You Only Live Twice or so it seems,

One life for yourself and one for your dreams.

You drift through the years and life seems tame,

Till one dream appears and love is its name.

– “You Only Live Twice”, Nancy Sinatra, theme from 007: You Only Live Twice

The 2023 U.S. economy has been quite Bond-like in its resilience.

Like Agent 007, the U.S. economy has defied expectations for its demise (Powell warning of economic “pain” due to the Fed’s fight against inflation was like Goldfinger quipping “No, Mr. Bond, I expect you to die!”). Even more like 007, the U.S. economy has emerged from perilous close calls, like the regional bank crisis, with surprising strength.

2023’s string of stronger-than-expected economic data, continued with this week’s jobs data, has reminded us of the iconic 1967 scene in You Only Live Twice where a pronounced-dead Bond emerges from the depths of the ocean alive, well, and immaculately dressed.

We have written extensively about this “twice life”, or resilience, of the U.S. economy and its sources throughout 2023 (February’s No Land Before Time, June’s Party in the U.S.A., July’s You Can’t Stop the Beat, September’s Everybody’s Working for the Weekend), with expectations that forecasts for economic growth would need to be revised higher to reflect this strength.

But just as Bond is always looking over his shoulder for assailants (both violent and romantic), we are constantly on the watch for indications that the path of economic data could change in the future.

It is often said that one of the greatest failings of economic forecasts, and there are many, is that these forecasts are least accurate at turning points. Economic forecasts often have an underlying assumption that what has recently occurred will continue to occur, which is why expectations for soft landings after tightening cycles are often at their highest right before hard landing recessions (helpful WSJ article here).

We continue to see signs of resilience and even pockets of reacceleration in the U.S. economy, like the improvement in manufacturing data with the ISM Purchasing Manufacturers Index and strong jobs data this week, but also are starting to collect more, conflicting, signals that the impact of higher rates, and tighter policy/liquidity/financial conditions are starting to bite into the real economy.

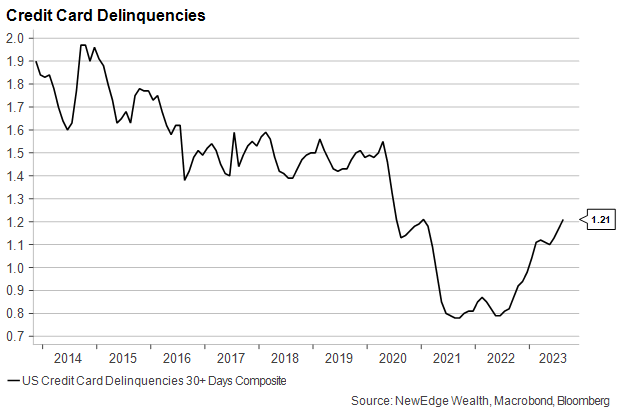

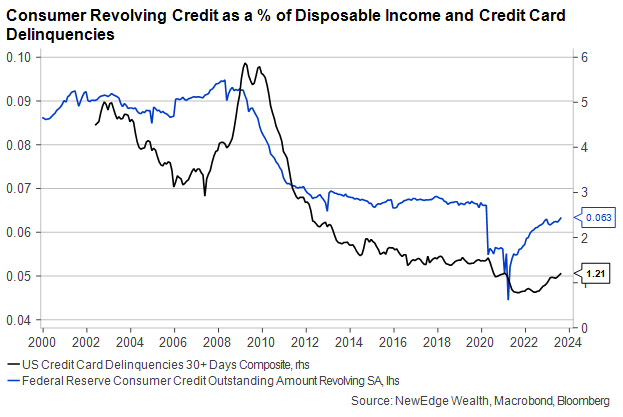

For the consumer, we observe that default rates for credit cards have started to move up rapidly, despite the tight labor market and wage gains.

Perspective is needed, however, as these default rates, though above 2022 levels, remain well below levels seen leading up to and during the Great Financial Crisis (GFC) and even pre-COVID, though the speed of their ascent is notable. Also note the overall usage of revolving credit as a percentage of income is far lower than it was prior to the GFC, illustrating how much healthier consumer balances are today.

