If you want to destroy my sweater (whoa, whoa, whoa, whoa)

Hold this thread as I walk away (as I walk away)

Watch me unravel

“Undone (The Sweater Song)” – Weezer

“Undone (The Sweater Song)” may be the first Weezer song that Rivers Cuomo wrote, but it is also the most appropriate Weezer song for today’s macro and market environment.

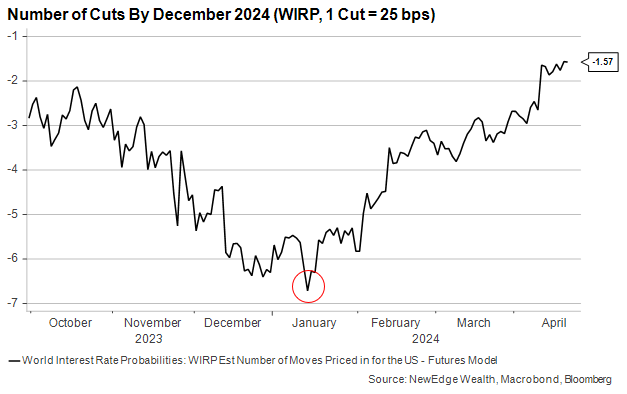

Expectations for a Fed pivot to rate cuts in 2024 have been “undone” by stickier inflation readings and resilient economic growth statistics, resulting in an “unraveling” of market trades that expected to benefit from a friendlier Fed.

The Undoing of Rate Cut Expectations

We are not surprised to see this undoing of rate cut expectations, as we thought the bond market’s pricing of a peak 6.5 cuts for 2024 was far too aggressive given our expectations for growth and inflation.

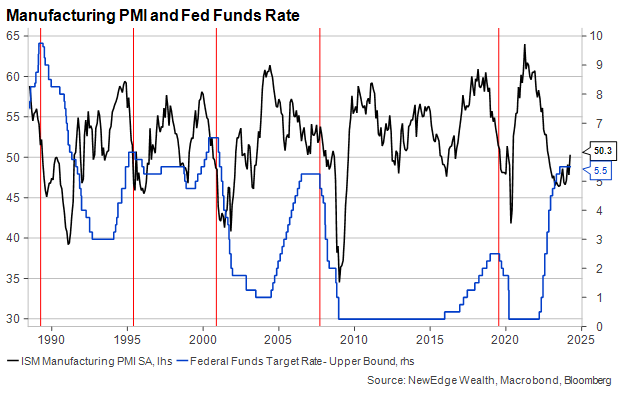

Further, we thought the Fed’s recent discussions of rate cuts were premature and ambitious given the historical backdrop that, in the past 40 years, they have never started a rate cutting cycle when manufacturing Purchasing Managers Indices (PMIs) were accelerating. As we are now seeing a recovery in PMIs, meaning there is the potential for a reacceleration in some cyclical parts of the economy, this would not be historically consistent with a Fed about to embark on a rate cutting cycle.

The Fed was initially eager to look through the inflation stickiness to start the year, considering the hotter readings as “bumps” on the “golden path” to disinflation and still classifying policy rates as “sufficiently restrictive”, with Chairman Powell’s Wayne’s World-like “party on” press conference in March as the fever pitch of this dedication to cutting rates.

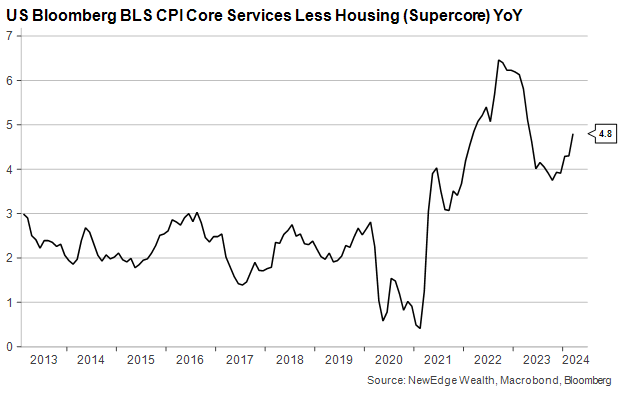

However, since the March CPI data, which showed an unwelcome reacceleration in important measures like Supercore CPI, the Fed’s ambitious tone on starting rate cuts has been reversed materially.

This week, Fed speak still largely classified policy rates as restrictive (this Bloomberg article does a great job in summarizing recent comments), but some members raised questions about whether policy rates were restrictive enough, even mentioning the prospect of further rate hikes (this was the Fed’s Williams who said that this was not his base case). The overall message from the Fed was for fewer rate cuts starting later than previously expected.

The Fed’s “higher for longer” predicament has also revealed a sharp divergence between policy in the U.S. and around the world. While other central banks, both developed and emerging, have begun to cut or have signaled imminent cuts to come, thanks to moderating inflation and/or flagging growth, the Fed is pressed to remain tight.

