Made up my mind, break you this time

Won’t be so fine, it’s my turn to cry

Do what you want, I won’t take the brunt

It’s fading away, can’t feel you anymore

“Your Time is Gonna Come”, Led Zeppelin

When it comes to lags, Jimmy Page walked so the Fed could run.

Despite being called a “very limited producer and writer of weak, unimaginative songs” by Rolling Stone in the 1969 review of Led Zeppelin’s first studio album, Jimmy Page was inspiringly inventive in the short, 36 hour recording session that generated this instant-classic album.

One of Page’s innovations was capturing the band’s “ambient sound” in recording, which is why the album sounds paradoxically rich and raw at the same time.

Page accomplished this by playing with time-lags. One microphone was placed directly at the amplifier, and another was placed on the other side of the room. The extra distance the sound waves had to travel to the second microphone created a depth of sound on the record that makes you feel as if you are sitting right there in the studio with the band.

Lags can be a powerful force, not just in music, but also in monetary policy.

Longer Real Economy Lags

We have written extensively this year about consumer and corporate balance sheets being an important reason for the resilience of the U.S. economy, despite the rapid tightening by the Fed (here and here). The suppression of long-term interest rates through over a decade of Quantitative Easing allowed many consumers and corporations to “term out” their debt, locking in historically low interest rates for years (Powell finally acknowledged this term-out dynamic in this week’s press FOMC press conference, though he referred to it as a “little thing”).

In a classic case of unintended consequences, the Fed’s efforts to stimulate markets and the economy in the last easing cycles, by pressing long-term interest rates lower, effectively dampened their ability to restrict the economy in this current tightening cycle, by making broad swaths of borrowers far less sensitive to short term interest rate increases than they were in prior cycles.

We think this dynamic has resulted in an even longer lag for how monetary policy is impacting the real economy, while it has also resulted in the “pain” from higher interest rates being felt most by those that lent money/own bonds at the low interest rates (hence the balance sheet issues experienced by regional banks in March who are large owners of low coupon, long duration bonds).

- Note: we acknowledge that the lags for how policy has impacted soft data, like sentiment, and financial conditions, like risk asset pricing, have arguably been shorter this cycle, as seen by the sharp reset in sentiment and markets experienced in 2022, just as the tightening cycle was starting.

But even with this longer lag, eventually we expect higher interest rates, if they do in fact remain higher-for-longer, to begin to have a larger impact on the real economy.

This is because eventually debt will have to be refinanced at prevailing rates that are likely to be higher than when the debt was initially issued. Concurrently, not all balance sheets are created equal, meaning some borrowers will experience outsized jumps in interest expense if they have larger portions of their debt coming due in the near term.

And that’s when we can hear Robert Plant’s lagged vocals on the opening track of side two of Led Zeppelin I, cry out to borrowers “Your Time is Gonna Come!” as they contemplate refinancing at higher rates and seeing their interest expense rise.

Major Shift

Confronting a reality of higher, not lower interest rates is a major shift in the operating environment compared to the last 40 years (and well articulated by Howard Marks’ memos about a “Sea Change”.)