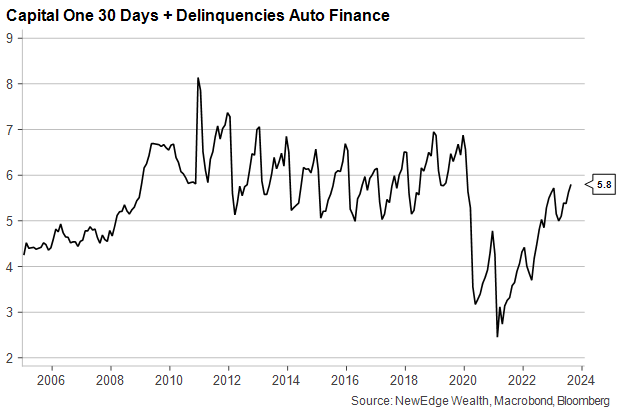

There are also signs of stress for lower income and sub-prime borrowers. There have been multiple sub-prime auto lenders and used car dealers declare bankruptcy in 2023, as more consumers struggle to make swelling auto loan payments given both higher rates and higher car prices (this Bloomberg article outlines stress within auto-loan backed bonds, while many with scars from the GFC remember it was the sub-prime mortgage lenders going bankrupt that served as the canary in the coal mine of the housing crisis).

Like credit card delinquencies, auto loan delinquencies are rapidly rising but only now back to pre-pandemic levels, as shown in the Capital One Auto Financing Delinquencies below.

We can also see renewed stress in areas like low-end and rental furniture, a proxy for the health of low-credit-quality consumer health. Below we show the deteriorating stock price performance of two furniture leasing companies, Aaron’s and Upbond.

Aaron’s Co (AAN) Absolute (Top) and Relative to the S&P 500 (Bottom)

Upbound Group (UPBD) Absolute (Top) and Relative to the S&P 500 (Bottom)

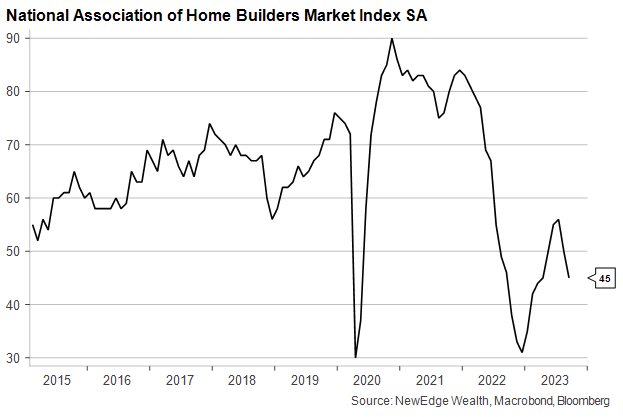

Relatedly, we have recently seen renewed weakness in homebuilder confidence, as high mortgage rates begin to slow housing demand and activity again.

Beyond the consumer, we are also watching for signs of corporate stress given the backdrop of higher rates that will eventually bite as borrowers need to refinance.

As we wrote about in the “You Can’t Stop the Beat” piece above, many corporate borrowers have the luxury of not having to refinance immediately, after extending the duration of their borrowings during the low-rate world of 2020 and 2021. However, for those that do need to refinance debt, the pinch of higher rates is acute.

Just this week, Bloomberg reported that Brookfield Property is at risk of being cut to junk as it faces the need to refinance debt at much higher rates, on top of much lower asset values, while the New York Times reported that WeWork skipped interest payments in hopes to spark a restructuring of its mountain of debt. This kind of story will likely become more common the longer rates remain elevated, as borrowers who were hoping for a swift return to a low-rate world face the reality of “higher for longer” rates.

We also will likely continue to see a wide bifurcation of experience for those with strong balance sheets made up of longer duration, low-cost debt, and those with weak balance sheets that have floating rate debt, near term refinancing needs, and/or large overall debt levels. This bifurcation is a great reminder as to why a quality focus for investing is so valuable at this stage of the economic cycle (read Jay Peters’ white paper on Quality Investing at NewEdge here).

