I’ve found a reason for me

To change who I used to be

A reason to start over new

And the reason is you

“The Reason”, Hoobastank

In the hubbub of the inauguration, the bulled-up CEOs at the World Economic Forum, a flurry of executive orders, AI competition, and earnings season (which is off to a strong start), it is easy to forget that next week we get the first Federal Open Market Committee meeting of 2025.

Now, we do not think that investors can “forget” the Fed in 2025, as interest rate and balance sheet decisions will have significant implications on markets (maybe less so the economy!). However, we do think that 2025 could be a year where the Fed will be driven by markets and other policy makers instead of driving markets, as it did earlier in this interest rate cycle.

As we discussed in our 2025 Outlook, we think the “recalibration” phase of this Fed cutting cycle is likely (or mostly) over. This means that further changes to interest rate policy will be for a reason, such as due to a substantial uptick in unemployment or a sharp slowing in economic growth. Said another way, interest rate cuts may be on pause until Powell begins singing Hoobstank’s 2004 one hit wonder saying “I’ve found a reason for me…” (supposedly Powell is quite the musician in his own right and is a confirmed Dead Head).

The rationale behind this expectation for a Fed on hold (certainly for the January meeting, which has just a 2% chance of the Fed delivering a cut next week) is a key part of our economic thesis since 2023: we do not think that the Fed’s high short-term interest rates are weighing on growth nearly as much this cycle as they have in prior cycles.

Our assertion is supported by the upside surprise and overall resilience in U.S. economic growth experienced over the last two years, despite the Fed being “restrictive” or “tight” by its own declarations.

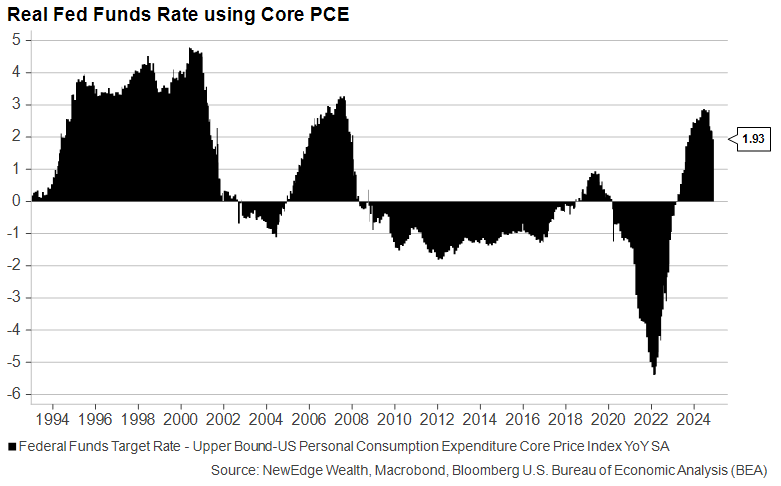

Our key observation is that the entire time that the Real Fed Funds rate has been positive (where Fed Funds is above the rate of inflation) and the entire time that the Fed Funds rate has been above the Fed’s estimate of “neutral” (the rate that is neither simulative nor restrictive to growth), the U.S. economy has grown above trend.

Further, if you were to use measures of inflation that swap out the heavily lagged and imputed housing-related components in CPI and PCE for today’s observable rents, both CPI and PCE would be lower, so the Real Fed Funds rate would be even higher into “restrictive” territory and it still is not stymieing growth! And so, resilient growth has not given the Fed The Reason to cut rates.