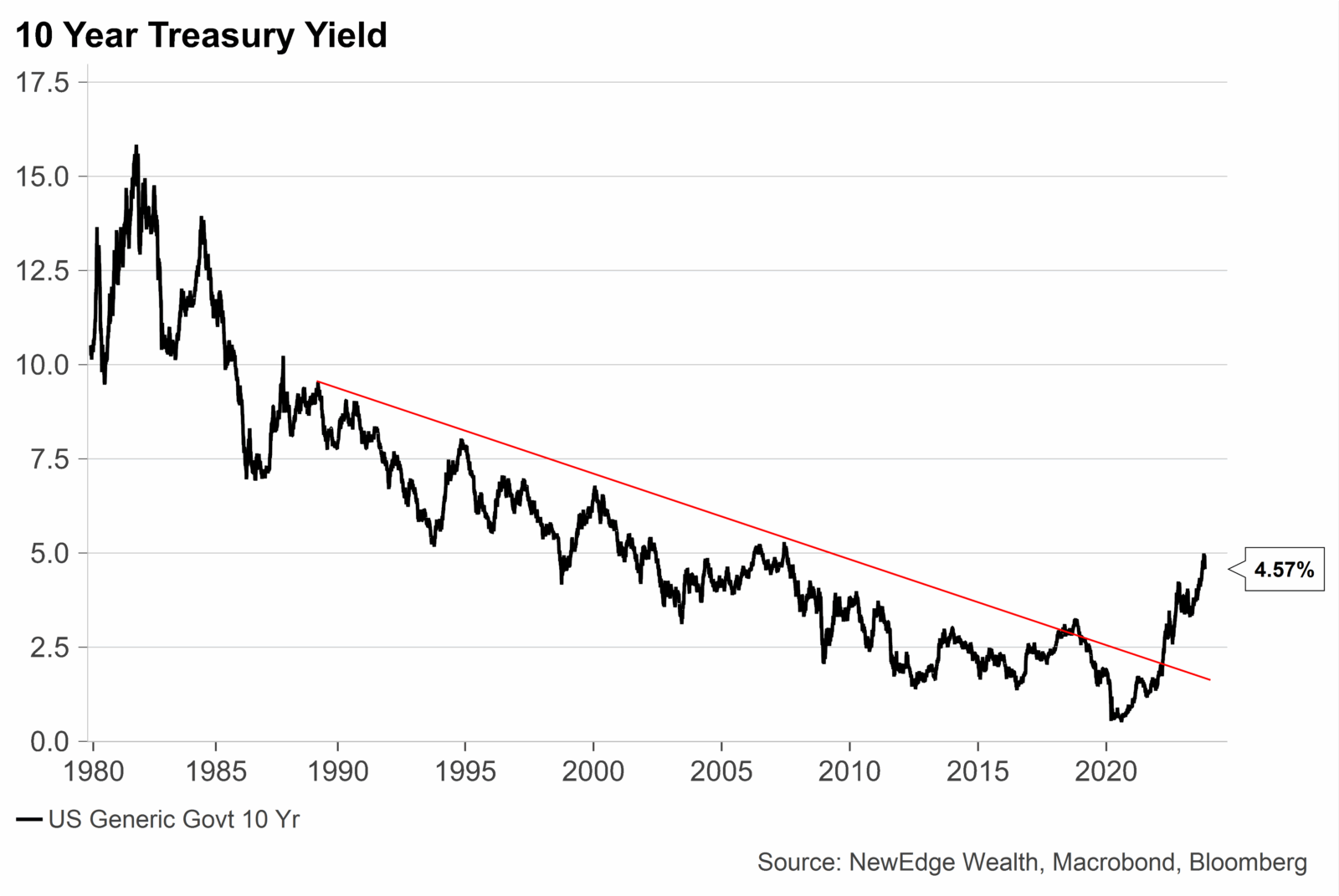

The 40-year slide in long-term interest rates running from 1982 to 2022 resulted in a powerful tailwind for borrowers, as each time a borrower went to refinance debt, there was a high likelihood that interest rates would be lower than the prior time they borrowed.

In fact, that likelihood of lower rates was not just high, it was near-certain: looking at monthly 10-year yields over the last 40 years and measuring 7 year rolling periods (7 years is about the average maturity of corporate bonds), 90% of the time interest rates were lower after 7 years than when they began1. This allowed borrowers to save on interest expenses over time and take on increasing amounts of debt, fueling the success of leveraged strategies.

We cannot know with certainty the future path of interest rates, but based on technical trends alone, the long, fortuitous chute lower for interest rates does appear to have ended. This is not to say that yields will not fall in the future, they will likely do so in the next period of economic stress and Fed support, however we do not expect the prior trend of lower highs and lower lows to continue (recall the 10-year hit a low of just 0.5% in the summer of 2020!).