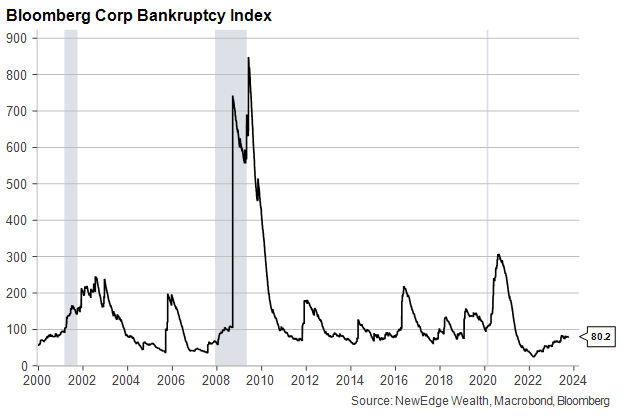

We will continue to watch bankruptcy filings for signs of stress. These filings are creeping higher, but note this is typically a lagging indicator, with an uptick in bankruptcies not always coincident with a recession (like in 2011 or 2016).

Overall, the “assailants” listed above are just a few examples of what we monitor closely. None of these measures alone are enough to call for the imminent demise of the U.S. economy’s Bond-like resilience. However, we will remain vigilant, watching for signs of a change or deterioration within the U.S. economy.

Top Points of the Week

By Austin Capasso and Ben Lope

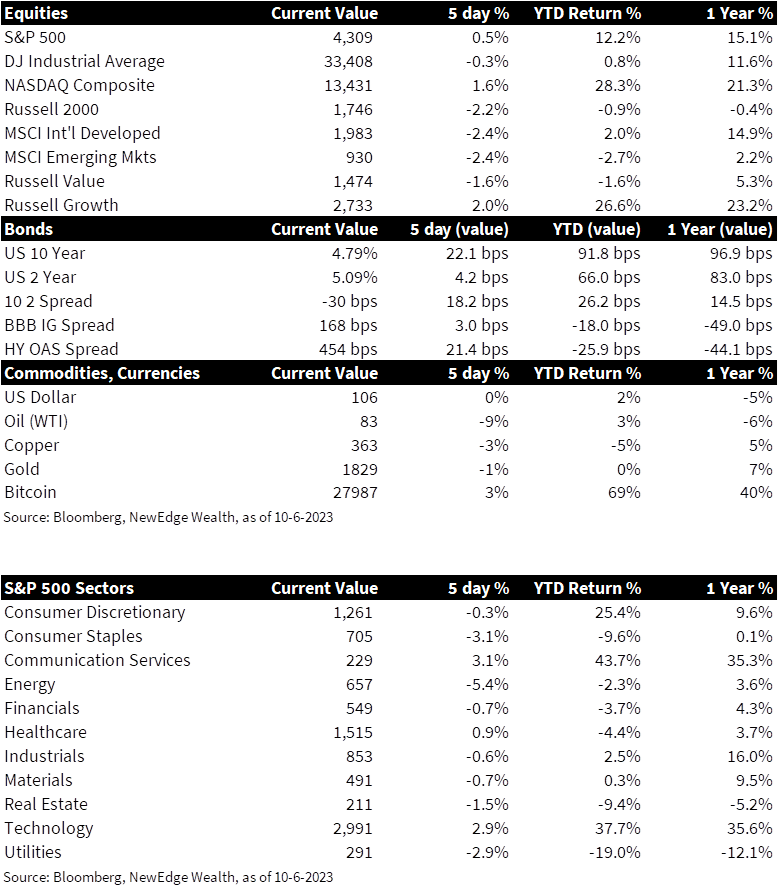

1. Equity markets climb after jobs report – Aside from the DOW Jones Index, the other major indices turned positive after investors digested today’s jobs report. Equities were initially down on the day, being that the jobs report showed strength, and quickly reversed back into the green with 10 of 11 sectors seeing positive returns for the week (consumer staples was in the red) after investors saw the gains may have been distorted by seasonal adjustments and that wage growth was actually modest.

2. US 10-year yield hits record highs – After the equity market sell off on Tuesday, the US 10-year yield saw its highest level since 2007 at 4.80%. The US 30-year yield also saw its highest level since 2007 after hitting 4.924% the same day. Prominent investors, like PIMCO’s Bill Gross, see the potential for the 10-year yield to shoot even higher in the short term, possibly reaching 5% and above. The big debate amongst investors, and something we continue to assess, is when to add duration into portfolios.