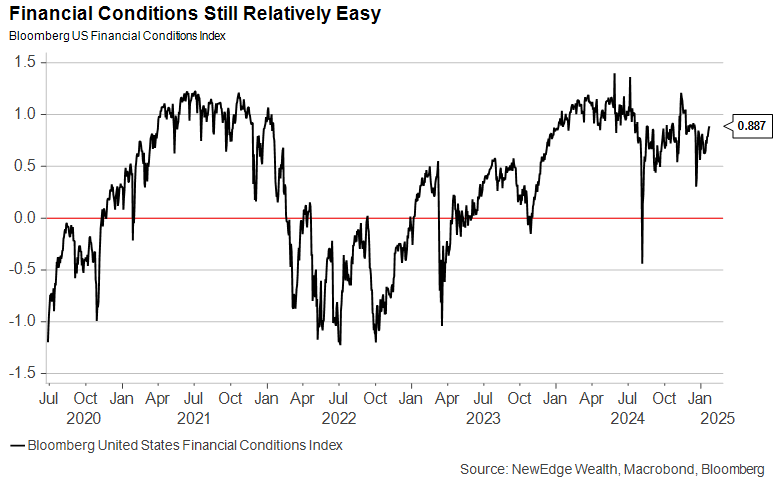

If the Fed was as tight and restrictive to growth as it thinks it is, we do not think we would be seeing measures like financial conditions remain in such easy/loose territory. Despite the movement higher in yields and the USD in recent months (which have recently reversed), we have seen financial conditions remain in easy territory thanks to high stock prices, low stock volatility, and tight credit spreads.

Again, if the Fed were as tight and restrictive to growth as it thinks it is, growth would be weaker and we would see this reflected in lower equity valuations and wider credit spreads. In part, both measures may be fulsomely valued for specific reasons, like AI/tech optimism for equities and lower supply of bonds for credit, but just as the old saying goes “you can’t outrun a bad diet”, these measures for equity and credit valuations can’t outrun weak growth.

Of course, there are pockets of the economy that are buckling under the weight of high interest rates. Housing and commercial real estate are significant examples, and it is a fair question to ask if the hope of lower rates in 2025 helped prop up activity in these areas in 2024 (the “survive to 2025” mentality), suggesting that higher-for-longer rates could eventually begin to weigh on growth in a more meaningful way.

As we detailed in our 2025 Outlook, there are reasons to expect economic growth to moderate in 2025, but at this time, we do not see signs of an imminent collapse in the growth rate that could spur the Fed to act more aggressively.

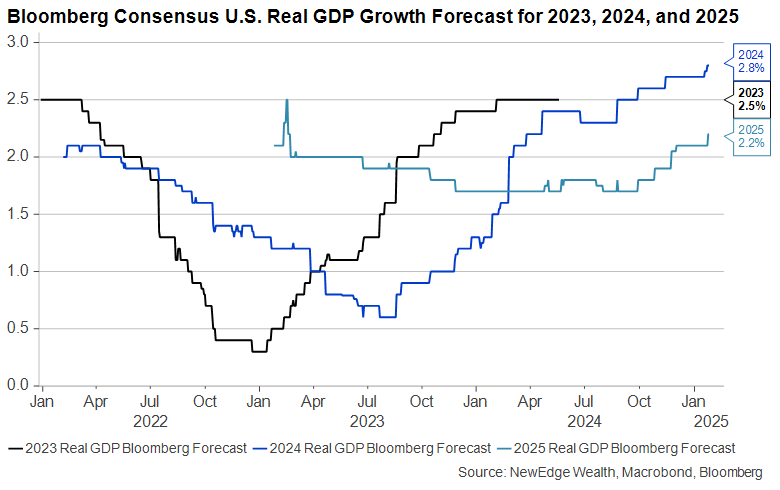

Betting against U.S. economic resilience has been the wrong call for the past two years, and with this week bringing the first revision higher to 2025 growth estimates (to 2.2% vs. 2.1% to start the year), doubting the U.S. continues to be a misplaced call. This does not mean that we are ignoring potential risks (like the continued creep higher of Continuing Jobless Claims that suggests that it is increasingly hard to find work), but we continue to see little evidence that would support a call for an imminent collapse in growth.

This growth resilience suggests that there is little reason for the Fed to rush to cut interest rates further, however there is a wild card on this front as we progress through President Trump’s second term.

This week, President Trump said that he will “demand that interest rates drop immediately”. And though monetary policy does not work that way, this statement will certainly lead to questions about Fed independence at next week’s FOMC press conference. We expect Powell to vehemently defend the Fed’s independence when asked, as he so curtly did in December when asked if he would “leave” if Trump asked him to.

However, we could be starting to get auditions to be future Fed Chair from some existing Fed members, such as Governor Waller two weeks ago delivering dovish remarks about delivering cuts in 1H25. Added to this is Treasury Secretary Bessent’s earlier open mind to a installing a “shadow Fed Chair” (Barron’s, Bloomberg), comments about which he has since walked back after sparking concern.