Refinancing Needs

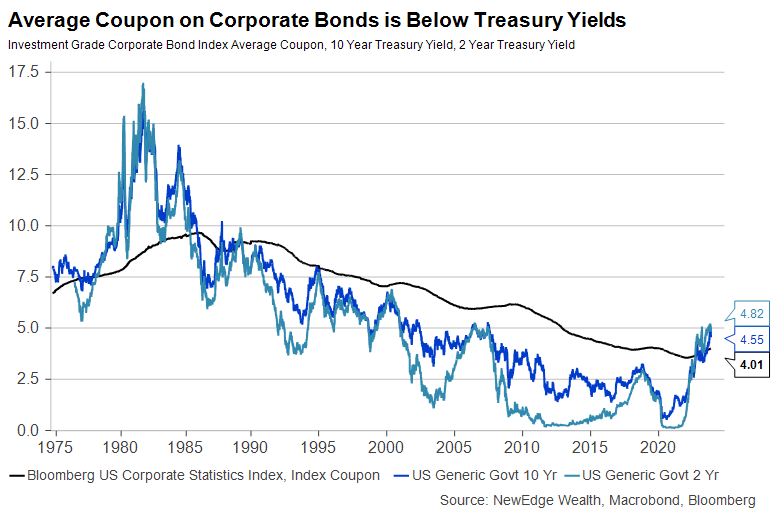

As corporations confront this potential major shift in the path of interest rates, the near-certainty that rates will be ever-lower on future refinancing has been shattered.

Notably, the average coupon on the Bloomberg investment grade corporate bond index is 4.01%, meaning this coupon is now below the entirety of the U.S. Treasury yield curve for the first time since the mid-1980s. This implies a sharp step up in interest expense for debt that needs to be refinanced in the coming years, as long as interest rates remain in their recent range.

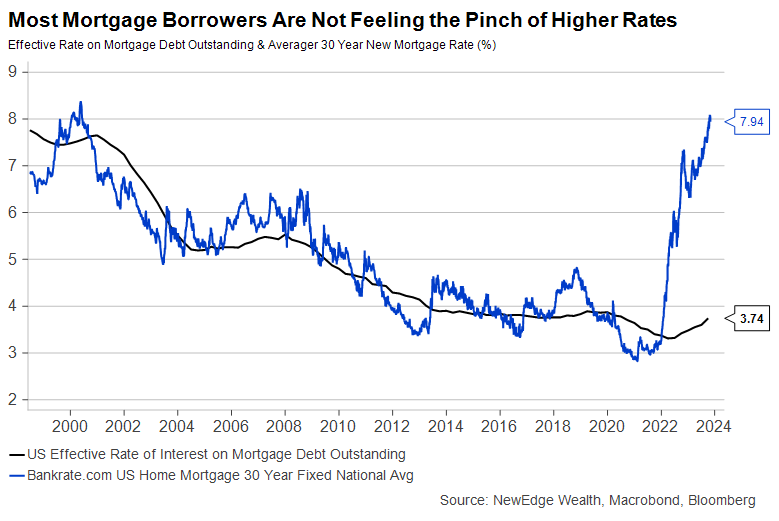

The good news is that for many borrowers, the realization of higher interest rates has been delayed thanks to ultra-low rate period of 2020-2021.

According to the Federal Reserve Bank of New York, about one-third of mortgages were refinanced in 2020-2021, locking in historically low rates, and, in combination with low usage of adjustable rate mortgages, has resulted in a record spread between the prevailing rate for a new mortgage and the effective rate for existing mortgages.