The relative hawkishness of the Fed is finding its way into currency markets, where the USD has strengthened versus other currencies and sparked discussions that intervention might be needed to stem the sharp weakening in some currencies, such as in Japan, Korea, Vietnam and Mexico.

U.S. Dollar Spot Index (DXY)

At the IMF meetings this week, many participants called out abundant U.S. fiscal policy as driving the relative strength/higher inflation of the U.S. economy and necessitating a tighter Fed.

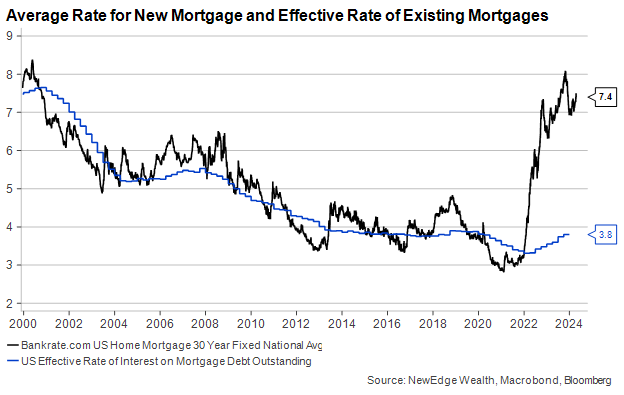

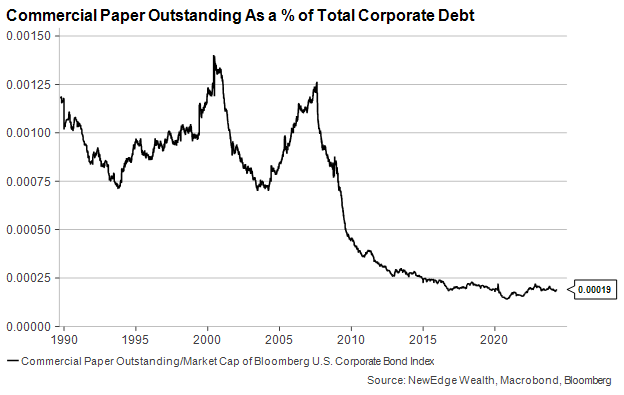

However, stimulative fiscal policy is not the only source the U.S. economy’s resilience in the face of rate cuts. Last year we wrote extensively about why higher short term rates were not having the same impact on economic growth as prior cycles (Nov 23, Jul 23, Feb 23), focusing on how the “long tail of Quantitative Easing” has dulled the impact of rate hikes.

Low long-term rates, along with market structures that allowed borrowers to borrow at these low rates, enabled aggregate U.S. households and corporations to reduce their sensitivity to higher short-term interest rates compared to prior cycles. The following two charts display this dynamic for households (effective mortgage rates vs. rates for new mortgages) and corporations (commercial paper as a % of borrowing).

We can contrast this balance sheet set-up to a market like Europe, where, depending on the country, financing depends more on shorter term bank loans than long-term bonds and mortgages see interest rates reset more frequently than the U.S.’s 30-year fixed rate. In Europe, higher rates have proliferated through the economy in a more rapid way, resulting in a weaker economic growth backdrop and greater justification for interest rate cuts.

But the term aggregate is key when discussing the U.S. economy, because not all borrowers have been able to immunize against higher rates, which brings us beyond the undoing of rate cut bets to the unraveling of Fed-pivot-benefitting asset performance.

Unraveling Pivot Party Trades

Post the 4Q23 spark of the “Pivot Party” (discussed in this November 2023 Weekly Edge), when markets soared on Powell’s opening of the door to rate cuts, assets that could benefit from lower rates began to outperform the market. These included low-quality and more speculative parts of the market that have heavily indebted, and/or floating rate, balance sheets.

Though the overall equity market was able to shrug off higher rates and expectations for a tighter Fed, reaching new highs even as rate cuts were priced out over the course of the first quarter, these lower quality Pivot Party trades have been languishing all year.

The heavily indebted and more unprofitable Russell 2000 Index has seen all its relative outperformance from 4Q23 reverse in 2024, with the index now back to its relative lows from November 2023.

This Russell 2000 small cap index is now oversold on a technical basis (using the Relative Strength Index), setting it up for a potential recovery. It will be telling as to how robustly the index bounces out of this oversold condition. If the rebound is powerful, then it could be a sign of reinvigorated risk appetite and optimism; however if the rebound is tepid, it could be a sign of a continued risk off mood.

Russell 2000 Absolute (top) and Relative to the S&P 500 (bottom)

But the Pivot Party was about more than just balance sheet relief, it was about animal spirits getting reinvigorated, with Initial Public Offering, IPO, activity picking up (the number of IPOs that have been filed is +10% YTD from last year, while the amount of proceeds raised is +326% YTD from last year), and debt issuance increasing, taking advantage of tighter credit spreads as markets rallied. Strong results from the Capital Markets businesses of the large banks in 1Q24 confirmed this activity.