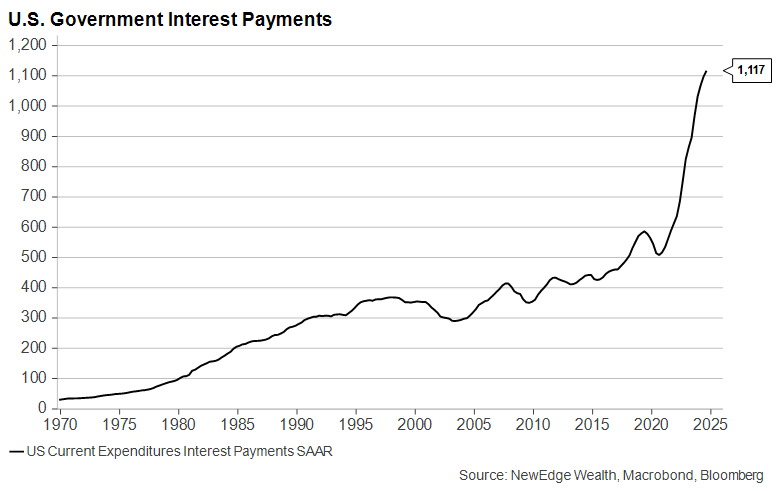

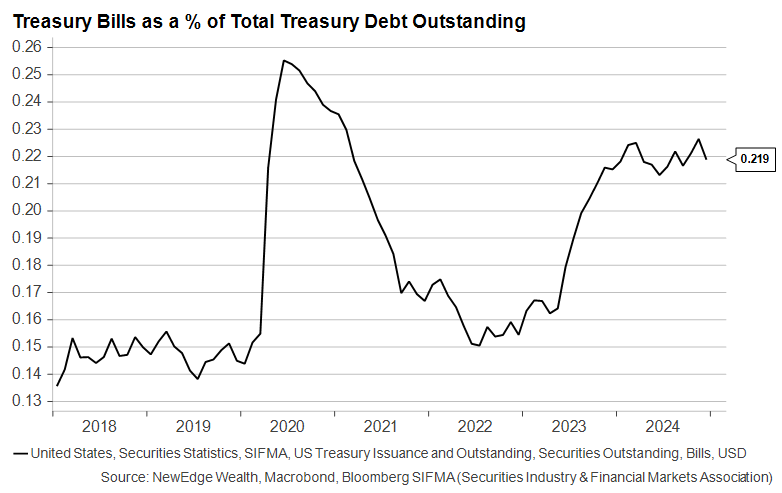

We know that Bessent will face quite the quagmire in deciding how to fund the ever-ballooning Treasury deficit, with lower short-term interest rates a potential relief given soaring interest expense and the Treasury’s heavy reliance on short-term bill issuance in recent years. So if Trump wants lower interest rates, Bessent really wants lower interest rates.

Overall, we do not see economic growth giving the Fed The Reason to cut rates in the near term, with the U.S. economy exhibiting much more resilience to short term interest rates this cycle. But given the wild cards of President Trump’s second term and the funding challenges of the Treasury, we expect to see continued jawboning around a desired path forward for Fed policy, even if growth remains resilient.

IMPORTANT DISCLOSURES

The views and opinions included in these materials belong to their author and do not necessarily reflect the views and opinions of NewEdge Capital Group, LLC.

This information is general in nature and has been prepared solely for informational and educational purposes and does not constitute an offer or a recommendation to buy or sell any particular security or to adopt any specific investment strategy.

NewEdge and its affiliates do not render advice on legal, tax and/or tax accounting matters. You should consult your personal tax and/or legal advisor to learn about any potential tax or other implications that may result from acting on a particular recommendation.

The trademarks and service marks contained herein are the property of their respective owners. Unless otherwise specifically indicated, all information with respect to any third party not affiliated with NewEdge has been provided by, and is the sole responsibility of, such third party and has not been independently verified by NewEdge, its affiliates or any other independent third party. No representation is given with respect to its accuracy or completeness, and such information and opinions may change without notice.

Investing involves risk, including possible loss of principal. Past performance is no guarantee of future results.

Any forward-looking statements or forecasts are based on assumptions and actual results are expected to vary from any such statements or forecasts. No assurance can be given that investment objectives or target returns will be achieved. Future returns may be higher or lower than the estimates presented herein.

An investment cannot be made directly in an index. Indices are unmanaged and have no fees or expenses. You can obtain information about many indices online at a variety of sources including: https://www.sec.gov/answers/indices.htm.

All data is subject to change without notice.

© 2026 NewEdge Capital Group, LLC