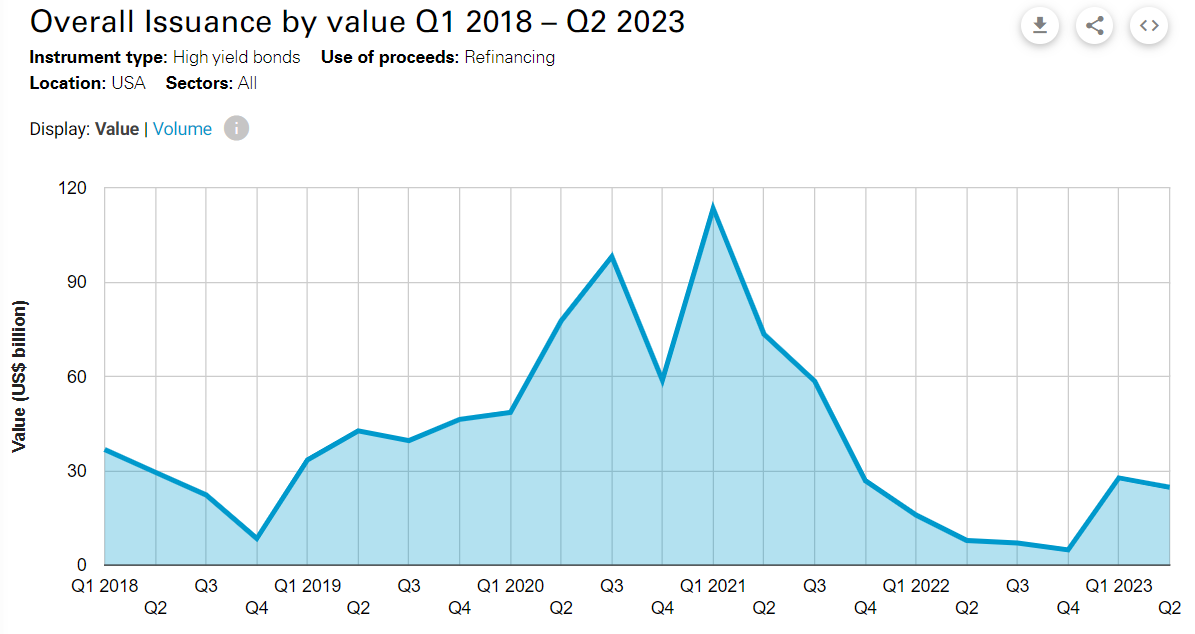

For corporates, a similar dynamic occurred in 2020 and 2021, when companies utilized low rates to refinance debt. Using data from White & Case, refinancing was a whopping 65% of all high yield issuance over the course of 2020 and 2021 ($551B of the $858B total in those two years).

High Yield Bonds Issued for Refinancing (White & Case)

Goldman Sachs estimates that over the next two years, the U.S. investment grade and corporate bond market will have to refinance ~16% of its debt, down from 20% in 2020 and over 25% prior to 2008 (showing the impact of QE suppressing long term interest rates that enable borrowers to use longer maturity debt). This debt is likely to be refinanced at higher rates, as shown above, with Treasury yields higher than current average coupons, which Goldman argues will present a drag on both corporate capex and hiring.

It must be noted that companies with low or long maturity debt and high cash balances have, in some cases, actually benefited from higher interest rates as cash/short term yields have boosted interest income but have not yet been offset by higher interest costs. A similar dynamic has occurred for some lucky households with high cash balances generating income that is not being fully offset by higher debt costs thanks to locked-in low interest rate mortgages.

(For those that would like to dive in to the details of refinancing, this Schroder’s report and this S&P Global report, requires free registration, are helpful).

Balance Sheets in Late Cycle

Even with a smaller maturity wall to digest thanks to 2020 and 2021 refinancing, it is important to note that not all balance sheets are created equal, with some borrowers facing much larger financing needs in the near term, and others with a larger burden of floating rate debt, which has already become much more expensive in today’s high-rate environment.

According to S&P Global, about 17% of global investment grade borrowers’ debt is floating rate, but a significant 50% of speculative grade borrower’s debt is floating rate.

This dynamic is also seen when comparing large and small companies, with 30% of the Russell 2000’s debt outstanding being floating rate, compared to just 6% for the S&P 500 (FT article citing Goldman Sachs data). This debt cost pressure explains a great deal of small caps’ underperformance in 2023 (trailing the S&P 500 by ~13%) but has been well appreciated by markets for some time.

This raises an important assertion: balance sheets matter the most when an economy is late cycle, and can be a key determinant of success, both in profit and stock price, for companies as the business cycle ages.

At the beginning of an economic cycle, the health of balance sheets is secondary to the expected growth in income statement profit. At this early stage, liquidity is free flowing, and interest rates are relatively low-to-moderate, allowing investors to deprioritize balance sheet health. In fact, the equity of low-quality companies with weak balance sheets often outperforms at the beginning of cycles, as near-death companies get “bailed out” by policy support and they live to fight another day.

But as interest rates rise, liquidity becomes more scare, and policy turns to be a headwind, classic characteristics of being late cycle, balance sheets begin to matter a lot more.

We think with low unemployment and tight monetary policy that we are in a late cycle economy (that can stay late cycle for some time as experienced in 2023!), meaning we must remain vigilant about the health of balance sheets in equity investing. Monitoring balance sheets is a key component of identifying Quality companies, as outlined by our Jay Peters in his recent piece on investing in Quality equities through cycles.

Conclusion

Overall, Rolling Stone was wrong about Led Zeppelin I.

