach, arguing that we should, at once, be optimistic, pessimistic, and nihilistic. The last portfolio personality looks at finding opportunities for returns that have low correlations to public equity or fixed income markets.

This is a time for markets that is equally complicated and fascinating. The current snapshot is near record valuations for equity and credit, positioning that is chasing returns, sentiment that has become ebullient, widespread optimism about growth, and a massive circular and interconnected technology capex cycle that is seemingly justifying the rest of this snapshot. This snapshot could a high bar for markets to jump over, mostly as we enter 2026, a dynamic that we will be watching and analyzing closely through the end of the year.

IMPORTANT DISCLOSURES

NewEdge Wealth is a division of NewEdge Capital Group, LLC. Investment advisory services offered through NewEdge Wealth, LLC, an investment adviser registered with the US Securities and Exchange Commission. Securities offered through NewEdge Securities, LLC, Member FINRA/SIPC.

The views and opinions included in these materials belong to their author and do not necessarily reflect the views and opinions of NewEdge Wealth, LLC.

This information is general in nature and has been prepared solely for informational and educational purposes and does not constitute an offer or a recommendation to buy or sell any particular security or to adopt any specific investment strategy.

The trademarks and service marks contained herein are the property of their respective owners. Unless otherwise specifically indicated, all information with respect to any third party not affiliated with NewEdge has been provided by, and is the sole responsibility of, such third party and has not been independently verified by NewEdge, its affiliates or any other independent third party. No representation is given with respect to its accuracy or completeness, and such information and opinions may change without notice.

Investing involves risk, including possible loss of principal. Past performance is no guarantee of future results.

Any forward-looking statements or forecasts are based on assumptions and actual results are expected to vary from any such statements or forecasts. No assurance can be given that investment objectives or target returns will be achieved. Future returns may be higher or lower than the estimates presented herein.

An investment cannot be made directly in an index. Indices are unmanaged and have no fees or expenses. You can obtain information about many indices online at a variety of sources including: https://www.sec.gov/answers/indices.htm.

All data is subject to change without notice.

© 2025 NewEdge Wealth, LLC