3. September jobs report shows upside surprise to nonfarm payrolls – Nonfarm payrolls saw a big upside surprise in the September jobs report today. The 336k increase, well above the 170k forecast, indicates a resilient US economy, which is contradictory to what the Fed wants to see. The unemployment rate came in at 3.8% versus the expected 3.7%. Average hourly earnings rose 0.2% for the month and 4.2% from a year ago, compared to respective estimates for 0.3% and 4.3%. After the report came out, the probability of a Fed rate hike in the December FOMC meeting rose above 50%, indicating that the Fed will likely hike once more this year.

4. US government averts shutdown, McCarthy ousted – After a deadline of September 30, the US was able to pass legislation that helped the government avoid a shutdown. President Biden signed a stopgap spending bill to fund federal agencies for 45 days just hours before the midnight deadline. Despite striking a deal, Kevin McCarthy was later voted out of his position of Speaker of the House in a move led by Florida congressman Matt Gaetz, who accused McCarthy of making a side deal with President Biden on Ukraine aid. The House of Representatives are expected to hold an election to replace McCarthy next week.

5. Fed member Bostic speaks out on current Fed policy – Raphael Bostic, CEO and President of Atlanta Fed, spoke on the current stance of the Fed. He believes the Fed is sufficiently restrictive to where it can hold interest rates and watch incoming economic data, although one more hike in 2023 is likely. The main idea here is that the Fed will be in a “higher for longer” stance for some time. Bostic sees the Fed implementing one rate cut towards the end of 2024. He also deemed it important to see how yields react to tighter conditions.

6. ISM Report shows strength in service sector, improving trend in manufacturing – On Monday, the Institute for Supply Management (ISM) released manufacturing September PMI data that showed improving trends in domestic manufacturing, as the monthly reading remained in contractionary territory for the eleventh straight month, but jumped 1.4 points month-over-month to a reading of 49. Manufacturing’s decline has coincided with continued expansion in the service sector, as evidenced by the ISM’s release of September non-manufacturing PMI data on Wednesday, which showed a healthy reading of 53.6. The readings speak to the broader consumer spending shift from goods to services following the end of pandemic protocols and an increase in interest rates.

7. Strong Fed JOLTS report spooks equity markets, pushes yields higher – The Labor Department’s release of August Job Openings and Labor Turnover Survey (JOLTS) data revealed that after falling for three consecutive months, job openings increased in July. The month over month increase from 8.9 million job openings to 9.6 million job openings caused equity markets to move lower and yields to move higher, as investors likely view the increased availability of jobs as another factor bolstering US economic resilience, which could lead the Fed to increase the federal funds rate yet again.

8. PMI in China shows improvement – China’s official manufacturing PMI measure sector tipped into expansionary territory in August with a reading of 50.2. A reading above 50 indicates expansion, while a reading below 50 indicates contraction. China’s Manufacturing PMI originally dipped into contractionary territory in April, bottomed in March at 48.8, and has since slowly risen to August’s expansionary level amid constant narratives of stagnation for the world’s second largest economy. Chinese officials hope that this reading signals economic momentum that could allow the nation to meet the lofty GDP targets set by officials.

9. Eurozone PMI still in contraction – Europe’smanufacturing sector slid slightly deeper into contractionary territory in September, according to a PMI index compiled by S&P Global. The September reading of 43.4 was slightly lower than August’s reading of 43.5 and sits near the lowest levels for the index since the eurozone manufacturing sector entered contractionary territory in mid-2022. The continued slowdown in the manufacturing sector could motivate the ECB to pause rate hikes following the decision to enact a tenth consecutive hike last month.

10. Incoming data next week – Monday is Columbus Day, where the bond market will be closed while the equity market remains open for normal trading hours. The BLS will release September PPI and CPI data on Wednesday and Thursday, respectively, which will provide signals on the effectiveness of the Fed’s ongoing efforts to tamp down inflation.