In addition, we anticipate that eventually the lagged effect of the Fed’s tightening and the higher rate environment will have an impact on the real economy. We think it is taking longer this cycle than prior cycles due to refinancing and terming out dynamics made possible by record Fed intervention in bond markets in recent years. Just because the refinancing has not “bit” companies yet with higher interest rates does not mean that we should grow complacent about how we view eventual risks to company financials and the economy from higher rates. There are many strong, high quality U.S. companies that can thrive even in this higher rate and uncertain environment, while at the same time, there are lower quality companies that are likely to see their balance sheets become an increasing headwind and constraint. Looking longer term, the potential major shift in the path of interest rates could have broad consequences for business models that benefited from the persistent slide lower in interest rates over the last 40 years.

Top Points of the Week

By Austin Capasso and Ben Lope

1. Equities in the Green This Week, but Down for Month of October –US equities finished in the red for the month of October with weaknesses in a lot of areas. The 200-day moving average was broken, market breadth is at its lowest in a year, extremely tight financial conditions, and the lowest investor sentiment in a year. However, this has been a strong week for USequities. A resilient US economy showed goldilocks data where we saw employment costs slow and wage costs move lower which resulted in better productivity.

2. Volatile Time for Rates – Yields of US Treasuries ended the week lower after the initial jobless claims came in 20,000 jobs lower than the estimate and the unemployment rate inched up. The 30-year Treasury yield finished with the biggest weekly drop since March 2020. We will continue to monitor the labor market for any implications within rates and the broader ecosystem.

3. US October Payrolls Show Weakness – The widely anticipated US payroll data released this morning came in less than expected. US payrolls increased by 150k against the 170k estimate which was a sharp decline from the gain of 297k in September. The unemployment rate rose slightly from last month to 3.9%, which is the highest level since January 2022. Manufacturing posted a decline in employment that was predicted by investors given the ongoing United Auto Workers strike. The strength and resiliency of the economy was reflected by continued job creation in leisure, hospitality, and construction sectors.

4. Fed Keeps Interest Rates Unchanged – Jerome Powell and the Fed left interest rates unchanged at the latest FOMC meeting. This marks the second consecutive month that rates have been left unchanged, following a sequence of 11 straight monthly rate hikes. The Fed also decided to hold the target range on the Fed Funds Rate to 5.25%-5.50%, which has been intact since July. The combined probability of a rate hike over future FOMC meetings in December and January has whittled down from over 40% to just 15%, with a 10% chance of a rate hike in December. The Fed remains patient and continues to assess incoming economic data.

5. ISM Manufacturing PMI Struggles – US ISM manufacturing Purchasing Manager’ Index (PMI) saw a sizeable contraction in October despite showing signs of improvement in months prior. Manufacturing PMI stayed in contractionary territory after dropping to 46.7 in October from 49.0 in September, which was the highest reading since November 2022. New order and employment both slumped because of the United Auto Workers union strike. This marks the 12th consecutive month the reading has stayed in contractionary territory (reading below 50.0) and the longest stretch since the 2007-2009 Great Financial Crisis.

6. Updates in Europe: BoE Rate Decision & Eurozone GDP – The Bank of England (BoE) left rates unchanged in their latest policy meeting, using similar language seen from the Fed. The BoE plan on remaining patient to assess incoming economic data with hopes that the market will do the tightening for them. Third quarter GDP in the Eurozone (spans 20 countries that use the Euro as main currency) showed slowing after a -0.1% contraction. Germany, Europe’s largest economy, was especially weak in particular. The ongoing growth concerns in Europe continue.

7. Details of This quarter’s Treasury Refunding Plan – Rapidly increases in rates made this quarter’s Treasury refunding announcement more anticipated than past instances. The Treasury said it will slow the pace of increases in its longer-dated debt auctions in the November 2023 and January 2024 quarters and expects it will need one more additional quarter of increases after this announcement to meet its financing needs. The Treasury plans to sell $112 billion in its quarterly refunding next week, which will raise $9.8 billion in new cash and refund $102.2 billion in securities. The make-up will include $48 billion of 3-year notes, $40 billion of 10-year notes, and $24 billion of 30-year bonds. Treasury yields fell after the announcement.