However, as the Pivot Party has faded, with rates rising and the performance of recently IPO’d companies lagging, it will be important to monitor the health of the nascent recovery in animal spirits.

Renaissance IPO ETF (IPO) Absolute (top) and Relative to the S&P 500 (bottom)

These animal spirits and the rate backdrop are important for how companies will plan to invest and raise capital in the coming quarters, as there was a great deal of hope that an easier Fed could give the green light to IPOs, debt raises, M&A, and capital expenditures. This is especially important in the context of a wave of refinancing for high yield borrowers that is expected to build later in 2024 and 2025.

The Music Video: Assessing the Speed of Growth

We find it interesting how rapidly the market narrative has swung from expecting a recession, to no recession, and from 6.5 cuts, to calls for more hikes.

It raises the question if consensus has now become too one-sided in expecting strong growth and a tight Fed to continue in perpetuity.

We are not making the call for an imminent slowdown in U.S. growth, but we are alert to the one-sidedness of the consensus for growth.

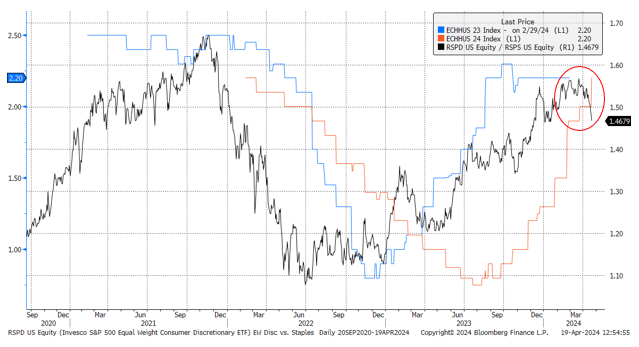

We continue to closely monitor the performance of equal weight Consumer Discretionary vs. Consumer Staples stocks as a sign of both risk appetite and forward expectations for consumer spending growth (which makes up 70% of GDP). We find it very interesting that Discretionary sharply underperformed Staples this week on the back of strong retail sales data and another revision higher to Household Consumption growth in GDP.

Equal Weight Consumer Discretionary vs. Consumer Staples & GDP Household Consumption Bloomberg Consensus Forecasts for 2024 and 2025 Growth

Staying on theme, the music video for Weezer’s “Undone” is also an appropriate representation of today’s growth backdrop, as it uses paradoxical and somewhat disorienting speeds to create a real-time slow motion effect (the band played a sped up version of the song, so when slowed to real-time, it looks as though they are playing in slow motion).

As we outlined in our 2024 Outlook, we expect economic data to be paradoxical and somewhat disorienting, just like the “Undone” video. This makes listening to what the market says about the growth backdrop even more important, as it could help “sniff out” when changes to the growth trajectory are occurring.

Conclusion

The Fed and the market’s expectations for 2024 cuts have clearly been undone and unraveled by stickier inflation and growth data in the U.S. This has sent shockwaves through rates and currency markets, as U.S. strength divergences other countries. We will continue to monitor U.S. inflation and growth data, and what markets are “saying” about this data to gauge if consensus has become too one-sided in its now rosy expectations.

IMPORTANT DISCLOSURES

Abbreviations/Definitions: CPI: Consumer Price Index; GDP: gross domestic product; Quantitative easing (QE): refers to the Fed buying assets to lower longer-term interest rates; Relative Strength Index (RSI): a technical indicator intended to chart the current and historical strength or weakness of a stock or market based on the closing prices of a recent trading period; Supercore CPI: measures core services ex shelter.

The views and opinions included in these materials belong to their author and do not necessarily reflect the views and opinions of NewEdge Capital Group, LLC.

This information is general in nature and has been prepared solely for informational and educational purposes and does not constitute an offer or a recommendation to buy or sell any particular security or to adopt any specific investment strategy.

NewEdge and its affiliates do not render advice on legal, tax and/or tax accounting matters. You should consult your personal tax and/or legal advisor to learn about any potential tax or other implications that may result from acting on a particular recommendation.

The trademarks and service marks contained herein are the property of their respective owners. Unless otherwise specifically indicated, all information with respect to any third party not affiliated with NewEdge has been provided by, and is the sole responsibility of, such third party and has not been independently verified by NewEdge, its affiliates or any other independent third party. No representation is given with respect to its accuracy or completeness, and such information and opinions may change without notice.

Investing involves risk, including possible loss of principal. Past performance is no guarantee of future results.

Any forward-looking statements or forecasts are based on assumptions and actual results are expected to vary from any such statements or forecasts. No assurance can be given that investment objectives or target returns will be achieved. Future returns may be higher or lower than the estimates presented herein.

An investment cannot be made directly in an index. Indices are unmanaged and have no fees or expenses. You can obtain information about many indices online at a variety of sources including: https://www.sec.gov/answers/indices.htm.

All data is subject to change without notice.

© 2026 NewEdge Capital Group, LLC