IMPORTANT DISCLOSURES

Abbreviations/Definitions: BLS: the Bureau of Labor Statistics is a unit of the United States Department of Labor that is the principal fact-finding agency for the U.S. government in the broad field of labor economics and statistics and serves as a principal agency of the U.S. Federal Statistical System; Bostic: Raphael Bostic, President of the Federal Reserve Bank of Atlanta; Caixin China General Manufacturing PMI: one of the first available indicators every month of the strength of the Chinese economy and is based on data compiled from monthly replies to questionnaires sent to purchasing executives in over 500 manufacturing companies; CPI: Consumer Price Index; ECB: European Central Bank; FOMC: Federal Open Market Committee; GFC: great financial crisis; ISM Manufacturing PMI: Institute for Supply Management Purchasing Managers Index; ISM Services PMI: The Institute of Supply Management (ISM) services PMI (formerly known as Non-Manufacturing Index) is an economic index based on surveys of more than 400 non-manufacturing (or services) firms’ purchasing and supply executives; JOLTS: Job Openings and Labor Turnover Survey; Powell: Jerome Powell, Chair of the Board of Governors of the Federal Reserve System; PPI: Producer Price Index.

Index Information: All returns represent total return for stated period. S&P 500 is a total return index that reflects both changes in the prices of stocks in the S&P 500 Index as well as the reinvestment of the dividend income from its underlying stocks. Dow Jones Industrial Average (DJ Industrial Average) is a price-weighted average of 30 actively traded blue-chip stocks trading New York Stock Exchange and Nasdaq. The NASDAQ Composite Index measures all NASDAQ domestic and international based common type stocks listed on the Nasdaq Stock Market. Russell 2000 is an index that measures the performance of the small-cap segment of the U.S. equity universe. MSCI International Developed measures equity market performance of large, developed markets not including the U.S. MSCI Emerging Markets (MSCI Emerging Mkts) measures equity market performance of emerging markets. Russell 1000 Growth Index measures the performance of the large- cap growth segment of the US equity universe. It includes those Russell 1000 companies with relatively higher price-to-book ratios, higher I/B/E/S forecast medium term (2 year) growth and higher sales per share historical growth (5 years). The Russell 1000 Value Index measures the performance of the large cap value segment of the US equity universe. It includes those Russell 1000 companies with relatively lower price-to-book ratios, lower I/B/E/S forecast medium term (2 year) growth and lower sales per share historical growth (5 years). The BBB IG Spread is the Bloomberg Baa Corporate Index that measures the spread of BBB/Baa U.S. corporate bond yields over Treasuries. The HY OAS is the High Yield Option Adjusted Spread index measuring the spread of high yield bonds over Treasuries.

Sector Returns: Sectors are based on the GICS methodology. Returns are cumulative total return for stated period, including reinvestment of dividends.

The views and opinions included in these materials belong to their author and do not necessarily reflect the views and opinions of NewEdge Capital Group, LLC.

This information is general in nature and has been prepared solely for informational and educational purposes and does not constitute an offer or a recommendation to buy or sell any particular security or to adopt any specific investment strategy.

NewEdge and its affiliates do not render advice on legal, tax and/or tax accounting matters. You should consult your personal tax and/or legal advisor to learn about any potential tax or other implications that may result from acting on a particular recommendation.

The trademarks and service marks contained herein are the property of their respective owners. Unless otherwise specifically indicated, all information with respect to any third party not affiliated with NewEdge has been provided by, and is the sole responsibility of, such third party and has not been independently verified by NewEdge, its affiliates or any other independent third party. No representation is given with respect to its accuracy or completeness, and such information and opinions may change without notice.

Investing involves risk, including possible loss of principal. Past performance is no guarantee of future results.

Any forward-looking statements or forecasts are based on assumptions and actual results are expected to vary from any such statements or forecasts. No assurance can be given that investment objectives or target returns will be achieved. Future returns may be higher or lower than the estimates presented herein.

An investment cannot be made directly in an index. Indices are unmanaged and have no fees or expenses. You can obtain information about many indices online at a variety of sources including: https://www.sec.gov/answers/indices.htm.

All data is subject to change without notice.

© 2026 NewEdge Capital Group, LLC