8. Apple Earnings – Technology giant Apple reported earnings this morning. Despite meeting expectations of Wall Street on both the top and bottom lines, the stock is down today after the company provided cautious guidance going forward. Apple’s top line growth continues to be the missing piece after the company reported a fourth straight quarter of a decline in sales. Returns on invested capital for the company are among the highest in the world at 53%, which continues to be a bright spot.

9. The Week Ahead – Next week comes with an abundance of Fed Speak, with speeches from Fed members Powell, Waller, Cook and Jefferson. We will also get a look into the US trade deficit, consumer credit and wholesale inventories. This week’s earnings are somewhat quiet, but the marquee announcement will come from Disney whose stock price has seen its ups and downs from July through September.

SOURCES

1 NewEdge Wealth calculations on Bloomberg data

IMPORTANT DISCLOSURES

Abbreviations/Definitions: Cook: Lisa D. Cook, member of the Federal Reserve Board of Governors; FOMC: Federal Open Market Committee; ISM Manufacturing PMI: Institute for Supply Management Purchasing Managers Index; Jefferson: Phillip Jefferson, a member of the Federal Reserve Board of Governors; Quantitative easing (QE): refers to the Fed buying assets to lower longer-term interest rates; Powell: Jerome Powell, Chair of the Board of Governors of the Federal Reserve System; PMI: Purchasing Managers’ Index; Waller: Christopher Waller, member of the Federal Reserve Board of Governors.

Index Information: All returns represent total return for stated period. S&P 500 is a total return index that reflects both changes in the prices of stocks in the S&P 500 Index as well as the reinvestment of the dividend income from its underlying stocks. Dow Jones Industrial Average (DJ Industrial Average) is a price-weighted average of 30 actively traded blue-chip stocks trading New York Stock Exchange and Nasdaq. The NASDAQ Composite Index measures all NASDAQ domestic and international based common type stocks listed on the Nasdaq Stock Market. Russell 2000 is an index that measures the performance of the small-cap segment of the U.S. equity universe. MSCI International Developed measures equity market performance of large, developed markets not including the U.S. MSCI Emerging Markets (MSCI Emerging Mkts) measures equity market performance of emerging markets. Russell 1000 Growth Index measures the performance of the large- cap growth segment of the US equity universe. It includes those Russell 1000 companies with relatively higher price-to-book ratios, higher I/B/E/S forecast medium term (2 year) growth and higher sales per share historical growth (5 years). The Russell 1000 Value Index measures the performance of the large cap value segment of the US equity universe. It includes those Russell 1000 companies with relatively lower price-to-book ratios, lower I/B/E/S forecast medium term (2 year) growth and lower sales per share historical growth (5 years). The BBB IG Spread is the Bloomberg Baa Corporate Index that measures the spread of BBB/Baa U.S. corporate bond yields over Treasuries. The HY OAS is the High Yield Option Adjusted Spread index measuring the spread of high yield bonds over Treasuries.

Sector Returns: Sectors are based on the GICS methodology. Returns are cumulative total return for stated period, including reinvestment of dividends.

The views and opinions included in these materials belong to their author and do not necessarily reflect the views and opinions of NewEdge Capital Group, LLC.

This information is general in nature and has been prepared solely for informational and educational purposes and does not constitute an offer or a recommendation to buy or sell any particular security or to adopt any specific investment strategy.

NewEdge and its affiliates do not render advice on legal, tax and/or tax accounting matters. You should consult your personal tax and/or legal advisor to learn about any potential tax or other implications that may result from acting on a particular recommendation.

The trademarks and service marks contained herein are the property of their respective owners. Unless otherwise specifically indicated, all information with respect to any third party not affiliated with NewEdge has been provided by, and is the sole responsibility of, such third party and has not been independently verified by NewEdge, its affiliates or any other independent third party. No representation is given with respect to its accuracy or completeness, and such information and opinions may change without notice.

Investing involves risk, including possible loss of principal. Past performance is no guarantee of future results.

Any forward-looking statements or forecasts are based on assumptions and actual results are expected to vary from any such statements or forecasts. No assurance can be given that investment objectives or target returns will be achieved. Future returns may be higher or lower than the estimates presented herein.

An investment cannot be made directly in an index. Indices are unmanaged and have no fees or expenses. You can obtain information about many indices online at a variety of sources including: https://www.sec.gov/answers/indices.htm.

All data is subject to change without notice.

© 2026 NewEdge Capital Group, LLC